Lessons from Steve Rattner

Steve Rattner is a financier and former journalist who led the Obama administration’s 2009 Auto Task Force. He frequently relies on televised charts to explain economic realities like inflation, wages, and corporate restructuring. This collection organizes his views on government intervention, consumer finances, and the broader U.S. economy.

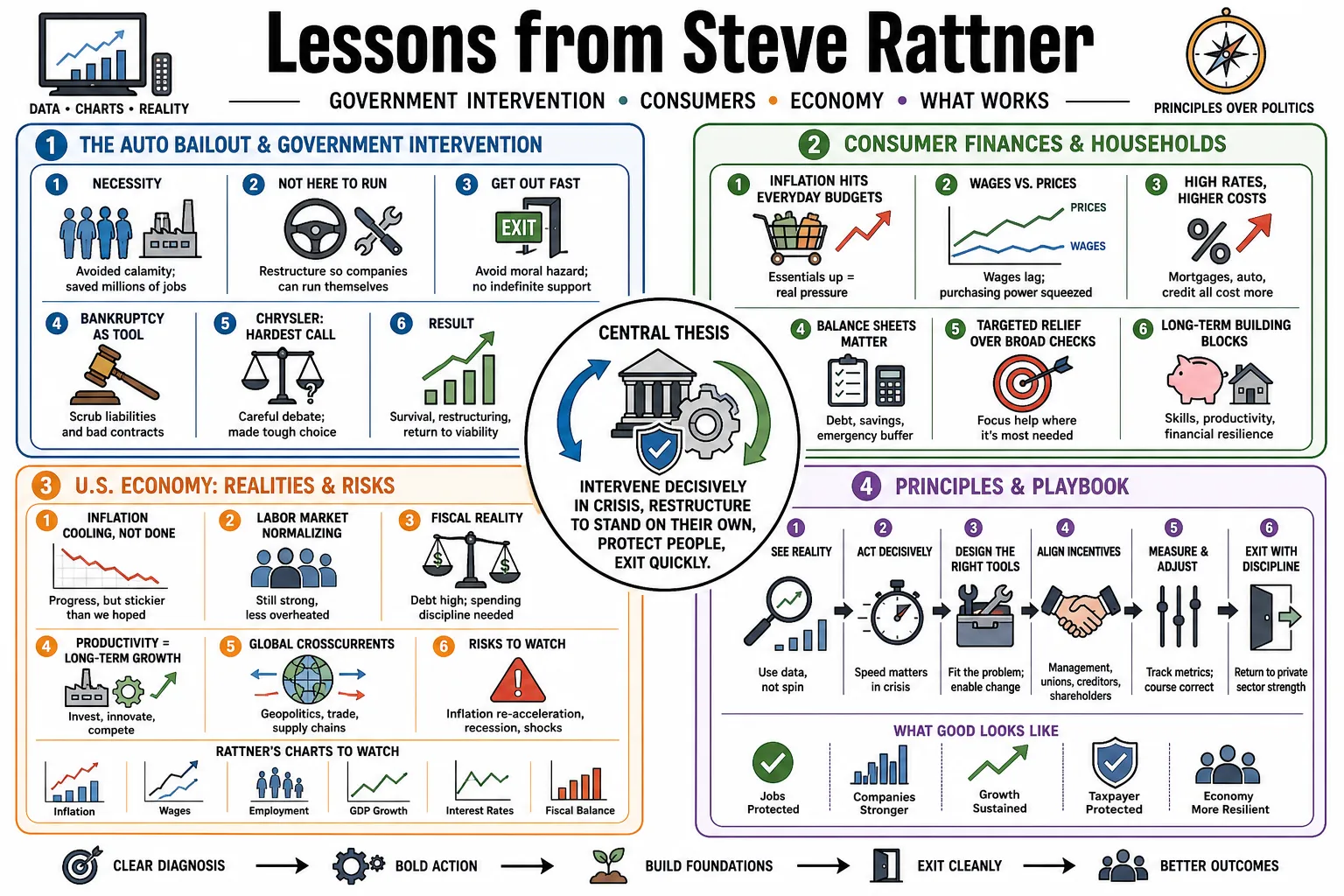

Part 1: The Auto Bailout and Government Intervention

- On the necessity of the auto bailout: "It would have been an economic calamity. You would have had a couple million people out of work. We just felt it was an unacceptable risk to take." — Source: [Stanford Business]

