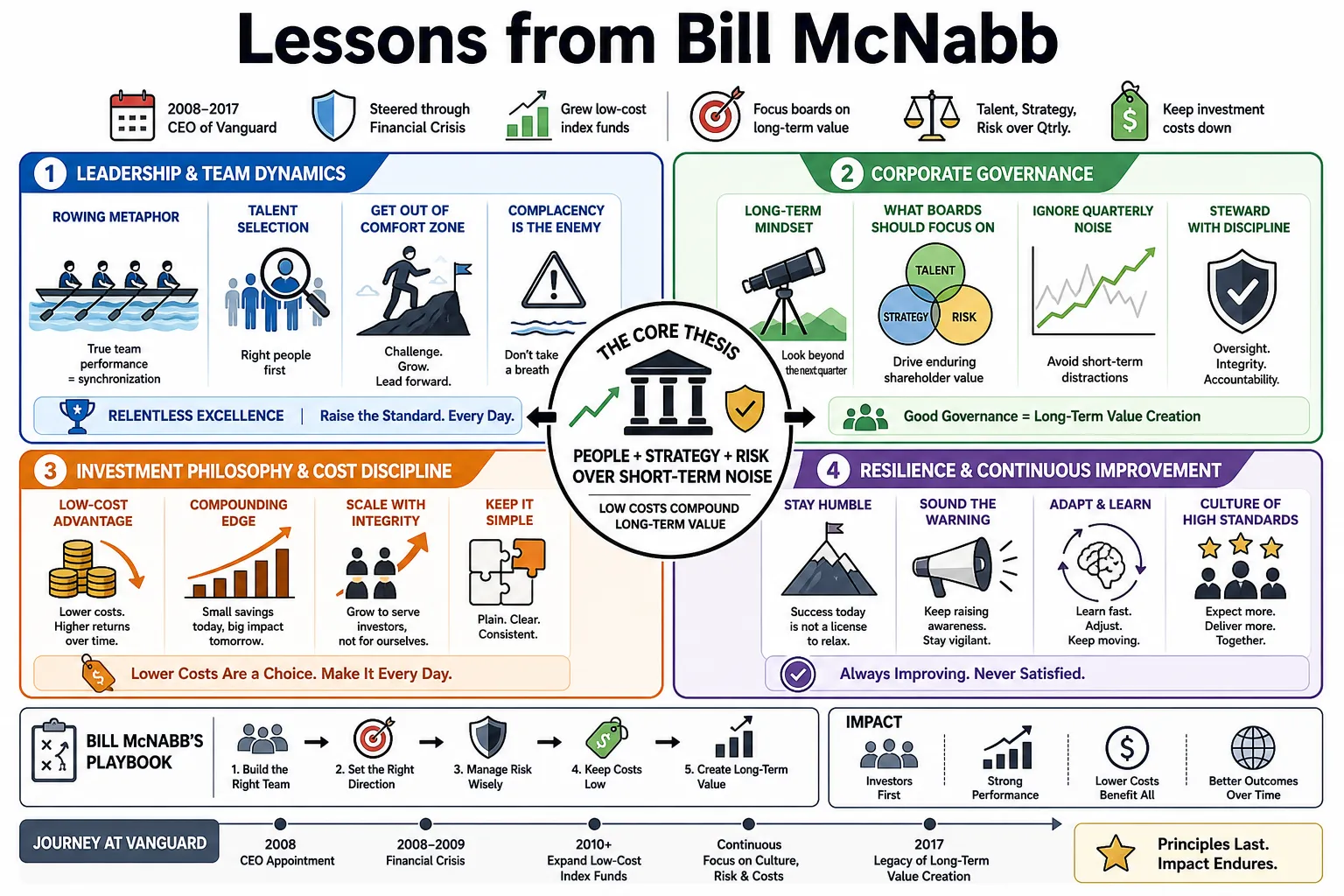

Lessons from Bill McNabb

Bill McNabb ran Vanguard from 2008 to 2017, steering the firm through the financial crisis and expanding its low-cost index funds. He pushed corporate boards to ignore quarterly earnings in favor of talent, strategy, and risk to drive long-term shareholder value. This profile collects his advice on team building, corporate governance, and keeping investment costs down.

