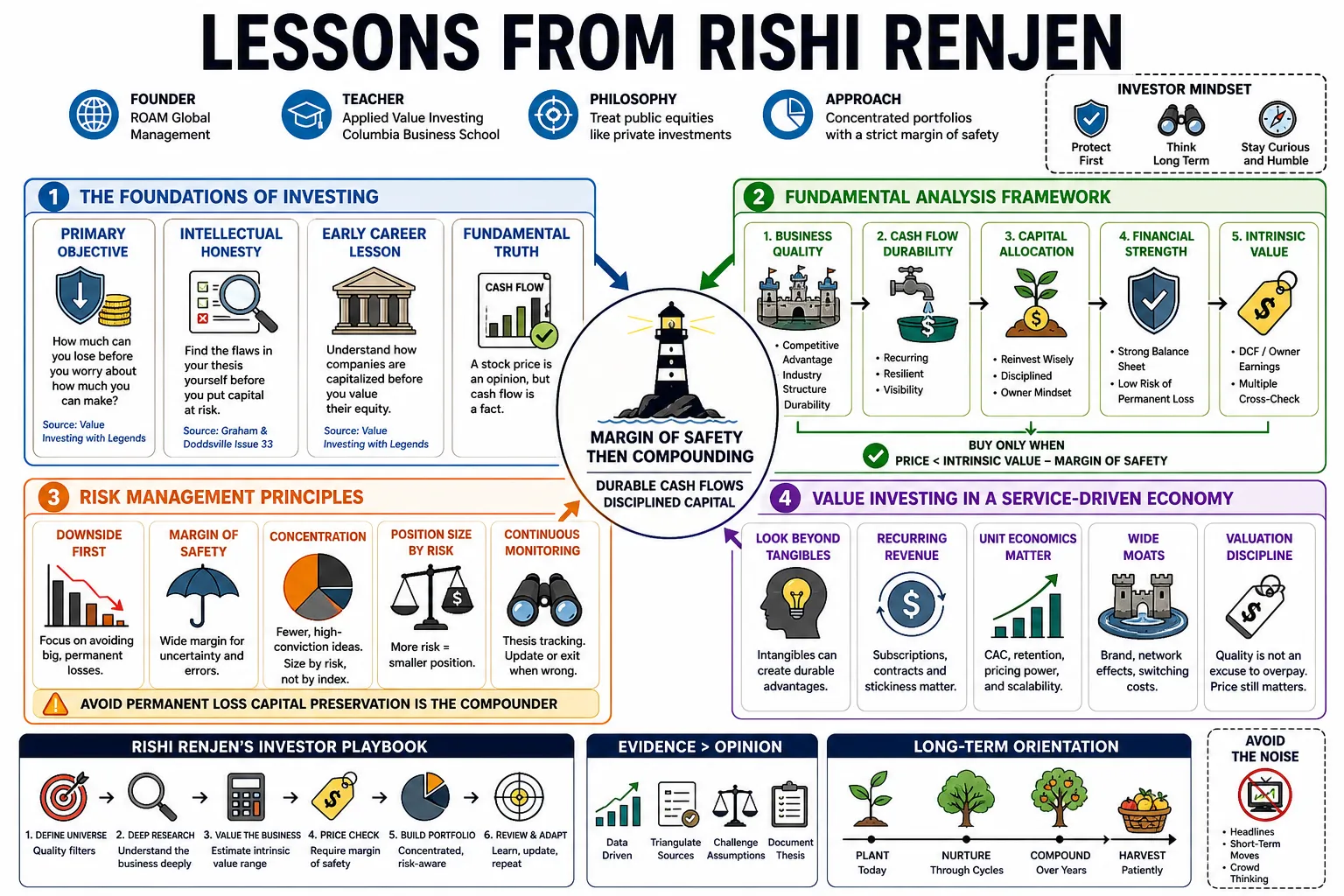

Lessons from Rishi Renjen

Rishi Renjen founded ROAM Global Management and teaches applied value investing at Columbia Business School. He treats public equities like private investments, running concentrated portfolios that demand a strict margin of safety. This profile breaks down his approach to fundamental analysis and risk management, along with his take on value investing in a service-driven economy.

