Lessons from Steven Galbraith

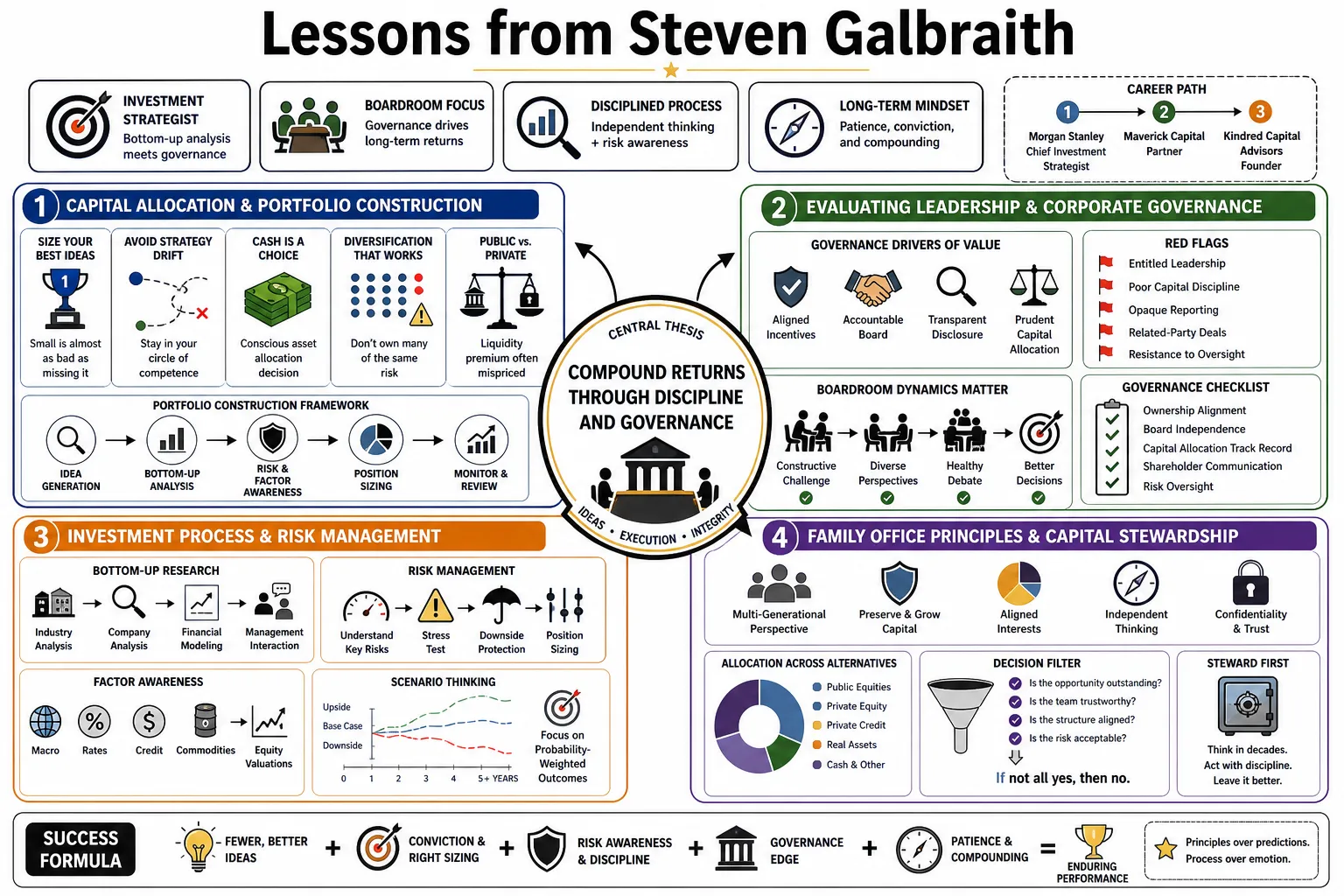

Steven Galbraith served as Morgan Stanley's Chief Investment Strategist and a partner at Maverick Capital before founding Kindred Capital Advisors. He pairs bottom-up security analysis with a strict focus on corporate governance, treating boardroom dynamics as a central driver of long-term returns. The insights below organize his methods for allocating capital, evaluating leadership, and managing family offices.

