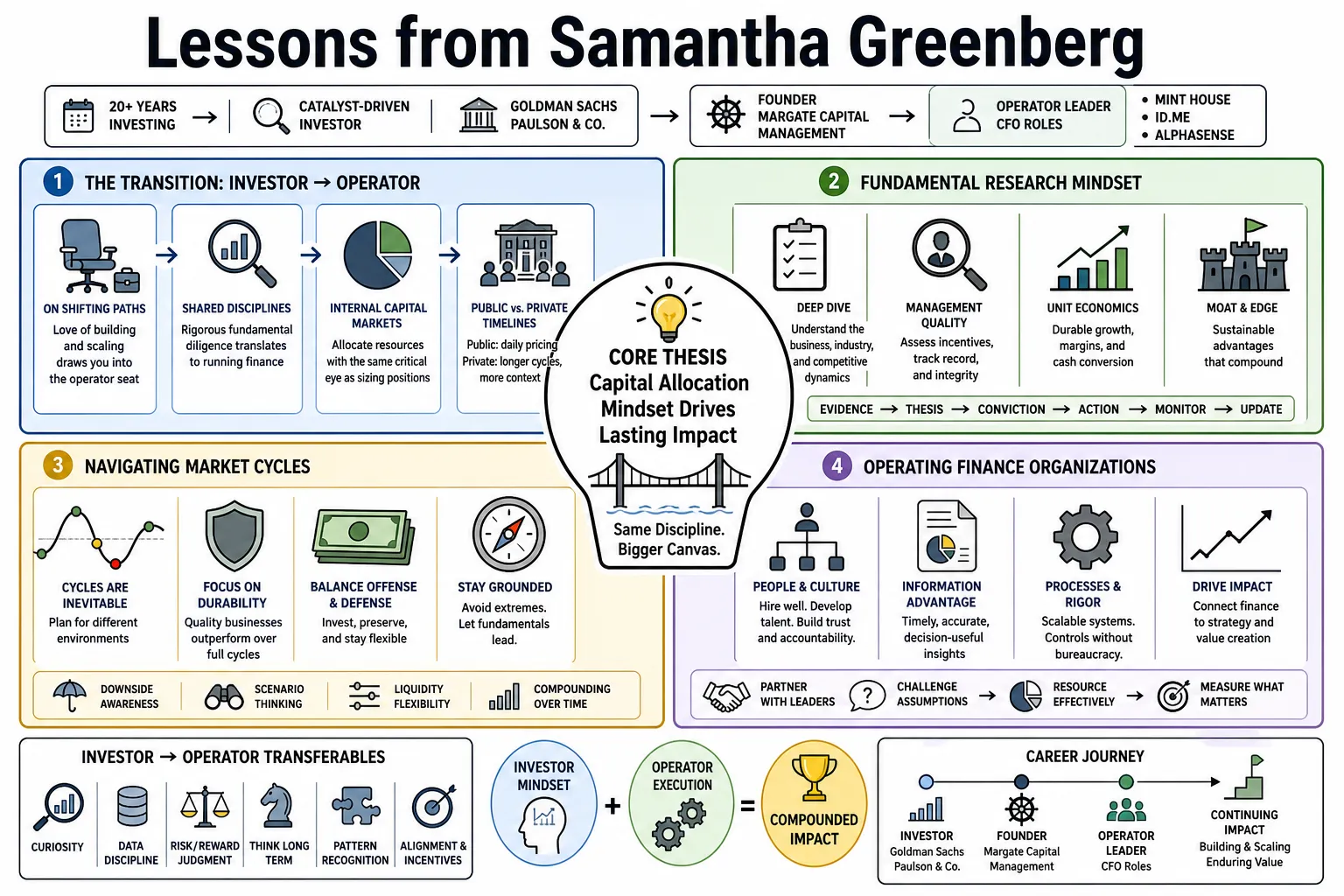

Samantha Greenberg spent over two decades as a catalyst-driven investor at firms like Goldman Sachs and Paulson & Co. before founding the hedge fund Margate Capital Management. She subsequently transitioned into executive leadership, applying her capital allocation background as the CFO of technology companies including Mint House, ID.me, and AlphaSense. This compilation captures her approach to fundamental research, navigating market cycles, and operating finance organizations.

