Thomas Russo is a managing member of Gardner Russo & Quinn, best known for his long-term investments in global consumer brands and family-controlled businesses. He popularized the concept of the "capacity to suffer," arguing that management must be willing to endure short-term earnings pressure to make investments that secure long-term advantages. This collection organizes his core ideas on capital allocation, delayed gratification, and the mechanics of compounding wealth.

Part 1: The Capacity to Suffer

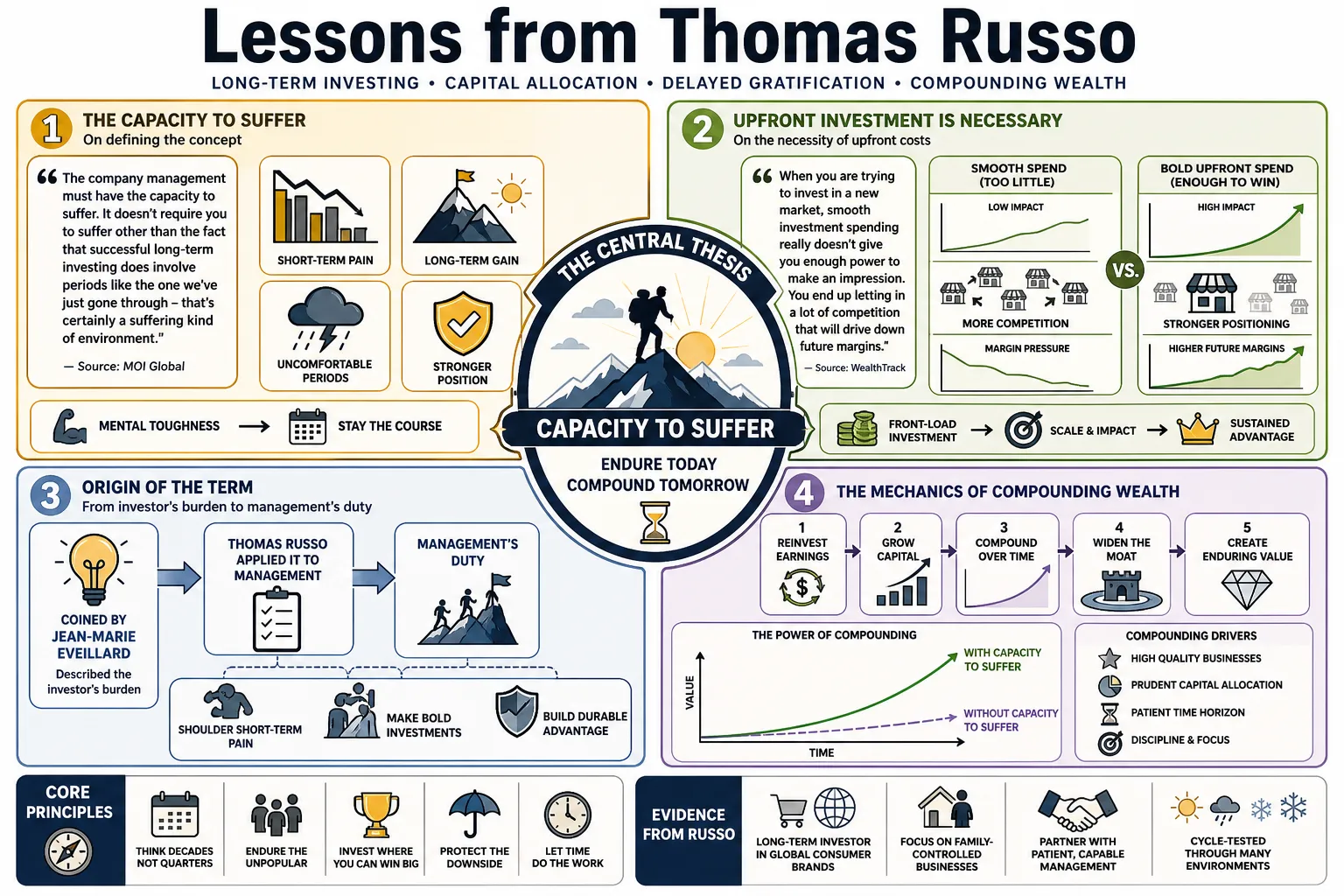

- On defining the concept: "The company management must have the capacity to suffer. It doesn't require you to suffer other than the fact that successful long-term investing does involve periods like the one we've just gone through – that's certainly a suffering kind of environment." — Source: MOI Global

