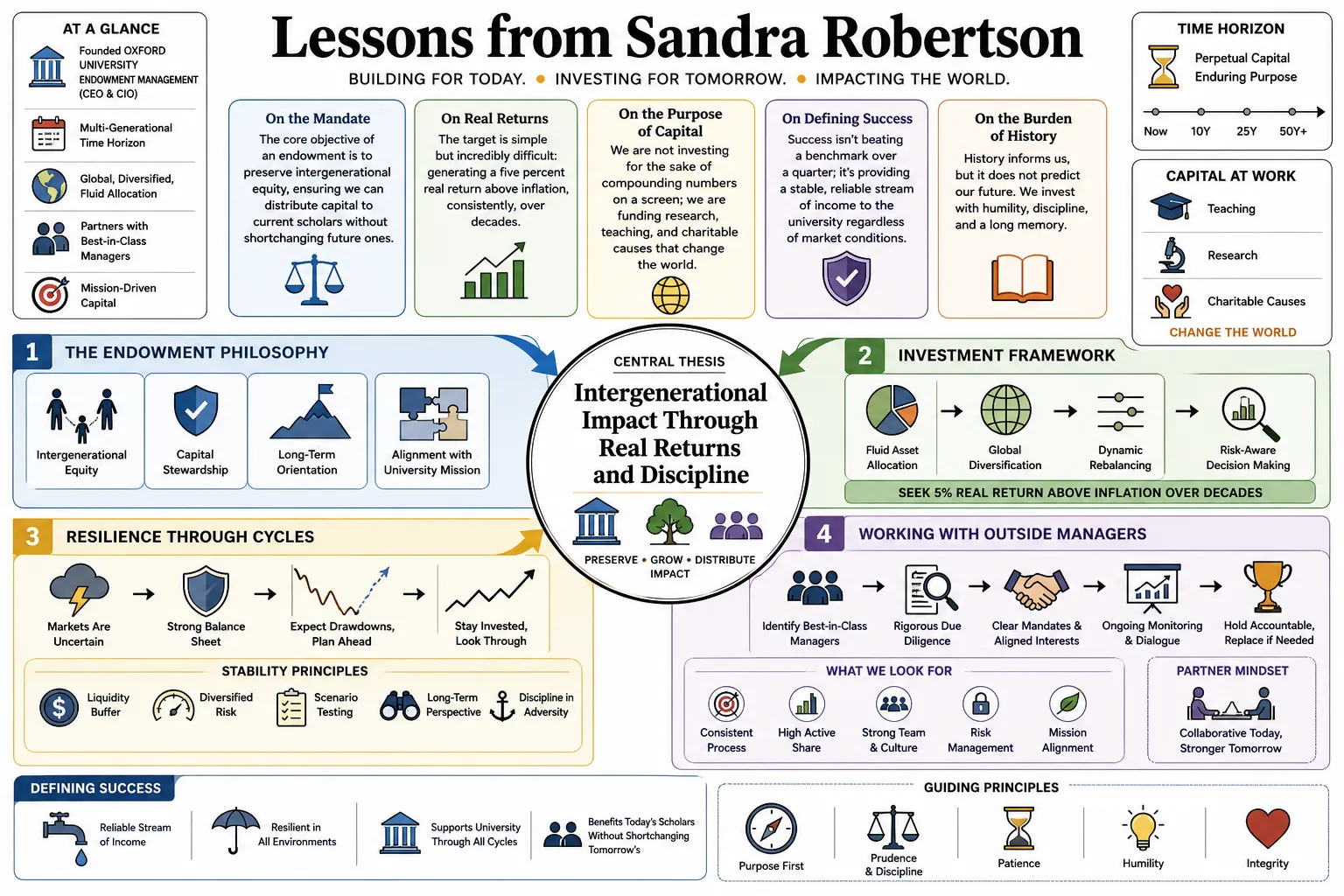

Lessons from Sandra Robertson

As the founding CEO and CIO of Oxford University Endowment Management, Sandra Robertson built the modern investment structure for the university's capital. She pairs a fluid approach to asset allocation with a strict, multi-generational time horizon. This profile outlines her framework for managing institutional portfolios, handling market drawdowns, and working with outside managers.

