Lessons from Richard Bernstein

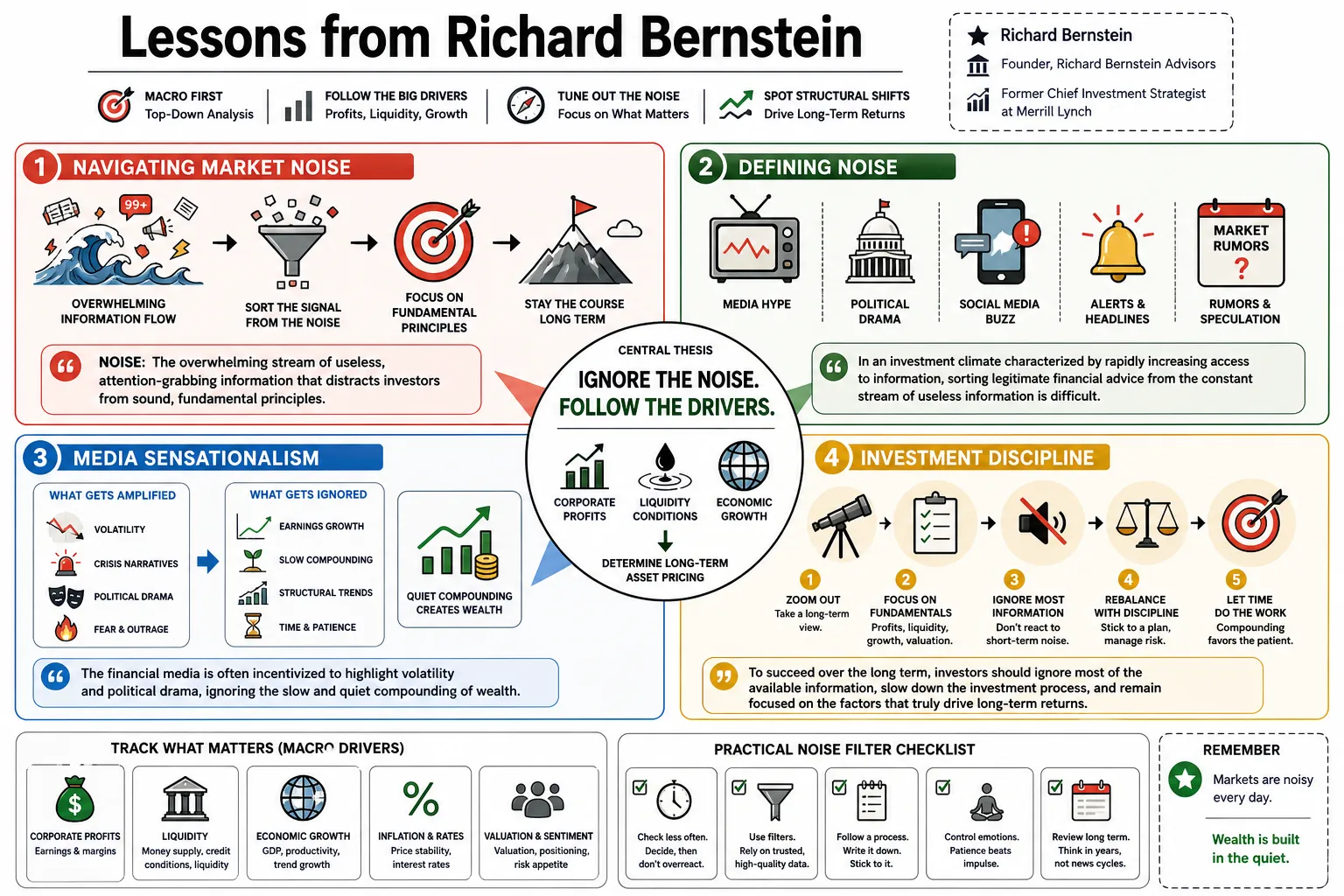

Richard Bernstein, founder of Richard Bernstein Advisors and former Chief Investment Strategist at Merrill Lynch, is a macroeconomic strategist who favors top-down analysis over individual stock picking. By tracking broad data like corporate profits and liquidity, his approach provides practical rules for tuning out financial media noise and spotting the structural shifts that actually determine long-term asset pricing.

