Lessons from Torsten Slok

Torsten Slok is the Chief Economist at Apollo Global Management, where he publishes daily macroeconomic charts tracking everything from AI capital expenditure to consumer credit. The former Deutsche Bank economist regularly challenges consensus views on inflation, labor markets, and interest rates. This profile breaks down his core arguments on the direction of the global economy.

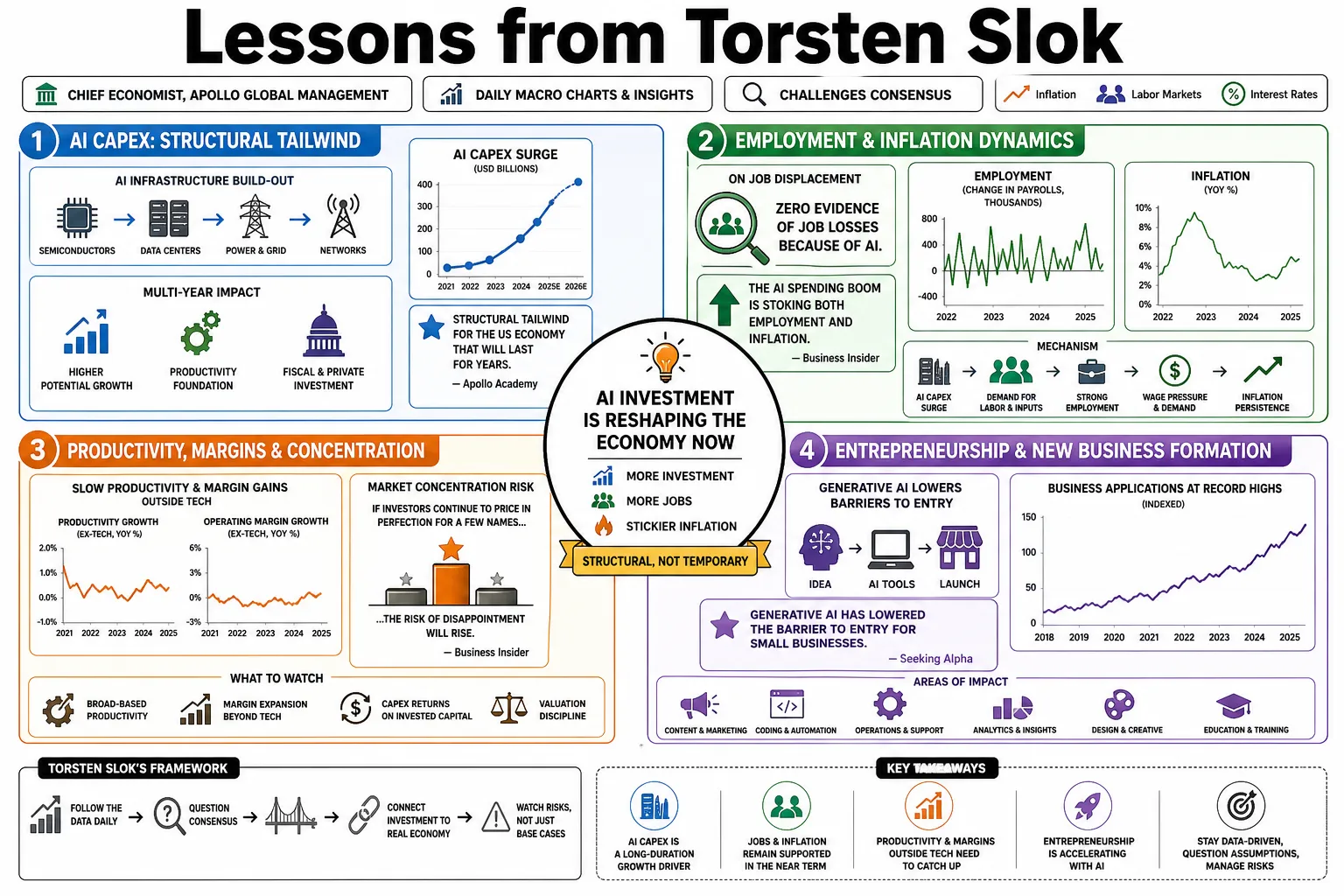

Part 1: Artificial Intelligence and Productivity

- On job displacement: "There is zero evidence of job losses because of AI. The AI spending boom is stoking both employment and inflation." — Source: Business Insider