Part 1: The Transition from Investor to Operator

- On shifting paths: "There is a career-abiding love for seeing businesses built and scaled that ultimately draws you out of the allocator seat and into the operator seat." — Source: [CFO.com]

- On shared disciplines: "The rigorous fundamental diligence used to underwrite a stock translates directly to the daily mechanics of running a company's internal finance function." — Source: [CFO Dive]

- On internal capital markets: "Operating a company requires viewing internal resource allocation with the same critical eye a portfolio manager uses when sizing positions." — Source: [Value Investing with Legends]

- On public vs. private timelines: "In public markets, feedback is immediate through daily pricing. Inside a company, you have to establish your own leading indicators to know if a strategy is working before the quarter ends." — Source: [AlphaSense Press Release]

- On evaluating internal projects: "Every new product launch or geographic expansion must be underwritten like an acquisition, complete with downside scenarios and base-case modeling." — Source: [StreetFins Interview]

- On executive communication: "Investors train you to synthesize massive amounts of data into a clear thesis; that same skill is necessary when presenting to a board of directors." — Source: [CSG Systems Board Materials]

- On continuous adaptation: "Moving from the buy-side to the C-suite requires unlearning the instinct to solely observe and developing the muscle to intervene and fix." — Source: [CFO.com]

- On forecasting accuracy: "A budget is effectively a forward-looking model. If you miss your internal targets, it is no different than a portfolio company missing consensus estimates." — Source: [CFO Dive]

- On operational patience: "You cannot trade in and out of a corporate strategy. You have to live with the structural decisions you make and guide the team through the execution phase." — Source: [Value Investing with Legends]

- On cross-functional alignment: "The finance team cannot exist in a vacuum; it must act as a strategic partner to engineering, sales, and product to ensure capital follows the highest returns." — Source: [AlphaSense Press Release]

Part 2: Catalyst-Driven Investment Strategy

- On defining a catalyst: "A cheap stock is not a thesis. You need a specific, identifiable event—a merger, a spin-off, or a management change—that will force the market to re-evaluate the asset." — Source: [Value Investing with Legends]

- On sector consolidation: "Identifying the logical acquirers in a fragmented industry like technology or media often yields better returns than betting on standalone turnarounds." — Source: [Business Insider]

- On structural advantages: "We look for companies possessing structural advantages that allow them to compound earnings faster than consensus anticipates, usually unlocked by a near-term catalyst." — Source: [CNBC Events]

- On event timing: "It is entirely possible to be right about a thesis but wrong about the timeline. Catalyst investing is designed to minimize the duration of capital commitment." — Source: [Institutional Investor]

- On corporate restructuring: "Spin-offs frequently create mispriced assets because the initial shareholder base often indiscriminately sells the newly separated entity." — Source: [Value Investing with Legends]

- On industry secular shifts: "You want to align your capital with irreversible secular trends, such as the shift from linear television to streaming, and find the specific events that accelerate that transition." — Source: [Business Insider]

- On management changes: "A new CEO with a mandate for capital discipline can be one of the most powerful drivers of multiple expansion in a stagnant company." — Source: [StreetFins Interview]

- On identifying acquisition targets: "When looking at the media landscape, you have to map the capability gaps of the largest players and identify the specific mid-cap companies that fill those voids." — Source: [CNBC Events]

- On avoiding value traps: "Without a forcing function to alter the capital structure or operational trajectory, a discounted valuation will likely persist." — Source: [Value Investing with Legends]

- On M&A arbitrage: "Understanding the regulatory environment and antitrust precedent is just as important as the financial terms of a proposed merger." — Source: [Institutional Investor]

Part 3: Technology and AI in the Finance Function

- On AI preparedness: "I dedicate hours every week to honing my artificial intelligence skills to ensure I can build and run an AI-native finance organization." — Source: [CFO Dive]

- On data scaling: "As a company scales rapidly, manual data reconciliation becomes a failure point. Automation must be implemented before the transaction volume breaks the existing systems." — Source: [CFO.com]

- On actionable intelligence: "Finance is no longer just about reporting historical results; it is about ingesting unstructured data and delivering predictive insights to the business units." — Source: [AlphaSense Press Release]

- On software adoption: "The modern CFO stack requires integrating disparate data sources so that pricing, cost of goods sold, and customer acquisition metrics sit in a single, unassailable source of truth." — Source: [CSG Systems Board Materials]

