Rajiv Jain is the Chairman and Chief Investment Officer of GQG Partners, known for his "forward-looking quality" approach to global and emerging market equities. He built his reputation through a contrarian mindset, famously scaling multi-billion-dollar investments into out-of-favor assets like the Adani Group while actively rotating away from consensus technology bubbles. The following insights outline his philosophy on compounding earnings, preserving capital, and adapting to volatile markets.

Part 1: Forward-Looking Quality

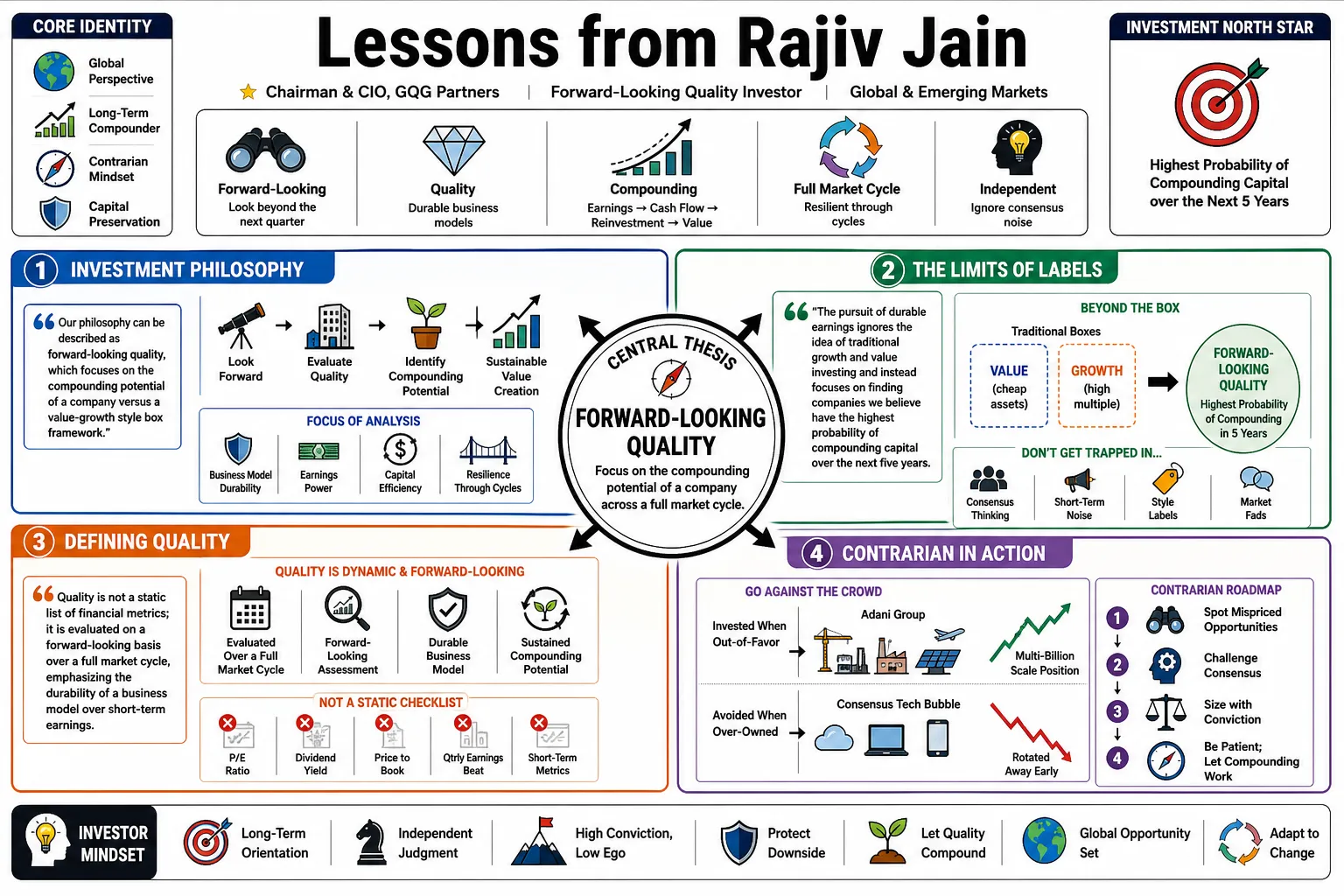

- On Investment Philosophy: "Our philosophy can be described as forward-looking quality, which focuses on the compounding potential of a company versus a value-growth style box framework." — Source: [Bridgehouse]

- On The Limits of Labels: "The pursuit of durable earnings ignores the idea of traditional growth and value investing and instead focuses on finding companies we believe have the highest probability of compounding capital over the next five years." — Source: [GQG Partners]

