Lessons from Allan Mecham

Allan Mecham ran Arlington Value Capital from an office above a Salt Lake City taco shop, beating the market for over a decade by doing as little as possible. He avoided complex models in favor of a heavily concentrated portfolio of simple businesses, prioritizing the avoidance of unforced errors over high-risk returns. This collection details his framework for stress-testing investments, staying intellectually honest, and tuning out Wall Street.

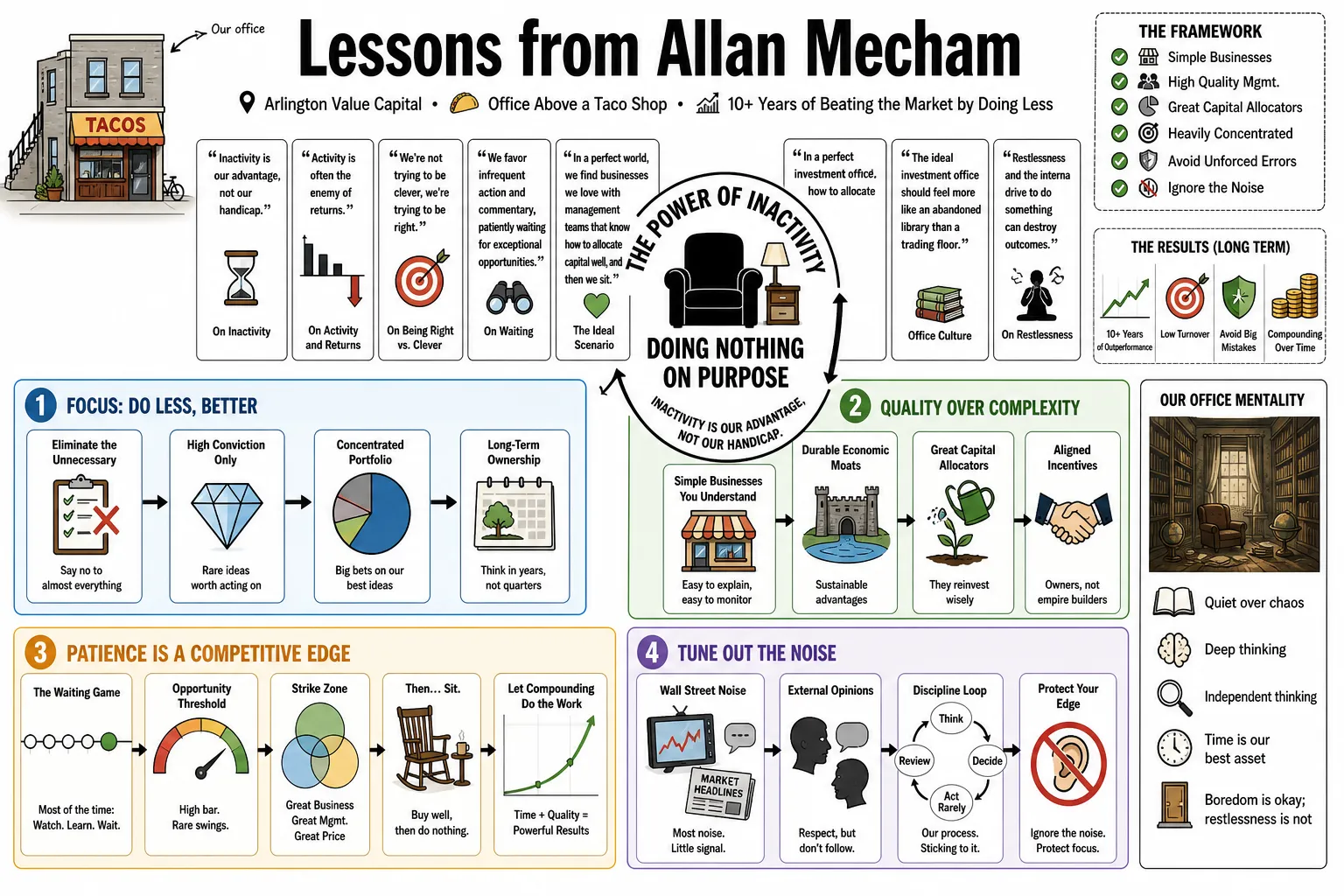

Part 1: The Power of Inactivity

- On Inactivity: "Inactivity is our advantage, not our handicap." — Source: [My Stock Secret]

- On Activity and Returns: "Activity is often the enemy of returns." — Source: [Substack]

- On Being Right vs. Clever: "We're not trying to be clever, we're trying to be right." — Source: [My Stock Secret]

- On Waiting: "We favor infrequent action and commentary, patiently waiting for exceptional opportunities." — Source: [Focused Compounding]

- On The Ideal Scenario: "In a perfect world, we find businesses we love with management teams that know how to allocate capital well, and then we sit." — Source: [Macro Ops]