- On AI in underwriting: "Generative AI can dramatically reduce the time it takes to parse SEC filings and earnings transcripts, allowing analysts to focus on modeling and synthesis." — Source: [CFO Dive]

- On technical fluency: "You cannot effectively allocate capital to engineering teams if you do not fundamentally understand the software development lifecycle." — Source: [StreetFins Interview]

- On automating compliance: "Regulatory and audit reporting should be the first candidates for automation, freeing up the team for higher-margin analytical work." — Source: [CFO.com]

- On system migrations: "Upgrading an ERP system is painful but necessary. Delaying the migration only compounds the technical debt in your finance operations." — Source: [CSG Systems Board Materials]

- On the future of modeling: "Excel will always exist, but the baseline for financial modeling is moving toward Python and integrated cloud databases." — Source: [AlphaSense Press Release]

Part 4: Capital Allocation and Strategy

- On board governance: "A well-functioning board requires directors who are willing to question the base assumptions of management's capital allocation plans." — Source: [CSG Systems Board Materials]

- On organic vs. inorganic growth: "M&A should never be used to mask a deteriorating core business. Acquisitions must accelerate an existing, healthy strategy." — Source: [Value Investing with Legends]

- On returning capital: "If the internal rate of return on new projects falls below your cost of capital, buying back stock or issuing dividends is the only responsible action." — Source: [StreetFins Interview]

- On strategic patience: "Sometimes the best allocation decision is holding cash while you wait for market valuations to correct to a point where acquisitions make mathematical sense." — Source: [Institutional Investor]

- On cost of capital: "In a higher interest rate environment, the hurdle rate for every internal initiative must adjust accordingly. Free money hides operational inefficiency." — Source: [CFO.com]

- On capital structures: "Optimizing the balance sheet means finding the exact ratio of debt to equity that minimizes cost without restricting the company's operational flexibility." — Source: [CFO Dive]

- On evaluating competitors: "You must constantly analyze how your peers are allocating their capital. If they are all divesting from a specific business line, you need to know why." — Source: [CNBC Events]

- On long-term value: "Quarterly earnings pressure often incentivizes deferred maintenance. A good CFO protects the investments that will yield results three years out." — Source: [AlphaSense Press Release]

- On asset sales: "Divesting a non-core asset is often harder than acquiring one because it requires admitting that the initial thesis was wrong or has simply played out." — Source: [Value Investing with Legends]

Part 5: Risk Management and Volatility

- On rules-based discipline: "Risk management cannot be emotional. You must establish strict, rules-based limits for position sizing and drawdowns before you put the capital to work." — Source: [Value Investing with Legends]

- On cutting losses: "The hardest discipline to learn is taking a small loss before it becomes a structural impairment to the portfolio." — Source: [Institutional Investor]

- On market corrections: "Volatility is not the same thing as risk. Volatility is the mechanism that creates the mispricing we need to generate excess returns." — Source: [CNBC Events]

- On corporate risk: "As a CFO, risk management means stress-testing your liquidity against multiple overlapping macroeconomic shocks." — Source: [CFO Dive]

- On portfolio concentration: "You only concentrate capital when the asymmetric risk-reward ratio is overwhelmingly in your favor, and you have exhausted all avenues of diligence." — Source: [Value Investing with Legends]

- On hedging strategies: "A hedge should protect against specific, identifiable macroeconomic tail risks, not just serve as a drag on portfolio performance." — Source: [Business Insider]

- On short selling: "Shorting requires a completely different psychological makeup than going long. The market naturally drifts upward, so your thesis must be airtight and catalyst-driven." — Source: [StreetFins Interview]

- On internal controls: "Financial controls are the operational equivalent of portfolio risk limits. They prevent single points of failure from threatening the enterprise." — Source: [CFO.com]

- On cognitive bias: "Confirmation bias is the enemy of risk management. You must actively seek out the analysts and data points that tell you why your thesis is wrong." — Source: [Value Investing with Legends]

Part 6: Fundamental Research and Diligence

- On reading filings: "There are no shortcuts to reading the footnotes in a 10-K. The actual health of a business is rarely found in the headline press release." — Source: [Value Investing with Legends]

- On primary research: "Talking to former employees, competitors, and suppliers gives you a completely different picture than the one presented by management on an earnings call." — Source: [Institutional Investor]

