Lessons from Renaud Laplanche

French-American entrepreneur Renaud Laplanche founded LendingClub and Upgrade, popularizing alternative lending in the US by exploiting the massive interest rate spread between bank depositors and borrowers. This profile collects his insights on consumer finance, scaling startups, and his parallel career as a record-breaking competitive sailor.

Part 1: The Origins of Innovation

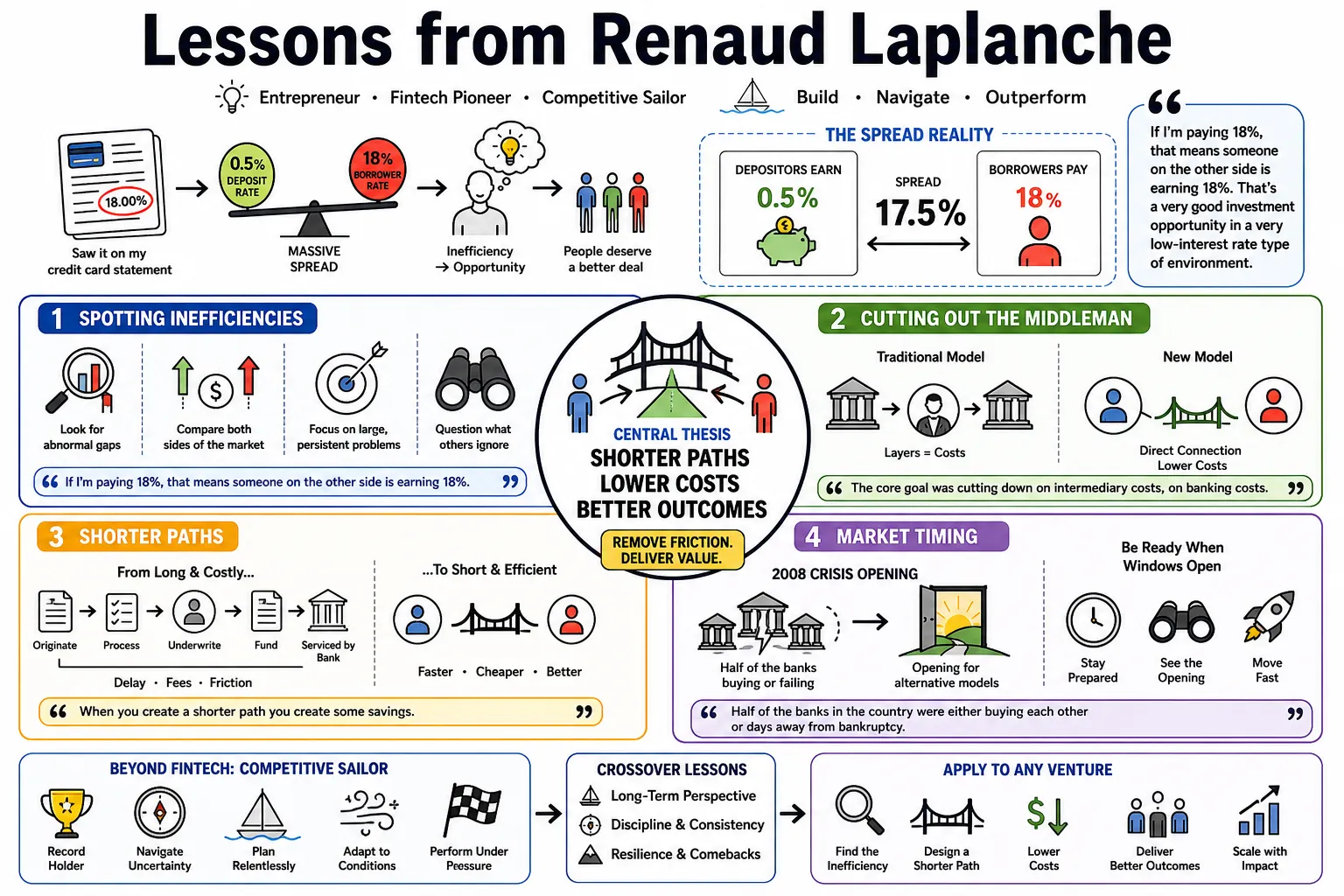

- On Spotting Inefficiencies: "If I'm paying 18%, that means someone on the other side is earning 18%. That's a very good investment opportunity in a very low-interest rate type of environment." — Source: [SEC]