Part 1: Capital Allocation and Portfolio Construction

- On sizing positions: "You only get a few great ideas a year. If you find one, sizing it small is almost as bad a mistake as missing it entirely." — Source: [Capital Allocators: Five Tool Player]

- On strategy drift: "Portfolios break down when managers start buying companies outside their core competency just to stay fully invested." — Source: [Columbia Business School Lectures]

- On cash balances: "Holding cash is a conscious asset allocation decision, not just the absence of an idea." — Source: [Morgan Stanley Investment Research]

- On diversification: "Owning fifty stocks doesn't protect you if forty of them are exposed to the same underlying economic factor." — Source: [Capital Allocators: Five Tool Player]

- On public vs. private markets: "The liquidity premium in public markets is often mispriced. You pay for the privilege of selling quickly, but most institutions don't need that feature." — Source: [Capital Allocators: In the Boardroom]

- On benchmarking: "Obsessing over quarterly tracking error forces you into average decisions. You have to be willing to look wrong for a year to be right over five." — Source: [Morgan Stanley Investment Research]

- On market timing: "You cannot predict macro turns with enough consistency to build a business on it. Stick to valuing individual assets." — Source: [Columbia Business School Lectures]

- On concentration: "A concentrated book forces a higher threshold for entry. Every new position has to actively fight for its spot." — Source: [Capital Allocators: Five Tool Player]

- On thematic investing: "Themes are useful for screening, but you still have to buy the specific cash flows of a specific business." — Source: [Morgan Stanley Investment Research]

- On rebalancing: "Trimming a winner is mentally difficult but mechanically necessary. You are managing risk, not rewarding past performance." — Source: [Institutional Investor Research Polls]

Part 2: Board Governance and Corporate Oversight

- On board composition: "A board full of former CEOs often struggles because everyone is used to running the show, rather than overseeing the person running it." — Source: [Capital Allocators: In the Boardroom]

- On asking questions: "The best board members ask simple, basic questions. Complexity is often used by management to hide poor execution." — Source: [Cumulus Media Governance Filings]

- On CEO compensation: "Incentives drive behavior. If you pay a management team solely on revenue growth, do not be surprised when margins compress." — Source: [Capital Allocators: In the Boardroom]

- On the role of a director: "Your job is not to manage the company. Your job is to hire, fire, and compensate the CEO, and approve the capital budget." — Source: [Cumulus Media Governance Filings]

- On capital allocation at the board level: "Most CEOs grew up in operations or marketing. They often need the board's help with capital allocation, which is an entirely different skill." — Source: [Capital Allocators: In the Boardroom]

- On independent directors: "Independence is a mindset, not a regulatory checkbox. You need people willing to tell a successful founder they are wrong." — Source: [Third Way Board Perspectives]

- On bad news: "A healthy board gets bad news quickly. If you are only hearing about problems after they hit the income statement, the culture is broken." — Source: [Success Academy Trust Meetings]

- On board materials: "If a management presentation is a hundred pages long, they are either disorganized or intentionally obscuring the main issue." — Source: [Capital Allocators: In the Boardroom]

- On term limits: "Stale boards become clubs. You need regular turnover to bring in fresh technical expertise as the business evolves." — Source: [Cumulus Media Governance Filings]

Part 3: Security Analysis and Valuation

- On defining quality: "Quality is a measure of how much capital a business requires to maintain its current earning power." — Source: [Columbia Business School Lectures]

- On valuation models: "A discounted cash flow model is only as useful as the conservatism of your terminal value assumptions." — Source: [Morgan Stanley Investment Research]

- On competitive advantage: "High returns on capital attract competition. You have to identify the specific mechanism that prevents rivals from entering the market." — Source: [Columbia Business School Lectures]

- On accounting adjustments: "Always look at the gap between GAAP earnings and management's adjusted numbers. When that gap widens consistently, be careful." — Source: [Morgan Stanley Investment Research]

- On debt: "Leverage does not create value. It only amplifies the underlying economics of the business while shortening your runway for mistakes." — Source: [Columbia Business School Lectures]

- On cyclical companies: "Buying a cyclical stock when the P/E ratio looks cheap is usually a trap. You buy them when earnings are depressed and the multiple looks high." — Source: [Morgan Stanley Investment Research]

