Bob Robotti is the founder and Chief Investment Officer of Robotti & Company Advisors, where he has practiced a bottom-up, fundamental value investing strategy for over four decades. He is best known for his "restoration of the fallen" thesis, which focuses on identifying deeply discounted companies in neglected or cyclical industries that are poised for recovery. This profile collects his core principles on capital allocation, industrial economics, and the psychological endurance required to hold unpopular investments.

Part 1: The Foundation of Value Investing

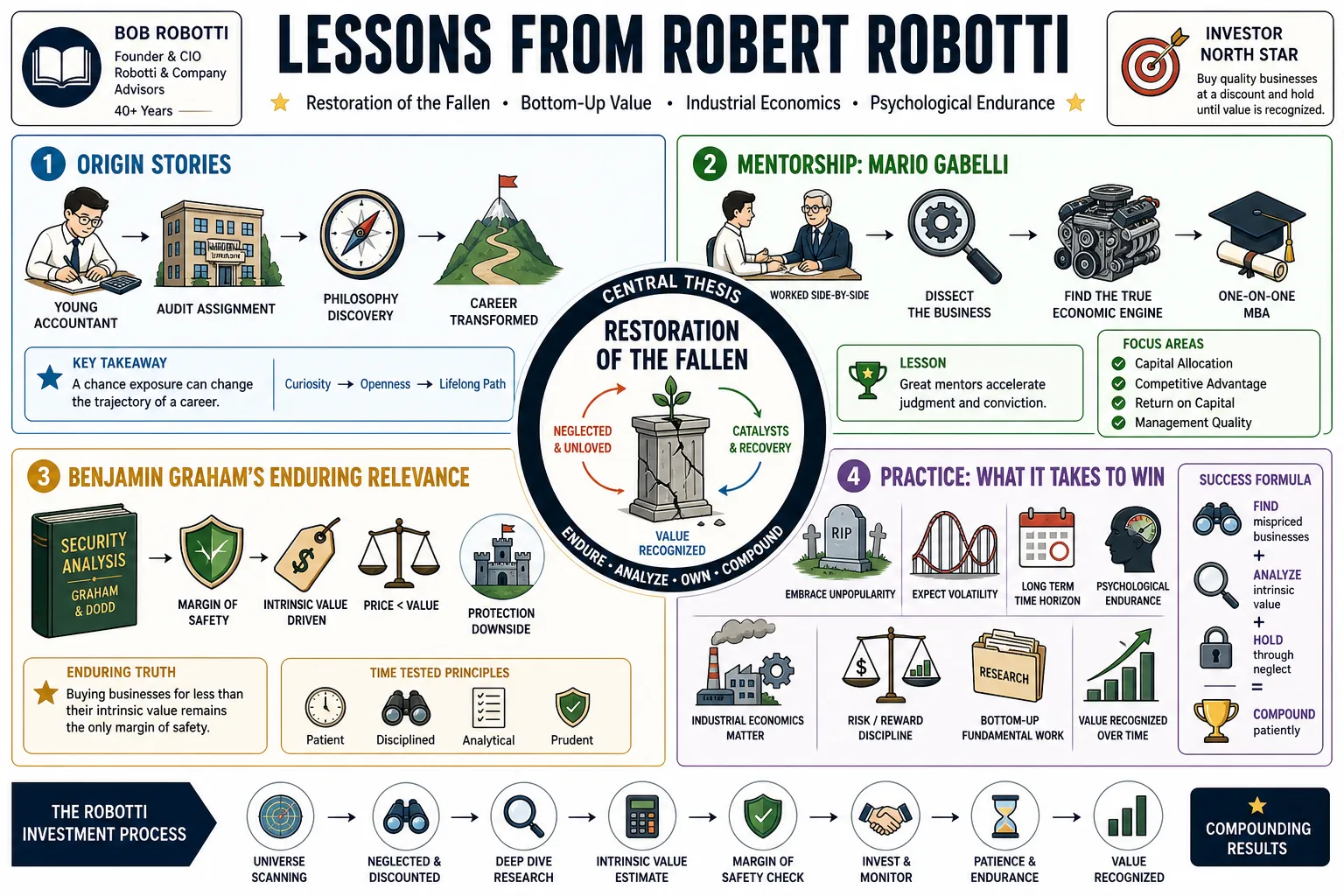

- On Origin Stories: Robotti traces his entry into value investing to early accounting work auditing firms such as Tweedy, Browne, which exposed him to underfollowed, undervalued companies. — Reference: Value Investing with Legends episode on Robotti's accounting roots

- On Mentorship: "Working alongside Mario Gabelli early in my career was essentially a one-on-one MBA in understanding how to dissect a business and uncover its true economic engine." — Source: Graham & Doddsville

