Samantha McLemore is the founder and Chief Investment Officer of Patient Capital Management, having previously spent two decades working alongside legendary investor Bill Miller. She is known for challenging the traditional, multiple-based definition of value investing and relying instead on a probability-weighted approach to intrinsic value. This profile collects her practical insights on managing behavioral bias, holding high-conviction positions through drawdowns, and assessing businesses based on their long-term cash flows rather than temporary market sentiment.

Part 1: The Definition of Value

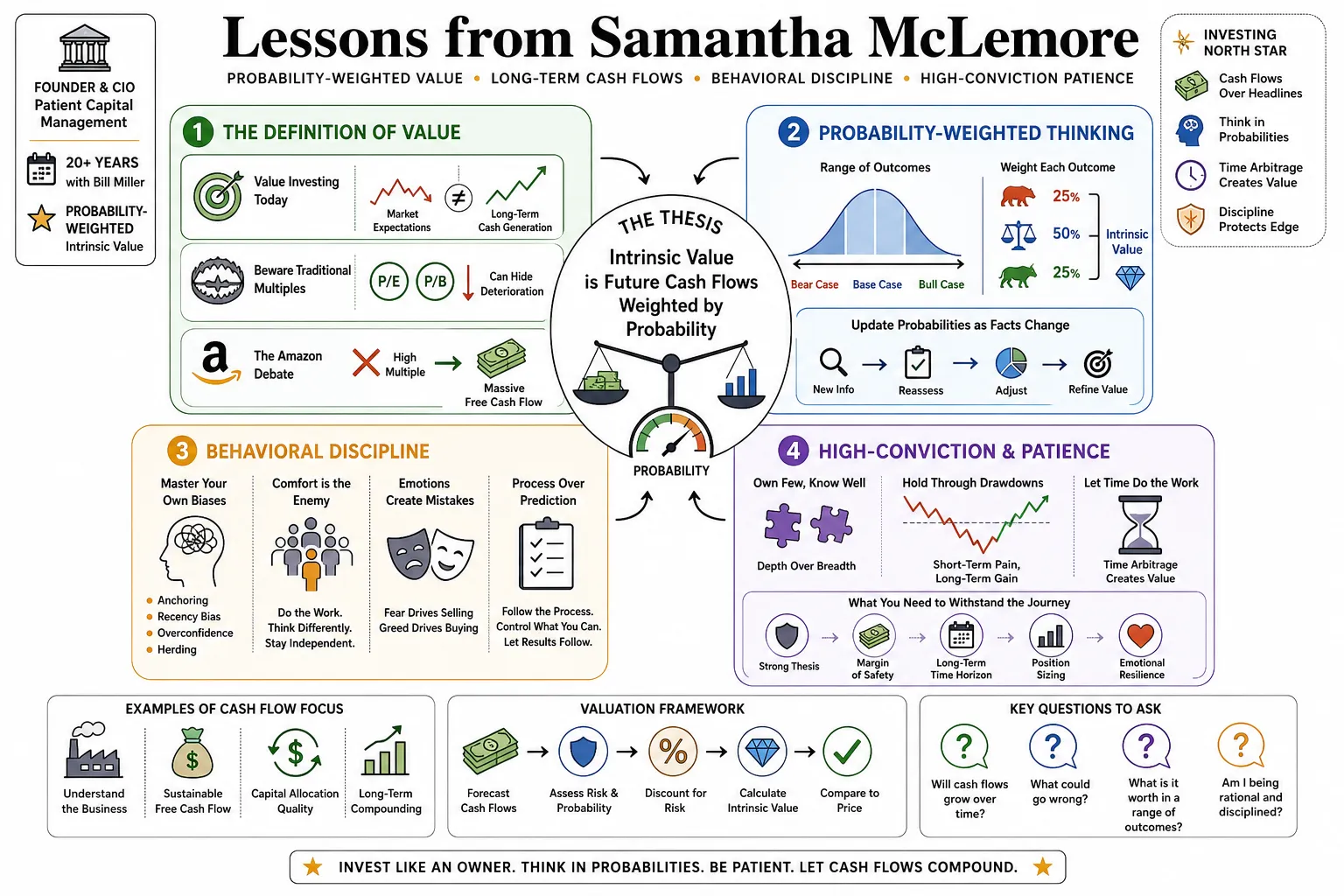

- On modern value investing: "Value investing isn't just about buying cheap stocks; it's about finding a disconnect between current market expectations and the long-term cash generation of a business." — Source: Masters in Business

