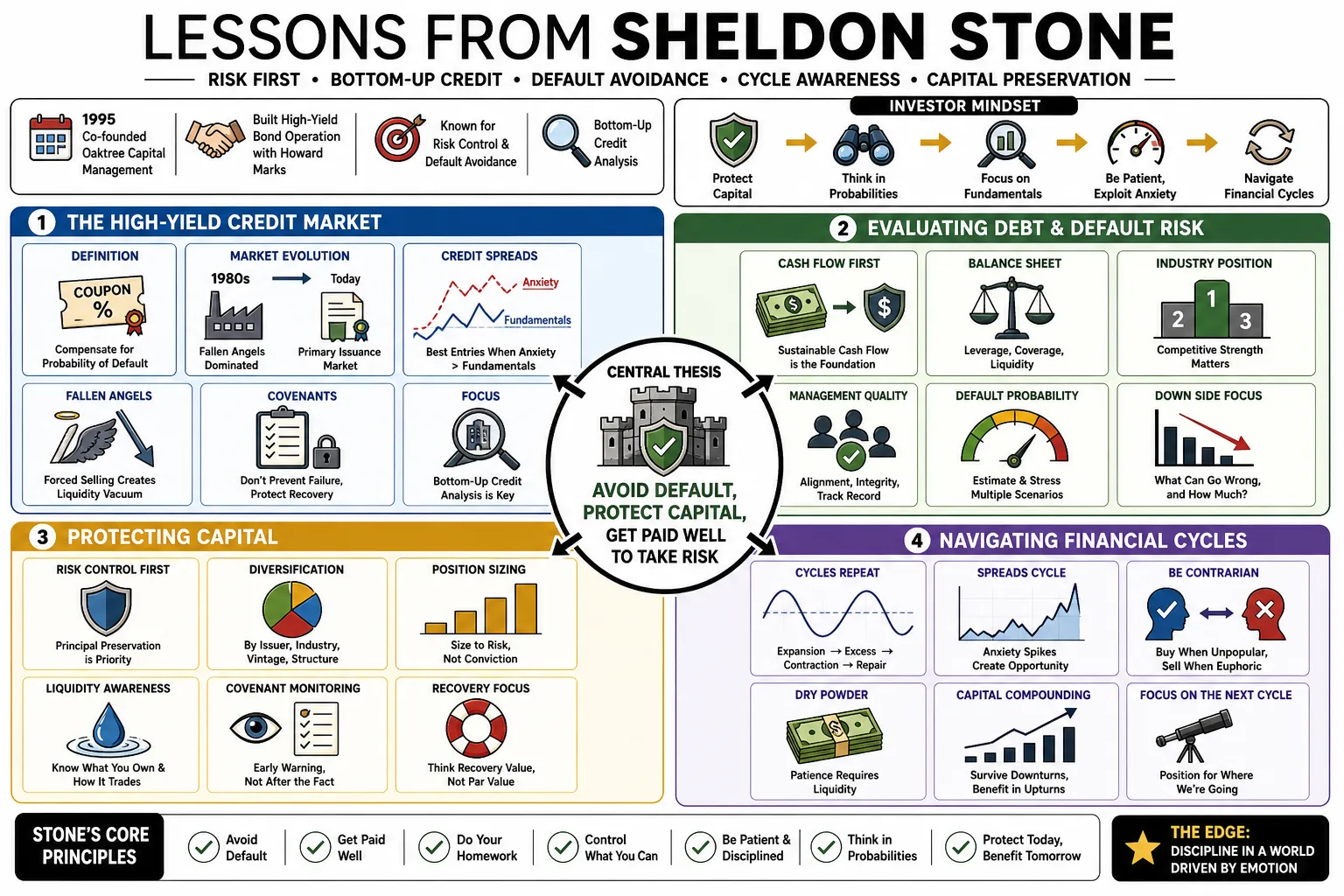

Sheldon Stone co-founded Oaktree Capital Management in 1995 and established its high-yield bond operation alongside Howard Marks. He is known for his strict focus on risk control, default avoidance, and bottom-up credit analysis. This profile collects his core principles on evaluating debt, protecting capital, and navigating financial cycles.