Part 1: The Endowment Philosophy

- On the Mandate: "The core objective of an endowment is to preserve intergenerational equity, ensuring we can distribute capital to current scholars without shortchanging future ones." — Source: [Capital Allocators Podcast]

- On Real Returns: "The target is simple but incredibly difficult: generating a five percent real return above inflation, consistently, over decades." — Source: [OUem Annual Report]

- On the Purpose of Capital: "We are not investing for the sake of compounding numbers on a screen; we are funding research, teaching, and charitable causes that change the world." — Source: [Money Maze Podcast]

- On Defining Success: "Success isn't beating a benchmark over a quarter; it's providing a stable, reliable stream of income to the university regardless of market conditions." — Source: [Capital Allocators Podcast]

- On the Burden of History: "When you manage money for an institution that is over 800 years old, you quickly realize you are just a temporary steward of the capital." — Source: [Trinity Student Managed Fund Podcast]

- On Resisting Short-Termism: "The industry is obsessed with quarterly performance, but our liabilities stretch out for centuries. We have to structure our thinking to match that reality." — Source: [Capital Allocators Podcast]

- On Inflation Risk: "For an endowment, inflation is the silent killer. Protecting purchasing power is our baseline responsibility." — Source: [OUem Annual Report]

- On the Oxford Advantage: "The name opens doors to world-class managers, but it's the permanence of our capital that keeps them interested in partnering with us." — Source: [Money Maze Podcast]

- On Distributions: "Smoothing mechanisms in our distribution policy protect the operating budget of the university from the worst volatility of the financial markets." — Source: [Capital Allocators Podcast]

- On Institutional Patience: "True patience is structural. It means having the governance and the mandate to hold through drawdowns when others are forced to sell." — Source: [Trinity Student Managed Fund Podcast]

Part 2: Asset Allocation and Fluidity

- On Rigid Asset Allocation: "We don't believe in rigid asset class buckets. The portfolio must be deliberately fluid to adapt to where the best risk-adjusted returns are." — Source: [Money Maze Podcast]

- On Relative Value: "Capital allocation is a constant exercise in relative value—comparing the opportunity set in public equities against private markets, real estate, and credit." — Source: [Capital Allocators Podcast]

- On Private Equity: "We look for private equity managers who are actually building businesses, not just applying leverage to multiple expansion." — Source: [OUem Annual Report]

- On Liquidity Constraints: "Illiquidity is a tool, not a burden. We get paid a premium to lock up capital, provided we don't need it to meet immediate distribution requirements." — Source: [Money Maze Podcast]

- On Defining Risk: "Risk is not tracking error against a peer group. Risk is the permanent impairment of capital." — Source: [Capital Allocators Podcast]

- On Public Markets: "Public markets offer liquidity, but they can be heavily influenced by short-term sentiment. We use that volatility to our advantage." — Source: [OUem Annual Report]

- On Unconstrained Investing: "Having a flexible mandate allows us to pivot. If credit markets freeze, we can step in without having to ask a committee to approve a new asset class." — Source: [Capital Allocators Podcast]

- On Real Assets: "Real assets provide essential inflation protection, but you have to be highly selective about the entry price and the quality of the underlying cash flows." — Source: [Money Maze Podcast]

- On Diversification: "Diversification only works if the underlying assets truly march to different drums. In a crisis, correlations tend to go to one." — Source: [Capital Allocators Podcast]

- On Cash Management: "Holding cash is a strategic decision. It allows you to be a provider of liquidity when everyone else is desperate for it." — Source: [Trinity Student Managed Fund Podcast]

Part 3: Managing Through Crisis and Volatility

- On Early Crisis Reactions: "During the initial shock of a crisis, it’s usually too late to sell and too early to buy. You have to sit on your hands and wait for clarity." — Source: [Capital Allocators Podcast]

- On Market Panic: "When the market panics, you need a pre-prepared shopping list. You won't have the time or the emotional bandwidth to do fundamental research in the middle of a crash." — Source: [Capital Allocators Podcast]

- On Drawing on History: "Having managed capital through the dot-com bust, the global financial crisis, and the pandemic, you learn that every crisis feels unprecedented, but the market mechanics often rhyme." — Source: [Money Maze Podcast]

- On Forced Selling: "The worst position an endowment can be in is becoming a forced seller of illiquid assets during a drawdown to meet capital calls." — Source: [Capital Allocators Podcast]

- On Crisis Communication: "Over-communicate with your board and your constituents when markets are down. Silence breeds anxiety." — Source: [OUem Annual Report]

- On Stress Testing: "We constantly stress test the portfolio for severe shocks, not to predict the future, but to ensure we can survive it." — Source: [Money Maze Podcast]