- On traditional multiples: "Relying strictly on low price-to-earnings or price-to-book ratios often leads you into value traps where the business is fundamentally deteriorating." — Source: Alpha Exchange

- On the Amazon debate: "For years, people said Amazon couldn't be a value stock because of its high multiple, completely ignoring the massive free cash flow it was destined to produce." — Source: The Meb Faber Show

- On future cash flows: "The true value of any asset is the present value of its future free cash flows, regardless of whether it's categorized as a growth or value stock by index providers." — Source: Patient Capital Management Letters

- On evolving frameworks: "If you refuse to adapt your valuation framework to an economy driven by intangible assets, you will miss out on the best compounding machines of our era." — Source: Richer, Wiser, Happier

- On early opportunities: "One thing that differentiates our funds is our flexibility to do unique things and our willingness to invest in attractive opportunities early in their life cycle." — Source: Economic Times

- On business quality: "You have to distinguish between a stock that is cheap because the market is irrationally pessimistic and a stock that is cheap because the underlying business is impaired." — Source: Talking Billions

- On intangible assets: "Accounting rules have not kept pace with the shift to knowledge-based businesses, meaning standard financial statements often understate the true value of aggressive internal reinvestment." — Source: Masters in Business

- On absolute value: "We don't care what sector a company is in or what style box it fits into; we only care about the gap between price and absolute intrinsic value." — Source: Patient Capital Management Letters

- On long-term vision: "A true value investor must be willing to underwrite the future, not just stare in the rearview mirror of historical financial data." — Source: Alpha Exchange

Part 2: Lessons from Bill Miller

- On capturing upside: "The biggest lesson I learned from Bill is that the big money's made in the big moves. You have to let your winners run." — Source: Richer, Wiser, Happier

- On the asymmetry of returns: "In investing, you can only lose 100% of your money, but you can make thousands of percent on a single successful investment if you have the patience to hold it." — Source: The Meb Faber Show

- On handling criticism: "Bill taught me to be entirely comfortable looking foolish in the short term if the long-term thesis remains intact." — Source: Masters in Business

- On thinking differently: "You cannot generate outsized returns by sharing the exact same consensus view as the broader market; you have to train yourself to think differently." — Source: Alpha Exchange

- On market panic: "Bill had an extraordinary ability to get excited and aggressive exactly when everyone else in the market was consumed by fear and panic." — Source: Talking Billions

- On managing drawdowns: "Surviving severe drawdowns requires an unwavering focus on the underlying business value rather than the daily fluctuations of the stock ticker." — Source: Patient Capital Management Letters

- On intellectual flexibility: "You have to be willing to change your mind when the facts change. Dogmatism is lethal in portfolio management." — Source: Richer, Wiser, Happier

- On defining success: "Success isn't about your batting average or how often you are right; it is entirely about the magnitude of your gains when you are right versus your losses when you are wrong." — Source: Masters in Business

- On long-term partnerships: "Working alongside someone for two decades allows you to deeply absorb their decision-making framework and apply it across entirely different market environments." — Source: Patient Capital Management Letters

Part 3: The Behavioral Edge

- On emotional control: "Your behavioral edge—the ability to control your own emotions when others cannot—is often more valuable than any informational or analytical advantage." — Source: Richer, Wiser, Happier

- On time arbitrage: "Most of the market is optimizing for the next quarter. If you can simply optimize for the next three to five years, you immediately gain a structural advantage." — Source: The Meb Faber Show

- On market extremes: "We actively try to get excited in times of fear, pessimism, and panic, because that is when the largest gaps between price and value are created." — Source: Masters in Business

- On temperament: "Intelligence is a commodity on Wall Street. A calm temperament and the discipline to execute your strategy during a crisis is exceptionally rare." — Source: Alpha Exchange

- On fighting human nature: "Human biology is wired to flee from pain and seek comfort, which is exactly the opposite of what you need to do to buy out-of-favor assets." — Source: Talking Billions

- On the herd mentality: "It feels safer to fail conventionally with the herd than to risk failing unconventionally on your own, but outperformance requires leaving the herd." — Source: Patient Capital Management Letters

