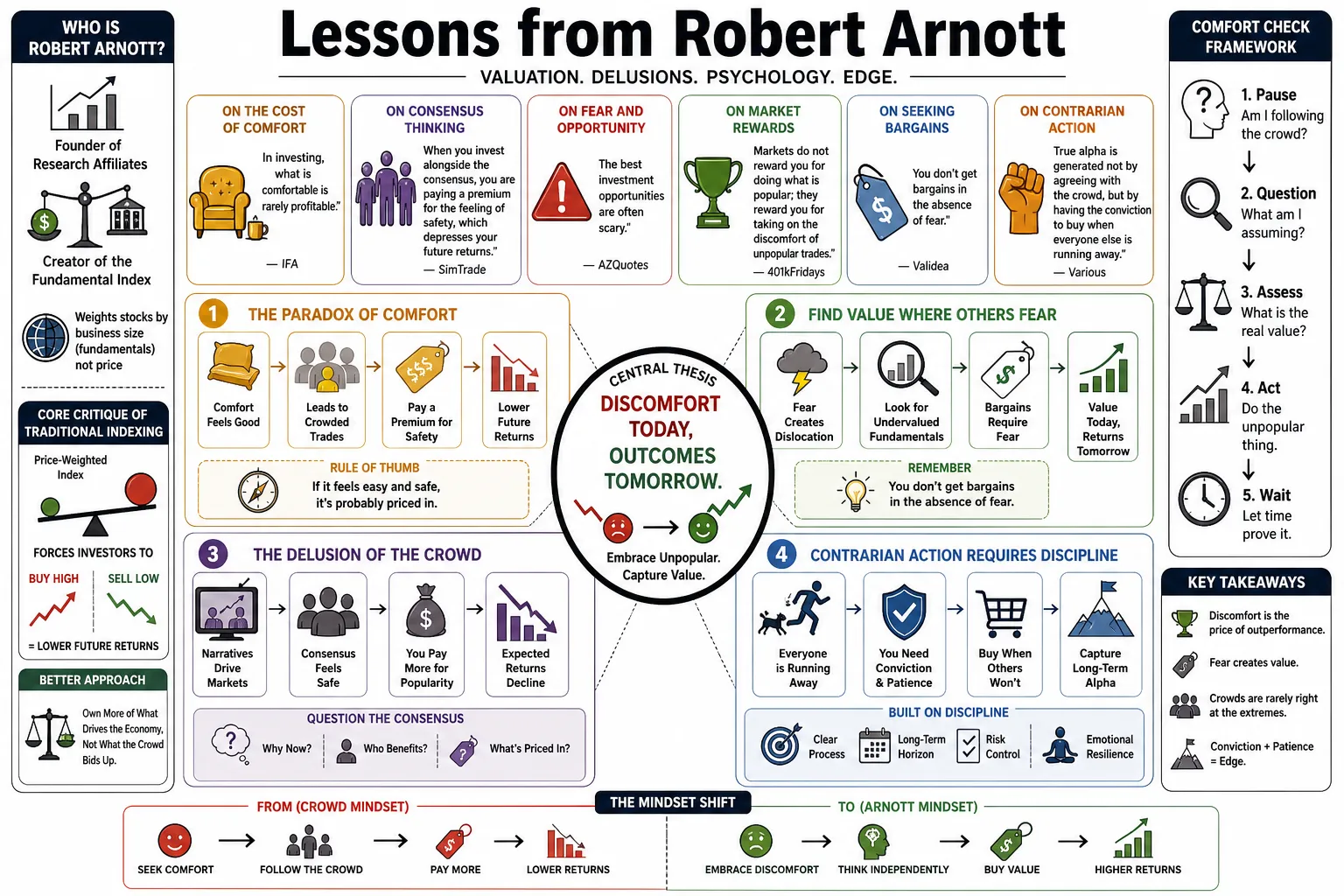

Robert Arnott founded Research Affiliates and created the Fundamental Index, a system that weights stocks by business size rather than market price. He is known for arguing that traditional index funds force investors to buy high and sell low, and that the best market opportunities usually feel deeply uncomfortable. This profile organizes his core arguments on valuation, market delusions, and investor psychology.