- On unit economics: "If a business loses money on every customer, scaling up will not save it. Volume does not fix a fundamentally broken unit model." — Source: [Columbia Business School Lectures]

- On management calls: "Pay attention to what management chooses not to discuss on earnings calls. Omissions are louder than the prepared remarks." — Source: [Morgan Stanley Investment Research]

- On price targets: "Price targets are artificial constraints. If the thesis is intact and the business is growing intrinsic value, let it run." — Source: [Columbia Business School Lectures]

- On margin expansion: "It is much harder to expand profit margins than to grow the top line. Never model margin expansion unless you can point to a specific operational change." — Source: [Morgan Stanley Investment Research]

Part 4: Managing Institutional Capital and Endowments

- On investment committees: "Committees excel at finding flaws, which means they often reject the best, most unconventional ideas." — Source: [Capital Allocators: In the Boardroom]

- On manager selection: "You are hiring a person, not a track record. Past performance is just the byproduct of a process you need to understand." — Source: [Capital Allocators: Five Tool Player]

- On liquidity needs: "Endowments often overpay for liquidity they do not need. If your spending rate is five percent, you do not need half the portfolio available tomorrow." — Source: [Success Academy Trust Meetings]

- On alignment of interest: "Only invest with managers who have a meaningful portion of their own liquid net worth in the same strategy." — Source: [Capital Allocators: In the Boardroom]

- On fee structures: "A high management fee removes the manager's incentive to take risk. You want them hungry for the performance fee." — Source: [Third Way Board Perspectives]

- On firing managers: "Fire a manager for changing their process, not for a period of underperformance. If they stick to the process, the cycle will eventually turn." — Source: [Capital Allocators: Five Tool Player]

- On asset class silos: "Organizing a team by asset class creates artificial barriers. Capital should flow to the best absolute risk-adjusted return, regardless of the bucket." — Source: [Institutional Investor Research Polls]

- On illiquidity premiums: "Locking up capital for ten years in a private fund requires a massive premium over public equities. Many institutions accept too little for this trade-off." — Source: [Capital Allocators: In the Boardroom]

- On operational due diligence: "A brilliant investor with a messy back office is a disaster waiting to happen. The operations team must have veto power." — Source: [Capital Allocators: Five Tool Player]

Part 5: Risk Management in Volatile Markets

- On defining risk: "Risk is not volatility. Risk is the permanent impairment of capital." — Source: [Columbia Business School Lectures]

- On stop losses: "Mechanical stop losses force you to sell when an asset is cheapest. Your thesis should dictate the exit, not the stock price." — Source: [Morgan Stanley Investment Research]

- On hedging: "A bad hedge is worse than no hedge at all. It costs money and provides a false sense of security." — Source: [Capital Allocators: Five Tool Player]

- On value traps: "A stock is not a value play just because it is down fifty percent. Some businesses deserve to go to zero." — Source: [Columbia Business School Lectures]

- On leverage in crises: "When markets dislocate, the people with leverage are forced to sell to the people with cash. You always want to be the one with cash." — Source: [Morgan Stanley Investment Research]

- On correlation: "In a true panic, all asset classes correlate to one. Diversification fails exactly when you need it most." — Source: [Capital Allocators: Five Tool Player]

- On position limits: "No single idea should be capable of ruining the year. Set hard limits on exposure, no matter how high your conviction." — Source: [Columbia Business School Lectures]

- On macro risks: "You cannot manage every geopolitical risk. Instead, build a portfolio of companies resilient enough to survive external shocks." — Source: [Morgan Stanley Investment Research]

- On short selling: "Shorting is not just the opposite of going long. Your risk is infinite, and you pay to wait. It requires a completely different temperament." — Source: [Capital Allocators: Five Tool Player]

- On liquidity crunches: "The time to secure a credit line or build a cash buffer is when credit is cheap and easy, not when the market is freezing up." — Source: [Morgan Stanley Investment Research]

Part 6: Leadership and the Role of the CIO

- On building a team: "Hire analysts who naturally disagree with each other. A consensus-driven research team produces average results." — Source: [Capital Allocators: Five Tool Player]