Part 1: The Foundations of Investing

- On the primary objective: "Your first job as an investor is to establish how much money you can lose before you start worrying about how much you can make." — Source: Value Investing with Legends

- On intellectual honesty: "The market will eventually find the flaws in your thesis. It is cheaper and less painful to find them yourself before you put capital at risk." — Source: Graham & Doddsville Issue 33

- On early career lessons: "Starting in investment banking forces you to understand the mechanics of how companies are capitalized before you try to value their equity." — Source: Value Investing with Legends

- On fundamental truth: "A stock price is an opinion, but cash flow is a fact. We spend our time trying to understand the durability of those facts." — Source: Columbia Business School Lectures

- On the necessity of reading: "You cannot shortcut the process of reading primary documents. Summaries and sell-side notes tell you what everyone else already knows." — Source: Value Investing with Legends

- On patience: "The hardest thing to do in public markets is to sit on your hands and wait for a fat pitch when prices are moving every second." — Source: Graham & Doddsville Issue 33

- On market efficiency: "Markets are mostly efficient most of the time. You only get paid when there is a structural misunderstanding of a business model or a temporary dislocation in price." — Source: Value Investing with Legends

- On defining your circle of competence: "Knowing what you don't understand is a structural advantage. We ignore vast swaths of the market simply because we lack an edge there." — Source: Columbia Business School Lectures

- On the nature of edge: "Information edge is mostly gone. Analytical edge is hard to maintain. Behavioral edge—the ability to act rationally when others are emotional—is the most durable advantage." — Source: Value Investing with Legends

Part 2: Transitioning from Private Equity to Public Markets

- On the PE mindset: "In private equity, you underwrite a business assuming you own it for five years and cannot sell it. We try to bring that exact same underwriting standard to liquid markets." — Source: Value Investing with Legends

- On liquidity as a distraction: "The ability to trade a stock every day often tempts investors to react to noise rather than changes in fundamental value." — Source: Graham & Doddsville Issue 33

- On control versus influence: "Public market investors lack the control of private equity sponsors. You have to compensate for that by being incredibly rigorous about the management teams you partner with." — Source: Value Investing with Legends

- On capital allocation: "Without board control, we spend a massive amount of time analyzing a company's historical capital allocation. It is the clearest window into how they will treat minority shareholders." — Source: Columbia Business School Lectures

- On modeling: "A complex model does not reduce risk. In private equity, you learn that if a thesis requires a 50-tab spreadsheet to justify, it is probably too fragile." — Source: Value Investing with Legends

- On time horizons: "Arbitraging time is one of the few reliable ways to generate alpha. If the market is obsessing over the next quarter, we try to focus on normalized earnings three years out." — Source: Graham & Doddsville Issue 33

- On unit economics: "You have to decompose the business down to the unit level. If the core transaction doesn't make economic sense, scaling it won't fix the problem." — Source: Value Investing with Legends

- On due diligence: "We conduct primary research similar to a PE firm—speaking with former employees, competitors, and suppliers—to build a mosaic that goes beyond reported financials." — Source: Columbia Business School Lectures

- On exit multiples: "Never base a thesis on multiple expansion. If an investment only works because you assume someone will pay a higher multiple later, you are speculating, not investing." — Source: Value Investing with Legends

- On structural barriers: "Private equity teaches you to look for barriers to entry. In public markets, those barriers are often less obvious but equally necessary to protect returns on capital." — Source: Graham & Doddsville Issue 33

Part 3: Margin of Safety and Risk Management

- On defining safety: "Margin of safety is not just a low valuation. It is the combination of a defensible balance sheet, recurring cash flows, and a price that bakes in bad news." — Source: Value Investing with Legends

- On downside protection: "We spend the first half of any investment meeting trying to figure out how a position can permanently impair capital. If we survive that conversation, we talk about upside." — Source: Graham & Doddsville Issue 33

- On leverage: "Debt introduces path dependency. A great business can still go bankrupt if it has the wrong capital structure during a temporary downturn." — Source: Columbia Business School Lectures

- On position sizing as risk control: "Your largest positions should not necessarily be the ones with the highest upside. They should be the ones with the narrowest range of potential outcomes." — Source: Value Investing with Legends

- On short selling: "Shorting requires a completely different psychological makeup. The math works against you, and you are fighting the natural upward drift of markets." — Source: Graham & Doddsville Issue 33

- On take-out risk: "When you short a company, the greatest risk isn't that their earnings recover. The greatest risk is that a larger competitor buys them out for strategic reasons at a massive premium." — Source: Value Investing with Legends

- On the danger of valuation shorts: "Shorting a stock simply because it is expensive is a quick way to lose money. You need a specific catalyst or structural deterioration." — Source: Columbia Business School Lectures

