Lessons from Richard Lawrence

Richard Lawrence has compounded capital in Asian equities at over 14% annually since founding Overlook Investments in 1991. He relies on "The Overlook Model," a strict framework that caps fund size to protect returns and forces financial alignment between managers and clients. This profile covers how he evaluates businesses, structures an independent firm, and survives severe bear markets across emerging economies.

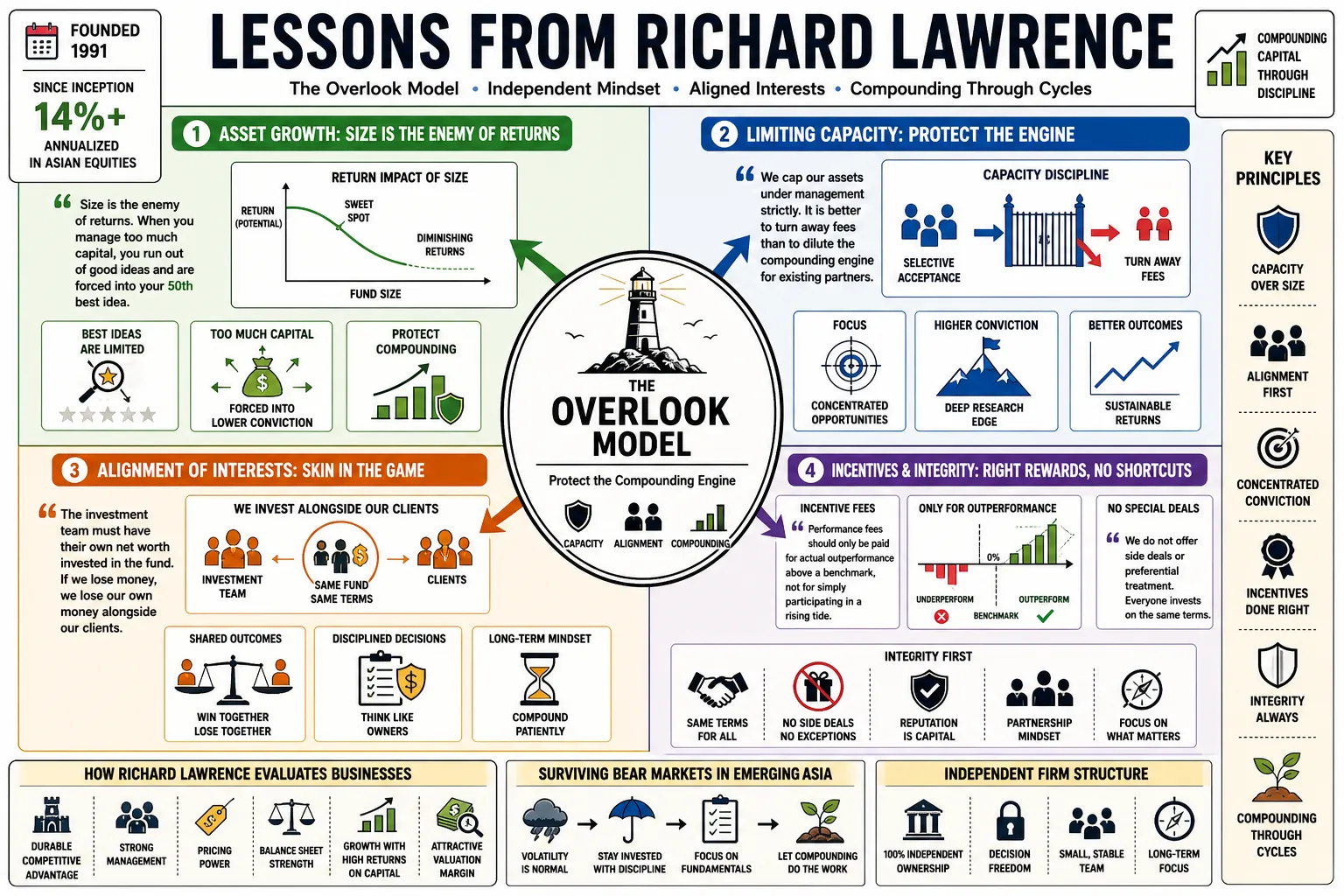

Part 1: The Overlook Model and Fund Structure

- On Asset Growth: "Size is the enemy of returns. When you manage too much capital, you run out of good ideas and are forced into your 50th best idea." — Source: [The Model: 37 Years Investing in Asian Equities]

- On Limiting Capacity: "We cap our assets under management strictly. It is better to turn away fees than to dilute the compounding engine for existing partners." — Source: [The Investor’s Podcast Network (TIP661)]