- On government intervention: "We were not there to run the auto companies, but to restructure them so they could run themselves." — Source: [Overhaul]

- On avoiding full nationalization: "The goal was always to get the government out of the auto business as quickly as practically possible, avoiding the moral hazard of indefinite state support." — Source: [The New York Times]

- On bankruptcy as a tool: "Bankruptcy was the only mechanism powerful enough to scrub away the accumulated liabilities and bad contracts that were dragging these companies under." — Source: [The Guardian]

- On evaluating Chrysler: "We seriously debated letting Chrysler fail. The math was terrible, and the standalone prospects were grim until the Fiat alliance materialized." — Source: [Overhaul]

- On shared sacrifice: "Saving the industry required everyone—unions, bondholders, management, and dealers—to take painful haircuts. Nobody got out whole." — Source: [NPR]

- On political pressure: "You have to insulate the financial and operational decisions from the political calendar, or the restructuring will fail." — Source: [Yale Program on Financial Stability]

- On the limits of federal rescues: "A bailout is a temporary bridge over a specific crisis, not a substitute for a viable long-term business model." — Source: [The New Republic]

- On accountability: "We demanded the resignation of the CEO of General Motors because the government cannot inject billions of taxpayer dollars without changing the leadership that required the bailout." — Source: [Overhaul]

- On the ultimate measure of success: "The true test was whether the companies survived 2009, and more importantly, whether they were structurally sound enough to weather the next inevitable recession." — Source: [StevenRattner.com]

Part 2: Corporate Restructuring and Culture

- On GM's pre-crisis culture: "The company needed a personality overhaul as much as it needed a financial one. They were disconnected from the reality of their declining market share." — Source: [Forbes]

- On corporate complacency: "General Motors was a classic case of a dominant corporation that became too slow, too bureaucratic, and too happy with itself." — Source: [The Guardian]

- On management depth: "You can change the CEO, but if the layers of management below are still operating under the old rules, the turnaround will stall." — Source: [Overhaul]

- On the cost of bureaucracy: "They had meetings to plan meetings. Speed of execution is a structural advantage that old industrial giants frequently lose." — Source: [StevenRattner.com]

- On pruning brands: "Creating a leaner organization meant killing off beloved but unprofitable brands like Pontiac and Saturn. Sentimentality has no place in a restructuring." — Source: [The New York Times]

- On labor relations: "A sustainable company requires a labor cost structure that is competitive with foreign transplants operating in the American South." — Source: [Overhaul]

- On board oversight: "Corporate boards often fail to ask the hard questions until the cash is nearly gone. Active governance requires challenging management's optimistic projections." — Source: [Yale Program on Financial Stability]

- On fixing operations: "Financial engineering buys you time, but operational excellence is what actually generates free cash flow." — Source: [Morning Joe]

- On taking the hard medicine: "Companies delay restructuring because it is painful, but waiting only increases the severity of the cuts required when the money finally runs out." — Source: [Overhaul]

Part 3: The Macroeconomy and the Consumer

- On the disconnect between data and sentiment: "Macroeconomic indicators look strong on paper, but the pocketbook reality for average Americans feels vastly different when they go to the grocery store." — Source: [Morning Joe]

- On household savings: "We are seeing a rapid depletion of the excess savings accumulated during the pandemic, returning many consumers to a paycheck-to-paycheck existence." — Source: [Steven Rattner's Substack]

- On consumer debt: "The rise in credit card balances and mortgage delinquencies among lower-income households is a clear signal of underlying financial stress." — Source: [The New York Times]

- On retirement security: "The increasing rate of hardship withdrawals from 401(k) accounts suggests families are sacrificing their future security to meet present living expenses." — Source: [Morning Joe]

- On the housing squeeze: "When housing and energy costs consume a disproportionate share of income, consumer spending on discretionary goods inevitably contracts." — Source: [StevenRattner.com]

- On the labor market: "A low unemployment rate is a positive headline, but the quality of the jobs and the wage growth attached to them dictate actual consumer health." — Source: [The New York Times]

- On economic resilience: "The American consumer has shown remarkable resilience, but that spending is increasingly debt-fueled rather than income-supported." — Source: [Morning Joe]