Part 1: The High-Yield Credit Market

- On high-yield definition: "High yield is about ensuring that the coupon adequately compensates for the probability of default." — Source: [Oaktree Memos]

- On the origin of the market: "When we started in the 1980s, the market was mostly fallen angels. Today, it is a primary issuance market that requires a completely different analytical toolkit." — Source: [Financial Times Interview]

- On credit spreads: "Spreads are a measure of market anxiety alongside default risk. When anxiety outpaces fundamental deterioration, we find our most compelling entry points." — Source: [Oaktree Insights Podcast]

- On fallen angels: "A fallen angel represents an opportunity because institutional mandates often force selling regardless of the underlying credit quality, creating a liquidity vacuum we can step into." — Source: [Bloomberg Markets]

- On covenants: "Covenants do not prevent bad businesses from failing, but they dictate who holds the negotiating power when a restructuring inevitably occurs." — Source: [Oaktree Client Conference]

- On yield-to-worst: "We manage portfolios based on yield-to-worst because in credit, the upside is capped by the call price while the downside is a complete loss of principal." — Source: [Oaktree Memos]

- On market evolution: "The high-yield market has grown exponentially in size and complexity, yet the fundamental math of credit risk and recovery rates remains unchanged." — Source: [High-Yield Bond Commentary]

- On the role of rating agencies: "Ratings are backward-looking indicators. If you wait for a downgrade to sell or an upgrade to buy, you have already missed the price action." — Source: [Columbia Business School Address]

- On primary issuance: "The quality of new issuance is the clearest indicator of where we are in the credit cycle. When lenders accept weak covenants and low yields, caution is mandatory." — Source: [Oaktree Memos]

- On liquidity: "In the bond market, liquidity is a mirage that disappears exactly when you need it most. You must construct the portfolio assuming you cannot sell your way out of a mistake." — Source: [Wall Street Journal Profile]

Part 2: Risk Control and Downside Protection

- On avoiding losers: "Our entire philosophy is built on the premise that if we avoid the defaults, the yield will take care of the returns." — Source: [Oaktree Client Conference]

- On the asymmetry of credit: "Equities offer asymmetric upside while credit offers asymmetric downside. A bondholder's best-case scenario is getting their money back with interest." — Source: [Oaktree Memos]

- On capital preservation: "In fixed income, you do not recover from large drawdowns by hitting home runs. You recover by avoiding the drawdown in the first place." — Source: [Oaktree Insights Podcast]

- On default rates: "A zero percent default rate is not the goal. The goal is a default rate significantly lower than what the market has priced into the aggregate spread." — Source: [High-Yield Bond Commentary]

- On margin of safety: "A margin of safety in credit is achieved through asset coverage, cash flow visibility, and structural seniority. You need at least two of the three." — Source: [Columbia Business School Address]

- On diversification: "Diversification is our first line of defense against the idiosyncratic risks that our fundamental analysis might miss." — Source: [Oaktree Memos]

- On downside scenarios: "We spend the vast majority of our time analyzing what happens if the business underperforms its base case, because the upside takes care of itself." — Source: [Financial Times Interview]

- On risk vs. volatility: "Volatility is distinct from risk. Risk is the permanent impairment of capital resulting from a default with a poor recovery." — Source: [Oaktree Insights Podcast]

- On stress testing: "You must stress test cash flows against the worst economic conditions seen in the last decade, rather than the mildest recession." — Source: [Bloomberg Markets]

- On taking risk: "Risk control differs from risk avoidance. We take risk intentionally, but only when we are being disproportionately paid for it." — Source: [Oaktree Memos]

Part 3: Navigating Market Cycles

- On cycle awareness: "We do not forecast the macro economy, but we are acutely aware of where we stand in the credit cycle based on the behavior of other lenders." — Source: [Oaktree Client Conference]

- On market timing: "You cannot time the exact bottom or top. You can only calibrate your aggressiveness based on the prevailing temperature of the market." — Source: [Wall Street Journal Profile]

- On early cycle behavior: "At the beginning of a cycle, capital is scarce, spreads are wide, and terms are strict. That is when you want to be fully invested." — Source: [Oaktree Memos]

- On late cycle behavior: "When capital is plentiful and investors are stretching for yield by accepting weaker covenants, it is time to increase quality and shorten duration." — Source: [Financial Times Interview]

