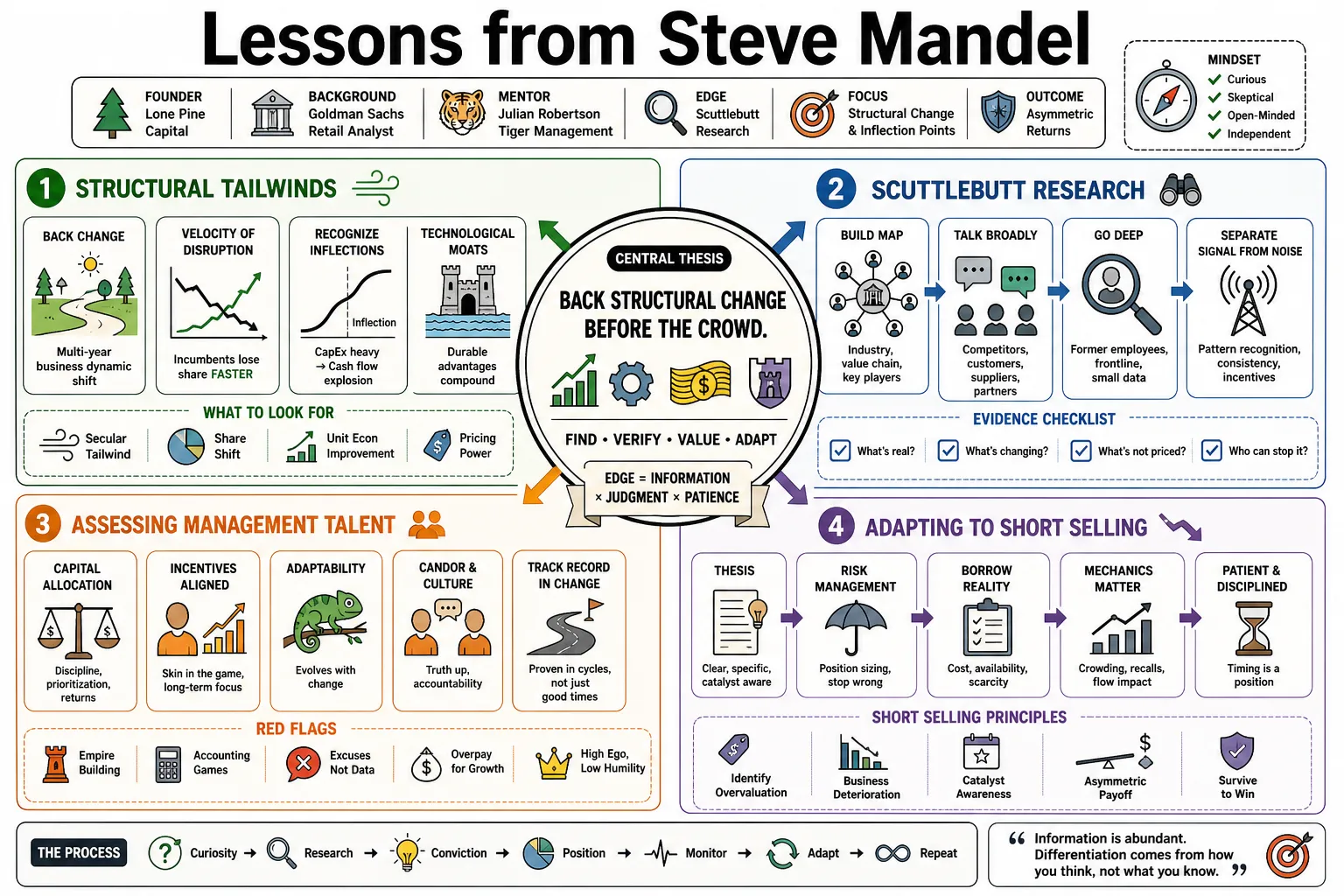

Lessons from Steve Mandel

Steve Mandel founded Lone Pine Capital after working as a retail analyst at Goldman Sachs and training under Julian Robertson at Tiger Management. He built his track record on intensive "scuttlebutt" research, routinely interviewing competitors and former employees to evaluate a company's leadership and unit economics. This collection covers his approach to backing structural change, assessing management talent, and adapting to the changing mechanics of short selling.