Part 1: Navigating Market Noise

- On Defining Noise: "Noise is the overwhelming stream of useless, attention-grabbing information that distracts investors from sound, fundamental principles." — Source: [Navigate the Noise]

- On the Challenge of Information: "In an investment climate characterized by rapidly increasing access to information, sorting legitimate financial advice from the constant stream of useless information is difficult." — Source: [Navigate the Noise]

- On Media Sensationalism: "The financial media is often incentivized to highlight volatility and political drama, ignoring the slow and quiet compounding of wealth." — Source: [Richard Bernstein Advisors]

- On Investment Discipline: "To succeed over the long term, investors should ignore most of the available information, slow down the investment process, and trade less frequently." — Source: [Navigate the Noise]

- On Social Media: "The proliferation of social media has exponentially increased market noise, making it harder than ever to separate actual financial data from hype." — Source: [CNBC Interview]

- On Focus: "A successful investment process must be explicitly designed to be noise-cancelling, focusing strictly on macro-level indicators rather than daily headlines." — Source: [Richard Bernstein Advisors]

- On Short-Termism: "Reacting to the latest market trends is a surefire way to destroy capital; true investment requires looking past the immediate news cycle." — Source: [Bloomberg Masters in Business]

- On Patience as a Strategy: "Patience is the ultimate noise-cancelling mechanism; time arbitrage is one of the few edges left in modern markets." — Source: [Excess Returns Podcast]

- On the Information Illusion: "Having more data does not equal having more insight; often, it just means having more reasons to second-guess a solid strategy." — Source: [Navigate the Noise]

Part 2: Corporate Profits and Fundamentals

- On the Primary Driver: "While media headlines focus on political drama, the primary driver of long-term market performance is corporate profits." — Source: [Richard Bernstein Advisors]

- On Earnings Recessions: "Stock markets typically do not suffer sustained bear markets without a corresponding deterioration in corporate earnings fundamentals." — Source: [Barron's Commentary]

- On the Macro Pillars: "The most important pillars of top-down investing are corporate profits, global liquidity, and market sentiment." — Source: [Richard Bernstein Advisors]

- On Ignoring Politics: "Investors waste too much time analyzing election outcomes when they should be analyzing the trajectory of corporate cash flows." — Source: [CNBC Interview]

- On Profit Cycles: "Understanding where we are in the global corporate profit cycle is far more predictive of equity returns than guessing the next geopolitical event." — Source: [Bloomberg Masters in Business]

- On Quality: "High-quality companies with reliable earnings streams are consistently underpriced relative to speculative companies with merely a good story." — Source: [Style Investing]

- On Fundamental Disconnects: "When the stock price detaches entirely from the underlying earnings reality, you are no longer investing; you are speculating on greater fool theory." — Source: [Excess Returns Podcast]

- On Economic Normalization: "As the economy shifts back to historical norms, fundamental analysis of balance sheets will matter far more than it did during the era of free money." — Source: [Richard Bernstein Advisors]

- On Liquidity vs. Profits: "Liquidity can drive a market in the short term, but only enduring corporate profitability can sustain it in the long term." — Source: [Financial Times]

- On Macro Indicators: "Tracking leading economic indicators provides a much clearer picture of future market health than obsessing over daily stock ticker movements." — Source: [Navigate the Noise]

Part 3: Inflation and the Macroeconomic Shift

- On the End of an Era: "The forty-year era of secular disinflation, driven by globalization and favorable demographics, is definitively over." — Source: [Richard Bernstein Advisors]

- On Federal Reserve Targets: "The Fed’s insistence on returning to a two percent inflation target is backward-looking and ignores structural changes in the global economy." — Source: [CNBC Interview]

- On Structural Inflation: "Investors should prepare for a structural shift toward higher, more persistent inflation, likely settling in the three to four percent range for the foreseeable future." — Source: [Barron's Commentary]

- On Deglobalization: "The unwinding of global supply chains and the push for on-shoring are inherently inflationary forces that will persist for years." — Source: [Bloomberg Masters in Business]

- On the Guns and Butter Economy: "We are witnessing a return to the 1960s-style guns and butter economy, where massive fiscal spending on both domestic programs and defense drives sustained inflation." — Source: [Excess Returns Podcast]

- On Demographics: "The aging of the global workforce reduces labor supply, fundamentally shifting power back to workers and driving up wage inflation." — Source: [Richard Bernstein Advisors]

- On the Energy Transition: "The transition to green energy, while necessary, is highly capital intensive and will act as a structural inflationary pressure during the build-out phase." — Source: [Financial Times]