- On credit contractions: "Credit windows do not close slowly. They slam shut. You must have your portfolio positioned defensively before the panic starts." — Source: [Oaktree Insights Podcast]

- On contrarianism: "Being a contrarian is uncomfortable, but doing what everyone else is doing guarantees average results at best and disaster at worst." — Source: [Oaktree Memos]

- On market psychology: "The credit market swings like a pendulum from flawless execution being priced in, to impending doom being assumed. The truth is always in the middle." — Source: [Bloomberg Markets]

- On distressed cycles: "A distressed debt cycle is born during the preceding boom when too much money chases too few good ideas." — Source: [High-Yield Bond Commentary]

- On buying opportunities: "The best buys happen when forced selling meets a complete absence of liquidity. That is when you dictate the terms." — Source: [Oaktree Client Conference]

- On patience: "Sometimes the hardest thing to do in investing is absolutely nothing, waiting for the cycle to present an opportunity that fits our criteria." — Source: [Columbia Business School Address]

Part 4: Investment Philosophy

- On consistency: "We aim for top-quartile performance in bad years and average performance in good years. Over a decade, that math produces exceptional compounded returns." — Source: [Oaktree Memos]

- On specialization: "We believe in deep specialization. You cannot be a part-time participant in the high-yield market and expect to beat dedicated professionals." — Source: [Financial Times Interview]

- On macro forecasting: "We spend zero time trying to predict interest rates or GDP growth. We focus entirely on the microeconomics of the companies we lend to." — Source: [Oaktree Insights Podcast]

- On knowledge advantage: "Our edge is having a deeper understanding of the capital structure and the bankruptcy code, rather than possessing better economic forecasts." — Source: [Wall Street Journal Profile]

- On investment process: "A repeatable process is more important than a brilliant intuition. Intuition fails under stress while process holds steady." — Source: [Oaktree Client Conference]

- On absolute vs. relative return: "We are absolute return investors operating in a relative return world. We will hold cash if the market offers no compelling investments." — Source: [Bloomberg Markets]

- On complexity: "We do not seek out complexity for its own sake, but we embrace it when it obscures fundamental value and drives away other investors." — Source: [Oaktree Memos]

- On intellectual honesty: "You must be willing to admit when a thesis is broken. Holding onto a losing position out of pride destroys track records." — Source: [High-Yield Bond Commentary]

- On the role of luck: "You have to construct portfolios that can survive bad luck, because eventually everyone experiences it." — Source: [Columbia Business School Address]

Part 5: Bottom-Up Credit Analysis

- On cash flow: "Earnings can be manipulated, but cash is a fact. We analyze cash flow generation above all other financial metrics." — Source: [Oaktree Memos]

- On debt metrics: "Gross debt tells you the size of the burden, while interest coverage tells you the ability to carry it. You need both to assess survival." — Source: [Oaktree Client Conference]

- On management teams: "In distressed situations, the incumbent management team is often part of the problem. We look for businesses that can survive bad management." — Source: [Financial Times Interview]

- On enterprise value: "Lending safely requires a firm grasp on the enterprise value of the business. You must ensure the debt sits well below that threshold." — Source: [Oaktree Insights Podcast]

- On asset coverage: "Asset coverage provides the margin of safety, but cash flow pays the interest. A great asset with no cash flow is a restructuring waiting to happen." — Source: [Wall Street Journal Profile]

- On structural subordination: "You must know exactly where your claim sits in the corporate structure. Being structurally subordinated without knowing it is a fatal error." — Source: [Bloomberg Markets]

- On capital expenditures: "Understanding the difference between maintenance capex and growth capex is essential to knowing how much cash is actually available to service debt." — Source: [Oaktree Memos]

- On industry dynamics: "We avoid industries subject to rapid technological obsolescence. We prefer boring businesses with predictable cash flows." — Source: [High-Yield Bond Commentary]

- On legal documentation: "The indenture is the rulebook. If you do not read it yourself, you are trusting someone else with your capital." — Source: [Columbia Business School Address]

Part 6: Behavioral Discipline

- On emotional control: "The most important organ in investing is the stomach. You must be able to endure volatility without panic." — Source: [Oaktree Insights Podcast]