- On the Genesis of LendingClub: The idea started by looking at his own credit card statement and realizing the massive spread between what depositors earned and borrowers paid. — Source: [SEC]

- On Cutting Out the Middleman: The core goal of his early fintech ventures was "cutting down on intermediary costs, on banking costs." — Source: [SEC]

- On Shorter Paths: "When you create a shorter path you create some savings." — Source: [SFGate]

- On Market Timing: Half of the banks in the country were either buying each other or days away from bankruptcy during the 2008 crisis, creating an opening for alternative lending. — Source: [Foundation Capital]

- On Naming Companies: The name "Lending Club" was chosen partly to convey the notion of getting a good deal, similar to Sam's Club. — Source: [Future Nexus]

- On Building During Crises: The financial crisis of 2008 meant the world was falling apart, yet it provided the exact conditions needed for a transparent lending alternative. — Source: [Foundation Capital]

- On Continuous Innovation: "Innovation needs to be part of your culture. Consumers are transforming faster than we are, and if we don't catch up, we're in trouble." — Source: [Fintechly]

- On Meaningful Innovation: "What matters at the end of the day is to continue to innovate, continue to bring new products to consumers that incrementally help either [reduce] costs or deliver better economics." — Source: [Regulation Innovation]

- On Reducing Friction: True financial innovation is ultimately about removing friction in everyday consumer experiences. — Source: [Regulation Innovation]

Part 2: Product Philosophy & Design

- On Creating Value: "At Upgrade, we are really trying to create financial services and products that help consumers move in the right direction." — Source: [Regulation Innovation]

- On Predictability: Consumers want products with "the predictability of a fixed rate and equal monthly payments." — Source: [Upgrade]

- On Flexibility: "Today consumers expect transparency and flexibility in their financial life." — Source: [Upgrade]

- On Convergence: The future of finance lies in "the convergence of payment and credit products." — Source: [TMCNet]

- On Helping Consumers: Implementing rewards programs was a strategic choice to "help consumers cope with this environment" of rising costs. — Source: [CrossRiver]

- On Multi-Product Platforms: It is critical to build a "multi-product platform from day one" to ensure sustainable, long-term growth. — Source: [Frontlines]

- On Responsible Credit: Financial consumers need access to affordable credit that does not unintentionally pull them into over-indebtedness. — Source: [Regulation Innovation]

- On Simplicity: The most effective financial tools provide simpler ways for users to manage their financial lives. — Source: [Regulation Innovation]

- On Alignment: Products must set consumers up well for the future, ensuring the company's success is tied to the user's financial health. — Source: [Regulation Innovation]

Part 3: The Credit Card Debt Crisis

- On Persistent Problems: "When I started there was $800 billion in credit cards, so I’m $500 billion in the red." — Source: [Asatunews]

- On the Minimum Payment Trap: Traditional credit cards make it "way too easy to just kick the can down the road, make a small minimum monthly payment and pay the interest but really not pay down the principal very much." — Source: [Asatunews]

- On Destructive Models: Traditional cards are often "designed to keep people in debt" through indefinite revolving balances. — Source: [Substack]

- On Behavioral Traps: Consumers often unintentionally accumulate debt by using credit cards for everyday purchases to maximize rewards, rather than planned expenses. — Source: [Asatunews]

- On Revolving vs. Installment Debt: Installment-based lending provides better outcomes because it enforces a predictable repayment schedule. — Source: [Alejandro Cremades]

