Lessons from Sarah Samuels

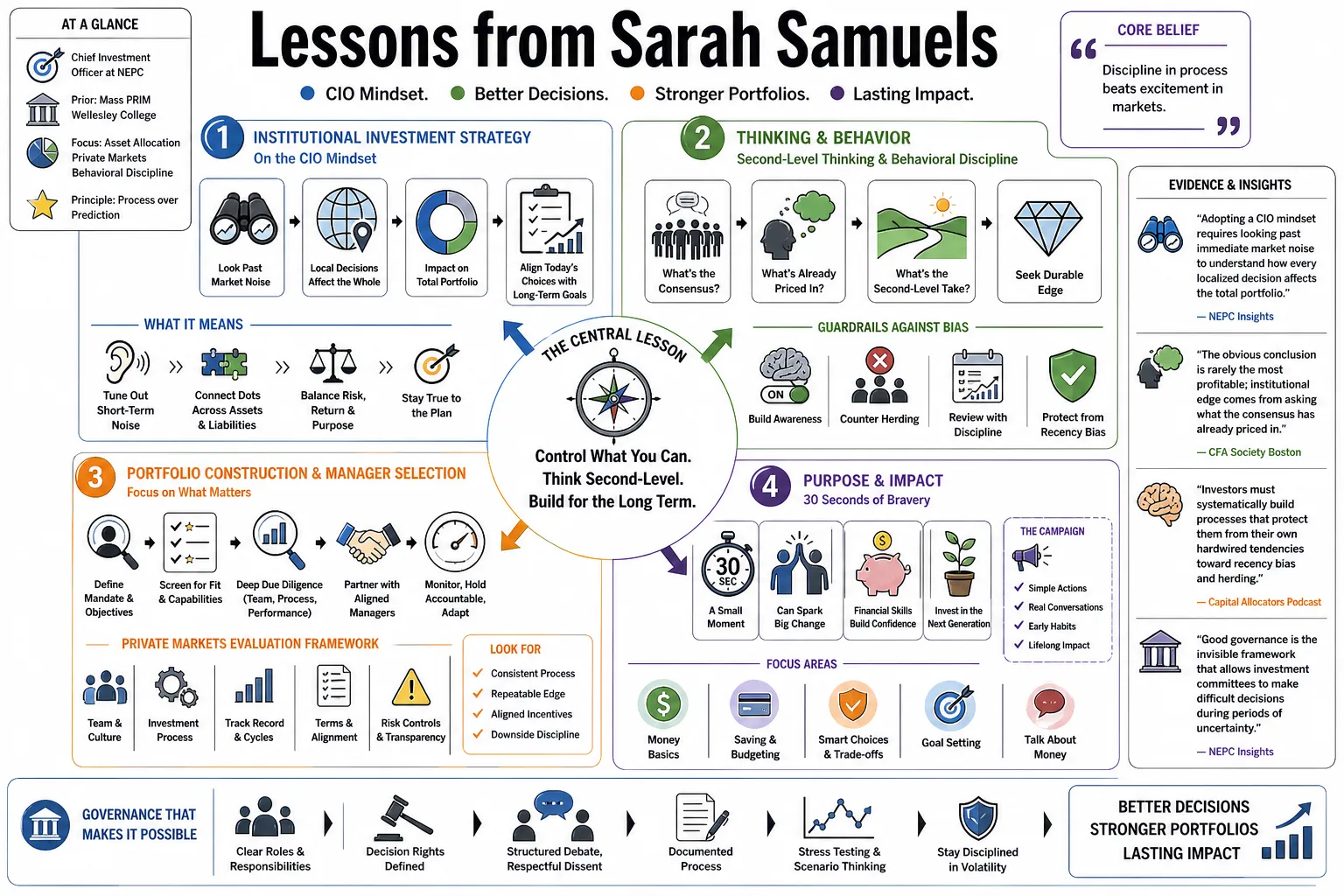

Sarah Samuels is the Chief Investment Officer at NEPC, managing asset allocation for institutional portfolios following earlier roles at Mass PRIM and Wellesley College. Her work centers on keeping behavioral biases in check and evaluating private market managers. This profile outlines her approach to manager selection and portfolio construction, alongside her "30 Seconds of Bravery" campaign for childhood financial literacy.

