Lessons from Ross Glotzbach

Ross Glotzbach is the CEO and Head of Research at Southeastern Asset Management, the firm behind the Longleaf Partners Funds. He relies on a strict "Business, People, Price" framework and engaged ownership to push companies to realize their underlying value. This compilation breaks down his approach to building concentrated portfolios, allocating capital, and maintaining the discipline required for long-term investing.

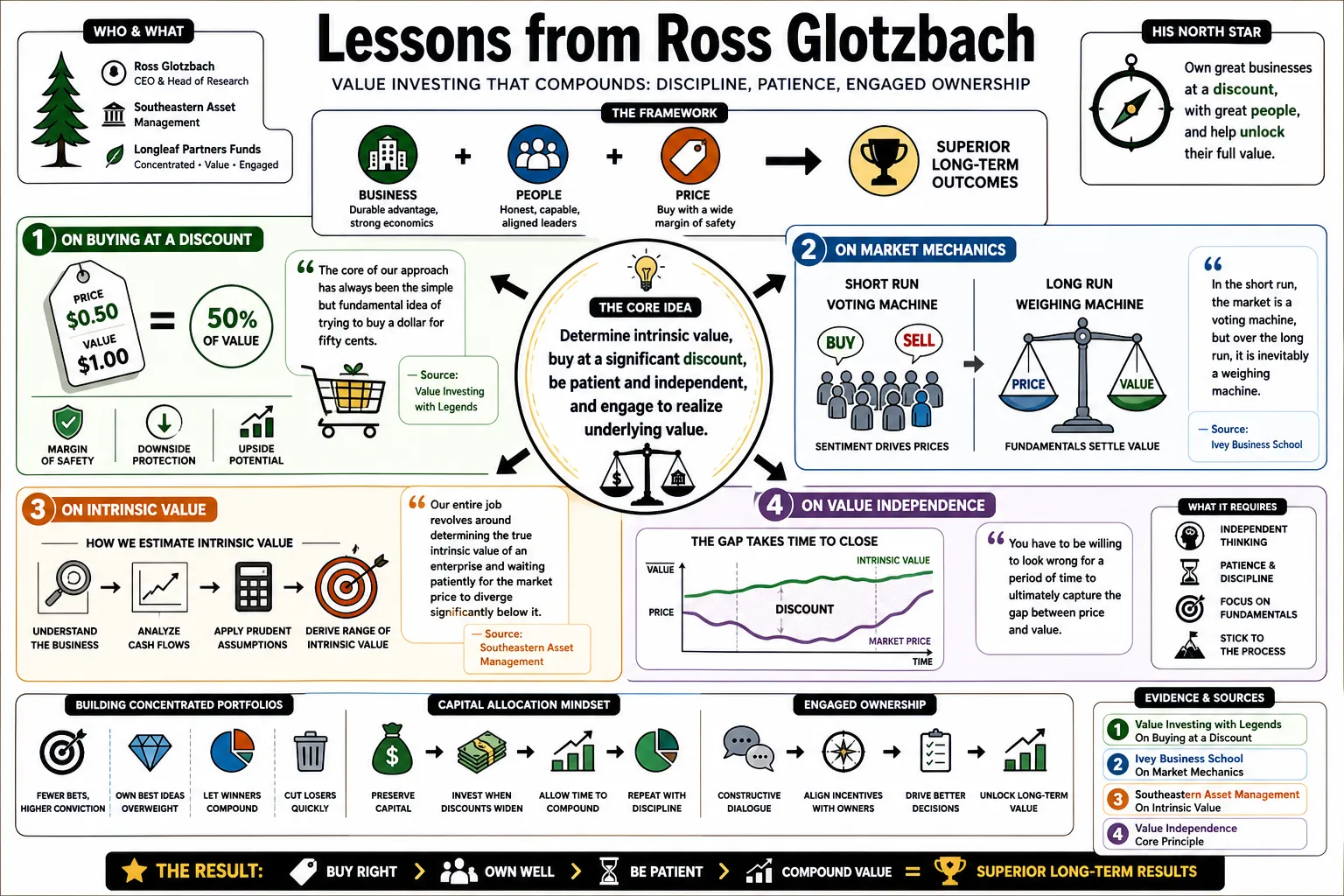

Part 1: The Foundations of Value Investing

- On Buying at a Discount: "The core of our approach has always been the simple but fundamental idea of trying to buy a dollar for fifty cents." — Source: Value Investing with Legends