- On admitting mistakes: "The thesis drift is the enemy of returns. If the reason you bought the stock is no longer true, you have to sell it, regardless of the price." — Source: Value Investing with Legends

- On macro risks: "We don't bet on macro outcomes, but we stress-test every portfolio company against severe macro shocks to ensure they can survive." — Source: Graham & Doddsville Issue 33

- On avoiding zeroes: "Compounding capital requires avoiding permanent losses. A 50% loss requires a 100% gain just to get back to even." — Source: Columbia Business School Lectures

Part 4: Evolving Value in a Service Economy

- On the changing nature of assets: "Traditional value investing relied heavily on tangible assets. Today, the most valuable assets are often intangible—networks, software, and brand equity." — Source: Barron's Interview

- On GAAP limitations: "Accounting rules were built for a manufacturing economy. They force companies to expense investments in customer acquisition and software that actually create long-term value." — Source: Value Investing with Legends

- On adjusting the lens: "You cannot use a 1950s Graham and Dodd framework on a modern SaaS business. You have to reconstruct the income statement to separate maintenance capex from growth investments." — Source: Columbia Business School Lectures

- On network effects: "A strong network effect is the modern equivalent of a physical moat. It creates a barrier to entry that requires an enormous amount of capital to breach." — Source: Value Investing with Legends

- On switching costs: "In service economies, high switching costs are often invisible on the balance sheet but show up clearly in customer retention rates and pricing power." — Source: Graham & Doddsville Issue 33

- On evaluating growth: "Growth destroys value if the return on invested capital is below the cost of capital. We only care about growth that is highly accretive." — Source: Barron's Interview

- On tech as a value sector: "Technology is no longer a separate sector; it is a horizontal layer across the entire economy. Value investors who ignore tech do so at their own peril." — Source: Value Investing with Legends

- On the illusion of cheapness: "A dying legacy business trading at five times earnings is often a value trap, not a bargain. Price is irrelevant if terminal value is zero." — Source: Columbia Business School Lectures

- On recurring revenue: "The transition from transactional sales to subscription models has fundamentally lowered the risk profile of many businesses, justifying higher normalized multiples." — Source: Barron's Interview

Part 5: Portfolio Concentration and Sizing

- On the purpose of concentration: "If you truly understand a business and have a high degree of conviction, it makes no sense to hold 100 names. We concentrate capital in our best ideas." — Source: Value Investing with Legends

- On diversification: "Diversification is often a substitute for doing the work. You need enough names to protect against idiosyncratic risk, but few enough to generate outperformance." — Source: Graham & Doddsville Issue 33

- On sizing criteria: "Position sizing is a function of the quality of the business, the width of the moat, and the depth of the discount to intrinsic value." — Source: Columbia Business School Lectures

- On scaling into positions: "We rarely buy a full position on day one. We prefer to build a position over time as management executes and our thesis is validated." — Source: Value Investing with Legends

- On averaging down: "You have to distinguish between a stock that is down because the market is volatile, and a stock that is down because the business is broken. We only average down on the former." — Source: Graham & Doddsville Issue 33

- On portfolio turnover: "High turnover creates tax friction and behavioral mistakes. We aim to hold our core longs for multiple years to let compounding do the heavy lifting." — Source: Value Investing with Legends

- On trimming winners: "Selling a great business simply because it hit your initial price target is a common mistake. If the intrinsic value is growing faster than the stock price, you hold." — Source: Columbia Business School Lectures

- On cash balances: "Cash is the residual of an investment process, not a top-down asset allocation decision. If we cannot find ideas that meet our hurdle rate, cash builds naturally." — Source: Value Investing with Legends

- On correlation: "When you run a concentrated book, you have to be highly aware of factor correlations. You don't want ten distinct stock ideas that all collapse if interest rates rise." — Source: Graham & Doddsville Issue 33

- On conviction: "Conviction is built in the library, not on the trading floor. The depth of your research is what allows you to hold through painful drawdowns." — Source: Value Investing with Legends

Part 6: Building an Analyst-First Firm Culture

- On flat structures: "Good ideas do not care about titles. An analyst straight out of business school should feel empowered to challenge the portfolio manager if the data supports their view." — Source: Graham & Doddsville Issue 33

- On the role of debate: "We institutionalize dissent. If everyone in the room agrees on an idea immediately, we probably haven't looked hard enough at the bear case." — Source: Value Investing with Legends