- On modeling assumptions: "A financial model is only as good as its underlying assumptions. If you adjust the growth rate by two percent to make the math work, you are lying to yourself." — Source: [CNBC Events]

- On structural advantages: "True moats are rare. We look for high switching costs, network effects, or regulatory capture that allow a company to maintain pricing power." — Source: [Business Insider]

- On unit economics: "You cannot scale a bad business model. If the unit economics are negative, adding more customers only accelerates the cash burn." — Source: [CFO.com]

- On management track records: "Past performance does not guarantee future results, but a management team's history of capital allocation is the best proxy you have for how they will behave tomorrow." — Source: [StreetFins Interview]

- On customer retention: "Churn is the silent killer of subscription businesses. You have to understand exactly why customers leave, not just celebrate when they sign up." — Source: [AlphaSense Press Release]

- On TAM expansion: "Companies often define their Total Addressable Market too broadly. Diligence requires sizing the market based on actual, immediate adjacencies." — Source: [CFO Dive]

- On margin profiles: "Gross margin tells you what the product is worth; operating margin tells you how well the company is run." — Source: [Value Investing with Legends]

- On tracking competitors: "Diligence never stops. You have to underwrite a company's competitors with the same intensity as the company you actually own." — Source: [Institutional Investor]

Part 7: Building and Scaling Businesses

- On early-stage growth: "In the early days of scaling, momentum can cover up a lot of operational sins. Eventually, those inefficiencies mature into structural problems." — Source: [CFO.com]

- On operational metrics: "You have to distill the complexity of the business down to three or four key performance indicators that every employee can understand and influence." — Source: [AlphaSense Press Release]

- On hiring for scale: "The team that takes a company from zero to fifty million in revenue is rarely the exact same team that can navigate the path to five hundred million." — Source: [CFO Dive]

- On infrastructure investment: "Underinvesting in back-office infrastructure during periods of hyper-growth guarantees that you will hit a painful operational wall later." — Source: [CSG Systems Board Materials]

- On pricing strategy: "Pricing is the most underutilized lever in a growing business. Testing price elasticity should be a continuous operational function." — Source: [StreetFins Interview]

- On cash conversion cycles: "Growth consumes cash. Optimizing your billing and collections processes is the cheapest form of financing available to a scaling business." — Source: [CFO.com]

- On founder transitions: "When a company scales, the founder must transition from doing the work to designing the machine that does the work." — Source: [Value Investing with Legends]

- On geographic expansion: "Entering a new market is essentially starting a new business. It requires localized product-market fit and dedicated resources, not just a translation of the website." — Source: [AlphaSense Press Release]

- On sustaining culture: "As headcount doubles, culture dilutes unless you actively formalize the behaviors and expectations that made the company successful in the first place." — Source: [CFO Dive]

Part 8: Leadership and Diversity in Finance

- On starting a fund: "Partnering with experienced seeders who understand the mechanics of emerging managers provides the institutional credibility needed to attract early capital." — Source: [Business Insider]

- On representation: "You cannot be what you cannot see. Increasing the visibility of female portfolio managers and CFOs is necessary to change the pipeline." — Source: [StreetFins Interview]

- On building teams: "Diversity of thought in a research team is not a corporate requirement; it is a structural advantage that prevents groupthink in underwriting." — Source: [Institutional Investor]

- On mentorship: "Effective mentorship in finance is less about giving advice and more about actively sponsoring junior analysts for specific, high-visibility projects." — Source: [CNBC Events]

- On navigating the industry: "You have to be willing to advocate for your own track record. Capital is not allocated purely on merit; it is allocated to those who can clearly articulate their edge." — Source: [Value Investing with Legends]

- On resilience: "Working through the financial crisis at a distressed debt desk teaches you that survival requires separating your intellect from market panic." — Source: [StreetFins Interview]

- On imposter syndrome: "The best investors constantly question their assumptions, but they do not question their right to sit at the table." — Source: [CFO.com]

- On structural barriers: "The industry must move past networking events and focus on changing the fundamental ways capital is seeded and distributed to underrepresented managers." — Source: [Institutional Investor]

- On legacy: "The ultimate measure of leadership is not just the returns you generate, but the quality of the investors and operators who trained under your watch." — Source: [Value Investing with Legends]