- On fear and greed: "Our job is to provide liquidity when the market is paralyzed by fear, and to take liquidity when the market is blinded by greed." — Source: [Oaktree Memos]

- On the fear of missing out: "Fear of missing out is responsible for more bad loans than any fundamental miscalculation. You must be comfortable watching others make money in the short term." — Source: [Oaktree Client Conference]

- On humility: "The market is a humbling mechanism. The moment you believe you have it completely figured out is the moment you are about to lose money." — Source: [Wall Street Journal Profile]

- On objective analysis: "We train our analysts to decouple their view of a company's product from their view of its debt. A great product does not guarantee a safe bond." — Source: [Financial Times Interview]

- On peer pressure: "In institutional investing, the pressure to conform is immense. Sticking to a disciplined process requires institutional support from the top down." — Source: [Bloomberg Markets]

- On reacting to news: "Most daily news is noise. We react to changes in fundamental cash flow expectations, ignoring short-term headlines." — Source: [High-Yield Bond Commentary]

- On overconfidence: "During a long bull market, investors confuse the absence of defaults with their own brilliance. We never make that mistake." — Source: [Oaktree Memos]

- On admitting mistakes: "When a bond drops heavily in price, the first question is whether our original thesis was flawed, before deciding to buy or sell." — Source: [Columbia Business School Address]

Part 7: Institutional Building and Oaktree

- On partnership: "Oaktree was built on a foundation of intellectual partnership. No single person has a monopoly on good ideas." — Source: [Oaktree Client Conference]

- On firm culture: "A culture of risk control cannot be imposed. It must be ingrained in every hiring decision and compensation structure." — Source: [Wall Street Journal Profile]

- On aligning interests: "We invest heavily alongside our clients because alignment of interest is the only way to ensure true fiduciary behavior." — Source: [Oaktree Memos]

- On hiring: "We look for analysts who are inherently skeptical. Optimists make great equity investors, but they make terrible credit analysts." — Source: [Oaktree Insights Podcast]

- On team stability: "The stability of our team is our biggest competitive advantage. You cannot navigate a credit cycle if your team turns over every three years." — Source: [Financial Times Interview]

- On client communication: "We communicate as candidly in bad times as we do in good times. Trust is built during the drawdowns." — Source: [Bloomberg Markets]

- On scaling: "We only grow our assets under management when the opportunity set expands. We have returned capital when the market became too frothy." — Source: [Oaktree Memos]

- On decision making: "Investment decisions must be debated vigorously, but once a decision is made, the portfolio manager owns the outcome entirely." — Source: [High-Yield Bond Commentary]

- On legacy: "The true measure of a firm is whether its philosophy outlives its founders. We built Oaktree to be a multi-generational institution." — Source: [Columbia Business School Address]

Part 8: Long-Term Compounding and Consistency

- On the power of compounding: "Compounding is the eighth wonder of the world, but it only works if you avoid the large losses that interrupt the math." — Source: [Oaktree Memos]

- On short-termism: "The financial industry is obsessed with quarterly performance. We optimize exclusively for the five-to-ten-year horizon." — Source: [Oaktree Insights Podcast]

- On survival: "To finish first, you must first finish. Survival in bear markets is the prerequisite for long-term outperformance." — Source: [Financial Times Interview]

- On measuring success: "Success is not beating a benchmark in a roaring bull market. Success is delivering the promised return over a full cycle with less risk." — Source: [Oaktree Client Conference]

- On market efficiency: "The high-yield market is inefficient enough to reward hard work, but efficient enough that you cannot rely on obvious mispricings." — Source: [Wall Street Journal Profile]

- On the illusion of certainty: "We deal in probabilities rather than certainties. The best we can do is stack the odds heavily in our favor." — Source: [Bloomberg Markets]

- On continuous learning: "Every default is a tuition payment. If you do not learn from it and adjust your process, you have wasted the capital." — Source: [Oaktree Memos]

- On historical context: "Financial history rhymes. Understanding past crises is necessary for navigating the ones that are yet to come." — Source: [High-Yield Bond Commentary]

- On the ultimate goal: "Our goal has never been to be the biggest firm; it has been to be the most trusted steward of capital in the credit markets." — Source: [Columbia Business School Address]