Part 1: The Anatomy of Change

- On Structural Tailwinds: "We have invested pretty much forever behind change. That can mean a large technological shift or a managerial overhaul, but it must alter the business dynamic for a multi-year period." — Source: [Invest Like the Best: Episode 235]

- On the Velocity of Disruption: "The pace at which incumbents lose market share to insurgents has accelerated significantly. You can no longer rely on brand heritage to protect a declining business model." — Source: [Lone Pine Q4 2020 Letter]

- On Recognizing Inflection Points: "The best investments are found when a company is transitioning from a period of heavy capital expenditure into a phase of massive cash flow generation." — Source: [Yale School of Management Fireside Chat]

- On Technological Moats: "Technology is no longer a vertical; it is a horizontal layer that dictates the competitive position of every company in every industry." — Source: [Titan Series Interview]

- On Market Myopia: "Wall Street tends to price change linearly. When a structural shift occurs, the market often underestimates the duration and magnitude of the resulting growth." — Source: [The Joys of Compounding Podcast]

- On Adapting to New Eras: "You have to be willing to abandon the frameworks that made you successful ten years ago if the underlying rules of the industry have fundamentally shifted." — Source: [Invest Like the Best: Episode 235]

- On Regulatory Shifts: "A change in regulation can destroy a profitable business overnight or create a multi-billion dollar opportunity. It is one of the most under-analyzed areas of fundamental research." — Source: [Lone Pine Q1 2018 Letter]

- On Legacy Assets: "Physical assets that were once considered unassailable competitive advantages often become heavy liabilities during periods of rapid technological adoption." — Source: [Yale School of Management Fireside Chat]

- On the Durability of Growth: "Growth is only valuable if it expands the competitive moat. We look for companies where every incremental dollar of revenue makes the core product harder to replicate." — Source: [Titan Series Interview]

Part 2: Management and Human Capital

- On the Cost of Bad Leadership: "Nearly every major investment mistake I have made traces back to a misjudgment of the people running the business." — Source: [Yale School of Management Fireside Chat]

- On Assessing CEOs: "You do not learn about a CEO by listening to their earnings call. You learn about them by talking to the people who used to report to them." — Source: [Invest Like the Best: Episode 235]

- On Capital Allocation: "A management team's true skill is revealed in how they allocate free cash flow. It is the ultimate test of their strategic foresight." — Source: [Lone Pine Q2 2019 Letter]

- On Founder-Led Companies: "Founders who retain a significant stake tend to operate with a long-term horizon that hired executives struggle to replicate. They care about the legacy of the business rather than only the next quarter." — Source: [The Joys of Compounding Podcast]

- On Incentive Structures: "Show me how a management team is compensated, and I will tell you exactly what decisions they are going to make over the next three years." — Source: [Yale School of Management Fireside Chat]

- On Middle Management: "The strength of a company is often determined by the quality of its middle management. They are the translation layer between strategy and execution." — Source: [Titan Series Interview]

- On Hubris: "When a CEO starts talking more about their personal brand than their company’s unit economics, it is usually time to exit the stock." — Source: [Invest Like the Best: Episode 235]

- On Operational Excellence: "Great leaders are obsessed with the details. They know their supply chain constraints and customer acquisition costs off the top of their head." — Source: [Tiger Management Alumni Panel]

- On Board Composition: "A passive board of directors is a red flag. We want boards that actively challenge the CEO and hold them accountable for capital returns." — Source: [Lone Pine Q1 2021 Letter]

Part 3: The Retail Lens and Unit Economics

- On the Retail Foundation: "Starting as a retail analyst teaches you to focus on unit economics. If a single store does not make economic sense, scaling to a thousand stores will only multiply the losses." — Source: [Invest Like the Best: Episode 235]

- On Sam Walton's Playbook: "Walton understood that operational efficiency in the backend allowed for lower prices on the front end, creating a flywheel that competitors simply could not break." — Source: [The Joys of Compounding Podcast]

- On Inventory Turns: "Inventory is the silent killer of retail. Companies that can turn their inventory faster than their payables effectively fund their own growth." — Source: [Tiger Management Alumni Panel]

- On Customer Acquisition: "In both physical retail and software, the fundamental equation is the same: the lifetime value of a customer must drastically exceed the cost to acquire them." — Source: [Yale School of Management Fireside Chat]

- On Margin Expansion: "We prefer businesses with expanding gross margins. It usually indicates pricing power or a shift toward a more profitable product mix." — Source: [Lone Pine Q3 2017 Letter]

- On Format Obsolescence: "Retail formats have a natural lifecycle. You have to recognize when a previously dominant store format is losing its relevance to the marginal consumer." — Source: [Titan Series Interview]

- On E-commerce Penetration: "The shift to online commerce goes beyond convenience; it fundamentally rewrites the cost structure of distribution." — Source: [Invest Like the Best: Episode 235]

- On Pricing Power: "True pricing power means you can raise prices without losing unit volume. It is the rarest and most valuable attribute a business can possess." — Source: [The Joys of Compounding Podcast]