Part 1: Institutional Investment Strategy

- On the CIO mindset: "Adopting a CIO mindset requires looking past immediate market noise to understand how every localized decision affects the total portfolio." — Source: NEPC Insights

- On second-level thinking: "The obvious conclusion is rarely the most profitable; institutional edge comes from asking what the consensus has already priced in." — Source: CFA Society Boston

- On behavioral bias: "Investors must systematically build processes that protect them from their own hardwired tendencies toward recency bias and herding." — Source: Capital Allocators Podcast

- On governance: "Good governance is the invisible framework that allows investment committees to make difficult decisions during periods of maximum uncertainty." — Source: NEPC Research

- On long-term horizons: "Endowment models succeed because they align illiquidity constraints with perpetual time horizons, allowing them to harvest premiums others cannot hold." — Source: Wellesley College Investment Office

- On public vs. private models: "The line between public and private investing is blurring, requiring institutions to evaluate risk factors across the entire capital structure rather than in silos." — Source: S&P Global Private Markets 360

- On continuous learning: "Markets are highly adaptive systems; an investment process that worked perfectly a decade ago will naturally decay if it is not constantly refined." — Source: CFA Society Boston

- On risk management: "Risk is not a single number on a spreadsheet; it is the probability of failing to meet the institution's primary objectives." — Source: Mass PRIM Publications

- On scale: "Managing large pools of state pension assets forces you to focus on macro asset allocation, because manager alpha simply cannot scale enough to move the needle alone." — Source: Mass PRIM Reports

- On alignment: "An effective consultant must fully align their success metrics with the long-term viability of the client's fund." — Source: NEPC Consulting

Part 2: The Evolution of Private Markets

- On secondaries: "The secondary market has shifted from being a Hail Mary move for distressed funds to a primary investment tool today for portfolio construction and management." — Source: S&P Global Private Markets 360

- On private market maturity: "Private equity is no longer an alternative asset class; for many large institutions, it is the core driver of growth." — Source: NEPC Private Markets Report

- On lower middle markets: "The lower middle market offers distinct inefficiencies where skilled operators can build value through actual business improvement, rather than relying on financial engineering." — Source: Capital Allocators Podcast

- On capital raising: "The dynamics of fundraising have changed, forcing general partners to clearly articulate their specific operational edge to secure capital." — Source: Private Equity Women Investor Network

- On valuations: "Lagging private valuations can create a false sense of security during public market drawdowns, making accurate cash flow forecasting essential." — Source: NEPC Insights

- On co-investments: "Co-investing is a powerful tool to reduce fee drag, but it requires the institution to have the internal resources to make rapid, high-conviction decisions." — Source: Mass PRIM Reports

- On illiquidity premiums: "Investors must constantly verify that the return they are getting in private markets actually compensates them for locking up their capital for ten years." — Source: NEPC Research

- On manager specialization: "Generalist funds are struggling to compete with sector specialists who bring deep operational playbooks to their portfolio companies." — Source: S&P Global Private Markets 360

- On venture capital: "Venture requires a completely different mindset from buyout; you are underwriting the magnitude of success, not the probability of failure." — Source: TBD Angels Network

Part 3: Manager Selection and Due Diligence

- On succession planning: "Analyzing a firm's succession plan is a primary investment risk; a poorly handled transition will destroy alpha." — Source: Capital Allocators Podcast

- On past performance: "Historical returns tell you what a manager achieved, but deep due diligence reveals whether the conditions that created those returns are repeatable." — Source: NEPC Manager Research

- On qualitative analysis: "The numbers get you in the door, but the final allocation decision depends on evaluating the culture, alignment, and intellectual honesty of the team." — Source: CFA Society Boston

- On team dynamics: "We watch how portfolio managers interact with their analysts; dominant personalities who stifle debate are a red flag for future underperformance." — Source: NEPC Insights

- On capacity constraints: "A great strategy can ruin its own returns if the manager accepts more assets than their specific market niche can absorb." — Source: Wellesley College Investment Office

- On intellectual humility: "The best investors readily admit when they are wrong and adapt; those who stubbornly defend losing theses are dangerous to institutional capital." — Source: Capital Allocators Podcast

- On alignment of interests: "We require managers to invest heavily alongside our clients so that they feel the pain of capital impairment personally." — Source: Mass PRIM Reports

- On emerging managers: "Allocating to newer, hungry funds often yields better alignment and performance than sticking solely to massive, established mega-funds." — Source: Private Equity Women Investor Network

