Lessons from Ricky Sandler

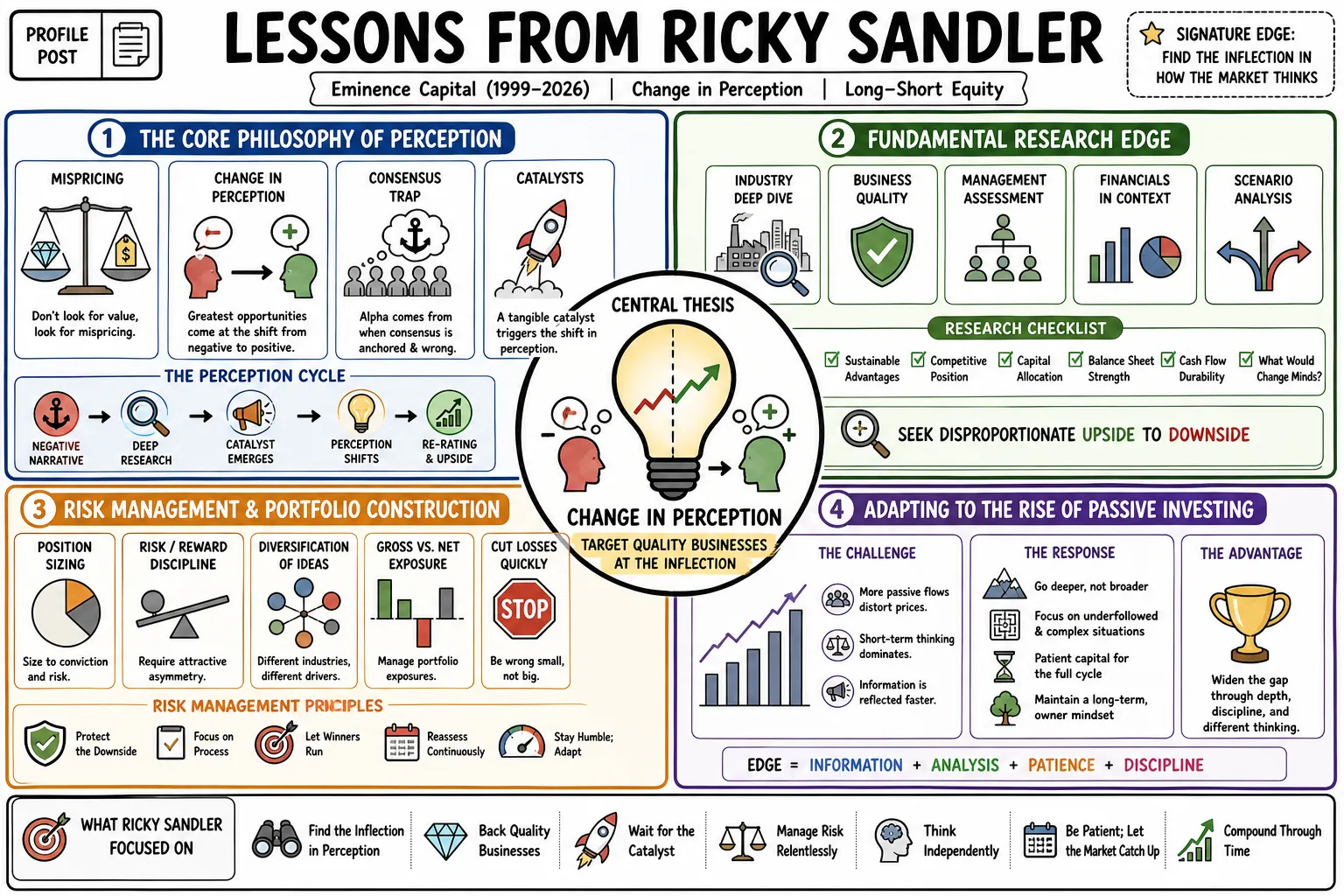

Ricky Sandler managed the long-short equity hedge fund Eminence Capital from 1999 until it closed in 2026. His signature "change in perception" strategy targeted quality businesses exactly when the market consensus started to shift. This profile covers his methods for fundamental research, managing risk, and dealing with the rise of passive investing.