- On Calibration: "The speed of the March 2020 drawdown was breathtaking, but because we had liquidity and a flexible mandate, we could focus on calibrating the portfolio rather than panicking." — Source: [Capital Allocators Podcast]

- On Tolerating Volatility: "Volatility is the price you pay for long-term returns. If you can't stomach volatility, you will struggle to meet a five percent real return target." — Source: [Trinity Student Managed Fund Podcast]

- On Recovery Phases: "The market often prices in a full economic recovery long before the underlying economic data confirms it. You have to be willing to hold through the noise." — Source: [Capital Allocators Podcast]

Part 4: Partnering with Managers

- On Selecting Managers: "We are not just hiring money managers; we are seeking true partners who view our capital as an extension of their own." — Source: [Money Maze Podcast]

- On Alignment: "Alignment of interests is paramount. We want managers who have a significant portion of their own net worth invested alongside us." — Source: [Capital Allocators Podcast]

- On Capacity Constraints: "The best managers are often the ones who close their funds to new capital because they recognize that asset bloat is the enemy of returns." — Source: [OUem Annual Report]

- On Manager Turnover: "We evaluate managers on a decade-long horizon. Firing a manager after three years of underperformance usually means you hired them for the wrong reasons." — Source: [Money Maze Podcast]

- On Contrarian Managers: "It is uncomfortable to invest with managers who are genuinely contrarian, because they will look wrong for long stretches of time before they look right." — Source: [Capital Allocators Podcast]

- On Fee Structures: "Fees must be justified by true alpha generation. We will not pay hedge fund fees for beta dressed up as skill." — Source: [Trinity Student Managed Fund Podcast]

- On Intellectual Honesty: "The trait I look for most in a manager is intellectual honesty—the ability to admit when an investment thesis was wrong and adapt." — Source: [Money Maze Podcast]

- On Specialization: "We prefer managers who have a deep, narrow edge in a specific sector or geography, rather than generalists trying to do everything." — Source: [Capital Allocators Podcast]

- On Being a Good LP: "As a permanent capital vehicle, we strive to be the limited partner that managers call first when they have a unique, capacity-constrained idea." — Source: [OUem Annual Report]

Part 5: The Multi-Generational Horizon

- On the Concept of Time: "Time is the single greatest edge an endowment has. We can look past the next quarter, the next year, and even the next decade." — Source: [Capital Allocators Podcast]

- On Compounding: "Compounding is a slow, quiet process. The hardest part of the job is letting it happen without interrupting it unnecessarily." — Source: [Money Maze Podcast]

- On Long-Term Themes: "We try to identify structural shifts—demographics, technology, resource scarcity—that will play out over thirty years, not three." — Source: [OUem Annual Report]

- On Evaluating Decisions: "Every decision we make is weighed against the question: Does this serve the Oxford student of 2050 as well as the student of today?" — Source: [Trinity Student Managed Fund Podcast]

- On Short-Term Noise: "The financial media is designed to induce anxiety and provoke action. An endowment manager must learn to tune out the daily noise." — Source: [Capital Allocators Podcast]

- On Precision: "You cannot precisely model the global economy five years out. You can only position the portfolio to be robust across a range of possible futures." — Source: [Money Maze Podcast]

- On the J-Curve: "In private equity and venture capital, the J-curve requires extreme patience. You are planting seeds that you won't harvest for seven to ten years." — Source: [OUem Annual Report]

- On Performance Measurement: "One-year returns are largely noise. Three-year returns show a trend. Ten-year returns reveal whether your strategy actually works." — Source: [Capital Allocators Podcast]

- On Enduring Institutions: "Oxford has survived plagues, world wars, and economic depressions. The endowment's portfolio must be built to weather similar existential shocks." — Source: [Trinity Student Managed Fund Podcast]

Part 6: Governance and Institutional Alignment

- On the Investment Committee: "An investment committee should provide strategic oversight and challenge our thinking, but they should not be picking individual stocks or managers." — Source: [Capital Allocators Podcast]

- On Trust: "Trust between the investment team and the board is the foundation of a successful endowment. Without it, you cannot sustain a contrarian position during a drawdown." — Source: [Money Maze Podcast]

- On Clear Mandates: "A vaguely defined investment mandate is a recipe for disaster. Both the university and the investment office must agree exactly on what success looks like." — Source: [OUem Annual Report]