- On Benjamin Graham's Enduring Relevance: "The core tenets of Graham and Dodd haven't expired. Buying businesses for less than their intrinsic value remains the only margin of safety that protects you from an unknowable future." — Source: MOI Global

- On Active vs. Passive Management: "After extended periods where passive indexing dominates, the market inherently creates massive inefficiencies. The future belongs to active stock pickers willing to look where the indices aren't." — Source: The Investor's Podcast Network

- On Defining Value: "Value isn't just a low price-to-book ratio. It's understanding the cash-generating capability of an asset that the rest of the market has decided is permanently broken." — Source: Robotti & Company Advisors

- On Accounting as a Foundation: His accounting background remains central to the process: the Value Investing with Legends episode frames practical accounting as a formative tool for analyzing discounted public companies. — Reference: Value Investing with Legends episode on practical accounting

- On the Role of Inflation: "We are transitioning into a macroeconomic environment where inflation and structural economic factors will drive returns, making the ability to own hard assets and pricing power essential." — Source: Hedge Fund Alpha

- On Avoiding the Consensus: "If you are buying what everyone else is buying, you are paying a premium for comfort. We look for discomfort." — Source: Latticework

- On the Nature of Financial Markets: "Progress is cumulative in science and engineering, but it remains decidedly cyclical in finance." — Source: MOI Global

Part 2: The "Restoration of the Fallen"

- On the Horace Quote: "'Many shall be restored that now are fallen, and many shall fall that now are in honor.' That line from Graham's Security Analysis perfectly encapsulates our approach to neglected industries." — Source: The Investor's Podcast Network

- On Industry Depressions: "Prolonged downturns are cathartic. They brutally force consolidation, eliminate the weakest players, and set the stage for outsized returns for the survivors." — Source: Latticework

- On Buying 'Ugly Ducklings': "We actively look for the ugly ducklings—companies operating in sectors that are so out-of-favor that institutional investors are prohibited by mandate or peer pressure from owning them." — Source: Latticework

- On the Value of Neglect: "Neglect is the value investor's best friend. When an entire sector is starved of capital and attention, the few remaining assets become drastically mispriced." — Source: Buy Side Digest

- On Survivor Economics: "If a company can simply survive a ten-year bear market in its industry, it will likely emerge with a larger market share and significantly increased earnings power when the cycle turns." — Source: The Business Brew

- On Fire-Sale Assets: "During a severe industry down-cycle, disciplined operators can acquire productive assets for pennies on the dollar compared to their replacement cost." — Source: Robotti & Company Advisors

- On Institutional Constraints: "Large funds cannot buy illiquid, beaten-down small caps. Their size constraints create a structural inefficiency that nimble, bottom-up investors can exploit." — Source: The Investor's Podcast Network

- On Identifying the Turn: "You don't need to perfectly time the bottom. You just need to ensure the balance sheet is strong enough to survive until the inevitable restoration occurs." — Source: MOI Global

- On the Illusion of Permanent Decline: "Wall Street frequently mistakes a severe cyclical trough for terminal secular decline. That misdiagnosis is where the greatest opportunities lie." — Source: Yet Another Value Podcast

Part 3: Cyclicals and the Capital Cycle

- On Capital Destruction: "In capital-intensive businesses, high prices attract too much capital, which destroys returns. Low prices starve the industry of capital, which eventually drives the next boom." — Source: Richer, Wiser, Happier

- On Replacement Costs: "When you can buy existing, functional capacity at a steep discount to what it would cost to build it today, you have found a margin of safety." — Source: Latticework

- On Supply-Side Dynamics: "Investors spend too much time forecasting demand, which is unpredictable. We focus on supply, which you can actually track by watching capital expenditures and industry capacity." — Source: The Business Brew

- On Embracing Cyclicality: "Rather than running from cyclicals, we embrace them. We want to own the lowest-cost producer when the commodity price is below the marginal cost of production." — Source: Richer, Wiser, Happier

- On the Metamorphosis of the Old Economy: "Old economy businesses are undergoing a massive shift. Decades of underinvestment mean that when demand normalizes, the remaining suppliers have unprecedented pricing power." — Source: The Investor's Podcast Network

- On Creative Destruction: "Schumpeter’s creative destruction is not just about tech startups disrupting incumbents; it is also about down-cycles ruthlessly clearing out inefficient capacity in traditional industries." — Source: MOI Global

- On Capacity Exits: "The most bullish signal for a cyclical business is when competitors start permanently retiring capacity and scrapping equipment." — Source: Yet Another Value Podcast

- On Normalizing Earnings: "You cannot value a cyclical business on peak earnings or trough earnings. You must calculate a normalized mid-cycle cash flow and pay a conservative multiple on that." — Source: Robotti & Company Advisors

- On the Danger of High Prices: "The cure for high prices is high prices. When profit margins in an industry look unsustainably high, capital will flood in and ruin the economics." — Source: The Investor's Podcast Network