- On tracking the economy: "If you want to understand the economy, stop looking solely at GDP and start looking at real median household income." — Source: [Steven Rattner's Substack]

- On consumer expectations: "People benchmark their financial well-being not against historical data, but against their own recent past and expectations for the future." — Source: [Morning Joe]

- On economic data lags: "The numbers we debate on television are often a rearview mirror. The consumer is already reacting to conditions that won't show up in the data for months." — Source: [The New York Times]

Part 4: Income Inequality and the "K-Shaped" Economy

- On the K-shaped recovery: "We are experiencing a K-shaped economy where those at the top, buoyed by asset prices, pull away from those at the bottom who are struggling with basic costs." — Source: [Morning Joe]

- On the asset divide: "The stock market is not the economy. Nearly half of Americans own no stock at all, meaning they gain nothing from Wall Street's record highs." — Source: [Steven Rattner's Substack]

- On structural inequality: "Wage stagnation for the bottom half of earners is a multi-decade trend that cannot be fixed by short-term fiscal stimulus alone." — Source: [The New York Times]

- On the wealth gap: "When the Federal Reserve keeps interest rates near zero, it inflates the value of assets held by the wealthy while punishing the cash savings of the middle class." — Source: [StevenRattner.com]

- On educational attainment: "The clearest dividing line in the modern American economy is a college degree, which increasingly determines exposure to unemployment and wage growth." — Source: [Morning Joe]

- On corporate profits vs. wages: "Corporate margins have expanded significantly, often driven by tight expense management and productivity gains that are not proportionately shared with the workforce." — Source: [The New York Times]

- On regional disparity: "National economic averages mask deep geographic inequalities. The recovery in coastal tech hubs looks entirely different from the reality in the industrial Midwest." — Source: [Steven Rattner's Substack]

- On policy impacts: "Tax codes that heavily favor capital gains over ordinary income structurally reinforce wealth concentration at the very top." — Source: [The New York Times]

- On social mobility: "If the rungs on the economic ladder grow further apart, the traditional American promise of upward mobility becomes mathematically harder to achieve." — Source: [Morning Joe]

Part 5: Inflation, Wages, and Purchasing Power

- On the pain of inflation: "Inflation acts as a highly regressive tax, punishing lower-income households who spend the majority of their paychecks on non-discretionary items like food and gas." — Source: [Morning Joe]

- On real wages: "A five percent raise feels like a loss if inflation is running at seven percent. Workers correctly perceive that they are falling behind." — Source: [Steven Rattner's Substack]

- On the psychology of inflation: "Once inflation expectations become entrenched in the minds of consumers and businesses, it requires significant economic pain to root them out." — Source: [The New York Times]

- On the causes of price spikes: "You cannot inject trillions of dollars of fiscal stimulus into a supply-constrained economy without triggering a massive increase in the price level." — Source: [Morning Joe]

- On the Fed's response: "The Federal Reserve was late to recognize that inflation was not transitory, forcing them into a steeper and more aggressive tightening cycle." — Source: [The New York Times]

- On sticky prices: "Certain categories, like rent and services, are sticky. Once those prices go up, they rarely come back down, permanently altering the cost of living." — Source: [StevenRattner.com]

- On supply chain vulnerabilities: "The pandemic exposed the fragility of just-in-time inventory models, proving that efficiency without resilience carries a heavy inflationary cost." — Source: [Morning Joe]

- On the wage-price spiral: "Central bankers fear a scenario where higher prices demand higher wages, which in turn drive companies to raise prices further, creating a self-sustaining loop." — Source: [The New York Times]

- On historical context: "We spent decades worrying about deflation, which left policymakers ill-equipped and slow to react when traditional inflation returned with a vengeance." — Source: [Steven Rattner's Substack]

- On political fallout: "No incumbent government can easily survive an environment where the average voter is losing purchasing power month after month." — Source: [Morning Joe]

Part 6: Market Behavior and Investment Strategy

- On speculative investing: "For the average retail investor, trying to pick winners among young, speculative companies is pure folly. Buy a lottery ticket instead. Your chance of winning is likely to be higher." — Source: [StevenRattner.com]

- On market exuberance: "Periods of easy money consistently breed speculative bubbles, as investors chase yield in increasingly risky assets." — Source: [The New York Times]