- On Managing Stakeholders: "Managing an endowment involves managing the expectations of a highly intelligent, highly opinionated academic community." — Source: [Trinity Student Managed Fund Podcast]

- On Independent Thinking: "Groupthink is dangerous in governance. We need committee members who are willing to ask the obvious, difficult questions." — Source: [Capital Allocators Podcast]

- On Complexity Limits: "If you cannot explain an investment strategy simply to a board of trustees, it is probably too complex to own." — Source: [Money Maze Podcast]

- On Delegation: "Effective governance requires delegating execution to the professionals while retaining control over the broad asset allocation parameters." — Source: [OUem Annual Report]

- On Policy Portfolios: "A policy portfolio is a useful anchor, but it should not become a straitjacket that prevents the team from exploiting market dislocations." — Source: [Capital Allocators Podcast]

- On Institutional Memory: "Documenting why decisions were made is critical. When the market turns, you need to remind the board of the original thesis to prevent panic selling." — Source: [Money Maze Podcast]

Part 7: ESG and Sustainable Investing

- On the Evolution of ESG: "ESG is not a separate bucket or a compliance exercise; it is a fundamental framework for assessing the long-term viability of a business." — Source: [Capital Allocators Podcast]

- On Climate Transition: "The transition to a low-carbon economy is one of the most significant investment themes of our time. It carries both immense risks and massive opportunities." — Source: [Money Maze Podcast]

- On Engagement vs. Divestment: "Blanket divestment often means you lose your seat at the table. We prefer to engage with managers and companies to drive structural change." — Source: [OUem Annual Report]

- On Greenwashing: "We are highly skeptical of managers who simply rebrand their existing strategies as sustainable. We look for authentic, verifiable integration of ESG principles." — Source: [Trinity Student Managed Fund Podcast]

- On the Cost of Carbon: "Any long-term financial model that ignores the future cost of carbon emissions is inherently flawed." — Source: [Capital Allocators Podcast]

- On Social Responsibility: "An endowment tied to a major university has a reputational risk profile that requires us to be acutely aware of the social impact of our investments." — Source: [Money Maze Podcast]

- On Data Quality: "The biggest challenge in sustainable investing right now is the inconsistency of data. We spend significant time interrogating the metrics our managers report." — Source: [OUem Annual Report]

- On Governance within ESG: "The 'G' in ESG is often the most critical. Poor governance is the root cause of almost every major corporate failure." — Source: [Capital Allocators Podcast]

- On Investing in Solutions: "We are actively seeking out companies that are developing the technologies and infrastructure necessary to solve the climate crisis." — Source: [Money Maze Podcast]

- On the Nuance of Sustainability: "Sustainability is rarely black and white. It requires a nuanced understanding of supply chains, labor practices, and regulatory environments." — Source: [Trinity Student Managed Fund Podcast]

Part 8: Leadership and Team Building

- On Building a Culture: "An investment office must have a culture of intellectual curiosity, where junior analysts feel empowered to debate the CIO." — Source: [Capital Allocators Podcast]

- On Hiring Talent: "We hire for temperament and cognitive diversity. You can teach financial modeling, but you cannot teach someone to remain calm during a market crash." — Source: [Money Maze Podcast]

- On Retention: "To retain top talent in an endowment setting, you have to align them with the mission. They must care about the university, not just the bonus." — Source: [OUem Annual Report]

- On Mistakes: "Mistakes are inevitable. The key is to have a post-mortem process that focuses on what went wrong with the decision-making process, rather than assigning blame." — Source: [Capital Allocators Podcast]

- On Mentorship: "My time at the Wellcome Trust taught me the importance of apprenticing under experienced investors. I view mentoring my team at Oxford as a core responsibility." — Source: [Trinity Student Managed Fund Podcast]

- On Leadership During a Crisis: "In a crisis, the team is looking to the CIO for stability. You have to absorb the anxiety of the market so your team can focus on their research." — Source: [Money Maze Podcast]

- On the Value of Generalists: "While we want specialized external managers, I prefer generalists on my internal team who can connect dots across different asset classes." — Source: [Capital Allocators Podcast]

- On Continuous Learning: "The market is a humbling machine. The day you stop reading, learning, and questioning your assumptions is the day you start losing money." — Source: [OUem Annual Report]

- On Stepping Down: "Succession planning is the final duty of a founder. Leaving the endowment in capable hands ensures the mission continues long after you are gone." — Source: [Trinity Student Managed Fund Podcast]