- On AI capex: "The massive infrastructure build-out required for AI represents a structural tailwind for the US economy that will last for years." — Source: Apollo Academy

- On tech margins: "While AI spending remains high, productivity gains and margin growth outside of the technology sector have been slow to materialize." — Source: Business Insider

- On entrepreneurship: "Generative AI has lowered the barrier to entry for small businesses, contributing to record-high business applications." — Source: Seeking Alpha

- On market concentration: "If investors continue to price in instant earnings growth while the productivity hockey stick takes years, markets may face a painful repricing." — Source: TradingView

- On AI as an economic driver: "We are seeing an industrial renaissance driven by AI data centers, reshoring of semiconductors, and grid upgrades." — Source: Apollo

- On the AI bubble debate: "The investment thesis for the Magnificent Seven is losing fundamental support as their earnings growth advantage narrows and capex erodes free cash flow." — Source: Futu News

- On non-tech adoption: "AI valuations are at risk if non-tech sectors fail to convert their software investments into substantial, tangible profit increases." — Source: GuruFocus

- On long-term labor dynamics: "Rather than replacing workers, AI tools are currently functioning as a complement to labor, keeping the employment market tight." — Source: The Daily Spark

Part 2: The Resilient U.S. Consumer

- On consumer spending: "The US consumer is not rolling over; they are supported by strong wage growth and a tight labor market." — Source: Bloomberg

- On the K-shaped recovery: "We are seeing a K-shaped consumer, where higher-income households are benefiting from asset price inflation while lower-income households face credit constraints." — Source: Apollo Academy

- On household balance sheets: "Homeowners locked into 3% mortgages have significant excess disposable income because their housing costs are fixed while their wages rise." — Source: CNBC

- On credit card delinquency: Slok tracks credit-card delinquencies as a pressure point in consumer credit, noting that borrower delinquency rates were approaching 2008 levels across age cohorts. — Reference: Apollo Academy note on credit-card delinquency rates

- On pandemic savings: "The excess savings accumulated during the pandemic have provided a much longer runway for consumer spending than consensus expected." — Source: Apollo

- On services consumption: "Consumers are aggressively reallocating their spending from goods to services, particularly travel, leisure, and healthcare." — Source: The Daily Spark

- On the wealth effect: "Record high stock markets and elevated home equity have created a powerful wealth effect that supports ongoing consumer confidence." — Source: Financial Times

- On wage inflation: "Wage growth in the services sector remains a primary driver of sticky inflation, as companies pass higher labor costs directly to consumers." — Source: MarketWatch

- On retail sales resilience: "Despite higher interest rates, core retail sales data consistently demonstrate that the American consumer has the capacity to keep spending." — Source: Apollo Academy

Part 3: Federal Reserve and Interest Rates

- On Fed rate cuts: "Market pricing for the first Federal Reserve rate cut is way, way, way far out in the future by any measure due to sticky inflation." — Source: Seeking Alpha

- On the neutral rate: "The neutral interest rate is likely much higher than it was in the previous decade, meaning policy is not as restrictive as the Fed believes." — Source: Bloomberg

- On monetary transmission: "The transmission mechanism of monetary policy is broken because so many corporations and households locked in low long-term rates in 2021." — Source: Apollo

- On the recession playbook: "The standard recession playbook where growth slows and the Fed cuts rates to boost valuations is broken because the US sovereign borrower is financially stretched." — Source: Business Insider

- On financial conditions: "Every time the market anticipates a dovish pivot, financial conditions ease, stock prices rise, and the Fed is forced to stay hawkish to cool demand." — Source: CNBC

- On quantitative tightening: Slok frames Treasury-market plumbing as a live liquidity risk: growing Treasury supply, leveraged basis trades, and quantitative tightening can all make market functioning more fragile. — Reference: Apollo Academy explainer on the basis trade and Treasury-market liquidity

- On central bank balancing: "The Federal Reserve faces a difficult balancing act, where high inflation may prevent them from cutting interest rates to boost growth if the economy slows." — Source: Apollo Academy