- On Intrinsic Value: "Our entire job revolves around determining the true intrinsic value of an enterprise and waiting patiently for the market price to diverge significantly below it." — Source: Southeastern Asset Management

- On Value Independence: "You have to be willing to look wrong for a period of time to ultimately capture the gap between price and value." — Source: Advisor Perspectives

- On Defining Value: "Value investing is not simply buying stocks with low statistical multiples; it is buying high-quality assets at a material discount to their appraised worth." — Source: The Insightful Investor

- On Margin of Safety: "A significant margin of safety is what allows you to survive the inevitable mistakes and unforeseen macroeconomic shocks." — Source: Ivey Business School

- On True Value Investor Culture: "Maintaining a culture dedicated to true value principles is essential, as the industry constantly pushes you toward short-term thinking." — Source: Value Investing with Legends

- On Fads and Fundamentals: "We ignore hot themes and index-driven fads because our focus remains strictly on the underlying business fundamentals." — Source: Southeastern Asset Management

- On the Importance of Process: "A rigorous, repeatable appraisal process is your anchor when market sentiment swings wildly." — Source: Ivey Business School

- On Historical Perspective: "Understanding how a business has navigated past cycles provides important context for estimating its future cash-generating power." — Source: The Price-to-Value Podcast

Part 2: The "Business, People, Price" Framework

- On the Three Pillars: "Every investment we make must pass our three distinct hurdles: Business, People, and Price." — Source: Southeastern Asset Management

- On Quality Businesses: "A great business is one that has pricing power, competitive advantages, and the ability to compound capital over time." — Source: Longleaf Partners Funds

- On Evaluating People: "We look for management teams who think and act like owners, and who possess a demonstrated track record of smart capital allocation." — Source: Ivey Business School

- On Aligning Interests: "The ideal executive team has a substantial portion of their own net worth invested alongside our clients." — Source: Southeastern Asset Management

- On the Right Price: "Even a phenomenal business run by exceptional people is a poor investment if you pay an exorbitant price for it." — Source: Advisor Perspectives

- On the Interplay of Pillars: "The three elements of Business, People, and Price are deeply intertwined; great people can improve a business, which in turn affects its intrinsic value." — Source: The Price-to-Value Podcast

- On Avoiding Weak Links: "If a prospective investment fails on the 'People' test, it doesn't matter how cheap the 'Price' is; we will walk away." — Source: Value Investing with Legends

- On Competitive Moats: "A durable business must have defensible barriers to entry to protect its margins from competitive erosion over the next decade." — Source: Longleaf Partners Funds

- On Capital Allocation Skills: "We evaluate CEOs heavily on how intelligently they deploy the free cash flow the business generates, rather than solely on their operational execution." — Source: Southeastern Asset Management

- On Pricing Discipline: "Maintaining strict pricing discipline is the hardest part of the framework during raging bull markets." — Source: Ivey Business School

Part 3: The Price-to-Value (P/V) Metric

- On Defining P/V: "The Price-to-Value ratio simply measures where a stock is currently trading relative to our conservative appraisal of its intrinsic worth." — Source: The Price-to-Value Podcast

- On Target Thresholds: "Historically, we look to build positions when the P/V falls well below 60 percent, indicating a substantial discount." — Source: Advisor Perspectives

- On P/V as a Compass: "The P/V ratio serves as an internal compass, guiding our decisions on when to add to a position or trim it." — Source: Southeastern Asset Management

- On Portfolio Construction: "We systematically allocate capital toward our highest conviction ideas offering the lowest Price-to-Value ratios." — Source: Longleaf Partners Funds

- On Contextualizing P/V: "P/V is a vital data point, but investors must remember to weigh it against business quality and management rather than in isolation." — Source: SEC Filings

- On Dynamic Appraisals: "Intrinsic value is not a static number; our P/V appraisals evolve as we digest new information about the business's fundamental performance." — Source: The Price-to-Value Podcast