- On structural advantages: "As capital continues to flow into passive strategies and high-frequency algorithms, the behavioral advantage for patient, active stock pickers only increases." — Source: Masters in Business

- On reacting to news: "You have to train yourself to ask whether a piece of bad news permanently impairs the business or simply creates a temporary pricing dislocation." — Source: Alpha Exchange

- On patience: "Patience is not just about waiting; it is about maintaining your conviction and doing nothing when the market is demanding that you do something." — Source: Richer, Wiser, Happier

- On self-awareness: "The best investors understand their own psychological triggers and build frameworks to prevent themselves from making emotional decisions." — Source: The Meb Faber Show

Part 4: Volatility and Risk

- On the cost of returns: "Volatility is the price you pay for returns. If you are unwilling to endure drawdowns, you cannot capture long-term compounding." — Source: Patient Capital Management Letters

- On defining risk: "Risk is not the daily fluctuation of a stock price; real risk is the permanent loss of capital caused by a flawed thesis or a deteriorating business." — Source: Masters in Business

- On market timing: "Trying to time the market to avoid volatility almost always results in missing the sharp, sudden rebounds that account for the bulk of historical returns." — Source: Talking Billions

- On accepting discomfort: "To generate alpha, you have to be comfortable being uncomfortable. Periods of severe volatility are a feature of the market, not a bug." — Source: Alpha Exchange

- On the illusion of safety: "Fleeing to cash during a market panic feels safe in the moment, but it introduces the massive risk of missing the subsequent recovery." — Source: Richer, Wiser, Happier

- On opportunity cost: "The fear of volatility causes investors to drastically truncate their upside, leading to portfolios that slowly underperform over time." — Source: The Meb Faber Show

- On long horizons: "The longer your investment horizon, the less relevant daily or monthly volatility becomes to your actual outcomes." — Source: Patient Capital Management Letters

- On position sizing: "You manage volatility not by avoiding great businesses that fluctuate, but by sizing your positions so that you can survive the inevitable drawdowns without being forced to sell." — Source: Masters in Business

- On market corrections: "A market correction is the mechanism by which risk is flushed out of the system and future returns are recalibrated higher." — Source: Alpha Exchange

Part 5: Assessing Intrinsic Value

- On Central Tendency of Value: "We use a Central Tendency of Value metric, which is a probability-weighted estimate of intrinsic value that accounts for a wide range of future scenarios." — Source: Patient Capital Management Letters

- On avoiding precision: "Intrinsic value is not a single, precise number. It is a distribution of potential outcomes, and pretending otherwise creates false confidence." — Source: Alpha Exchange

- On scenario modeling: "You have to model the upside, the base case, and the downside, and then honestly assign probabilities to each based on the business economics." — Source: Richer, Wiser, Happier

- On multiple methods: "We never rely on a single valuation method. We look at discounted cash flows, private market comparables, and historical multiples to triangulate the truth." — Source: Masters in Business

- On portfolio upside: "By tracking the portfolio upside to our Central Tendency of Value, we can mathematically measure the embedded return potential of the entire fund at any given moment." — Source: Patient Capital Management Letters

- On qualitative factors: "A spreadsheet can give you a valuation, but assessing the alignment and capital allocation skills of management requires qualitative judgment." — Source: Talking Billions

- On updating models: "When new information arrives, you update the probabilities in your model. You do not stubbornly anchor to your original thesis." — Source: The Meb Faber Show

- On margin of safety: "A deep discount to intrinsic value provides a margin of safety, but the ultimate margin of safety is a business that grows its intrinsic value every year." — Source: Alpha Exchange

- On market efficiency: "Markets are mostly efficient, but they periodically become highly inefficient regarding specific companies due to narrative shifts or liquidity events." — Source: Masters in Business

Part 6: Long-Term Compounding

- On time in the market: "The mathematical reality is that time in the market is vastly more powerful than timing the market when it comes to wealth creation." — Source: Patient Capital Management Letters

- On holding periods: "To truly benefit from compounding, you must be willing to hold exceptional businesses for a decade or more, not just trade them for a 20% gain." — Source: Richer, Wiser, Happier