- On Down-Cycle Acquisitions: "The best management teams in cyclical industries don't build new capacity during a boom; they buy distressed assets from bankrupt competitors during the bust." — Source: Graham & Doddsville

Part 4: Price, Value, and Market Psychology

- On Certainty and Mispricing: "When the market is absolutely certain that a business is doomed, the stock price reflects a 100% probability of failure. 'You wanna bet?' is the question I ask when I see that level of certainty." — Source: Latticework

- On Media Narratives: "You shouldn't believe everything that is written in the newspaper. Articles are often written by people with above-average writing skills who fundamentally misunderstand the core tenets of the business." — Source: Buy Side Digest

- On Tolerating Volatility: "Volatility is not risk; it is the price you pay for the opportunity to buy assets cheaply. Risk is the permanent impairment of capital." — Source: Robotti & Company Advisors

- On Contrarianism: Robotti's contrarianism is tied to market inefficiency rather than reflexive opposition: the episode describes his focus on cyclical industries and under-the-radar public firms. — Reference: Value Investing with Legends episode on contrarian market inefficiencies

- On Short-Term Noise: "The market is obsessed with quarterly earnings misses. We use that myopia to our advantage by extending our time horizon past the next three months." — Source: MOI Global

- On Market Inefficiencies: "Information is ubiquitous, but interpretation is not. The edge today comes from analyzing the exact same public data as everyone else but drawing a different, more accurate conclusion." — Source: The Business Brew

- On the Disconnect Between Price and Value: "Market prices are driven by liquidity and emotion in the short term. Over a five-year horizon, they are driven by the cash a business actually produces." — Source: Richer, Wiser, Happier

- On Herd Mentality: "Institutional imperatives often force portfolio managers to sell what is going down and buy what is going up, regardless of valuation. We do the exact opposite." — Source: The Investor's Podcast Network

- On Emotional Discipline: "The most difficult part of our job isn't the spreadsheet modeling; it is maintaining the psychological discipline to hold a position when the market tells you you're wrong for three straight years." — Source: Latticework

Part 5: Deep Research and Financial Forensics

- On Bottom-Up Analysis: "We don't start with a macro forecast. We start by looking at individual companies, and if we see a pattern of extreme value across an industry, that informs our macro view." — Source: Graham & Doddsville

- On Free Cash Flow: "EBITDA is an opinion; cash in the bank is a fact. We focus heavily on businesses that generate true, unencumbered free cash flow." — Source: Robotti & Company Advisors

- On Balance Sheet Safety: "A strong balance sheet is your primary defense mechanism against being wrong on the timing of a cyclical recovery. It buys you the time needed to be proven right." — Source: MOI Global

- On Pulling Research Threads: "Good research involves finding a loose thread and pulling on it until you understand the entire fabric of the industry, the competitors, and the supply chain." — Source: Robotti & Company Advisors

- On Evaluating Assets: "You have to go beyond the stated book value. What is the real liquidation value? What is the replacement cost? What would a strategic buyer pay for this specific facility?" — Source: Yet Another Value Podcast

- On Hidden Liabilities: The auditing thread matters because Robotti learned to connect accounting discipline with business analysis before committing capital to neglected public companies. — Reference: Value Investing with Legends episode on accounting discipline

- On Field Research: "You can't truly understand an industrial business just by reading 10-Ks in New York. You have to go to the plants, talk to the operators, and understand the physical reality of the assets." — Source: The Business Brew

- On Financial Complexity: "Beware of companies with excessively complex capital structures. Complexity is often used by management to obscure poor operational performance." — Source: Buy Side Digest

- On the Margin of Safety: "The margin of safety isn't a static number. It is a combination of a low purchase price, a conservative balance sheet, and a management team that won't destroy value." — Source: Latticework

Part 6: Patience and the Long-Term View

- On Delayed Gratification: "Value investing is the ultimate exercise in delayed gratification. You are planting seeds that may not bear fruit for half a decade." — Source: Tilson Funds

- On the '3-Second Rule': "There is no 3-second rule in investing. Reacting instantly to news headlines is a guaranteed way to destroy wealth; deliberate, thorough research takes time." — Source: Robotti & Company Advisors

- On Time Horizon Arbitrage: "The single biggest advantage we have over a hedge fund is our time horizon. We can comfortably sit in a dead-money stock for three years if the intrinsic value is growing." — Source: The Investor's Podcast Network

- On Weathering the Storm: "If you know you own a high-quality asset at a fraction of its worth, a 30% drawdown in the stock price should excite you, not panic you." — Source: MOI Global

- On Portfolio Turnover: "High turnover is the enemy of compounding. If you do the work upfront and buy correctly, the best action is usually to do absolutely nothing." — Source: Richer, Wiser, Happier