- On Adapting Portfolios: "Most modern investment portfolios were built for a disinflationary world; they are wholly unprepared for an environment of structural inflation." — Source: [CNBC Interview]

- On Real Returns: "In a higher inflation regime, investors must focus intensely on generating real returns rather than being distracted by nominal numbers." — Source: [Richard Bernstein Advisors]

Part 4: The Dangers of Market Concentration

- On the Narrow Market: "The unprecedented narrowness in stock markets, driven by a handful of mega-cap tech stocks, creates significant and unacknowledged risks for passive investors." — Source: [Richard Bernstein Advisors]

- On Passive Illusion: "Passive index investing in a highly concentrated market is no longer passive; it is an active, leveraged bet on a tiny subset of companies." — Source: [CNBC Interview]

- On Speculative Growth: "Chasing speculative growth stocks at peak valuations is a historically proven recipe for future underperformance." — Source: [Barron's Commentary]

- On Market Breadth: "Healthy bull markets are characterized by expanding breadth; extremely narrow markets are typically a warning sign of a pending correction." — Source: [Bloomberg Masters in Business]

- On Historical Precedents: "Today’s market concentration resembles the Nifty Fifty era of the 1970s or the Tech Bubble of 2000, both of which ended poorly for those who overpaid for popular stocks." — Source: [Excess Returns Podcast]

- On Hidden Concentration Risk: "Many investors think they are diversified by holding multiple ETFs, not realizing that those funds hold the exact same concentrated top positions." — Source: [Financial Times]

- On Mean Reversion: "The sheer weight of market history suggests that extreme concentration eventually unwinds, leading to a massive rotation of capital into neglected sectors." — Source: [Richard Bernstein Advisors]

- On Capital Misallocation: "When all the market's capital flows into a few dominant tech names, it starves the rest of the economy of investment, creating opportunities elsewhere." — Source: [CNBC Interview]

- On the Inevitable Broadening: "As the economic cycle matures, profit growth will broaden out to the remaining stocks in the broader index, ending the mega-cap monopoly on returns." — Source: [Richard Bernstein Advisors]

Part 5: The Case for Value and Boring Assets

- On Pricing Disconnects: "A lot of Maseratis are priced like Fords, highlighting the incredible disconnect between high-quality, undervalued stocks and the expensive assets currently in favor." — Source: [CNBC Interview]

- On Bad Companies: "Bad companies make very good stocks over the long term when they are neglected and attractively priced, because expectations are so low." — Source: [Style Investing]

- On Boring Assets: "Investors should move away from speculative, high-growth tech stocks and embrace high-quality, boring, defensive value assets." — Source: [Richard Bernstein Advisors]

- On Global Value: "The most attractive investment opportunities often lie outside the United States, where valuations are depressed and expectations are grounded." — Source: [Bloomberg Masters in Business]

- On the Glamour Premium: "Investors consistently overpay for glamour stocks with exciting narratives, while underpaying for mundane businesses that actually generate cash." — Source: [Style Investing]

- On Small Caps: "Small and mid-cap companies, heavily discounted during periods of mega-cap dominance, represent some of the best long-term value propositions in the market." — Source: [Barron's Commentary]

- On Real Assets: "In an inflationary regime, hard assets, commodities, and industrials transition from being old-economy relics to essential portfolio anchors." — Source: [Excess Returns Podcast]

- On the Cost of Excitement: "Excitement is usually the enemy of returns; the more thrilling an investment sounds at a cocktail party, the worse it is likely to perform." — Source: [Navigate the Noise]

- On Expectation Revisions: "Value investing works because it capitalizes on the upward revision of extremely pessimistic expectations." — Source: [Richard Bernstein Advisors]

- On Forgotten Sectors: "The market frequently ignores essential sectors like energy and materials until a supply shock reminds everyone of their fundamental necessity." — Source: [Financial Times]

Part 6: Dividends and Long-Term Compounding

- On the Power of Compounding: "The power of compounding dividends is a far more reliable path to long-term wealth than chasing market hype or attempting to time explosive growth." — Source: [Richard Bernstein Advisors]

- On Total Return: "Investors forget that historically, a massive percentage of the stock market's total return has come from reinvested dividends, not capital appreciation alone." — Source: [Bloomberg Masters in Business]

- On the Margin of Safety: "A strong, growing dividend provides a critical margin of safety when market valuations contract." — Source: [Barron's Commentary]