- On Market Panics: "When broad market panics cause a company's stock price to drop without a corresponding decline in intrinsic value, the P/V ratio screams opportunity." — Source: Ivey Business School

- On Trimming Positions: "As the price appreciates and the P/V gap closes toward our estimate of fair value, we naturally begin to reduce our exposure." — Source: Southeastern Asset Management

- On Margin of Safety via P/V: "A low P/V inherently provides the margin of safety required to protect capital against errors in our appraisal." — Source: Value Investing with Legends

Part 4: Engaged Ownership and Management

- On Engaged Value: "We believe that being a concentrated, engaged owner allows us to actively help bridge the gap between a company's stock price and its intrinsic value." — Source: The Insightful Investor

- On Constructive Dialogue: "Engagement doesn't always mean hostility; it means having a constructive, ongoing dialogue with the board and management." — Source: Southeastern Asset Management

- On Board Representation: "When necessary, we will seek board representation to ensure that capital allocation decisions align with long-term shareholder interests." — Source: Longleaf Partners Funds

- On Catalyst Creation: "Sometimes a cheap stock needs an active owner to catalyze value realization through strategic reviews or balance sheet optimization." — Source: Ivey Business School

- On Partnering with CEOs: "Our best investments often involve partnering closely with excellent operators to remove short-term market pressures." — Source: The Price-to-Value Podcast

- On Executive Compensation: "We vigorously advocate for compensation structures that reward executives for growing per-share intrinsic value, rather than simply expanding the corporate empire." — Source: Southeastern Asset Management

- On Patience in Engagement: "Meaningful corporate change takes time, and our structure allows us the patience required to see long-term engagements through." — Source: Value Investing with Legends

- On Collaborative Problem Solving: "We view ourselves as sounding boards for management teams facing complex capital allocation dilemmas." — Source: The Insightful Investor

- On Protecting Downside: "Active engagement serves as a risk management tool, allowing us to intervene if a company strays from its core competencies." — Source: Advisor Perspectives

- On Corporate Governance: "Strong governance is a prerequisite for long-term compounding, and we dedicate significant resources to evaluating and improving board dynamics." — Source: Longleaf Partners Funds

Part 5: Navigating Market Volatility

- On Embracing Volatility: "Volatility is not risk; it is the source of our returns, creating the very price-to-value disparities we seek to exploit." — Source: Ivey Business School

- On Market Noise: "We deliberately structure our organization and our days to tune out the daily market noise that distracts from fundamental analysis." — Source: Southeastern Asset Management

- On Emotional Discipline: "The most critical skill during a market dislocation is the emotional discipline to buy when others are indiscriminately selling." — Source: Value Investing with Legends

- On Acting with Conviction: "When the market offers you a premier business at a fraction of its worth, you must be prepared to act decisively." — Source: Advisor Perspectives

- On the Danger of Market Timing: "We do not attempt to forecast macroeconomic shifts or time market cycles; we simply value businesses and buy them when they are cheap." — Source: Longleaf Partners Funds

- On Liquidity: "Maintaining a mindset that values liquidity allows us to pivot quickly and concentrate capital into our highest conviction ideas during panics." — Source: The Price-to-Value Podcast

- On Macro Distractions: "Time spent predicting interest rates or political outcomes is time stolen from analyzing unit economics and competitive positioning." — Source: Ivey Business School

- On the Opportunities in Pessimism: "The best investment opportunities invariably arise in sectors or regions clouded by temporary, resolvable pessimism." — Source: Southeastern Asset Management

- On Staying the Course: "Our long-term orientation prevents us from abandoning sound investments just because their stock prices face short-term headwinds." — Source: The Insightful Investor

Part 6: Long-Term Concentration and Patience

- On Portfolio Concentration: "We concentrate our portfolios because our deep research typically yields only a handful of truly compelling, mispriced opportunities at any given time." — Source: Southeastern Asset Management

- On Dilution of Conviction: "Owning fifty or a hundred stocks guarantees mediocrity and dilutes the impact of your best, most thoroughly researched ideas." — Source: Longleaf Partners Funds