Part 1: The Paradox of Comfort

- On the Cost of Comfort: "In investing, what is comfortable is rarely profitable." — Source: IFA

- On Consensus Thinking: "When you invest alongside the consensus, you are paying a premium for the feeling of safety, which depresses your future returns." — Source: SimTrade

- On Fear and Opportunity: "The best investment opportunities are often scary." — Source: AZQuotes

- On Market Rewards: "Markets do not reward you for doing what is popular; they reward you for taking on the discomfort of unpopular trades." — Source: 401kFridays

- On Seeking Bargains: "You don't get bargains in the absence of fear." — Source: Validea

- On Contrarian Action: "True alpha is generated not by agreeing with the crowd, but by having the conviction to buy when everyone else is selling." — Source: SimTrade

- On the Danger of Popularity: "An asset's popularity is its own worst enemy, as it attracts capital until the price is completely detached from underlying fundamentals." — Source: LiveMint

- On Emotional Friction: "The investments that make your stomach churn are often the ones most likely to produce outsized long-term gains." — Source: The Investor's Podcast

- On Short-Term vs. Long-Term Profit: "Buying what is comfortable may yield short-term profits, but it is mathematically destined to disappoint over longer horizons." — Source: 401kFridays

Part 2: Fundamental Indexing and Smart Beta

- On Market-Cap Weighting: "With cap weighting, the more expensive the stock, the bigger its weight in your portfolio. Why do we want to do that? It doesn't make intuitive sense." — Source: REIT.com

- On the Flaw of Traditional Indices: "Cap-weighted index funds force investors to systematically buy high and sell low by automatically allocating more capital to overvalued companies." — Source: ETF.com

- On the Smart Beta Trap: "How can 'smart beta' go horribly wrong? It happens when investors chase a strategy until its valuations are artificially inflated." — Source: Research Affiliates

- On the Economic Footprint: "Fundamental indexing involves selecting companies based on their fundamental economic footprint rather than selecting and weighting by market cap." — Source: REIT.com

- On Index Evolution: "Indexes were originally designed to measure markets, not to influence them. As indexing evolved from measurement to investment, however, the act of replication began to influence the market itself." — Source: Research Affiliates

- On Price Disconnects: "If the price is wrong, it can be really dumb." — Source: WealthTrack

- On Measuring Size: "A company's true weight should be determined by objective metrics like book value, cash flow, dividends, and sales, not by the market's shifting mood." — Source: ETF.com

- On Valuation of Factors: "A factor strategy's success is deeply dependent on whether the factor itself is trading rich or trading cheap at the time of investment." — Source: WealthManagement

- On Artificial Expectations: "Many quantitative strategies fail because their backtests create expectations that cannot be met when live money floods the trade." — Source: Validea

- On the Performance Chase: "The structure of cap-weighted indexing creates an inescapable performance chase that inherently punishes long-term holders during market corrections." — Source: Ritholtz

Part 3: The Big Market Delusion

- On Industry-Wide Rises: "The 'big market delusion' is when all firms in an evolving industry rise together, although as competitors ultimately some will win and some will lose." — Source: Research Affiliates

- On Innovation and Competition: "Investors often treat new disruptive markets as if every participant will dominate, forgetting the basic rule that disruptors get disrupted." — Source: Morningstar

- On the Fallacy of Composition: "Just because a macro trend or new technology will reshape the world does not mean every company in that sector will be a profitable investment." — Source: Research Affiliates

- On the Marginal Buyer: "During a market delusion, the marginal buyer abandons traditional valuation metrics entirely in favor of compelling growth narratives." — Source: Rational Reminder

- On Shorting Bubbles: "One should never sell a bubble short, because it can last longer and go further than we can possibly imagine." — Source: Cornell Capital

- On the Social Benefit of Delusions: "While market delusions wipe out investor capital, they actually provide a net social benefit by rapidly funding the infrastructure for new technologies." — Source: PM Research

- On Electric Vehicles: "The EV market became a textbook example of the delusion, where the combined market cap of EV startups vastly exceeded the total addressable market of the entire auto industry." — Source: Kitces

- On the Allure of Big Markets: "The promise of finding the next Microsoft or Apple causes investors to bid up entire sectors without any regard for competitive friction." — Source: PWL Capital

- On Price Corrections: "A big market delusion only ends when the industry matures and the collective valuation of the sector is forced to reconcile with actual cash flows." — Source: Substack