- On Defining Quality: Quality is not a static list of financial metrics; it is evaluated on a forward-looking basis over a full market cycle, emphasizing the durability of a business model over short-term earnings beats. — Source: [Bridgehouse]

- On Compounding: "A core tenet of our investing philosophy is compounding wealth over time... we're playing the long game." — Source: [Goldman Sachs Asset Management]

- On Valuation vs. Quality: An investment is only viable if a high-quality business with highly visible, durable earnings is available at a reasonable price, avoiding the trap of overpaying for mere growth. — Source: [GQG Partners]

- On Avoiding Traps: Cheaper stocks do not equate to safety; during periods of market stress, prioritizing large, stable companies over cheap assets is a more effective defense mechanism. — Source: [GQG Partners]

- On The Illusion of Static Markets: "From a philosophical perspective, investing is all about changes, not about static. The world is never static. Adapting is key to our ongoing search for quality businesses." — Source: [The Big Picture]

- On Long-Term Orientation: True compounding requires looking beyond quarterly noise and anchoring analysis to the underlying fundamentals over a five-year horizon. — Source: [Bridgehouse]

- On Recognizing Deterioration: "Singapore might be a wonderful place, but if it's deteriorating, that's not... a problem" if you recognize the change and adjust your portfolio accordingly. — Source: [The Big Picture]

- On Style Box Constraints: Rigid adherence to traditional value or growth constraints frequently forces investors to ignore the most durable compounding opportunities in the broader market. — Source: [GQG Partners]

Part 2: Adaptability & Market Dynamics

- On Survival First: "You're not here to make the most money; you're here to survive. If the capital is gone, you're done. You have to make sure you have enough firepower to come back the next day." — Source: [Forbes]

- On Long-Term Survival: "The only way to survive long-term is to be adaptive." — Source: [The Meb Faber Show]

- On Market Timing Risks: "If you're late, the losses are horrendous." — Source: [Morningstar]

- On Recognizing Tops: Market tops are only obvious in hindsight, and no one rings a bell telling you precisely when to exit a concentrated position. — Source: [GQG Partners]

- On Changing Your Mind: A core part of the investment process is the willingness to rapidly change one's mind as market conditions evolve, avoiding rigid adherence to a fading trend. — Source: [The Meb Faber Show]

- On Avoiding Heroics: "This is not the time for heroics. Many other stocks beyond tech will do a perfectly good job of delivering returns at sensible prices." — Source: [GQG Partners]

- On Pivoting Away from AI: Recognizing when a thesis becomes stretched, he reduced exposure to high-flying semiconductor names in favor of more defensive, unloved sectors as the AI boom matured. — Source: [Morningstar]

- On Being Wrong Early: Analysts are actively encouraged to challenge their own investment theses and pivot if new information arises, preferring to be wrong in the conference room rather than in the market. — Source: [Trustnet]

- On Macro Awareness: While investing strictly bottom-up, top-down macro data is utilized as a "risk-off switch" to reduce exposure if challenging environments threaten aggregate corporate earnings. — Source: [Goldman Sachs Asset Management]

- On Flexibility Across Sectors: Being benchmark-agnostic allows the strategy to move seamlessly from technology to energy or emerging markets based on where the strongest compounding opportunities exist. — Source: [Lloyds Bank]

Part 3: Earnings & Fundamental Analysis

- On The Core Driver: The foundational belief driving the strategy is that, ultimately, "earnings drive stock prices" over the long term. — Source: [Bridgehouse]

- On The Research Mosaic: Achieving a competitive edge requires a "Research Mosaic" that seeks an insight advantage rather than just an information advantage, combining traditional analysis with investigative techniques. — Source: [GQG Partners]

- On Non-Traditional Analysts: Employing analysts with backgrounds in investigative journalism and specialized accounting helps uncover deep risks and opportunities consistently missed by standard financial modeling. — Source: [Bridgehouse]

- On Earnings Durability: Finding companies that can generate durable, sustainable earnings in various economic climates is more crucial than chasing hyper-growth at elevated multiples. — Source: [Grokipedia]

- On The AI Profit Margin Problem: Examining the AI infrastructure boom reveals warning signs, particularly regarding the unsustainable profit margins of advanced semiconductor chips and the heavy reliance on debt financing. — Source: [Morningstar]

- On Assessing Moats: Long-term earnings visibility requires a continuous, skeptical reassessment of a company's competitive advantage and its underlying market share dynamics. — Source: [Goldman Sachs Asset Management]

- On Management Quality: Beyond the numbers, rigorous fundamental analysis must evaluate the depth of management and their demonstrated ability to execute consistently across multiple market cycles. — Source: [GQG Partners]