Part 1: Leadership and Team Dynamics

- On the rowing metaphor: "True team performance resembles a crew shell, where individual brilliance is secondary to absolute synchronization." — Source: Wharton Executive Education

- On talent selection: "Picking the right people for the team is the fundamental precursor to any successful business strategy." — Source: Wharton Executive Education

- On comfort zones: "Successful leaders must continue to challenge themselves, get out of their comfort zone, and grow." — Source: Wharton Executive Education

- On complacency: "I'm continually sounding the warning about the danger of complacency to employees and leadership. It would be very easy for us to feel like we can take a breath." — Source: Harvard Business School

- On relentless excellence: "Complacency is a temptation. But we can't succumb to that temptation. A relentless pursuit of excellence is required." — Source: Harvard Business School

- On the necessity of margin: "Margin is not natural. You need to create it. Margin is the time and space needed to reflect, assess, think, create, and plan." — Source: Leadership Now

- On humility in knowledge: "Effective decision-making starts with an honest, humble assessment of what you actually know versus what you assume." — Source: Venrock

- On defining success: "A team cannot perform if the leader has not established a clear, unambiguous definition of what victory looks like." — Source: Venrock

- On raising the bar: "When an organization is performing at its peak, leaders should introduce stretch objectives and rotate talent to prevent stagnation." — Source: Wharton Executive Education

- On teaming as the future: "Individual heroics are becoming obsolete because the future of business belongs to highly collaborative, interdependent teams." — Source: Valence

Part 2: Navigating Crises and Market Volatility

- On crisis communication: "Nobody is getting fired. Everybody's job is safe. Your job is now is when you earn your money." — Source: Masters in Business

- On earning your keep: "Your job is to keep clients informed and happy and let them know this too will pass." — Source: Masters in Business

- On market turbulence: "Market volatility is always with us. It is a permanent feature of the market, not an anomaly to be feared." — Source: 401(k) Specialist

- On staying the course: Vanguard frames staying the course as active discipline, not set-and-forget investing: investors should keep a target asset allocation, rebalance when markets push it off course, and avoid letting headlines drive major portfolio changes. — Reference: Vanguard advisor article explaining staying the course through target allocation, rebalancing, and resisting market-driven portfolio changes

- On tempering volatility: "You can temper the effect of volatility by staying balanced among stock, bond, and money market funds, and by being diversified within those asset classes." — Source: 401(k) Specialist

- On the illusion of control: "You can't control market returns, but you can control how much you pay to invest." — Source: 401(k) Specialist

- On reactionary behavior: "Making major portfolio changes in the middle of a market drawdown is usually the most damaging mistake an investor can make." — Source: Vanguard

- On leadership visibility: "When markets crash, leaders must be highly visible to both employees and clients to project stability." — Source: Masters in Business

- On crisis as a test of culture: "A severe downturn reveals whether a company's stated values are real or just marketing copy." — Source: Masters in Business

- On the inevitability of recovery: "Historical perspective is essential during a crisis. Leaders must remind their teams that severe drawdowns have always eventually resolved." — Source: Masters in Business

Part 3: Cost Discipline and Passive Investing

- On the math of investing: "The less investors pay for an investment, the more they keep. Cost savings compound over the long term." — Source: ETF Strategy

- On giving away returns: "Think of cost as a percentage of your return that you give away. Every dollar you save in fees is a dollar that you keep." — Source: 401(k) Specialist

- On lowering the bar on fees: "We are not done on the cost side. We think we need to keep raising the bar on that." — Source: Masters in Business

- On the active management struggle: "I don't think we have seen the end of active management. But anyone who is a high-cost active manager will struggle." — Source: Financial Planning

- On industry competition: "The cost of investing will keep falling as more money shifts to passive investments and competition across the industry drives prices lower." — Source: Financial Planning

- On the passive misnomer: "In the past, some have mistakenly assumed that our predominantly passive management style suggests a passive attitude with respect to corporate governance. Nothing could be further from the truth." — Source: Special Situations Law

- On the structural advantage: "Operating at cost provides a permanent, compounding advantage over competitors who must extract profit margins for external shareholders." — Source: Masters in Business

- On the evolution of the investor: "Individual investors are smart and getting smarter. And that's a good thing. Increasingly, they are bringing a healthy consumer mentality to their investment portfolios." — Source: ETF Strategy