Part 1: The Core Philosophy of Perception

- On Mispricing: "Don't look for value, look for mispricing. A cheap stock can stay cheap forever if the market's understanding of it never changes." — Source: Bloomberg Masters in Business

- On the Change in Perception: "The greatest opportunities arise more than when a business is doing well, but when the market's embedded expectations about that business fundamentally shift from negative to positive." — Source: Value Investing with Legends

- On the Consensus View: "You cannot generate alpha by agreeing with the consensus. You have to find situations where the consensus is anchored to outdated information and is demonstrably wrong." — Source: Invest Like the Best

- On Catalysts: "A change in perception rarely happens in a vacuum; it requires a tangible catalyst—a management change, a capital allocation shift, or an earnings inflection—that forces the market to re-evaluate." — Source: Capital Allocators

- On Identifying Change: "We look for businesses that are transitioning from 'bad to less bad' or 'okay to great.' The delta in perception is where the multiple expansion happens." — Source: Value Investing with Legends

- On Time Horizons: "The market is increasingly focused on the next quarter. If you can extend your duration and underwrite a shift in perception over a two- to three-year horizon, you face significantly less competition." — Source: Bloomberg Masters in Business

- On Value vs Growth: "The labels of 'value' and 'growth' are often restrictive. We prefer to view investments through the lens of quality and mispriced expectations, regardless of the traditional bucket they fall into." — Source: Invest Like the Best

- On Asymmetry: "We structure trades where if our thesis on a perception change is wrong, the downside is protected by a solid balance sheet, but if we are right, the upside is outsized." — Source: Capital Allocators

- On the Setup: "The ideal setup is a high-quality business experiencing a temporary, fixable problem that the broader market has extrapolated into a permanent impairment." — Source: Value Investing with Legends

- On Market Reactions: "Often, the market's initial reaction to a positive data point in a hated stock is skepticism. That disbelief is the window to build a position before the perception fully shifts." — Source: Bloomberg Masters in Business

Part 2: Bottom-Up Fundamental Analysis

- On Old Research, New Events: "Our best ideas tend to come from what I call 'old research, new events.' That's typically the good company you've studied carefully and would love to own at the right price, that gets marked down after it trips or its industry goes out of favor." — Source: Invest Like the Best

- On Deep Research: "Fundamental research is more than about reading the 10-K; it is about tearing apart the unit economics to understand exactly how a company generates free cash flow and where those margins can improve." — Source: Capital Allocators

- On Management Quality: "A great business can survive bad management for a while, but exceptional management can accelerate a change in perception by aggressively reallocating capital." — Source: Value Investing with Legends

- On Free Cash Flow: "Earnings can be manipulated through accounting assumptions, but free cash flow generation is the ultimate truth-teller of a business's health." — Source: Bloomberg Masters in Business

- On Competitive Moats: "We look for businesses with durable competitive advantages that the market is temporarily ignoring due to a cyclical downturn or a macro scare." — Source: Invest Like the Best

- On Capital Allocation: "One of the quickest ways to change market perception is when a company stops wasting capital on poor acquisitions and starts buying back heavily discounted shares." — Source: Eminence Capital Letters

- On Unit Economics: "Before you can predict earnings three years out, you must understand the profitability of the next marginal unit sold. If the unit economics are broken, the macro environment won't save you." — Source: Capital Allocators

- On Financial Modeling: "A model should not be an exercise in false precision; it should be a tool to stress-test the key drivers of the business under different scenarios." — Source: Value Investing with Legends

- On Red Flags: "Consistently aggressive accounting, high executive turnover, and confusing disclosures are almost always leading indicators of a fundamental deterioration." — Source: Invest Like the Best

- On Focus: "You have to isolate the two or three variables that actually matter to the business's long-term value, rather than getting distracted by the dozens of data points the market fixates on daily." — Source: Bloomberg Masters in Business

Part 3: Adapting to Market Structure

- On Market Participants: "We as investors and analysts love to value business, love to understand what's happening, then we operate in the larger marketplace, which can humble you." — Source: Capital Allocators

- On Passive Flows: "The rise of passive investing means that stocks increasingly move based on fund flows rather than fundamental business developments, which requires active managers to adjust their entry and exit strategies." — Source: Bloomberg Masters in Business

- On Analyzing Investors: "In recent years, I have spent a significant portion of my time analyzing the behaviors of other investors in a stock, rather than just the business fundamentals alone." — Source: Forbes

- On Thematic Trading: "When thematic investing dominates, individual company fundamentals get overshadowed by the sector narrative. You have to wait for the narrative to exhaust itself before the fundamentals matter again." — Source: Value Investing with Legends

- On Quant Integration: "You can no longer ignore quantitative signals. Integrating data science and alternative data into fundamental research is mandatory to understand positioning and crowding." — Source: Capital Allocators

- On Price Discovery: "With fewer active, fundamental stock pickers providing liquidity, price discovery has become less efficient in the short term, leading to more dramatic dislocations." — Source: Invest Like the Best