- On the necessity of upfront costs: "When you are trying to invest in a new market, smooth investment spending really doesn't give you enough power to make an impression. You end up letting in a lot of competition that will drive down future margins." — Source: WealthTrack

- On the origin of the term: Jean-Marie Eveillard originally coined the phrase to describe the investor's burden, but Russo adapted it to describe the burden placed on corporate management teams willing to sacrifice present earnings for future dominance. — Source: The Investor's Podcast

- On Wall Street's impatience: Morningstar's recap of Russo's framework says the companies he admires must be willing to absorb short-term earnings pressure when they invest in new geographies or adjacent growth, even if activist-minded shareholders would rather protect current reported profits. — Reference: Morningstar recap on Russo backing companies that keep spending through short-term earnings pressure and activist pushback

- On the investor's burden: A portfolio manager needs an investor base that is stable and long-term oriented, so that the manager is not forced to sell great assets simply because clients panic during a market downturn. — Source: Ivey Business School

- On delayed gratification: The capacity to suffer is fundamentally about the willingness to accept current discomfort—whether in the form of depressed stock prices or lower quarterly earnings—for a much larger, more enduring reward later. — Source: Safal Niveshak

- On avoiding smooth earnings: Management teams that attempt to deliver perfectly smooth, predictable quarterly earnings often do so by underinvesting in their own businesses, leaving the door open for competitors. — Source: MOI Global

- On geographic expansion: Morningstar summarizes Russo's point that expansion into new countries usually comes with upfront losses and delayed payback, which is why he prizes businesses willing to keep funding those efforts long before the returns become obvious. — Reference: Morningstar recap on geographic expansion creating upfront losses before long-term returns show up

- On product innovation: True innovation requires a tolerance for failure and sunk costs. A company obsessed with next quarter's consensus estimate will rarely fund a project that might take a decade to pay off. — Source: Columbia Business School

- On filtering out noise: Management needs the psychological fortitude to ignore the constant barrage of criticism from analysts when their long-term investments temporarily depress return on equity. — Source: WealthTrack

Part 2: Family-Controlled Businesses

- On portfolio allocation: "Sixty-plus percent of my investments at the moment and most of the past decades have been invested in family-controlled companies, which is quite unusual." — Source: Masters in Invest

- On perceived risk: Family-controlled companies often trade at a discount because traditional investors view family control as a governance risk, whereas Russo views it as a structural advantage that protects long-term planning. — Source: GuruFocus

- On shielding from activists: A strong family voting bloc provides an impenetrable shield against activist hedge funds that might otherwise force a company to slash research and development to boost short-term margins. — Source: Hedge Fund Alpha

- On long-term orientation: Professional CEOs often manage for the duration of their option vesting schedules (three to five years), while family founders manage for the duration of their grandchildren's lifetimes. — Source: Ivey Business School

- On enduring market criticism: Because family owners cannot be easily fired by Wall Street, they possess the structural security required to exercise the "capacity to suffer." — Source: MOI Global

- On culture and retention: Family-run businesses often foster deeper loyalty among employees, as the corporate culture is tied to a human legacy rather than a faceless corporate entity. — Source: The Investor's Podcast

- On capital discipline: The Ivey notes emphasize Russo's preference for family-controlled companies because founding families still retain control and significant investment exposure, which he sees as a better setup for disciplined reinvestment and lower agency costs than purely short-term financial engineering. — Reference: Ivey notes on family control, significant investment exposure, and lower agency costs

- On generational transitions: The biggest risk in a family business is the transition of power. Russo looks for families that are willing to hire outside professional management when the gene pool falls short. — Source: WealthTrack