- On Financial Strength: True quality companies exhibit robust balance sheets that protect their fundamental earnings power during periods of economic contraction or sudden credit tightening. — Source: [Bridgehouse]

- On Bottom-Up Focus: While macro trends act as a risk-off switch, the primary driver of portfolio inclusion remains the bottom-up fundamental strength of the individual business. — Source: [RankiaPro]

Part 4: Risk Management & Capital Preservation

- On Risk as the Priority: Risk management is explicitly viewed as the absolute first consideration in the investment process, addressed before evaluating any upside potential. — Source: [Bridgehouse]

- On Absolute Return Mindset: The strategy operates with an absolute return mindset in long-only equities, actively aiming to limit the impact of market crises rather than just matching a benchmark. — Source: [GQG Partners]

- On Losing Less: Protecting capital during downturns is essential; the goal is to "lose less" than the broader market, which provides a significantly better starting point for the subsequent compounding recovery. — Source: [GQG Partners]

- On Quality as Risk Mitigation: Assessing the forward-looking "quality" of a business, including its balance sheet and management depth, operates as the primary tool for managing downside risk. — Source: [Bridgehouse]

- On The Danger of 'Value': Just because a stock is statistically cheap does not mean it is low risk; falling into stubborn value traps is a major threat to long-term capital preservation. — Source: [GQG Partners]

- On Active Risk Reduction: The team is nimble and willing to upgrade the portfolio by actively eliminating risks and rotating into more defensive, stable names during periods of extreme market volatility. — Source: [GQG Partners]

- On Avoiding Speculation: Prioritizing businesses with proven, durable cash flows over speculative companies ensures that the portfolio remains anchored in economic reality during market manias. — Source: [Forbes]

- On Concentration vs. Diversification: While the portfolio is concentrated to maximize returns from high-conviction ideas, risk is managed by ensuring these positions are not heavily correlated to the same underlying macro vulnerabilities. — Source: [Capital Allocators]

- On The Reality of Losses: While it is impossible to avoid all losses during a severe market correction, rigorous downside protection mechanisms dictate the speed at which the portfolio's capital recovers. — Source: [GQG Partners]

Part 5: Portfolio Construction & Sell Discipline

- On The Difficulty of Selling: "There's plenty of evidence that I can tell you with my own experience that buying is easy, selling is where the... trouble starts." — Source: [The Big Picture]

- On Objective Decision-Making: Capital allocation requires strict objectivity; because there are always alternative opportunities, there is zero benefit in stubbornly holding onto a broken position. — Source: [Goldman Sachs Asset Management]

- On Thesis-Driven Exits: A stock is sold immediately when the fundamental view of its risks or opportunities changes, or when the price simply no longer reflects reasonable value. — Source: [Citi]

- On Upgrading Alternatives: Selling is often triggered not by failure, but by the identification of superior, more attractive investment alternatives that offer better long-term compounding potential. — Source: [Citi]

- On Specific Sell Triggers: A meaningful deterioration of long-term earnings growth prospects or a loss of competitive advantage are immediate, non-negotiable triggers for exiting a position. — Source: [Goldman Sachs Asset Management]

- On Technological Disruption: If a company faces severe technology disruption or transformative M&A activity that permanently alters its investment case, the position is swiftly liquidated. — Source: [Goldman Sachs Asset Management]

- On Management Red Flags: Issues with management, particularly a loss of operational control or sudden shifts in corporate governance, warrant an immediate and complete portfolio exit. — Source: [Goldman Sachs Asset Management]

- On Price Discipline: Even the highest quality business will be sold if the market price meaningfully exceeds the team’s internal valuation estimate of its future discounted cash flows. — Source: [GQG Partners]

- On Turnover as a Byproduct: High portfolio turnover is not a deliberate strategy, but rather the natural byproduct of maintaining an unemotional, strictly enforced sell discipline. — Source: [SRP]

Part 6: Contrarian Positioning & Conviction

- On Contrarian Conviction: Generating absolute returns often requires taking large, concentrated positions in out-of-favor sectors, relying heavily on independent fundamental research rather than prevailing market sentiment. — Source: [Forbes]

- On Embracing the Unloved: Sectors like energy, tobacco, and traditional utilities often provide stable, long-term demand and highly durable cash flows exactly when the broader market is chasing technology. — Source: [Capital Allocators]

- On Ignoring the Herd: Investing in heavily criticized regions or companies can yield outsized returns if the underlying asset quality is strong and the market has mispriced the actual structural risks. — Source: [Forbes]

- On The Adani Investment: Stepping in to invest $1.87 billion in Adani Group companies during the depths of the Hindenburg crisis was a calculated bet on the irreplaceable quality of Indian infrastructure assets. — Source: [Straits Times]