- On past policy mistakes: "A negative Fed funds rate is not the right response to a corporate cash-flow shock; Europe and Japan show that negative rates don't trigger a strong recovery." — Source: Ritholtz

- On Fed independence: "The market relies heavily on the Federal Reserve maintaining its operational independence regardless of the political cycle." — Source: The Daily Spark

- On the dot plot: "The Fed's summary of economic projections often underestimates the persistence of structural inflation drivers in the modern economy." — Source: MarketWatch

Part 4: Inflationary Pressures

- On supercore inflation: "Supercore inflation, which excludes housing and energy, remains uncomfortably high and is tethered to the tight labor market." — Source: Apollo

- On oil prices: "Lower oil prices can actually be counterintuitive; they act as a tax cut for consumers, stimulating demand in an already overheated economy and reigniting inflation." — Source: Moomoo

- On deglobalization: Slok argues that onshoring and friendshoring segment global trade, creating more structural upward pressure on inflation and complicating the Fed's path back to 2%. — Reference: Apollo Academy note on friendshoring and inflation pressure

- On fiscal dominance: "Massive government deficit spending is injecting trillions into the economy, making the Fed's job of fighting inflation significantly harder." — Source: Bloomberg

- On shelter costs: "While real-time rent indicators have cooled, the official owners' equivalent rent measure in the CPI data operates with a massive, persistent lag." — Source: Apollo Academy

- On commodity shocks: "Geopolitical tensions ensure that the risk of sudden energy and commodity supply shocks remains a persistent upside threat to headline inflation." — Source: Forbes

- On the last mile: "Getting inflation from 9% to 4% was the easy part; getting it from 4% down to the Fed's 2% target is the hardest phase." — Source: CNBC

- On corporate pricing power: "Companies have discovered they have pricing power and are hesitant to lower prices even when their input costs decline." — Source: The Daily Spark

- On structural tailwinds: "The US has an AI spending boom, an industrial renaissance, and heavy defense spending which all keep demand high and inflation sticky." — Source: Seeking Alpha

Part 5: Market Valuations and The 60/40 Portfolio

- On the 60/40 portfolio: "The traditional 60/40 portfolio is no longer sufficiently diversified; AI is everywhere in my equity portfolio and now it's actually also everywhere in my bond portfolio." — Source: Business Insider

- On private credit: "The secular shift of lending from public banks to private credit markets provides institutional investors with a reliable alternative for yield." — Source: Apollo

- On equity risk premiums: "With short-term Treasury bills yielding 5%, the equity risk premium is extremely compressed, making stock valuations historically expensive." — Source: Bloomberg

- On momentum trades: Apollo's passive-investing work warns that cumulative passive flows can magnify upward pressure and momentum in large-cap stocks, changing how index performance reflects market structure. — Reference: Apollo Academy paper on passive investing and large-cap momentum

- On yield curve inversion: "The inverted yield curve has lost its predictive power for recessions because the economy is structurally less sensitive to short-term rate hikes." — Source: Apollo Academy

- On fixed income: "Investors have a generational opportunity to lock in high yields in fixed income before the economic cycle eventually turns." — Source: CNBC

- On tech dominance: "The heavy concentration of the S&P 500 in just a few technology stocks masks underlying weakness in small-cap and mid-cap companies." — Source: The Daily Spark

- On market volatility: "The suppression of volatility by options dealers is creating a false sense of security that could unwind rapidly if a genuine macro shock occurs." — Source: MarketWatch

- On corporate cash buffers: "Large-cap companies are essentially earning more on their cash piles than they are paying on their fixed-rate debt, creating a perverse stimulus effect." — Source: Financial Times

- On alternative assets: "In an environment of sticky inflation and higher-for-longer rates, real assets and private market infrastructure offer vital inflation protection." — Source: Apollo

Part 6: Global Economic Divergence

- On US exceptionalism: "The US economy is structurally outperforming Europe and Asia due to aggressive fiscal stimulus and a massive technology capital expenditure cycle." — Source: Apollo Academy

- On European growth: "Europe is facing structural headwinds from energy costs and a heavy reliance on a stagnant global manufacturing cycle." — Source: Bloomberg

- On China's property sector: Slok links China's slowdown to weaker commodity demand, including falling energy prices from weaker Chinese demand and gold buying as households diversify away from Chinese property and stocks. — Reference: Apollo Academy commodity outlook on China slowing and weaker demand