- On the Waiting Game: Patience is part of the edge in Robotti's style: the episode summary highlights patience, aligned incentives, and long-term success in neglected public companies. — Reference: Value Investing with Legends episode on patience and long-term success

- On Compounding: "True wealth is created by finding a business that can reinvest its cash flows at high rates of return and then leaving it alone to compound over decades." — Source: Graham & Doddsville

- On Ignoring the Fed: "Attempting to predict Federal Reserve interest rate decisions is a fool's errand. We focus on business fundamentals, which will ultimately dictate returns regardless of what the Fed does." — Source: Hedge Fund Alpha

- On Holding Through the Recovery: "The biggest mistake investors make in cyclicals is selling as soon as they get their money back. The real money is made by holding through the up-cycle." — Source: The Business Brew

- On Enduring Conviction: "Conviction isn't something you have on day one. It is built over years of following a company, understanding its capital cycle, and watching management execute." — Source: Latticework

Part 7: The North American Industrial Renaissance

- On the Energy Advantage: "North America possesses a durable, multi-decade competitive advantage simply because of our abundant, low-cost natural gas and energy infrastructure." — Source: Latticework

- On Reshoring Dynamics: "The shift of manufacturing back to North America isn't just a political talking point; it is a long-term trend driven by hard economic fundamentals and energy arbitrage." — Source: Buy Side Digest

- On Energy-Intensive Industries: "If you require massive amounts of energy to produce your product—like chemicals, fertilizers, or steel—North America is now the most rational place on earth to build a plant." — Source: Yet Another Value Podcast

- On Grassroots Macro: "We don't bet on macro trends from the top down. We arrived at our bullish view on North American industrials by looking bottom-up at the profit margins of individual chemical and manufacturing companies." — Source: Latticework

- On the Changing Global Cost Curve: "China’s historical cost advantages in manufacturing are eroding, while North America’s structural energy advantages have fundamentally reshaped the global supply curve." — Source: The Investor's Podcast Network

- On Building Materials: "The dynamics in sectors like homebuilding and lumber are fascinating because you have a structural housing deficit colliding with a consolidated supply chain." — Source: Robotti & Company Advisors

- On Industrial Policy: "Regardless of who is in the White House or what trade tariffs are implemented, the underlying economics of cheap domestic energy will drive capital investment in the U.S." — Source: Richer, Wiser, Happier

- On the Disconnect in Energy Stocks: "There has been a massive divergence between the actual cash flows of energy service companies and their public market valuations due to ESG mandates and institutional neglect." — Source: MOI Global

- On Regional Moats: "When a basic material like cement or aggregate is heavy and cheap, the transport cost creates a localized monopoly. That is a structural moat we love to own." — Source: The Business Brew

- On Capitalizing on the Renaissance: Robotti's industrial thesis centers on North American manufacturing advantages, with Latticework summarizing his case that cheap natural gas can fuel re-industrialization and demand for basic materials. — Reference: Latticework writeup on Robotti and neglected industrials

Part 8: Management, Capital Allocation, and Alignment

- On Assessing Management: "We want to partner with managers who think like owners, and the easiest way to verify that is to see if they have a significant portion of their own net worth invested in the stock." — Source: Graham & Doddsville

- On Capital Allocation Skills: "A CEO can be a brilliant operator, but if they destroy the cash they generate through empire-building acquisitions, the stock will be a terrible investment." — Source: Robotti & Company Advisors

- On Share Repurchases: "Buying back stock is only creating value if the stock is trading at a material discount to its intrinsic value. Otherwise, it is a destruction of shareholder capital." — Source: The Investor's Podcast Network

- On Collaborative Investing: "We don't view ourselves as hostile activists. We prefer collaborative investing—taking a significant stake and working constructively with management to optimize capital allocation." — Source: Buy Side Digest

- On Board Representation: "Sometimes the best way to ensure that a deeply undervalued company doesn't make a strategic error during a cyclical trough is to take a seat on the board of directors." — Source: MOI Global

- On Incentive Structures: "Show me the compensation proxy, and I will tell you how the management team will behave. If they are paid purely for revenue growth, they will sacrifice margins." — Source: Latticework

- On Opportunistic Reinvestment: "The highest returning capital allocation decision a management team can make is often heavily reinvesting in their own core business when their competitors are retreating." — Source: Yet Another Value Podcast

- On Dividend Policies: "A rigid dividend policy can be dangerous for a cyclical business. We prefer management teams that have the flexibility to deploy cash where the return is highest at that specific point in the cycle." — Source: The Business Brew

- On the Ultimate Margin of Safety: For Robotti, price is only one part of the setup: the episode summary pairs capital allocation, aligned incentives, and management quality as central to his long-term investing framework. — Reference: Value Investing with Legends episode on capital allocation and management quality