- On Short-Termism: "The market's duration has shrunk dramatically. Algorithms and day traders react to headlines in milliseconds, creating volatility that long-term investors can use to build positions." — Source: Bloomberg Masters in Business

- On Liquidity: "You have to be highly aware of the liquidity profile of your book. In flow-driven markets, the exits become very narrow when everyone decides to leave at the same time." — Source: Value Investing with Legends

- On Adapting the Process: "If you apply a 1999 investment process to a modern market, you will get run over. The businesses haven't changed as much as the players trading them have." — Source: Capital Allocators

Part 4: Risk Management and Volatility

- On Volatility vs Risk: "Volatility is terrific. What we don't want is the permanent loss." — Source: Bloomberg Masters in Business

- On Permanent Loss: "A stock going down 20% on a macro panic is volatility; a stock going to zero because the balance sheet was mismanaged is a permanent loss. You must know the difference." — Source: Invest Like the Best

- On Position Sizing: "Position size should be directly correlated to the depth of your conviction and the asymmetry of the risk/reward, more than how much you like the management team." — Source: Capital Allocators

- On Cutting Losses: "When the thesis breaks—when the reason you bought the stock is no longer valid—you must sell immediately. Hoping for a rebound is not a risk management strategy." — Source: Value Investing with Legends

- On Gross Exposure: "Gross exposure is a measure of your footprint in the market. In times of extreme uncertainty, taking down gross exposure is the most effective way to protect capital." — Source: Bloomberg Masters in Business

- On Correlation Risk: "True risk management requires looking past sector labels to understand how different positions in your portfolio will behave together under specific macroeconomic stressors." — Source: Capital Allocators

- On use: "use is a tool that amplifies both skill and mistakes. Using it to turn a mediocre return into an acceptable one usually ends in disaster." — Source: Invest Like the Best

- On Macro Factors: "We don't bet on macro outcomes, but we relentlessly stress-test our portfolios to ensure we can survive them." — Source: Value Investing with Legends

- On Respecting the Market: "The market is a discounting mechanism that is often smarter than any individual investor. If a stock is relentlessly acting against your thesis, you must re-evaluate your assumptions." — Source: Bloomberg Masters in Business

Part 5: The Psychology of Investing

- On Humility: "This profession requires extreme humility. The moment you think you have the market completely figured out is exactly when you are about to lose money." — Source: Capital Allocators

- On Conviction: "Conviction is built through exhaustive research. If you only have a superficial understanding of a business, you will get shaken out at the exact wrong time." — Source: Value Investing with Legends

- On Cognitive Bias: "We are all prone to confirmation bias. The job of a good analyst is to actively seek out the data that destroys their own thesis." — Source: Invest Like the Best

- On Patience: "In a market obsessed with daily movements, having the psychological endurance to wait for a change in perception to play out over two years is a massive structural advantage." — Source: Bloomberg Masters in Business

- On Contrarianism: "Being a contrarian just to be different is foolish. You have to be contrarian and right, which means having a rigorous, evidence-based reason for disagreeing with the crowd." — Source: Capital Allocators

- On Emotional Discipline: "The best investment decisions are rarely comfortable. Buying a stock when everyone hates it, or selling when everyone loves it, requires a high degree of emotional detachment." — Source: Value Investing with Legends

- On Learning from Mistakes: "Every loss is an expensive lesson. If you do not perform an honest post-mortem on why a trade failed, you are wasting the tuition you just paid to the market." — Source: Invest Like the Best

- On Intellectual Honesty: "You have to be willing to change your mind instantly when the facts change, without letting your ego get in the way of protecting capital." — Source: Bloomberg Masters in Business

- On Market Noise: "Filtering out the daily noise of financial media and price action is essential to maintaining focus on the underlying business trajectory." — Source: Capital Allocators

Part 6: Short Selling and Activism

- On the Purpose of Shorting: "Shorting is more than about hedging; it is an independent profit center. You want to find structurally flawed businesses where the market perception is irrationally optimistic." — Source: Value Investing with Legends

- On Asymmetric Risk in Shorts: "The math of shorting works against you—your upside is capped at 100%, and your downside is infinite. You must have a strict discipline for sizing and covering." — Source: Bloomberg Masters in Business

- On Valuation Shorts: "Shorting a great company simply because it looks expensive is a dangerous game. You need a catalyst, a broken business model, or aggressive accounting to make a short work." — Source: Invest Like the Best

- On Fraud and Fads: "The best shorts are either outright frauds, businesses facing secular decline that the market hasn't recognized, or unsustainable fads." — Source: Capital Allocators