- On Office Culture: The ideal investment office should feel more like an abandoned library than a trading floor. — Source: [MarketWatch]

- On Restlessness: Restlessness and the internal pressure to act lead directly to poor decision-making and capital destruction. — Source: [DocDroid]

- On Letting Capital Compound: By acting less, investors allow compound interest to work without the constant friction of frequent trading. — Source: [MOI Global]

- On Wall Street Norms: Most fund managers lack the structural leeway from their clients to patiently wait for exceptional opportunities. — Source: [Saber Capital Management]

- On Information Overload: "I disagree with the notion that more information is always better." — Source: [My Stock Secret]

Part 2: Intellectual Honesty and Mental Horsepower

- On Self-Deception: "Don't fool yourself, and remember you are the easiest person to fool," citing Richard Feynman as a guiding principle. — Source: [Substack]

- On Mental Boundaries: "Most investors are their own worst enemies, buying and selling too often, ignoring the boundaries of their mental horsepower." — Source: [Saber Capital Management]

- On Knowing Your Limits: Understanding the limits of your own intelligence is a far greater advantage than possessing a high IQ. — Source: [MOI Global]

- On The Electric Fence: An investor's circle of competence should be treated like an electric fence where you simply refuse to step outside of what you truly understand. — Source: [Substack]

- On Complexity: Complex financial models frequently mask a fundamental lack of business understanding. — Source: [Focused Compounding]

- On Critical Thinking: "There is no substitute for diligence and critical thinking." — Source: [Focused Compounding]

- On Temperament: Patience, discipline, and intellectual honesty matter far more in investing than raw processing power. — Source: [WordPress]

- On Ego: Adopting an ethos of not fooling oneself is the single greatest structural advantage an individual investor can develop. — Source: [Blogspot]

- On Humility in Research: Being diligent and thinking independently are the core ingredients of solid risk management. — Source: [Focused Compounding]

Part 3: Avoiding Unforced Errors

- On Reducing Mistakes: "I think if investors adopted an ethos of not fooling themselves, and focused on reducing unforced errors as opposed to hitting the next home run, returns would improve dramatically." — Source: [Economic Times]

- On The Loser's Game: Investing is akin to amateur tennis where the winner is typically the person who makes the fewest mistakes, not the one hitting spectacular winners. — Source: [Substack]

- On The Cost of Errors: "Unforced errors are a major barrier to strong returns." — Source: [Scribd]

- On Finding Big Winners: Avoiding big losers is consistently more important for long-term wealth creation than obsessively hunting for big winners. — Source: [MOI Global]

- On Emotional Interference: "Taking emotion out of the equation is like telling someone what's wrong with their golf game in the middle of their backswing." — Source: [My Stock Secret]

- On Hitting Home Runs: Focusing on base hits and mistake-avoidance yields better aggregate results than swinging for the fences. — Source: [Focused Compounding]

- On Self-Sabotage: The single biggest mistake investors make is acting as their own worst enemies through habitual over-trading. — Source: [Blogspot]

- On Structural Advantages: Individual investors have a distinct edge over professionals simply because they aren't forced to act when there is nothing intelligent to do. — Source: [Saber Capital Management]

- On The Need to Act: The internal pressure to constantly do something is the primary catalyst for most unforced errors in a portfolio. — Source: [DocDroid]

- On Defense vs Offense: "The best sell discipline is a stingy buy discipline." — Source: [My Stock Secret]

Part 4: Concentration and Conviction

- On Deep Understanding: "We believe it's more important to understand a few businesses deeply than dozens superficially." — Source: [My Stock Secret]

- On Frantic Diversification: "Concentrated patience beats frantic diversification every time." — Source: [My Stock Secret]

- On The Shot Clock: "We are a risk-averse fund looking for low-risk layup-type investments while other funds are akin to a run-and-gun offense that routinely takes a smattering of low-percentage shots." — Source: [Macro Ops]

- On Rarity of Opportunity: Extraordinary investment opportunities are incredibly rare and must be bet on heavily when finally identified. — Source: [Focused Compounding]

- On Fat Pitches: An investor should be willing to put up to half of their capital into an open-net tap-in goal if the conviction is high enough. — Source: [YouTube]

- On Core Holdings: A robust portfolio does not need fifty ideas because six to ten high-conviction holdings are often more than enough to compound capital. — Source: [Focused Compounding]

- On Sticking to What You Know: "We stick with what we know." — Source: [My Stock Secret]

- On Managing Turnover: "Turnover usually indicates a failure of judgement." — Source: [Macro Ops]

- On Selling Mistakes: "Selling is difficult, and my track record suggests it's usually a mistake." — Source: [My Stock Secret]

Part 5: Simplicity and Economic Furniture

- On Economic Furniture: Investors should seek out economic furniture, meaning stable and defensive businesses that fulfill permanent needs. — Source: [Substack]

- On Reading Habits: Time is better spent reading physical newspapers and historical annual reports than staring at blinking screens. — Source: [MarketWatch]