- On operational diligence: "A brilliant investment strategy is useless if the back office is disorganized; operational failure is an uncompensated risk." — Source: NEPC Manager Research

Part 4: Asset Allocation and Portfolio Construction

- On diversification: "True diversification means finding assets that behave differently during stress, rather than holding fifty versions of the same economic bet." — Source: NEPC Asset Allocation

- On absolute return: "Hedge funds must serve a specific utility in the portfolio, whether that is equity beta mitigation or providing uncorrelated cash flows." — Source: Mass PRIM Reports

- On inflation protection: "Institutions must build resilient portfolios that can withstand prolonged periods of sticky inflation, moving beyond the traditional sixty-forty model." — Source: NEPC Insights

- On liquidity management: "Over-committing to private markets during a bull run often leads to a liquidity squeeze when capital calls accelerate and distributions dry up." — Source: S&P Global Private Markets 360

- On strategic pacing: "Maintaining a steady, vintage-year pacing model in private equity prevents you from trying to time a market that cannot be timed." — Source: Wellesley College Investment Office

- On thematic investing: "Thematic bets must be sized appropriately; they are meant to capture long-term tailwinds, never to dominate the core allocation." — Source: NEPC Research

- On rebalancing: "Disciplined rebalancing is painful because it forces you to sell winners and buy losers, but it is mathematically essential for risk control." — Source: Mass PRIM Publications

- On fixed income: "The role of core bonds has shifted from purely yield generation back to providing a structural anchor against equity volatility." — Source: NEPC Asset Allocation

- On capital efficiency: "Employing judicious leverage at the portfolio level can sometimes improve the risk-return profile better than taking aggressive active risk within asset classes." — Source: Capital Allocators Podcast

Part 5: Financial Literacy and Early Education

- On early concepts: "Learning how to manage money at an early age provides a foundation that breaks generational cycles of financial uncertainty." — Source: Braving Our Savings

- On the 30 Seconds of Bravery: "So many things were scary during that time, but I kept choosing to be brave, if only for thirty seconds." — Source: Boston University Alumni Magazine

- On accessibility: "Financial concepts like stocks, bonds, and diversification can be made accessible and engaging for children of all backgrounds." — Source: Simon & Schuster Authors

- On representation: "Children need to see characters who look like them actively making smart decisions about saving and investing." — Source: 30 Seconds of Bravery

- On goal setting: "Teaching a child to save for a specific goal, like getting their ears pierced, translates abstract math into tangible delayed gratification." — Source: Braving Our Savings

- On systemic gaps: "The education system rarely teaches personal finance, leaving families responsible for instilling money habits that dictate future stability." — Source: NEPC Community Initiatives

- On compound interest: "Understanding compound growth early in life is the single most powerful tool for building long-term independence." — Source: 30 Seconds of Bravery

- On financial fear: Samuels links financial literacy to breaking a generations-long fear of money and institutions, using Braving Our Savings and athlete partnerships to make investing visible to children who may not have finance role models. — Reference: NEPC excerpt of Institutional Investor on Samuels, Braving Our Savings, financial fear, and children's financial literacy

- On philanthropy: "Giving back is a core component of financial education; children should learn that capital can be used to support their communities." — Source: 30 Seconds of Bravery

- On actionable habits: "Knowledge without action is useless; financial literacy programs must result in children actually opening and managing a savings account." — Source: Braving Our Savings

Part 6: Diversity, Equity, and Inclusion

- On systemic barriers: "I was told no many, many times for different roles or requests, which fueled my desire to help others rise in the industry." — Source: NEPC Insights

- On cognitive diversity: "A team of people with identical backgrounds will inevitably share the same blind spots; diversity of thought is a risk management tool." — Source: CFA Society Boston

- On entry-level pipelines: "Organizations like Girls Who Invest are important because they address the pipeline problem at the college level, before self-selection limits the talent pool." — Source: Girls Who Invest

- On female leadership: "Women in private markets often lack senior role models; creating networks provides the blueprint for navigating partnership tracks." — Source: Private Equity Women Investor Network

- On equitable capital: "Supporting diverse founders through angel investing is a direct way to shift the demographics of who gets to build wealth in the technology sector." — Source: TBD Angels Network