- On Short Squeezes: "In a market with heavy retail participation and algorithmic trading, the mechanics of a short squeeze can detach a stock from fundamentals entirely. You must respect positioning." — Source: Bloomberg Masters in Business

- On Activist Investing: "Activism is just an extension of value investing. When a board is destroying value, sometimes you have to serve as the catalyst for the perception change yourself." — Source: Value Investing with Legends

- On Constructive Engagement: "Most of our activism is behind the scenes, engaging constructively with management to outline paths for value creation, such as better capital allocation or divesting non-core assets." — Source: Eminence Capital Letters

- On Public Letters: "Going public with an activist letter is a last resort, used only when a board refuses to listen to logic and we need to rally the broader shareholder base." — Source: Capital Allocators

- On Board Accountability: "Directors often forget they are elected to represent the shareholders, not to protect the CEO. Holding boards accountable is essential to public market integrity." — Source: Eminence Capital Letters

- On Value Destructive M&A: "One of the most common reasons we intervene is to stop a management team from executing an illogical, empire-building acquisition that destroys shareholder capital." — Source: Bloomberg Masters in Business

Part 7: Portfolio Construction

- On Concentration vs Diversification: "A portfolio should be concentrated enough that your best ideas drive returns, but diversified enough that a single catastrophic event in one sector doesn't ruin the fund." — Source: Invest Like the Best

- On Capital Efficiency: "Every position must earn its keep. If a stock is dead money and lacks a catalyst, that capital is better deployed into an idea with an active perception shift underway." — Source: Capital Allocators

- On Pair Trades: "Pairing a long in a strong business with a short in its weaker competitor can isolate the fundamental delta between the two, removing broader market risk." — Source: Value Investing with Legends

- On Beta Neutrality: "Managing net exposure is about controlling your directional bet on the market, but true alpha is generated by the spread between your longs and your shorts." — Source: Bloomberg Masters in Business

- On Scaling In and Out: "You rarely nail the exact bottom or top. Scaling into positions as your conviction grows, and trimming as the stock approaches your price target, is a more strong strategy." — Source: Invest Like the Best

- On Cash as a Position: "Cash is a residual of the opportunity set. If there are no compelling ideas that meet our hurdle rate, holding cash is preferable to forcing capital into mediocre trades." — Source: Capital Allocators

- On Factor Risks: "You have to ensure your portfolio isn't unintentionally acting as a massive bet on a single macroeconomic factor, like interest rates or oil prices." — Source: Value Investing with Legends

- On Rebalancing: "Regular rebalancing forces you to trim the winners that have become a larger portion of risk, and add to the high-conviction ideas that have temporarily traded down." — Source: Bloomberg Masters in Business

- On Portfolio Agility: "A portfolio must remain liquid enough that when the market presents a massive dislocation, you can quickly pivot and deploy capital aggressively." — Source: Invest Like the Best

Part 8: The Evolution of the Hedge Fund Industry

- On the Golden Age of Long/Short: "The early days of long-short equity were defined by information asymmetry. Today, the edge is in behavioral analysis and time horizon, more than getting the data first." — Source: Capital Allocators

- On Rising Costs: "The infrastructure required to run a competitive institutional hedge fund today—compliance, data science, technology—has raised the barrier to entry astronomically." — Source: HedgeWeek

- On Talent Retention: "Attracting and retaining top analytical talent is the hardest part of the business. You are competing more than with other funds, but with private equity and technology firms." — Source: Bloomberg Masters in Business

- On Fee Structures: "The traditional fee model is under pressure because investors rightly demand alpha, not leveraged beta, for the fees they are paying." — Source: Invest Like the Best

- On Institutionalization: "The shift from high-net-worth capital to institutional capital changed the industry. Institutions require a level of process documentation and risk reporting that fundamentally altered how funds operate." — Source: Value Investing with Legends

- On Data Advantages: "Alternative data is no longer an edge; it is table stakes. If you aren't tracking credit card receipts and satellite imagery, you are operating at a deficit." — Source: Capital Allocators

- On the Decision to Close: "Closing a fund is never easy, but when market dynamics shift so aggressively that a rigorous bottom-up process struggles to generate the expected premium, returning capital is the intellectually honest choice." — Source: HedgeWeek

- On Staying Competitive: "To survive for decades, a firm cannot remain static. It must continuously iterate its research process while staying true to its core investment philosophy." — Source: Bloomberg Masters in Business

- On Legacy and Philosophy: "The ultimate measure of a firm is more than its annualized returns, but the rigor, integrity, and discipline it brought to the investment process over multiple market cycles." — Source: Value Investing with Legends