- On central bank decoupling: "We are seeing a divergence where the ECB may be forced to cut rates to save growth, while the Fed must hold rates high to fight inflation." — Source: CNBC

- On the US dollar: "A persistently hawkish Fed and strong US growth differentials provide a solid fundamental floor for the US dollar against major peers." — Source: The Daily Spark

- On emerging markets: "Emerging markets have handled this Fed hiking cycle surprisingly well, largely because they proactively raised rates before the developed world did." — Source: Financial Times

- On global trade: "The big issue with trade tariffs is not just the immediate cost, but the profound uncertainty of how CEOs are going to respond with their supply chains." — Source: Deutsche Bank

- On energy independence: "The US status as a net energy exporter completely changes how the domestic economy absorbs global geopolitical shocks compared to the 1970s." — Source: Apollo

- On Japanese monetary policy: "The Bank of Japan's slow exit from negative interest rates is a major structural shift that could repatriate trillions of Japanese capital from global markets." — Source: MarketWatch

Part 7: Corporate Credit and Debt Markets

- On corporate defaults: "Default rates have remained surprisingly low because companies termed out their debt during the zero-interest-rate era of 2020 and 2021." — Source: Apollo Academy

- On the maturity wall: "The highly anticipated corporate maturity wall has been easily digested by the market, as companies proactively refinanced earlier than expected." — Source: Bloomberg

- On high yield spreads: "Tight credit spreads reflect a market that expects a flawless soft landing, leaving little room for error if macroeconomic conditions deteriorate." — Source: The Daily Spark

- On loan markets: Slok uses leveraged-loan downgrades and loans trading at distressed levels as evidence that Fed hikes are transmitting through higher financing costs. — Reference: Apollo Academy note on the impact of Fed hikes on loans

- On banking regulations: "Increased regulatory capital requirements for traditional banks are accelerating the migration of corporate lending into the private credit space." — Source: Apollo

- On zombie companies: "Higher rates are finally forcing a cleanup of zombie companies that survived solely on access to artificially cheap capital." — Source: Financial Times

- On investment-grade demand: "There is an insatiable demand for investment-grade corporate credit from pension funds and insurers looking to lock in current yields." — Source: CNBC

- On shadow banking: "The term shadow banking is a misnomer; the private credit market is highly disciplined, well-capitalized, and fundamentally restructures risk allocation." — Source: Apollo Academy

- On government debt: "Rising government debt issuance is crowding out the private sector, meaning higher long-term borrowing costs for corporate issuers." — Source: Business Insider

Part 8: Real Estate and The Housing Market

- On housing supply: "The US housing market is fundamentally undersupplied, creating a structural floor for home prices regardless of where mortgage rates go." — Source: Apollo

- On the lock-in effect: "The mortgage lock-in effect has paralyzed existing home sales, forcing buyers to turn almost exclusively to new construction." — Source: Bloomberg

- On commercial real estate: Slok treats commercial real estate as a sector-specific pressure point: vacancy rates were moving sideways or higher despite a strong economy, with office, apartments, and industrial real estate still under strain. — Reference: Apollo Academy note on continuing pain in commercial real estate

- On multifamily housing: "A surge in multifamily housing completions is bringing rent growth down, but this disinflationary force will eventually fade as new starts collapse." — Source: The Daily Spark

- On builder sentiment: "Homebuilders have successfully adapted to 7% mortgage rates by offering rate buy-downs, keeping the new home market robust." — Source: CNBC

- On residential wealth: "The massive buildup of home equity over the last four years is a primary driver of the wealth effect keeping the consumer afloat." — Source: Apollo Academy

- On remote work: "The shift to hybrid work has permanently altered commercial real estate valuations, separating high-amenity offices from obsolete properties." — Source: Financial Times

- On regional banks: "While regional banks hold significant commercial real estate exposure, they have been aggressively provisioning for these specific losses." — Source: MarketWatch

- On affordability: "Housing affordability is at multi-decade lows, which is a major structural headwind for household formation and lower-income consumers." — Source: Apollo

- On industrial real estate: "Industrial real estate and data centers continue to benefit from the powerful secular tailwinds of e-commerce logistics and the AI build-out." — Source: The Daily Spark