- On interrupting compounding: "The most expensive mistake an investor can make is unnecessarily interrupting the compounding process of a great business due to macroeconomic fears." — Source: The Meb Faber Show

- On structural tailwinds: "We look for businesses operating with massive structural tailwinds because those are the companies capable of compounding cash flows at high rates for extended periods." — Source: Masters in Business

- On institutional constraints: "Many institutional investors structurally cannot think long-term because their clients evaluate them on a quarterly basis, which creates an opening for those who can." — Source: Alpha Exchange

- On delayed gratification: "Long-term compounding is essentially the practice of delayed gratification applied to finance." — Source: Talking Billions

- On knowledge compounding: "Investment knowledge compounds exactly like capital. The research you do on a company today pays dividends for decades as you track its evolution." — Source: Masters in Business

- On letting winners run: "Trimming your best-performing assets simply because they have gone up is often a mathematical error that degrades your long-term returns." — Source: Patient Capital Management Letters

- On enduring the flat periods: "Even the best compounding machines experience years of flat or negative price action. Holding through those periods is where the actual money is made." — Source: Richer, Wiser, Happier

Part 7: Contrarian Thinking

- On out-of-favor assets: "Embracing out-of-favor securities allows capital to be put to work when and where others are reluctant, setting the stage for long-term excess returns." — Source: Alpha Exchange

- On the pain of contrarianism: "True contrarianism is deeply uncomfortable. If buying a stock feels easy and reassuring, you are likely paying a premium for that comfort." — Source: Masters in Business

- On non-consensus views: "To outperform, your view must be both non-consensus and right. Being non-consensus and wrong is just a fast way to lose capital." — Source: The Meb Faber Show

- On hated industries: "We frequently search for ideas in industries that the broader market currently hates, because that is where expectations are lowest and valuations are cheapest." — Source: Patient Capital Management Letters

- On the consensus trap: "When everyone agrees that a macroeconomic outcome is a certainty, the market has usually already priced it in, eliminating the opportunity." — Source: Talking Billions

- On independent thought: "You have to actively cultivate independent thought by reading widely, stepping away from the screens, and ignoring the daily financial media noise." — Source: Richer, Wiser, Happier

- On embracing controversy: "If a company is highly controversial, it means the market is divided on its future, which is precisely the environment where mispricing occurs." — Source: Alpha Exchange

- On periods of underperformance: "Every successful contrarian strategy will endure painful periods of underperformance. If it didn't, the strategy would be arbitraged away." — Source: Masters in Business

- On avoiding groupthink: "Groupthink is the enemy of active management. You must build a culture where analysts are encouraged to present dissenting views." — Source: Patient Capital Management Letters

- On shifting sentiment: "The largest gains occur in the transition phase when a company goes from being universally hated to merely being tolerated by the market." — Source: The Meb Faber Show

Part 8: Mental Discipline and Mindset

- On focusing on the controllable: "Recognizing what is and is not within your control, and maintaining a sense of calm, turns out to be incredibly useful in markets." — Source: Masters in Business

- On mindfulness: "Practices like meditation and mindfulness are not just wellness trends; they are practical tools for maintaining mental clarity during severe market stress." — Source: Richer, Wiser, Happier

- On journaling decisions: "Writing down the exact reasons why you bought or sold a stock prevents hindsight bias and forces you to confront your actual decision-making process." — Source: Alpha Exchange

- On stoicism: "Adopting a stoic mindset helps you accept that markets will act irrationally, allowing you to focus purely on your response rather than your frustration." — Source: Talking Billions

- On managing stress: "Portfolio management is inherently stressful. If you do not have deliberate mechanisms to detach and recover, the stress will degrade your judgment." — Source: The Meb Faber Show

- On learning from mistakes: "You will make mistakes in this business. The objective is to analyze them ruthlessly without allowing them to destroy your confidence." — Source: Patient Capital Management Letters

- On cognitive stamina: "The market requires immense cognitive stamina. You have to maintain your focus and discipline day after day, regardless of the macro environment." — Source: Masters in Business

- On open-mindedness: "The moment you believe you have the market completely figured out is the moment you are about to suffer a massive loss." — Source: Alpha Exchange

- On the ultimate goal: "The goal of mental discipline isn't to eliminate emotion—it is to prevent emotion from dictating your capital allocation." — Source: Richer, Wiser, Happier