- On Omnichannel Reality: "The distinction between physical and digital retail is blending. The winners will be those who use their physical footprint to reduce digital fulfillment costs." — Source: [Lone Pine Q2 2020 Letter]

Part 4: The Evolution of Short Selling

- On the Difficulty of Shorting: "Generating alpha through short-selling is significantly harder today than it was twenty years ago. Information parity and the speed of capital flows have eroded the traditional short seller's edge." — Source: [Invest Like the Best: Episode 235]

- On Value Traps: "Shorting based purely on high valuation is a dangerous game. You must identify a catalyst like a deterioration in the underlying business fundamentals." — Source: [Tiger Management Alumni Panel]

- On Structural Losers: "The best shorts are companies structurally disadvantaged by technological change. Their decline is not cyclical; it is terminal." — Source: [Lone Pine Q1 2019 Letter]

- On the Cost of Borrowing: "The mechanics of shorting matter. If the cost to borrow a stock is exorbitant, the hurdle rate for the trade becomes insurmountable." — Source: [Yale School of Management Fireside Chat]

- On Squeeze Dynamics: "In the modern market, overcrowded shorts are weaponized by retail and institutional momentum. You have to be acutely aware of positioning." — Source: [Titan Series Interview]

- On Fraud vs. Obsolescence: "Shorting frauds can be profitable but unpredictable. Shorting obsolescence provides a smoother and more inevitable path to returns." — Source: [The Joys of Compounding Podcast]

- On Asymmetric Risk: "The math of shorting is inherently unfavorable. Your maximum upside is 100 percent, while your downside is theoretically infinite. Position sizing must reflect this asymmetry." — Source: [Invest Like the Best: Episode 235]

- On Management Denial: "When management blames the weather or macro factors for three consecutive quarters of missing numbers, it is often a signal of deeper operational rot." — Source: [Lone Pine Q4 2018 Letter]

- On Accounting Red Flags: "Aggressive revenue recognition and frequent one-time adjustments are classic indicators that the core business is struggling to generate real cash." — Source: [Tiger Management Alumni Panel]

- On the Role of Shorts: "Today, short positions often serve more as portfolio insurance to dampen volatility rather than independent profit centers." — Source: [Yale School of Management Fireside Chat]

Part 5: Deep Research and "Scuttlebutt"

- On Getting into the Guts: "You have to get into the guts of a business. Reading SEC filings is just the baseline; the real work begins when you start calling the supply chain." — Source: [Invest Like the Best: Episode 235]

- On Primary Research: "We do not rely on Wall Street research reports. We build our models from the ground up, verifying every assumption with industry participants." — Source: [Lone Pine Q1 2020 Letter]

- On Interviewing Competitors: "A company will rarely admit its weaknesses, but its fiercest competitors will eagerly point them out. You just have to reverse-engineer their bias." — Source: [The Joys of Compounding Podcast]

- On Former Employees: "Speaking with executives who left a company two years ago provides the most unvarnished view of internal culture and technical debt." — Source: [Yale School of Management Fireside Chat]

- On Alternative Data: "Data sets like credit card receipts and web traffic are useful, but they only tell you what happened. Fundamental qualitative research tells you why it happened." — Source: [Titan Series Interview]

- On Channel Checks: "If you want to know if a software product is good, talk to the IT procurement managers who are actually writing the checks." — Source: [Invest Like the Best: Episode 235]

- On Synthesizing Information: "The edge is no longer in acquiring information, but in filtering the noise and weighting the variables correctly." — Source: [Tiger Management Alumni Panel]

- On Intellectual Honesty: "When our thesis is proven wrong by facts on the ground, we change our minds immediately. Ego has no place in fundamental research." — Source: [Lone Pine Q2 2021 Letter]

- On Global Perspectives: "You cannot understand an internet marketplace in the US without studying how similar models evolved in China or Latin America." — Source: [The Joys of Compounding Podcast]

- On the Ground Game: "Julian Robertson taught us that there is no substitute for getting on a plane and visiting the physical operations of the businesses we own." — Source: [Tiger Management Alumni Panel]

Part 6: Technology and Internet Dominance

- On Network Effects: "Internet platforms benefit from a dynamic where the product improves automatically as more users join, creating a barrier to entry that capital alone cannot breach." — Source: [Yale School of Management Fireside Chat]

- On Software Economics: "The beauty of enterprise software is the near-zero marginal cost of distribution paired with high switching costs." — Source: [Lone Pine Q3 2019 Letter]

- On Platform Monopolies: "We look for companies that act as the digital toll roads for their respective industries. Once integrated, they are incredibly difficult to displace." — Source: [Titan Series Interview]