- On hiring analysts: "I look for intellectual curiosity and a tolerance for ambiguity. The market rarely provides clear answers, so you need people who are comfortable operating in gray areas." — Source: Columbia Business School Lectures

- On specialization: "Sector focus is critical. You cannot parachute into a complex industry on a Tuesday and expect to have an edge over someone who has studied it for ten years." — Source: Value Investing with Legends

- On the danger of consensus: "If your thesis relies on the exact same drivers that the sell-side consensus relies on, you don't have a variant perception. You just have beta." — Source: Graham & Doddsville Issue 33

- On evaluating talent: "The best analysts are the ones who update their priors quickly when presented with new evidence, rather than fighting to defend their original model." — Source: Columbia Business School Lectures

- On ownership: "Analysts must own their ideas from start to finish. You want a culture where people treat the firm's capital exactly as they would treat their own savings." — Source: Value Investing with Legends

- On continuous learning: "The market is a constantly adapting machine. The moment you stop reading and updating your framework, your edge begins to decay." — Source: Graham & Doddsville Issue 33

- On process over outcome: "We judge decisions based on the quality of the process, not the outcome. You can lose money on a good decision and make money on a bad one." — Source: Value Investing with Legends

Part 7: Assessing Management and Moats

- On management quality: "A bad management team can destroy a great moat over time. We want managers who think like owners, not employees." — Source: Graham & Doddsville Issue 33

- On incentive structures: "Proxy statements are mandatory reading. Show me how a CEO is compensated, and I will show you exactly what decisions they are going to make." — Source: Columbia Business School Lectures

- On insider ownership: "We look for alignment. When the management team has a significant portion of their net worth tied up in the common equity, our interests are naturally aligned." — Source: Value Investing with Legends

- On capital return: "A management team's willingness to buy back stock when it is cheap, and pay special dividends when they lack reinvestment opportunities, is the ultimate test of capital discipline." — Source: Graham & Doddsville Issue 33

- On acquisitions: "Serial acquirers are dangerous. Integration risk is consistently underestimated, and the premiums paid often destroy shareholder value." — Source: Value Investing with Legends

- On competitive advantage: "A true moat allows a company to raise prices without losing market share. If a company claims to have a moat but margins are shrinking, the moat is an illusion." — Source: Columbia Business School Lectures

- On industry structure: "We prefer to invest in oligopolies where the players compete rationally, rather than highly fragmented industries engaged in constant price wars." — Source: Graham & Doddsville Issue 33

- On disruption: "You have to ask how a business can be killed. If a company relies on an distribution channel that is being digitized, you cannot value it based on historical cash flows." — Source: Value Investing with Legends

- On corporate culture: "Culture is an intangible asset that rarely shows up in models, but it is often the deciding factor in whether a company successfully navigates a crisis." — Source: Columbia Business School Lectures

- On ROIC: "Return on invested capital is the single most important metric for evaluating a business over a decade. High ROIC covers up a lot of other mistakes." — Source: Value Investing with Legends

Part 8: Teaching and Mentorship

- On the purpose of teaching: "Teaching forces you to clarify your own thoughts. You cannot explain a complex valuation framework to sharp MBA students if your own understanding is muddy." — Source: Graham & Doddsville Issue 33

- On student stock pitches: "The most common mistake students make is pitching a great company without explaining why the current stock price is a mispricing. A good company is not automatically a good stock." — Source: Columbia Business School Lectures

- On learning from history: "We force students to study past cycles. The specific technologies change, but human psychology—the fear and greed that drive mispricings—has not changed in a century." — Source: Value Investing with Legends

- On the value of simplicity: "If you cannot explain your investment thesis to someone outside the industry in three sentences, you do not understand it well enough to invest." — Source: Columbia Business School Lectures

- On filtering noise: "We teach students how to ignore the daily macroeconomic headlines and focus relentlessly on the microeconomics of the specific business they are researching." — Source: Graham & Doddsville Issue 33

- On intellectual humility: "The best investors I have mentored are the ones who say 'I don't know' most frequently. Arrogance in this business is highly correlated with catastrophic losses." — Source: Value Investing with Legends

- On the apprenticeship model: "Investing is not a science you can learn purely from a textbook. It is a craft that requires apprenticeship, observation, and repetition under experienced practitioners." — Source: Columbia Business School Lectures

- On evolving frameworks: "The core principles of Graham and Dodd—buying at a discount to intrinsic value—are permanent. But the application of those principles must evolve as the economy changes." — Source: Value Investing with Legends