- On Separating Noise from Value: The Adani trade highlighted the absolute necessity of separating media controversy and short-term volatility from the long-term cash generation of critical ports and power grids. — Source: [Forbes]

- On Evaluating Founders: When making contrarian bets on family-run conglomerates, heavily weighting the operational track record and entrepreneurial drive of the founder is a critical component of the thesis. — Source: [Adani Group]

- On Scaling Conviction: When a contrarian thesis proves correct and asset quality remains intact, continuing to scale the investment—as seen in the expansion of the Adani holdings to nearly $10 billion—is key to maximizing alpha. — Source: [Alice Blue]

- On The Dot-Com Echoes: Recognizing the parallels between the late-90s tech bubble and the modern AI frenzy requires the conviction to step away from consensus darlings before the structural weaknesses fracture. — Source: [Morningstar]

- On Defying Benchmarks: True active management requires a willingness to look drastically different from the benchmark, accepting periods of relative underperformance in exchange for long-term absolute return generation. — Source: [Morningstar]

- On Independent Thinking: The ability to execute massive contrarian trades stems from a firm structure that deliberately insulates investment decisions from external peer pressure and institutional groupthink. — Source: [GQG Partners]

Part 7: Emerging Markets & The India Thesis

- On The India Growth Story: India represents a unique, structural growth story driven by a combination of favorable demographics, widespread digitalization, and a rapidly expanding credit cycle. — Source: [GQG Partners]

- On Banking as a Proxy: Investing heavily in major Indian private banks and conglomerates serves as an effective, high-quality proxy for capturing the country’s broad economic expansion. — Source: [TIKR]

- On Infrastructure as Destiny: For emerging markets to scale, physical infrastructure is paramount; thus, owning the foundational assets—like ports, power, and transmission—offers highly visible, long-duration earnings. — Source: [Adani Group]

- On Commodity Demand: Targeting resource-rich economies in Latin America allows the portfolio to capture the sustained global demand for energy and materials essential to the broader global transition. — Source: [TIKR]

- On Emerging Market Risks: While emerging markets offer superior growth, they require an intense focus on corporate governance and political stability, utilizing the macro "risk-off switch" when conditions deteriorate. — Source: [Goldman Sachs Asset Management]

- On The Tequila Crisis Lessons: Early career experiences navigating severe emerging market crises solidified the belief that capital preservation must always supersede the aggressive pursuit of yield. — Source: [The Meb Faber Show]

- On Avoiding State-Owned Traps: In emerging economies, distinguishing between dynamic, entrepreneur-led enterprises and inefficient, state-run monopolies is crucial for finding sustainable compounders. — Source: [Bridgehouse]

- On The Reality of Volatility: Emerging market investors must accept higher baseline volatility, but they mitigate this by demanding a significantly higher margin of safety in the underlying asset quality. — Source: [GQG Partners]

- On Global Context: Emerging market investments are never viewed in isolation; they are constantly weighed against the opportunity cost and risk-adjusted returns available in developed markets. — Source: [Capital Allocators]

Part 8: Culture, Alignment & Team Building

- On Skin in the Game: "I strongly believe that a portfolio manager should be invested in their own products because that gives you very good perspective on how they're likely to behave." — Source: [FundCalibre]

- On Client Responsibility: "One must always remember that managing other people's money is a privilege and that privilege comes with great responsibility." — Source: [Bridgehouse]

- On Organizational Structure: A successful investment firm requires a flat structure where honest discussions of ideas and internal criticism are structurally embedded and highly valued. — Source: [GQG Partners]

- On Devil's Advocacy: Encouraging analysts to explicitly take the other side of a high-conviction trade is essential for uncovering hidden risks and breaking down institutional confirmation bias. — Source: [Flagship Asset Management]

- On Aligning Incentives: Having a substantial portion of personal net worth invested alongside clients ensures that the emotional pain of a drawdown is shared, reinforcing the absolute return mindset. — Source: [GQG Partners]

- On Building the Firm: Transitioning from managing massive strategies at Vontobel to founding GQG was driven by the desire to build a culture entirely optimized around the "forward-looking quality" philosophy. — Source: [Forbes]

- On Diverse Perspectives: Bringing together traditional financial analysts and non-traditional investigative researchers creates a culture that prizes deep, differentiated insight over standard industry consensus. — Source: [GQG Partners]

- On The Role of the CIO: A Chief Investment Officer must balance the responsibility of final capital allocation decisions with the necessity of fostering an environment where anyone can challenge the prevailing thesis. — Source: [Capital Allocators]

- On The Ultimate Goal: The architecture of the firm, the structure of the team, and the rigor of the research process all serve a single purpose: to survive the market's worst days and compound wealth over decades. — Source: [The Meb Faber Show]