- On the Scale of the Issue: U.S. credit card debt reaching $1.3 trillion is an indicator of systemic flaws in how consumer credit is structured. — Source: [Asatunews]

- On Reinventing the Card: The goal with modern fintech is combining the convenience of a credit card with the responsible repayment structure of closed-end consumer finance. — Source: [Regulation Innovation]

- On Unintentional Indebtedness: Even financially responsible users can fall into debt traps when products obscure the true cost of revolving interest. — Source: [Regulation Innovation]

- On Solving a 20-Year Problem: The fight against revolving consumer debt has been the defining mission of his two-decade career in fintech. — Source: [Asatunews]

Part 4: The Future of Banking

- On the Future Experience: "The future of banking is about creating an experience that customers love." — Source: [Fintechly]

- On Small Business Capital: "Small businesses are not only a driving force in the US economy; they are an essential part of the American Dream." — Source: [House.gov]

- On Shared Responsibility: "I believe it is our shared responsibility to ensure that these businesses and their owners have sufficient access to capital on fair terms." — Source: [House.gov]

- On Partnerships: "We have essentially become a marketing engine for [small institutions], because we have a bigger brand, a national brand and access to online deposit gathering resources." — Source: [Banking Dive]

- On Ideal Relationships: "Fair, balanced, win/win. Taking more than your fair share of the economics will lead to long term failure." — Source: [Principal Post]

- On Institutionalization: Fintech cannot disrupt banking without eventually institutionalizing and working within established frameworks. — Source: [QZ]

- On Cost Savings: The ultimate goal of a marketplace platform is "creating savings that we pass on" to both ends of the transaction. — Source: [SFGate]

- On Broadening Access: Online deposit gathering allows smaller financial institutions to compete on a national scale. — Source: [Banking Dive]

- On Economic Impact: Ensuring capital flows to small businesses is vital for the broader economic health of the country. — Source: [House.gov]

Part 5: Entrepreneurship & Scaling

- On the Middle Ground: "When you know the beginning and the end, it's very comforting. It's the middle where the tension builds and where no entrepreneur wants to be stuck." — Source: [Foundation Capital]

- On Defining Success: "Achieving your goals more often than not! Not everyone has the same goals... success is achieving your goals, whatever they are." — Source: [BillionSuccess]

- On Isolation: "Surround yourself with people you trust and respect. Being an entrepreneur can be a very lonely experience." — Source: [BillionSuccess]

- On Inviting Others: It is "critical to invite others on the ride, both as support and also to provide a different perspective." — Source: [BillionSuccess]

- On Early Hires: The first few hires are critical because they ultimately build their own teams and have an outsize impact on business strategy. — Source: [Regulation Innovation]

- On Rushed Decisions: Rushing hiring decisions can have a disastrous downstream impact on a growing company. — Source: [Regulation Innovation]

- On the "Atomic" Approach: He encourages teams to focus on shorter, more manageable versions of projects: "What's the one-week version of what they're working on?" — Source: [Regulation Innovation]

- On Golden Rules: "Be Nice to People on Your Way Up, you'll Meet Them On Your Way Down." — Source: [BillionSuccess]

- On Building Platforms: True scale comes from creating a multi-faceted platform rather than a single-feature application. — Source: [Substack]

- On Speed vs. Strategy: While speed is important, taking the time to architect a sustainable business model from day one pays off. — Source: [Frontlines]

Part 6: Leadership & Company Culture

- On Culture as Foundation: Establishing a strong culture of compliance and effective internal controls is essential for any enduring financial institution. — Source: [Regulation Innovation]

- On Overcoming Setbacks: Overcoming major adversity—such as losing his first company’s office during 9/11—forces a team to bond and innovate. — Source: [Regulation Innovation]

- On Resilience: Shared trauma or extreme challenges can ultimately lead to a more resilient business structure. — Source: [Regulation Innovation]