- On alignment of interests: When the controlling family eats their own cooking, minority shareholders can ride their coattails, provided the governance structure prevents the family from self-dealing. — Source: GuruFocus

- On the willingness to absorb pain: Family-controlled boards are far more likely to approve a decade-long expansion plan into a new continent, even if it halves profits in the interim. — Source: Latticework

Part 3: Global Brands and Consumer Goods

- On pricing power: In the MOI Global transcript, Russo says he looks for indispensable products with price-inelastic demand, because the real test of brand strength is being able to raise prices without losing volume when inflation or input costs move against you. — Reference: MOI Global transcript on indispensable products, price-inelastic demand, and raising prices without losing volume

- On emerging market consumers: As disposable incomes rise in developing nations, consumers predictably trade up from unbranded, local commodities to aspirational, globally recognized brands. — Source: WealthTrack

- On the role of advertising: Advertising is not an expense but a capital investment in "share of mind." Brands that consistently outspend their peers on marketing build moats that are incredibly expensive for new entrants to cross. — Source: Ivey Business School

- On local tastes vs global scale: The best consumer companies operate with a "glocal" mindset—they leverage global supply chains and capital, but tailor their flavor profiles and marketing entirely to local customs. — Source: The Investor's Podcast

- On the predictability of consumer habits: People rarely change their toothpaste, beer, or chocolate preferences once established. This behavioral inertia generates highly predictable, recurring cash flows. — Source: Columbia Business School

- On barrier to entry: It is relatively cheap to manufacture a beverage, but it costs billions of dollars and decades of time to build the distribution network and consumer trust required to displace an incumbent like Nestlé. — Source: MOI Global

- On long-term holdings: Russo initiated positions in Nestlé and Heineken in the late 1980s and has held them for decades, allowing the compounding of their global growth to drive portfolio returns. — Source: Hedge Fund Alpha

- On brand loyalty: Morningstar recounts Russo's Jack Daniel's-versus-Jim Beam example to show what he means by brand power: loyal customers often care more about getting the brand they trust than about saving a small amount on a substitute. — Reference: Morningstar recap of Russo's Jack Daniel's example for brand loyalty and pricing power

- On the resilience of food and beverage: During economic downturns, consumers may delay purchasing a new car or home, but they rarely trade down on small, daily luxuries like premium coffee or spirits. — Source: WealthTrack

- On the volume illusion: True growth in consumer goods comes from unit volume increases driven by population growth and expanding middle classes, rather than relying solely on price hikes. — Source: Ivey Business School

Part 4: Capital Allocation and Reinvestment

- On management's primary job: "As an investor in businesses, which generate enormous cash flows, my single most important issue to get right is what management will do with cash flow through reinvestment." — Source: Novel Investor

- On reinvestment runways: Generating free cash flow is useless if a company has nowhere to put it. The ideal business possesses both a high return on invested capital and an endless runway to deploy more capital at those same rates. — Source: Value Research

- On returning capital too early: Companies that aggressively pay dividends or buy back stock when they still have high-return internal projects available are fundamentally misallocating capital and destroying long-term value. — Source: DCF Modeling

- On the friction of taxes: In the MOI Global talk, Russo says one of the biggest advantages of long holding periods is deferring taxes while companies redeploy cash internally, letting intrinsic value compound without the repeated drag that comes from realizing gains too early. — Reference: MOI Global transcript on tax deferral and internal redeployment of cash through long holding periods

- On owner-oriented management: "Do they care about the owner, or do they care about themselves?" The answer dictates whether excess cash will be used to build a durable moat or to fund an empire-building acquisition. — Source: Novel Investor

- On the lack of training: Most CEOs reach the top by being excellent operators or salespeople, yet once they become CEO, their primary job shifts to capital allocation—a skill they have rarely practiced. — Source: Ivey Business School

- On buying back shares: Share repurchases only create value if the stock is trading at a material discount to its intrinsic value. Buying back overvalued stock destroys shareholder wealth. — Source: Columbia Business School