- On the role of private equity: "Private equity can bring necessary discipline and capital to inefficient businesses, but the model breaks down when it relies entirely on excessive borrowing." — Source: [Overhaul]

- On passive investing: "The shift toward low-cost index funds is one of the most positive developments for average investors, mathematically outperforming active management over the long term." — Source: [Morning Joe]

- On assessing risk: "Investors frequently confuse a rising market with their own genius. True risk management is tested only when the tide goes out." — Source: [Steven Rattner's Substack]

- On market concentration: "When a handful of mega-cap technology stocks drive the vast majority of index gains, the broader market is more fragile than the headline numbers suggest." — Source: [Morning Joe]

- On corporate stock buybacks: "Buybacks are a legitimate way to return capital to shareholders, but they become problematic when funded by debt or prioritized over necessary capital expenditures." — Source: [The New York Times]

- On the Federal Reserve's influence: "Markets have become dangerously conditioned to expect a Fed rescue at the first sign of a sustained equity drawdown." — Source: [StevenRattner.com]

- On long-term horizons: "Wealth is generated by compounding over decades, not by trading around short-term macroeconomic news cycles." — Source: [Morning Joe]

Part 7: Fiscal Policy, Debt, and the Deficit

- On the national debt: "We are running peacetime deficits that rival those of major wars, creating a structural debt burden that will eventually crowd out other domestic priorities." — Source: [The New York Times]

- On political math: "Politicians of both parties prefer the easy math of cutting taxes or increasing spending, entirely ignoring the reality of the balance sheet." — Source: [Morning Joe]

- On interest expenses: "As interest rates normalize, the cost of simply servicing our national debt will become one of the largest line items in the federal budget." — Source: [Steven Rattner's Substack]

- On entitlement reform: "You cannot stabilize the long-term fiscal trajectory of the United States without addressing the math of Medicare and Social Security." — Source: [The New York Times]

- On the risk of fiscal dominance: "If federal borrowing becomes too large, it limits the Federal Reserve's ability to effectively manage interest rates without bankrupting the treasury." — Source: [StevenRattner.com]

- On targeted stimulus: "Government spending is most effective when it is highly targeted to those in need, rather than distributed broadly regardless of income." — Source: [Morning Joe]

- On infrastructure investment: "Borrowing to fund productive assets like infrastructure yields an economic return; borrowing to fund current consumption is simply passing the bill to our children." — Source: [The New York Times]

- On tax policy: "A competitive corporate tax rate is necessary for global competitiveness, but it must be paired with the elimination of loopholes that allow massive profitable entities to pay zero." — Source: [Morning Joe]

- On the illusion of free money: "The era of zero interest rates fostered a dangerous political illusion that deficits no longer matter." — Source: [Steven Rattner's Substack]

Part 8: Financial Literacy and Personal Finance

- On basic financial literacy: "A functioning capitalist system requires participants who understand the basic mechanics of compound interest, debt, and risk." — Source: [The New York Times]

- On emergency savings: "The inability of a large percentage of Americans to cover a $400 emergency expense is a systemic failure of both wages and financial planning." — Source: [Morning Joe]

- On credit card debt: "Revolving credit card debt at high interest rates is the single most destructive force in a household's financial life." — Source: [StevenRattner.com]

- On homeownership: "While housing is a primary engine for middle-class wealth creation, viewing a primary residence as a speculative investment often leads to too much debt." — Source: [The New York Times]

- On retirement planning: "The shift from defined-benefit pensions to 401(k)s transferred the entire burden of market risk and longevity risk onto the individual worker." — Source: [Steven Rattner's Substack]

- On behavioral finance: "Investors frequently let emotion drive their decisions, selling at the exact moment of maximum panic and buying at the peak of euphoria." — Source: [Morning Joe]

- On the cost of delay: "Because of the mathematics of compounding, a dollar saved in your twenties is worth vastly more than a dollar saved in your fifties." — Source: [The New York Times]

- On financial media: "Consumers must learn to distinguish between entertainment masquerading as financial advice and actual, prudent wealth management." — Source: [StevenRattner.com]

- On complexity: "The financial services industry often uses complexity to justify high fees. The most effective personal finance strategies are usually the simplest." — Source: [Morning Joe]