- On Management Discipline: "Committing to a regular dividend forces corporate management teams to be disciplined with capital allocation, preventing them from funding wasteful vanity projects." — Source: [CNBC Interview]

- On Inflation Protection: "Companies with the pricing power to consistently grow their dividends offer one of the most effective hedges against a high-inflation environment." — Source: [Excess Returns Podcast]

- On the Math of Wealth: "Wealth isn't built by finding the next hot stock; it's built by patiently allowing the math of reinvested cash flows to work over decades." — Source: [Navigate the Noise]

- On Yield Traps: "Not all dividends are created equal; a high yield is often a warning sign of a distressed balance sheet rather than a signal of fundamental strength." — Source: [Richard Bernstein Advisors]

- On Dividend Growth: "The trajectory of dividend growth is often a more accurate reflection of a company's true economic health than its reported earnings." — Source: [Style Investing]

- On Cash as Truth: "Earnings can be manipulated through accounting maneuvers, but a cash dividend paid into a brokerage account is undeniable proof of profitability." — Source: [Financial Times]

Part 7: Risk Management and Market Cycles

- On Black Swans: "Investors spend too much time worrying about unpredictable black swans while ignoring basic, observable business cycle risks that actually drive bear markets." — Source: [Richard Bernstein Advisors]

- On the Siren Song: "The siren song of assets that appear to offer high returns without risk will inevitably cause investors to crash on the rocks of reality." — Source: [Navigate the Noise]

- On Diversification: "True diversification is the only free lunch in finance, yet investors repeatedly abandon it the moment a single asset class starts to drastically outperform." — Source: [Bloomberg Masters in Business]

- On Valuation Timing: "Valuations are terrible tools for timing market tops or bottoms, but they are incredibly precise predictors of long-term ten-year returns." — Source: [CNBC Interview]

- On the Cycle of Liquidity: "When central banks drain liquidity from the system, the most speculative and overvalued assets are always the first to collapse." — Source: [Barron's Commentary]

- On Defining Risk: "Risk is not simply volatility; true risk is the permanent impairment of capital caused by overpaying for an asset at the peak of a cycle." — Source: [Excess Returns Podcast]

- On Style Cycles: "Investment styles like value versus growth or large versus small move in massive, multi-year cycles that investors must learn to ride rather than fight." — Source: [Style Investing]

- On Bear Market Anatomy: "Severe bear markets rarely happen in a vacuum; they are almost always preceded by high valuations combined with decelerating corporate profits." — Source: [Richard Bernstein Advisors]

- On Economic Gravity: "No asset class can permanently defy the gravity of the underlying macroeconomic fundamentals; eventually, reality reasserts itself." — Source: [Financial Times]

Part 8: Behavioral Finance and Contrarianism

- On Crowd Behavior: "The crowd is usually right during the middle of a market trend, but catastrophically wrong at the absolute peaks and troughs." — Source: [Richard Bernstein Advisors]

- On Uncomfortable Investing: "The best investment decisions are usually the ones that feel the most uncomfortable to execute at the time." — Source: [Bloomberg Masters in Business]

- On Sentiment Indicators: "Extreme bullish sentiment is not a reason to buy; it is often the most reliable signal that all available capital has already been deployed." — Source: [CNBC Interview]

- On Eating Relative Returns: "Investors obsess over beating a benchmark by a few basis points, forgetting the old Wall Street adage that you cannot eat relative returns." — Source: [Navigate the Noise]

- On the Fear of Missing Out: "The fear of missing out is the destroyer of wealth, driving investors to abandon their disciplined processes precisely when they need them the most." — Source: [Barron's Commentary]

- On Contrarian Action: "True contrarianism isn't just taking the opposite side of every trade; it is about recognizing when market prices have completely detached from fundamental economic reality." — Source: [Excess Returns Podcast]

- On Narrative Economics: "When investors stop talking about earnings and start talking about new paradigms or eyeballs, a bubble is usually about to burst." — Source: [Style Investing]

- On Humility: "The market is a brutally efficient mechanism for transferring wealth from the arrogant to the humble." — Source: [Richard Bernstein Advisors]

- On Consensus Thinking: "If you are reading the same headlines and buying the same index funds as everyone else, you cannot expect to achieve superior long-term results." — Source: [Financial Times]

- On Staying the Course: "The hardest part of investing is not identifying the right strategy, but having the psychological fortitude to stick with it during periods of severe underperformance." — Source: [Navigate the Noise]