- On decision making: "The CIO's job is to make the final call when the data is ambiguous. If the data were clear, a computer could do the job." — Source: [Institutional Investor Research Polls]

- On culture: "An investment culture is defined by how you treat the analyst who pitches a stock that goes down. If you punish them, you will never get another original idea." — Source: [Capital Allocators: Five Tool Player]

- On time management: "A CIO should spend most of their time reading and thinking, not in internal meetings." — Source: [Morgan Stanley Investment Research]

- On admitting mistakes: "The faster you admit you were wrong about a thesis, the less money you will lose. Ego is the most expensive trait in finance." — Source: [Columbia Business School Lectures]

- On mentoring: "You teach security analysis by tearing down a model line by line with the analyst. It is an apprenticeship." — Source: [Columbia Business School Lectures]

- On taking blame: "When the portfolio does well, credit the team. When it performs poorly, the CIO takes the blame." — Source: [Capital Allocators: Five Tool Player]

- On external communication: "Your limited partners need to hear from you most when performance is bad. Silence during a drawdown destroys trust." — Source: [Capital Allocators: In the Boardroom]

- On intellectual honesty: "You have to be willing to kill your own favorite idea if new facts disprove the original thesis." — Source: [Morgan Stanley Investment Research]

Part 7: Behavioral Tendencies in Investing

- On overconfidence: "A streak of winning trades usually means you are taking on hidden risks, not that you have suddenly become a genius." — Source: [Columbia Business School Lectures]

- On confirmation bias: "Once you buy a stock, your brain actively ignores negative news about the company. You have to force yourself to read the bear case." — Source: [Morgan Stanley Investment Research]

- On anchoring: "Investors anchor to the price they paid. The market does not know or care what your cost basis is." — Source: [Columbia Business School Lectures]

- On action bias: "Sitting still feels like you are not working. But most of the time, doing nothing is the most profitable decision." — Source: [Capital Allocators: Five Tool Player]

- On herd mentality: "It is professionally safer to lose money doing what everyone else is doing than to lose money standing alone." — Source: [Morgan Stanley Investment Research]

- On loss aversion: "People will hold onto a losing position for years just to avoid realizing the loss on paper." — Source: [Columbia Business School Lectures]

- On narrative appeal: "A great story often masks a terrible balance sheet. You have to separate the management's vision from the actual math." — Source: [Morgan Stanley Investment Research]

- On fatigue: "Decision fatigue is real. If you try to analyze twenty companies a day, the quality of your judgment collapses by the afternoon." — Source: [Capital Allocators: Five Tool Player]

- On emotional detachment: "You cannot fall in love with a stock. It is just a piece of paper attached to cash flows." — Source: [Columbia Business School Lectures]

Part 8: The Hedge Fund Business Model

- On asset gathering: "The goal of a fund should be to generate returns, not just accumulate assets. Size is the enemy of performance." — Source: [Capital Allocators: Five Tool Player]

- On founder succession: "Most hedge funds are tied to a single founder's brain. Transitioning that leadership to a second generation is historically very rare." — Source: [Capital Allocators: In the Boardroom]

- On prime brokers: "Your prime broker is a partner in normal times and a counterparty in a crisis. Understand the difference." — Source: [Capital Allocators: Five Tool Player]

- On transparent reporting: "Institutions will accept volatility, but they will not accept surprises. Be completely transparent about how you generate returns." — Source: [Third Way Board Perspectives]

- On the pressure to perform: "Monthly reporting creates a toxic incentive to smooth returns, which usually involves taking on tail risk." — Source: [Institutional Investor Research Polls]

- On team compensation: "If you pay analysts purely on the performance of their own ideas, you destroy any incentive for them to collaborate." — Source: [Capital Allocators: Five Tool Player]

- On closing to new capital: "The hardest decision a manager makes is turning away money. But it is the only way to protect the returns of existing clients." — Source: [Capital Allocators: In the Boardroom]

- On institutionalization: "A fund goes from a scrappy partnership to a corporate bureaucracy very quickly. You have to actively fight that drift." — Source: [Capital Allocators: Five Tool Player]

- On long-term survival: "The funds that survive decades are not the ones with the highest single-year returns. They are the ones that never take a fatal loss." — Source: [Morgan Stanley Investment Research]