- On sponsorship vs. mentorship: Samuels's advancement work goes beyond private advice: NEPC credits her with expanding visibility and opportunity through the Women's Leadership Forum, PEWIN Boston, CFA Society Boston, Girls Who Invest, and diverse-manager efforts. — Reference: NEPC profile on Samuels's Women's Leadership Forum, PEWIN, CFA Society Boston, Girls Who Invest, and diversity work

- On retaining talent: "Firms lose diverse talent in the middle ranks because they fail to provide clear, unbiased metrics for progression to partnership." — Source: NEPC Diversity Initiatives

- On network building: "Founding the Boston chapter of PEWIN was about creating a localized space where senior women could execute deals and share unvarnished intelligence." — Source: Private Equity Women Investor Network

- On unconscious bias: "Investment committees must actively review their selection criteria to ensure they are not penalizing emerging managers for lacking a legacy track record." — Source: NEPC Manager Research

- On taking space: "Underrepresented professionals often wait to be invited to the table; you have to pull up a chair and make your voice heard." — Source: CFA Society Boston

Part 7: Leadership and Career Resilience

- On non-traditional paths: "Starting as an administrative assistant with a degree in German proved that success in finance relies on tenacity rather than a specific undergraduate pedigree." — Source: NEPC Insights

- On hard work: In a Pensions & Investments profile excerpted by NEPC, Samuels names "extremely hard work" and tenacity after many noes as factors in a non-traditional path from administrative assistant to NEPC partner. — Reference: NEPC excerpt of Pensions & Investments on Samuels's non-traditional path, hard work, noes, and tenacity

- On taking risks: "Career growth happens in the margins of discomfort; if you are entirely confident in your ability to do a new job, you have waited too long to take it." — Source: Capital Allocators Podcast

- On leading teams: "A strong leader absorbs pressure from above and distributes credit below, creating an environment where analysts feel safe sharing contrarian views." — Source: NEPC Leadership

- On overcoming rejection: "Hearing no is data rather than a final verdict; it clarifies what you need to build before you ask the next time." — Source: 30 Seconds of Bravery

- On building consensus: "As a CIO, you cannot force a decision through sheer authority; you have to build intellectual consensus among the committee members." — Source: Mass PRIM Publications

- On imposter syndrome: Samuels describes a non-traditional entry into investing, repeated noes, and tenacity; the safer lesson is that preparation and persistence can turn an unconventional background into a reason to help others rise. — Reference: NEPC excerpt of Pensions & Investments on Samuels's non-traditional career path, repeated noes, tenacity, and helping others rise

- On authentic leadership: "You do not have to adopt an aggressive persona to succeed in finance; emotional intelligence and clear communication are far more effective." — Source: CFA Society Boston

- On continuous evolution: "The role you have today will look completely different in five years; your ability to adapt to new market regimes is your ultimate job security." — Source: NEPC Insights

Part 8: The Future of Finance and Innovation

- On artificial intelligence: "AI will not replace fundamental analysts, but analysts who use AI effectively will replace those who refuse to adapt to new data processing tools." — Source: CFA Society Boston

- On data edge: "The sheer volume of alternative data available today means institutional edge has shifted from acquiring information to correctly interpreting it." — Source: NEPC Research

- On democratization of alternatives: "We are seeing a structural shift where retail investors are gaining access to private markets, which requires entirely new frameworks for liquidity and education." — Source: S&P Global Private Markets 360

- On energy transition: "The shift toward renewable energy represents a multi-decade capital deployment cycle that will redefine infrastructure portfolios." — Source: NEPC Asset Allocation

- On digital assets: "While the volatility of crypto remains high, the underlying blockchain technology offers undeniable efficiencies for clearing and settlement." — Source: CFA Society Boston

- On globalization: "Supply chain realignment is creating localized investment opportunities in manufacturing and logistics that we have not seen in decades." — Source: Mass PRIM Reports

- On fee structures: "The industry is slowly moving toward fee structures that strictly reward actual alpha generation rather than simply charging for beta exposure." — Source: NEPC Manager Research

- On regulatory shifts: "Increasing regulatory scrutiny in private markets will inevitably raise compliance costs, which will favor larger managers with the scale to absorb them." — Source: S&P Global Private Markets 360

- On the role of consultants: "The future consulting model relies on becoming an extension of the client's staff, utilizing technology to provide real-time portfolio transparency." — Source: NEPC Consulting