- On organic growth vs acquisitions: Organic reinvestment into existing brands usually yields far higher returns and carries significantly lower integration risk than acquiring competitors at a premium. — Source: The Investor's Podcast

- On disciplined expansion: Reinvesting in adjacent product lines or new geographies makes sense only when the company can leverage its existing distribution advantages. — Source: WealthTrack

- On the danger of cash: A business that generates massive cash but lacks a reinvestment runway often attracts activist investors or tempts management into foolish, unrelated acquisitions. — Source: MOI Global

Part 5: Long-Term Holding and Compounding

- On the farmer vs hunter mentality: "I consider myself to be a farmer—not a hunter. And I think most people on Wall Street are hunters. They like to fell big beasts and I'm very comfortable planting a few rows and just tending to them carefully." — Source: Hedge Fund Alpha

- On letting winners run: The biggest mistake investors make is cutting their flowers and watering their weeds. A true compounder should be held for decades, not traded for a quick 20% gain. — Source: Ivey Business School

- On doing nothing: The MOI Global transcript shows how Russo operationalizes patience: with average turnover around 5.5% and holdings like Nestlé, Heineken, and Berkshire kept for decades, his default is to stay the course when the reinvestment case still holds rather than manufacture activity. — Reference: MOI Global transcript on 5.5% turnover and decades-long holdings as evidence of disciplined inaction

- On the friction costs of trading: Frequent trading enriches brokers and the government at the expense of the investor. Minimizing turnover is essential to maximizing long-term compound annual growth rates. — Source: Value Investing World

- On tax-deferred compounding: By rarely selling, investors allow their capital to compound continuously without the interruption of capital gains taxes, creating a massive mathematical advantage over time. — Source: WealthTrack

- On time horizons: While the market obsesses over the next quarter, extending your time horizon to ten or twenty years eliminates 90% of your competition. — Source: The Investor's Podcast

- On the rarity of great ideas: You only need a few exceptional businesses in a lifetime to build substantial wealth. Over-diversification often dilutes the impact of your best insights. — Source: Columbia Business School

- On surviving technological shifts: "With every company I own there is always the question of sustainability, that a transformation in its industry will leave it behind. I believe pronouncements of a new era will prove to be as misplaced going forward as they have been in the past." — Source: Novel Investor

- On the math of holding: If you buy a stock at $10 and it goes to $100, you make 10x your money. If it goes to zero, you only lose 1x. The math heavily favors holding on to exceptional winners. — Source: MOI Global

Part 6: Agency Costs and Wall Street Culture

- On the misalignment of incentives: When management's compensation is heavily tied to short-term stock performance, they will predictably underinvest in the future to prop up today's share price. — Source: Ivey Business School

- On stock options: Nasdaq's recap of Russo's Google talk says he favors European companies partly because managers there are more often paid in cash than in time-sensitive stock options, which he sees as a healthier incentive structure for long-term decision-making. — Reference: Nasdaq recap of the Google talk on cash compensation versus time-sensitive stock options

- On the pressure for quarterly guidance: Providing quarterly earnings guidance traps a company in a destructive cycle, forcing them to make operational decisions based on Wall Street's calendar rather than the business's natural cycle. — Source: WealthTrack

- On management treating the company like an ATM: Russo heavily scrutinizes proxy statements to ensure executives aren't extracting excessive salaries, perks, and bonuses at the expense of the owners. — Source: Columbia Business School

- On the advantage of ignoring the crowd: Wall Street is structurally designed to generate activity and fees. Investors who refuse to participate in the frenzy retain a massive behavioral advantage. — Source: The Investor's Podcast

- On the institutional imperative: Managers often blindly copy the actions of their peers—whether it's expanding into a new sector or adopting a new accounting method—simply to avoid looking foolish on their own. — Source: MOI Global

- On the danger of smooth earnings: Companies that perfectly hit consensus estimates penny-for-penny quarter after quarter are often manipulating accruals, deferring maintenance, or cutting marketing budgets to engineer the result. — Source: GuruFocus