Part 4: Fear, Not Risk

- On Traditional Risk Models: "Traditional asset pricing models fail because they rely on tidy math and objective volatility rather than the messy reality of human emotion." — Source: Quantpedia

- On Human Emotion: "Market pricing is driven not by a sterile calculation of standard deviation, but by the visceral tension between the fear of loss and the fear of missing out." — Source: Coinbase

- On Directional Volatility: "Investors do not actually dislike volatility; they explicitly desire upside volatility and only panic over downside volatility." — Source: Quantpedia

- On the DAPM: "The Deranged Asset Pricing Model suggests that asset prices diverge from fundamental value entirely due to collective behavioral overreactions." — Source: Treussard

- On High Prices and FOMO: "When prices are highest, objective risk is highest, yet investors pile in because their fear of missing out overrides their fear of loss." — Source: QuantSeeker

- On Market Panics: "During crashes, assets are fundamentally cheap and objective risk is low, but the acute fear of further loss prevents investors from buying." — Source: Treussard

- On the Illusion of Safety: "Assets that exhibit low volatility in the short term often mask massive structural risks that only reveal themselves during liquidity crises." — Source: Podbay

- On Temperament: "The difference between a good investor and a poor one is not their ability to model risk, but their capacity to manage their own fear." — Source: Economic Times

- On Emotional Cycles: "The market is a continuous cycle of transitioning from the fear of losing money to the fear of looking foolish for missing the rally." — Source: QuantSeeker

Part 5: Value vs. Growth Investing

- On Growth Narratives: "The stories driving growth stocks are often entirely true, but they are also always 100 percent reflected in current share prices." — Source: ETF.com

- On the Danger of High Multiples: Arnott warned on Bloomberg that making U.S. growth the core holding had become a steamroller trade: value was near its cheapest levels while expensive growth concentration left little room for error. — Reference: MarketScreener mirror of Arnott Bloomberg interview on U.S. growth concentration

- On the Value Cycle: "The past ten years have been tremendous for growth stocks, but we do not expect the trends that defined the last decade to persist through the next." — Source: Vanguard

- On the Horizon of Value: "On a one-year horizon, it's a coin toss. On a 10-year horizon, it's a slam dunk." — Source: ETF.com

- On Unloved Assets: "Value investing is never truly dead; it simply becomes deeply unloved, which is precisely what sets up the mechanism for future outperformance." — Source: ETF Trends

- On Valuation Gaps: "When the valuation gap between value and growth reaches historic extremes, a mean reversion becomes a mathematical inevitability rather than just a theory." — Source: Business Insider

- On Paying for Growth: "Investors systematically overpay for the comfort of holding companies with fast-growing earnings, ignoring the price they are paying for that growth." — Source: Investing.com

- On Cap-Weighted Bias: "Because cap-weighted indices automatically buy more of a stock as its price goes up, they systematically tilt the entire passive market toward growth at the worst possible times." — Source: The Idea Farm

- On Tech Dominance: In the Money Maze interview notes, Arnott argues that narratives around much-loved technology companies may already be reflected in their share prices, while profound value opportunities sit outside the crowded U.S. tech trade. — Reference: Money Maze interview notes on tech narratives, Nvidia, and value opportunities

- On the Persistence of Value: "Despite periodic and painful dry spells, buying companies for less than their intrinsic worth remains the most reliable long-term engine of compound wealth." — Source: ETF.com

Part 6: The "Too Big to Succeed" Phenomenon

- On Market Leaders: "The very business practices that propel an organization to number one become unacceptable if you're wearing the yellow jersey. Being number one means always having to say you're sorry." — Source: StrapiApp

- On the Top Dog Penalty: "Sector leaders generally underperform the average stock in their own sector by roughly 3 to 4 percent per year over the following decade." — Source: InvestorPlace

- On Valuation and Size: "You don't get to the top of the sector or top of the market without trading at high multiples. For that reason, these companies are likely to disappoint just on a valuation basis." — Source: Ritholtz

- On the Winner's Curse: "Reaching the absolute top of a market cap ranking is often a curse, as it triggers a cascade of competitive and regulatory forces aimed at tearing the leader down." — Source: Morningstar

- On Regulatory Targets: "Once a company becomes the undisputed giant of its industry, it inevitably moves into the crosshairs of government regulators and antitrust lawsuits." — Source: High Probability Advisors