- On Alignment of Interests: "The investment team must have their own net worth invested in the fund. If we lose money, we lose our own money alongside our clients." — Source: [Capital Allocators Podcast (Episode 144)]

- On Incentive Fees: "Performance fees should only be paid for actual outperformance above a benchmark, not for simply participating in a rising tide." — Source: [The Model: 37 Years Investing in Asian Equities]

- On Special Deals: "We do not offer side letters or special fee arrangements to large institutions. Every investor gets the exact same terms." — Source: [Investing by the Books (Episode 25)]

- On Independence: "Staying independent allows us to prioritize long-term results over short-term corporate pressures or asset gathering targets." — Source: [Ben Graham Centre for Value Investing]

- On Client Communication: "In difficult years, we write more, not less. Investors need transparency most when the numbers look the worst." — Source: [The Investor’s Podcast Network (TIP661)]

- On Fund Continuity: "A sustainable firm requires a clear succession plan where the next generation of investors is incentivized through real equity ownership." — Source: [Capital Allocators Podcast (Episode 144)]

- On the Role of the Manager: "Our job is not to build a financial empire. It is to protect and grow purchasing power for the families and endowments that trust us." — Source: [The Model: 37 Years Investing in Asian Equities]

Part 2: Business Quality and Profitability

- On Operating Return: "Operating return is the purest measure of profitability. It strips out financial engineering to show what the business actually produces." — Source: [MOI Global Meet-the-Author]

- On Cash Flow vs. Earnings: "Earnings can be manipulated through accounting choices. Cash flow is much harder to fake and represents the real blood supply of the enterprise." — Source: [Value Investing with Legends]

- On Corporate Debt: "We strongly prefer companies with minimal or no debt. Debt removes optionality when the cycle inevitably turns down." — Source: [The Model: 37 Years Investing in Asian Equities]

- On Reinvestment: "The best businesses can reinvest large portions of their free cash flow at consistently high rates of return." — Source: [Investing by the Books (Episode 25)]

- On Margins: "High profit margins are a defense mechanism. They provide a buffer against inflation and pricing wars that low-margin competitors simply do not have." — Source: [The Investor’s Podcast Network (TIP661)]

- On Moats: "A sustainable competitive advantage in Asia often comes down to distribution networks and brand loyalty, which take decades to build." — Source: [Capital Allocators Podcast (Episode 144)]

- On Capital Intensity: "Asset-light models are preferable because they generate cash rather than constantly consuming it just to maintain current operations." — Source: [Lunches with Legends]

- On Predictability: "We seek businesses where the outcome over the next five years is highly predictable, not those dependent on binary technological breakthroughs." — Source: [The Model: 37 Years Investing in Asian Equities]

- On Organic Growth: "Growth should come from expanding market share and entering adjacent markets organically, not through constant dilutive acquisitions." — Source: [Ben Graham Centre for Value Investing]

- On Inflation Protection: "Pricing power is the only true defense against inflation. If a company cannot raise prices without losing customers, its real value will erode." — Source: [MOI Global Meet-the-Author]

Part 3: Management and Corporate Governance

- On Dividends over Buybacks: "We favor dividends because they represent actual cash returned to owners. Buybacks in Asia are too often used to obscure poor capital allocation." — Source: [The Model: 37 Years Investing in Asian Equities]

- On Management Integrity: "You cannot build a successful long-term holding with a management team you do not completely trust. The math will eventually break." — Source: [LONGRIVER Podcast]

- On Quiet Activism: "Screaming at management in public rarely works in Asia. We engage constructively in private to improve corporate governance." — Source: [Capital Allocators Podcast (Episode 144)]

- On Skin in the Game: "Founders and managers should have their wealth tied up in the common equity, sharing the exact same downside risk as minority shareholders." — Source: [Value Investing with Legends]

- On Board Independence: "A board full of friends and insiders is a red flag. We look for directors who will actually challenge the CEO's assumptions." — Source: [The Investor’s Podcast Network (TIP661)]

- On Capital Allocation: "Most executives are promoted for operational excellence, but their primary job as CEO is capital allocation, a skill they often have to learn on the job." — Source: [Investing by the Books (Episode 25)]

- On Transparency: "Complex corporate structures are usually designed to hide something. We avoid companies that we cannot explain to a child in three sentences." — Source: [The Model: 37 Years Investing in Asian Equities]

- On Executive Compensation: "Pay packages must be tied to return on invested capital over multi-year periods, not just raw earnings per share growth." — Source: [MOI Global Meet-the-Author]