- On Cloud Computing: "The shift to the cloud fundamentally changed corporate IT spending from a lumpy capital expense to a predictable operating expense, improving earnings visibility." — Source: [Invest Like the Best: Episode 235]

- On Data as an Asset: "Companies that can successfully capture and utilize proprietary data possess a compounding advantage over time." — Source: [The Joys of Compounding Podcast]

- On Consumer Internet: "In consumer tech, engagement is the leading indicator of monetization. If people are spending hours on a platform daily, the revenue will follow." — Source: [Lone Pine Q4 2017 Letter]

- On Secular vs. Cyclical Tech: "You have to distinguish between tech companies riding a temporary hardware upgrade cycle and those benefiting from secular software adoption." — Source: [Tiger Management Alumni Panel]

- On Legacy Disruption: "Software goes beyond improving efficiency; it systematically dismantles the profit pools of legacy industries." — Source: [Yale School of Management Fireside Chat]

- On Global Scalability: "The best digital businesses are constrained only by language and local regulation, allowing them to scale globally with unprecedented speed." — Source: [Invest Like the Best: Episode 235]

Part 7: Culture and Talent at Lone Pine

- On Team Collaboration: "Investment management is not a solo sport. You need a team that can debate fiercely in the conference room but execute cohesively in the market." — Source: [The Joys of Compounding Podcast]

- On Hiring Analysts: "We do not hire people merely because they can build a complex spreadsheet. We hire people with an innate curiosity to figure out how things actually work." — Source: [Yale School of Management Fireside Chat]

- On Decentralized Decision-Making: "As a firm grows, the founder must transition from being the sole stock picker to a portfolio manager who allocates capital among talented sector specialists." — Source: [Invest Like the Best: Episode 235]

- On Retaining Talent: "The best way to keep great investors is to give them autonomy and clear economic alignment within a culture devoid of corporate politics." — Source: [Tiger Management Alumni Panel]

- On Learning from Mistakes: "Every mistake is subjected to a post-mortem. The goal is never to assign blame, but to update our mental models and prevent the same error from recurring." — Source: [Lone Pine Q1 2016 Letter]

- On Intellectual Diversity: "If everyone on your team has the exact same background and worldview, you will miss the blind spots in your thesis." — Source: [Titan Series Interview]

- On Succession Planning: "An enduring firm is one that can survive the departure of its founder. We have spent years building a multi-generational partnership." — Source: [Yale School of Management Fireside Chat]

- On Managing Size: "Asset growth is the enemy of performance. We have historically returned capital to partners to maintain the agility required to generate alpha." — Source: [Lone Pine Q4 2019 Letter]

- On Tiger Management's Legacy: "Julian taught us that you can be highly competitive in the markets while remaining deeply collaborative and collegial internally." — Source: [Tiger Management Alumni Panel]

Part 8: Long-Term Compounding and Patience

- On Time Horizon Arbitrage: "The market is obsessed with the next quarter's earnings beat. Our edge comes from underwriting what the business will look like in five years." — Source: [Invest Like the Best: Episode 235]

- On Letting Winners Run: "The biggest mistake investors make is selling a great company simply because the stock has doubled. If the fundamentals are compounding, stay out of the way." — Source: [The Joys of Compounding Podcast]

- On Volatility: "Volatility is not risk. A 20 percent drawdown in a fundamentally sound business is an opportunity to increase your position size." — Source: [Yale School of Management Fireside Chat]

- On Conviction: "High conviction is earned through exhausting research. When the market panics, only deep knowledge gives you the fortitude to hold." — Source: [Lone Pine Q2 2018 Letter]

- On Cash as an Option: "Holding cash is uncomfortable in a rising market, but it provides the essential liquidity needed to capitalize when fear causes asset mispricing." — Source: [Titan Series Interview]

- On the Law of Large Numbers: "Trees do not grow to the sky. You must realistically assess when a company's total addressable market limits its ability to compound at historic rates." — Source: [Invest Like the Best: Episode 235]

- On Over-Trading: "Action is often confused with progress in this industry. Sometimes the best investment decision you can make in a year is to do absolutely nothing." — Source: [Tiger Management Alumni Panel]

- On Macro Forecasting: "We spend very little time trying to predict interest rates or GDP growth. We focus entirely on the micro-economics of individual companies." — Source: [Lone Pine Q1 2017 Letter]

- On Enduring Value: "Great businesses create value for their customers first. If the customer is winning, the shareholder will eventually win." — Source: [The Joys of Compounding Podcast]

- On the Ultimate Goal: "We are not trying to be the smartest people in every trade; we are trying to find exceptional businesses and partner with great managers to let time do the heavy lifting." — Source: [Yale School of Management Fireside Chat]