- On the benefit of an aligned shareholder base: A company can only execute a long-term vision if it cultivates a shareholder base that understands and supports that vision. The company gets the shareholders it deserves. — Source: Ivey Business School

- On Wall Street's blind spot: The obsession with liquid, widely-traded names often causes the market to completely misprice the stability and compounding power of tightly-held, illiquid family businesses. — Source: Latticework

Part 7: Mentorship and Influences

- On learning from Warren Buffett: Russo frequently credits his early exposure to Buffett for shifting his focus away from cheap, low-quality businesses toward high-quality compounders with durable competitive advantages. — Source: Columbia Business School

- On Bill Ruane's influence: Working at the Sequoia Fund under Bill Ruane taught Russo the importance of concentrated portfolios and the conviction required to hold a few great ideas through market volatility. — Source: The Investor's Podcast

- On Charlie Munger's emphasis on quality: In the MOI Global transcript, Russo traces his framework to Buffett's move away from cigar-butt investing toward franchise businesses with goodwill, pricing power, and reinvestment capacity, underscoring why business quality matters more than buying the cheapest asset on the board. — Reference: MOI Global transcript on Buffett's migration from cigar-butt investing toward franchise businesses with pricing power

- On the 1984 Columbia Business School seminar: Listening to Buffett speak at Columbia was a defining moment for Russo, crystallizing the idea that investing is about buying pieces of businesses, not trading pieces of paper. — Source: WealthTrack

- On Jean-Marie Eveillard: Eveillard provided the exact phrasing for the "capacity to suffer," giving Russo a concrete vocabulary to describe the tension between long-term investment and short-term market expectations. — Source: MOI Global

- On the transition from cigar-butt investing: Early value investors often hunted for statistical bargains that required an immediate catalyst. Russo learned from his mentors that time is the friend of the wonderful business and the enemy of the mediocre. — Source: Ivey Business School

- On evaluating management character: A recurring lesson from Omaha is that you cannot make a good deal with a bad person. Assessing the integrity of the people running the business is just as important as reading the balance sheet. — Source: The Investor's Podcast

- On the simplicity of the approach: The best mentors in value investing don't rely on complex algorithms; they rely on basic arithmetic, historical context, and an understanding of human nature. — Source: Latticework

- On inheriting a philosophy of patience: The collective wisdom of his mentors reinforced that successful investing requires a temperament suited for waiting, watching, and doing absolutely nothing for long stretches of time. — Source: Columbia Business School

Part 8: Psychological Discipline and Market Volatility

- On resilience: "The greatest lessons are learned when trying to work yourself out of something that doesn't go well. And the worst thing to do is to avoid those from happening when they naturally would." — Source: Business Insider

- On developing judgment: Older investors "develop judgment, and you're a little less impetuous, and a little more patient, and probably a little bit more asleep." — Source: Business Insider

- On enduring underperformance: Morningstar notes that Russo stayed with holdings like Nestlé, Heineken, and Unilever through the deeply out-of-favor 1999-2000 period, using that stretch as evidence that sound long-term strategies can look wrong for a while before the compounding shows up again. — Reference: Morningstar recap on Russo enduring the 1999-2000 stretch when his style was badly out of favor

- On the necessity of independent thinking: You cannot achieve superior results if you construct a portfolio that perfectly mirrors the index. You must be willing to be wrong and alone for a period of time. — Source: Ivey Business School

- On learning from mistakes: The most expensive errors are usually errors of omission—failing to buy enough of a great business when the opportunity presents itself, rather than buying a stock that declines in value. — Source: WealthTrack

- On resisting the urge to act: The market bombards investors with stimuli designed to provoke a reaction. The strongest psychological defense is to deliberately disconnect from the daily ticker. — Source: The Investor's Podcast

- On the comfort of concentration: When you only own a dozen businesses, you can know them intimately. That depth of knowledge provides the psychological armor required to hold through terrifying market drawdowns. — Source: Columbia Business School

- On the ultimate goal: The objective is not to beat the market every quarter, but to compound capital at a high rate over a lifetime without exposing the portfolio to the risk of permanent loss. — Source: MOI Global