- On Admitting Mistakes: "The best CEOs tell you what went wrong before they tell you what went right. Candor is the strongest indicator of future success." — Source: [LONGRIVER Podcast]

Part 4: Valuation and The Buying Process

- On Bargain Prices: "A great business is only a great investment if purchased at a bargain valuation. Price dictates your margin of safety." — Source: [The Model: 37 Years Investing in Asian Equities]

- On the Research Funnel: "We look at hundreds of companies every year to find perhaps two or three that meet all our criteria for quality and price." — Source: [Ben Graham Centre for Value Investing]

- On Patience: "Cash is a viable option when nothing meets our hurdle rate. We are perfectly willing to sit on our hands and wait for the market to offer us a fat pitch." — Source: [The Investor’s Podcast Network (TIP661)]

- On Contrarianism: "To buy at a bargain, you usually have to buy when everyone else is selling. This requires ignoring the immediate macro noise." — Source: [Capital Allocators Podcast (Episode 144)]

- On DCF Models: "Discounted cash flow models are dangerous if you tweak the terminal value to justify the current price. We use them conservatively to test our assumptions." — Source: [Value Investing with Legends]

- On Value Traps: "A cheap stock is a trap if the underlying business is deteriorating. The margin of safety disappears as the intrinsic value shrinks." — Source: [The Model: 37 Years Investing in Asian Equities]

- On Initial Position Sizing: "We start with a meaningful but manageable position and add as management proves our thesis correct over time." — Source: [Investing by the Books (Episode 25)]

- On Ignoring Hype: "We consistently avoid the hype of the day. Hot sectors attract too much capital, destroying returns for late arrivals." — Source: [MOI Global Meet-the-Author]

- On Relative vs. Absolute Value: "We do not buy a company just because it is cheaper than its peers. It must be cheap relative to its own cash-generating ability." — Source: [LONGRIVER Podcast]

Part 5: The Discipline of Selling

- On Broken Theses: "If the original reason for buying the stock is no longer valid, you must sell immediately. Do not wait to get back to breakeven." — Source: [The Model: 37 Years Investing in Asian Equities]

- On Valuation Extremes: "When a stock becomes egregiously expensive, even if it is a wonderful business, we will sell and reallocate the capital to a better bargain." — Source: [The Investor’s Podcast Network (TIP661)]

- On Management Changes: "A sudden departure of a trusted founder or CEO triggers a hard review. Often it is the first sign that the internal culture is fracturing." — Source: [Capital Allocators Podcast (Episode 144)]

- On Capital Allocation Errors: "If management uses cash flow to make a massive and unrelated acquisition, we generally sell. It shows a lack of discipline." — Source: [Value Investing with Legends]

- On Holding Periods: "Our ideal holding period is forever, but the reality of business cycles means we average roughly five to seven years." — Source: [MOI Global Meet-the-Author]

- On Selling Winners: "Trimming a position that has grown too large is simply prudent risk management, not a lack of faith in the company." — Source: [Investing by the Books (Episode 25)]

- On Accounting Irregularities: "The moment we suspect the numbers are manipulated, we exit. There is rarely only one cockroach in the kitchen." — Source: [The Model: 37 Years Investing in Asian Equities]

- On Sunk Costs: "The market does not know what you paid for a stock. Decisions must be made on current reality, not past purchase prices." — Source: [Ben Graham Centre for Value Investing]

- On Upgrading the Portfolio: "We sell fair businesses at fair prices to buy exceptional businesses at bargain prices. The portfolio must always be improving in quality." — Source: [LONGRIVER Podcast]

- On Emotional Attachment: "Never fall in love with a stock. It is a piece of paper representing a business, and the business does not know you exist." — Source: [The Investor’s Podcast Network (TIP661)]

Part 6: Navigating Bear Markets and Risk

- On Crises as Opportunities: "The 1997 Asian Financial Crisis taught us that bear markets are the absolute best time to acquire outstanding assets at distressed prices." — Source: [The Investor’s Podcast Network (TIP661)]

- On True Risk: "Risk is not volatility or tracking error against an index. Risk is the permanent loss of capital." — Source: [The Model: 37 Years Investing in Asian Equities]

- On Macro Forecasting: "We spend zero time trying to predict interest rates or GDP growth. We focus entirely on how individual businesses will handle stress." — Source: [Capital Allocators Podcast (Episode 144)]

- On Liquidity: "In a panic, liquidity dries up instantly. You must ensure you hold businesses that do not require continuous access to capital markets to survive." — Source: [Value Investing with Legends]