- On Diseconomies of Scale: "As a corporation scales to become the market leader, it sacrifices the agility that made it great and drowns in internal bureaucracy and fixed costs." — Source: European Financial Review

- On the Size Effect: "The historical outperformance of smaller companies is largely driven by the structural inability of the very largest companies to maintain their peak growth rates." — Source: Stingy Investor

- On Paying for the Past: "When you buy the largest company in the world, you are almost always paying a massive premium for its past success, leaving little room for future upside." — Source: Meb Faber

- On Complacency: "Top dogs often breed internal complacency, allowing smaller, nimbler competitors to quietly steal market share while the leader defends its legacy products." — Source: European Financial Review

Part 7: Market Cycles and Mean Reversion

- On Historical Perspective: "For most long-term investors, bull markets are not nearly as beneficial, and bear markets not nearly as damaging as most investors seem to think." — Source: Goodreads

- On the Cost of Bull Markets: "A bull market raises the asset value, but delivers a proportionate reduction in the prospective real yields that the portfolio can deliver from that point." — Source: Goodreads

- On the Limits of History: Arnott and Peter Bernstein argue that investors should estimate the equity risk premium from forward-looking cash flows and prevailing valuations, not simply extrapolate the unusually strong historical U.S. equity record. — Reference: Arnott and Bernstein paper on forward-looking equity risk premiums

- On the Twenty-Year Myth: On the Meb Faber Show, Arnott points out that 20-year Treasury bonds beat the S&P 500 from the tech-bubble peak, a reminder that long horizons do not erase the damage from buying stocks at stratospheric valuations. — Reference: Meb Faber transcript on time horizons and stocks versus bonds after the tech bubble

- On Extreme Spreads: Arnott frames valuation spreads as cyclical opportunities: in the Meb Faber transcript he contrasts expensive U.S. equities with much cheaper developed international, emerging-market, and emerging-market value exposures. — Reference: Meb Faber transcript on U.S., EAFE, emerging-market, and EM value valuations

- On International Value: Arnott describes international and emerging-market value as unusually attractive because U.S. equities traded at far higher Shiller P/E multiples while EM value was available at a steep discount to U.S. valuations. — Reference: Meb Faber transcript on emerging-market value discounts and expected returns

- On Gravity in Finance: "Valuation is the closest thing to gravity in the financial markets; it can be defied for a season, but it cannot be escaped over a cycle." — Source: Masters in Business

- On Data Mining: "The quantitative finance industry is plagued by backtested models that simply data-mine historical anomalies rather than relying on robust economic principles." — Source: Research Affiliates

- On AI in Investing: "While artificial intelligence offers productivity gains, investors must beware of AI hallucinations and ensure that human judgment remains the ultimate sanity check on systematic models." — Source: Research Affiliates

Part 8: Investor Psychology and Discipline

- On Portfolio Construction: "Design a portfolio you are not likely to trade... try to build a portfolio that you can live with for a long, long time." — Source: IFA

- On Trading Friction: "The more an investor tinkers with their allocation in response to market news, the more they guarantee their own underperformance." — Source: LiveMint

- On Human Nature: "The greatest enemy of a solid investment plan is not the federal reserve or the economy, but the investor's own biological hardwiring." — Source: The Investor's Podcast

- On Market Noise: "Financial media is designed to agitate investors into action, but successful investing requires the discipline to sit quietly and do absolutely nothing." — Source: Skyview Wealth

- On the Herd Mentality: "It is psychologically exhausting to stand apart from the herd, which is exactly why the market so richly compensates those who can endure the isolation." — Source: Maven Adviser

- On False Certainty: "The market consistently punishes those who invest based on what they think they know for certain, while rewarding those who acknowledge their own ignorance." — Source: Masters in Business

- On Patience: "True investment discipline is the willingness to look foolish for an extended period of time while waiting for a thesis to play out." — Source: Excess Returns

- On Avoiding the Hype: "If an investment strategy is being discussed at cocktail parties and on the front page of newspapers, the opportunity to generate outsized returns has already passed." — Source: Research Affiliates

- On Self-Awareness: "Before analyzing a stock's balance sheet, an investor must first analyze their own capacity to stomach a fifty percent drawdown without capitulating." — Source: Economic Times

- On the Ultimate Goal: "The purpose of investing is not to be proven right on every trade, but to construct a durable process that survives your own inevitable mistakes." — Source: Rational Reminder