- On the Master List: "We maintain a 'master list' of exceptional companies we want to own, patiently waiting for years until their prices fall into our buy zone." — Source: Value Investing with Legends

- On Time Arbitrage: "Our primary competitive edge is time arbitrage, which is the willingness to hold an asset for five years when the rest of the market is focused on the next quarter." — Source: Ivey Business School

- On Ignoring Benchmarks: "To generate differentiated results, you must be willing to construct a portfolio that looks nothing like the benchmark index." — Source: Advisor Perspectives

- On the Cost of Patience: "Patience in investing often looks like underperformance in the short term, which is why structural alignment with your client base is essential." — Source: The Insightful Investor

- On Capital Deployment: "We prefer to hold cash rather than deploy it into mediocre opportunities just to be fully invested." — Source: Southeastern Asset Management

- On Tracking the Intrinsic Value: "As long as the intrinsic value of the business continues to grow at an acceptable rate, we are happy to wait for the market to recognize it." — Source: The Price-to-Value Podcast

- On Deep Work: "Concentration forces you to do the deep work; you cannot afford superficial research when an idea makes up a significant percentage of your portfolio." — Source: Value Investing with Legends

Part 7: Career, Learning, and Research Culture

- On Generalist Analysts: "Our analysts are generalists by design because looking across various industries leads to better debate amongst the team and superior capital allocation." — Source: Ivey Business School

- On Collaborative Debate: "A healthy research culture requires an environment where analysts feel empowered to vigorously challenge the portfolio managers' assumptions." — Source: Southeastern Asset Management

- On Intellectual Honesty: "You must cultivate intellectual honesty to recognize when your initial thesis was wrong and act quickly to correct the mistake." — Source: Value Investing with Legends

- On Continuous Learning: "The most successful investors are voracious readers who continuously adapt their mental models as industries evolve." — Source: The Insightful Investor

- On Early Career Lessons: "Learning to analyze businesses at the granular level of corporate finance early on provided the technical foundation for everything we do." — Source: Value Investing with Legends

- On Operational Efficiency: "The improved efficiencies possible with external operational partnerships allow us to focus most on delivering absolute returns and personalized service." — Source: Ultimus Fund Solutions

- On Humility: "The market will always humble you; building a team that embraces humility rather than hubris is vital for long-term survival." — Source: Ivey Business School

- On Analyzing Mistakes: "We spend as much time conducting post-mortems on our losers as we do celebrating our winners, to refine our appraisal process." — Source: Southeastern Asset Management

- On Mentorship: "Passing down the institutional memory of past market cycles is essential for developing the next generation of value investors." — Source: The Price-to-Value Podcast

Part 8: Analyzing Specific Businesses and Capital Allocation

- On Corporate Innovation: "You've got to be willing to step out there and extend your brand a little bit and try things." — Source: WMBD Radio

- On Share Repurchases: "When a company's stock is trading at a massive discount to intrinsic value, intelligent share repurchases are often the most accretive use of free cash flow." — Source: Southeastern Asset Management

- On Evaluating M&A: "We are highly skeptical of empire-building acquisitions; management must clearly demonstrate how a deal builds per-share value." — Source: Longleaf Partners Funds

- On Real Estate Assets: "We often find hidden value in companies that own prime real estate that is significantly under-appreciated by the public markets." — Source: The Price-to-Value Podcast

- On Balance Sheet Strength: "A strong balance sheet is a prerequisite for surviving cyclical downturns and seizing opportunities when weaker competitors falter." — Source: Advisor Perspectives

- On Sustainable Advantage: "We are drawn to businesses that provide essential services or products, where the cost of switching is high for the consumer." — Source: Ivey Business School

- On Capital Return Policies: "A clear, consistent policy of returning excess capital to shareholders via special dividends or buybacks signals a management team aligned with our goals." — Source: Southeastern Asset Management

- On Valuing Intangibles: "Traditional accounting often fails to capture the true economic value of strong brands, patents, or deeply entrenched customer networks." — Source: Value Investing with Legends

- On Spin-offs and Restructurings: "Corporate reorganizations and spin-offs frequently create forced selling and information asymmetry, making them fertile hunting grounds for value investors." — Source: The Price-to-Value Podcast