- On Forecasting: Predictions and macro-economic forecasting are largely useless distractions from understanding actual unit economics. — Source: [Focused Compounding]

- On Simplicity: A business must be simple enough that its fundamental staying power can be grasped without needing an advanced degree. — Source: [Scribd]

- On Complex Industries: Unproven companies or rapidly shifting, complex industries should be placed firmly in the too hard pile. — Source: [WordPress]

- On Financial Modeling: Deep qualitative understanding of a company’s competitive position beats complex spreadsheet modeling every time. — Source: [Scribd]

- On Common Sense: The investment industry often undervalues basic common sense in favor of false numerical precision. — Source: [Focused Compounding]

- On Predictability: The best investments are those where the outcome is highly predictable, not necessarily those with the highest theoretical ceiling. — Source: [Macro Ops]

- On The Hourglass Model: Distributors that sit in the middle of fragmented markets possess immense bargaining power and structural durability. — Source: [MOI Global]

- On Staying Power: The most critical variable to assess is a company's staying power over the next decade. — Source: [WordPress]

Part 6: The Owner Mentality

- On Viewing Stocks: "I need to understand the business like an owner," rejecting the idea of stocks as mere pieces of paper to be traded. — Source: [Blogspot]

- On Daily Fluctuations: An ownership mentality is the only reliable way to ignore daily market fluctuations and short-term noise. — Source: [Focused Compounding]

- On Assessing Management: The ideal setup requires a management team that intrinsically understands how to allocate capital efficiently. — Source: [Macro Ops]

- On Business Fundamentals: Buying a fractional share should carry the exact same weight and rigorous diligence as buying the entire enterprise outright. — Source: [Focused Compounding]

- On True Value: The intrinsic value of a business is disconnected from its daily quoted price on a public exchange. — Source: [YouTube]

- On Corporate Moats: A durable competitive moat is the primary protection an owner has against the gradual erosion of capital. — Source: [WordPress]

- On Operator Mindset: Thinking like a business operator rather than a fund manager grounds the entire investment process in reality. — Source: [MOI Global]

- On Capital Allocation: Management's ability to reinvest cash flow at high rates of return is the fundamental engine of long-term compounding. — Source: [Macro Ops]

- On Partnership: Investing should be viewed as a long-term partnership with the underlying business and its operators. — Source: [Focused Compounding]

Part 7: Risk and Stress Testing

- On The Downside: "It's ingrained in my DNA to think about the downside before any potential upside." — Source: [Focused Compounding]

- On The Primary Goal: The primary objective of an investor is not to maximize returns, but to absolutely ensure they do not lose capital. — Source: [WordPress]

- On Stress Testing: Every investment thesis must be severely stress-tested against difficult economic environments, such as high unemployment. — Source: [Focused Compounding]

- On Margin of Safety: A significant margin of safety is non-negotiable because it acts as the ultimate buffer against unforeseen adverse events. — Source: [WordPress]

- On Macro Shocks: Stress-testing should include hypothetical scenarios like sharply rising interest rates to see if the business would actually survive. — Source: [Focused Compounding]

- On Avoiding Zeros: You can recover from a period of low returns, but a permanent loss of capital structurally impairs compounding. — Source: [Substack]

- On Risk Profiles: Arlington Value sought low-risk, layup-type investments rather than speculating on heavily distressed turnarounds. — Source: [Macro Ops]

- On Resilience: A business is only as strong as its ability to weather the absolute worst-case scenario. — Source: [MOI Global]

- On Defense: Risk management is not about hedging with derivatives, it is about buying resilient businesses at sensible prices. — Source: [Focused Compounding]

Part 8: Culture, Capital, and Wall Street Contrast

- On Fund Size: "Ben and I gain satisfaction from trying to be among the best, not the biggest." — Source: [Hedge Fund Alpha]

- On Hot Money: "Accepting hot money would endanger the culture and my ability to perform." — Source: [MOI Global]

- On Investor Alignment: Having the right capital base composed of partners who understand long-term vision is essential to surviving periods of volatility. — Source: [YouTube]

- On Institutional Pressure: The pressure to generate short-term performance forces most institutions to act irrationally at exactly the wrong times. — Source: [WordPress]

- On Location: Operating from above a taco shop provided a necessary psychological distance from the manic noise of Wall Street. — Source: [Reddit]

- On Track Records: True outperformance requires a willingness to look foolish and tolerate non-activity in the face of short-term underperformance. — Source: [Scribd]

- On The Anti-Hero Path: Achieving massive long-term returns is the result of ignoring consensus and adhering strictly to personal boundaries. — Source: [MarketWatch]

- On Independence: Independence of thought is impossible if you are constantly measuring yourself against a benchmark on a quarterly basis. — Source: [Focused Compounding]

- On Legacy: True investment success is built quietly, without the need for constant media validation or asset gathering. — Source: [MOI Global]