- On Averaging Down: "We are happy to buy more of a position as it drops, provided our assessment of the intrinsic value remains completely intact." — Source: [Investing by the Books (Episode 25)]

- On Portfolio Concentration: "We hold a concentrated portfolio of our best ideas. Diversification for the sake of diversification just dilutes returns." — Source: [The Model: 37 Years Investing in Asian Equities]

- On Market Psychology: "Bear markets test your conviction. You must have the psychological endurance to look wrong for months while waiting for the fundamentals to assert themselves." — Source: [MOI Global Meet-the-Author]

- On Stress Testing: "We analyze how a company performed during the last two recessions to predict how it will survive the next one." — Source: [LONGRIVER Podcast]

- On Taking Action: "When blood is in the streets, you cannot just watch. You must have the discipline to actually execute buy orders when your instincts tell you to hide." — Source: [The Investor’s Podcast Network (TIP661)]

Part 7: Asian Equities and Emerging Markets

- On Market Inefficiencies: "Asian markets offer massive inefficiencies because retail participation is high and institutional research is often focused on short-term momentum." — Source: [The Model: 37 Years Investing in Asian Equities]

- On State-Owned Enterprises: "We approach state-owned enterprises with extreme caution. Their primary goal is often social stability or political alignment, not maximizing shareholder value." — Source: [Capital Allocators Podcast (Episode 144)]

- On China's Regulatory Environment: "Investing in China requires understanding the regulatory environment deeply. The rules can change overnight, affecting entire industries." — Source: [Investing by the Books (Episode 25)]

- On Regional Diversification: "While we focus on Asia, we recognize the distinct differences in governance, currency, and culture between markets like Taiwan, Korea, and India." — Source: [Value Investing with Legends]

- On Family Conglomerates: "Many Asian businesses are controlled by families. You must determine whether they treat minority shareholders as partners or as sources of cheap funding." — Source: [MOI Global Meet-the-Author]

- On Currency Risk: "We invest in local businesses operating in local currencies. We do not hedge currency exposure because over a ten-year period, purchasing power parity usually normalizes." — Source: [The Model: 37 Years Investing in Asian Equities]

- On Demographic Tailwinds: "The rising middle class in Asia provides a structural tailwind for consumer brands and financial services that spans decades." — Source: [Ben Graham Centre for Value Investing]

- On Local Research: "You cannot invest in Asia from a desk in New York. You have to visit the factories, talk to the distributors, and understand the local context." — Source: [LONGRIVER Podcast]

- On Geopolitics: "Geopolitical tensions create volatility, but they rarely alter the long-term cash flow trajectory of well-run domestic businesses." — Source: [The Investor’s Podcast Network (TIP661)]

Part 8: Philosophy and Lifelong Habits

- On Ethical Integration: "Good governance naturally leads to environmental and social responsibility. Furthermore, dedicating a portion of our profits to philanthropy grounds our mission." — Source: [Capital Allocators Podcast (Episode 144)]

- On Daily Reading: "An investor’s primary job is to read. We consume annual reports, trade journals, and financial history to build a reservoir of pattern recognition." — Source: [The Model: 37 Years Investing in Asian Equities]

- On Intellectual Honesty: "You must ruthlessly examine your own mistakes. We keep a detailed log of our worst investments to ensure we never repeat the same error." — Source: [Value Investing with Legends]

- On Saying No: "The most powerful word in investing is no. We pass on the vast majority of the ideas that cross our desks." — Source: [MOI Global Meet-the-Author]

- On Avoiding Envy: "Watching others get rich quickly in speculative bubbles is the hardest test of an investor. Envy drives rational people to make terrible decisions." — Source: [The Investor’s Podcast Network (TIP661)]

- On Simplicity: "Our investment process is incredibly simple to explain, but it is extremely difficult to execute with consistency over thirty years." — Source: [Ben Graham Centre for Value Investing]

- On Humility: "The market will humble you repeatedly. The moment you believe you have it all figured out, you are setting yourself up for a massive loss." — Source: [LONGRIVER Podcast]

- On Team Culture: "A great investment firm fosters debate. Junior analysts must feel completely comfortable telling the portfolio manager why a favorite stock is a bad idea." — Source: [Capital Allocators Podcast (Episode 144)]

- On Institutional Memory: "Writing down the investment thesis forces clarity and creates a permanent record that prevents goalpost-shifting when the stock drops." — Source: [The Model: 37 Years Investing in Asian Equities]

- On the Long Game: "Compounding takes time. The greatest edge you can have in modern markets is the willingness to hold a good business for a decade." — Source: [Investing by the Books (Episode 25)]