- On Human Capital: Talented people are consistently a company's greatest asset, regardless of technological advancements. — Source: [Regulation Innovation]

- On AI as a Co-pilot: Technology should be used as a "co-pilot" alongside human expertise rather than a wholesale replacement for human judgment. — Source: [Regulation Innovation]

- On Transparency: Maintaining an "open-door policy" in business builds the same trust required when relying on a crew offshore. — Source: [Latitude38]

- On Empowering Teams: A leader's job is to ensure that early hires have the autonomy and clarity needed to build their own successful departments. — Source: [Regulation Innovation]

- On Adapting Fast: If a company does not transform as fast as its consumers, it will quickly find itself in trouble. — Source: [Fintechly]

- On Honest Reflection: Learning from past failures in governance is crucial to building stronger internal controls in subsequent ventures. — Source: [Regulation Innovation]

Part 7: Regulation & Risk Management

- On the Scourge of Banking: He has described credit risk as the "scourge of banking," arguing for models that transfer this risk to investors rather than holding it on a balance sheet. — Source: [Fool.com]

- On Regulatory Frameworks: Working extensively with the SEC was a necessary step to bring marketplace lending out of the shadows and into a formal structure. — Source: [Foundation Capital]

- On the Hard Place of Government: Navigating government regulation is difficult but entirely necessary for industry legitimacy. — Source: [Foundation Capital]

- On Reliability: Partnering with federally regulated banks provides a foundational element of reliability for fintech platforms. — Source: [LendingClub]

- On Liquidity Risk: While marketplace lending mitigates balance sheet credit risk, it introduces significant liquidity risk that must be actively managed. — Source: [Fool.com]

- On Risk-Adjusted Returns: Technology creates marketplace efficiencies, which should be passed on to investors in the form of optimized, risk-adjusted returns. — Source: [LendingClub]

- On Macro Pressures: Broad economic pressures, including federal debt and energy risks, constantly reshape the landscape of consumer lending. — Source: [Deepscope]

- On Fiduciary Duty: The balance between a company's interests and the interests of the funds or investors it manages is a critical line that must never be blurred. — Source: [SEC]

- On Institutional Trust: A financial platform cannot survive a loss of trust; strict data integrity and transparency are non-negotiable. — Source: [Business Insider]

Part 8: Sailing & High-Performance Competition

- On Sensation and Balance: "You drive based on the balance of the boat... The sensations are different at night. You feel like you are going even faster. It's really exhilarating." — Source: [Forbes]

- On Facing the Unknown: "It's very scary when you don't get the moonlight." — Source: [Forbes]

- On the Necessity of Teams: "To beat a record like this you really need a great boat, great weather conditions and more importantly a great crew, and that's what we really had." — Source: [Cruising World]

- On Complete Dedication: Achieving world records requires that "everyone was almost 100 per cent almost all the time." — Source: [Cruising World]

- On Epic Conditions: "Getting into the Gulf Stream at 40 knots, with bright sunshine, the leeward hull spraying water up 10 feet in the air... that was quite epic." — Source: [Sailing World]

- On Shared Experience: Bringing employees and partners onto the boat was a deliberate extension of his philosophy on transparency and shared high-performance experience. — Source: [Latitude38]

- On Pushing Limits: Operating a maxi-trimaran at record speeds is a direct physical manifestation of the entrepreneurial drive to push beyond established boundaries. — Source: [RenaudLaplanche.com]

- On Preparation: In both ocean racing and business, you cannot control the weather or the market, but you can control your equipment, your team, and your readiness. — Source: [Cruising World]

- On High-Stakes Decision Making: Steering a boat at 40 knots in pitch darkness requires the same rapid, instinctual balance needed during severe economic turbulence. — Source: [Forbes]

- On Crossing the Finish Line: Setting the Newport to Bermuda or Transpac records proves that with the right alignment of crew and technology, traditional limits can be shattered. — Source: [Sailing World]