- On simplicity in fees: "Complicated fee schedules? Intricate investing strategies? Trash them. Selling complexity is a thing of the past." — Source: Financial Planning

Part 4: Corporate Governance and Board Engagement

- On demystifying governance: "Corporate governance should not be a mystery. For corporate boards, the way large investors vote their shares should not be a mystery." — Source: Harvard Law School Forum

- On the end of shyness: "There is still precious little communication between boards and shareholders. The historical hesitation to communicate directly is an outdated practice." — Source: Edelman

- On board self-awareness: "The best boards work hard to develop self-awareness, and seek feedback and perspectives independent of management." — Source: Edelman

- On engagement beyond the ballot: "Engagement beyond the ballot enables us to deal in nuance and in dialogue that drives meaningful progress over time." — Source: The Board Institute

- On stewardship: "An asset manager's duty extends beyond stock picking to acting as a permanent guardian of the clients' capital." — Source: Harvard Law School Forum

- On the board as eyes and ears: "Strong boards require diverse, experienced directors who serve as eyes and ears on risk." — Source: PR Newswire

- On behind-the-scenes pressure: "Public proxy fights are often less effective than private, sustained pressure on issues like excessive executive compensation." — Source: Masters in Business

- On CEO selection vs. pay: "Picking the right CEO is ten times more important than the compensation. But somebody has to be there to represent the shareholders." — Source: Business Insider

- On director diversity: "A board cannot effectively identify blind spots if its members share identical backgrounds and experiences." — Source: PR Newswire

Part 5: Rethinking Value: Talent, Strategy, Risk

- On flawed metrics: "Total Shareholder Return is an inadequate metric for evaluating the true, long-term health of an enterprise." — Source: Boardroom Governance

- On the TSR framework: "Boards must redefine value creation around three core pillars: Talent, Strategy, and Risk." — Source: Porchlight Books

- On incentivizing talent: "Building the right leadership team requires aligning their incentives with the long-term survival of the company, not the next quarter." — Source: Boardroom Governance

- On strategic communication: "Helping leaders take a longer-term view and effectively communicating that vision to investors is a primary duty of the board." — Source: Porchlight Books

- On centering risk: "Keeping major risks like cybersecurity and reputational crises front and center in board oversight is non-negotiable." — Source: Porchlight Books

- On reducing information asymmetry: "Directors must actively work to close the knowledge gap between themselves and the day-to-day management team." — Source: Indigo

- On the activist lens: "Boards should routinely analyze their own company with the critical, unsentimental eye of a hostile activist investor." — Source: Boardroom Governance

- On post-mortems: "Boards frequently fail to look back at past acquisitions to honestly assess if the promised synergies actually materialized." — Source: Business Insider

- On the failure to push reality: "It isn't fundamental dishonesty that causes people to go in a different direction. It's human nature. Boards usually don't push them to come to grips with reality." — Source: Business Insider

Part 6: Long-Termism and Countering Short-Term Pressures

- On toxic short-termism: "For too long, companies have sacrificed long-term value creation to generate short-term results, which erodes the sustainability strategic investors seek." — Source: Business Insider

- On the rise of permanent capital: "The growth of index funds has created a class of permanent investors who demand that companies manage for decades, not months." — Source: Harvard Business School

- On sustainable investing: "A company cannot survive if it ignores the long-term impacts of its operations on its stakeholders and environment." — Source: King & Spalding

- On the cost of complexity: "Intricate investing strategies usually exist to justify high fees, not to deliver better results for the client." — Source: Financial Planning

- On the savings mandate: "The most important and difficult step you can take to shore up your financial future is to save more than you think you'll need." — Source: 401(k) Specialist

- On patience as an edge: "In a market obsessed with immediate feedback, the willingness to wait years for a strategy to play out is a massive competitive advantage." — Source: Masters in Business

- On ignoring the noise: "Long-term investors must train themselves to tune out daily market commentary that encourages frantic trading." — Source: Vanguard

- On the danger of overreaching: "Competent executives often damage their companies by pursuing unnecessary acquisitions just to demonstrate short-term growth." — Source: Business Insider

- On regulatory disclosures: "The company lawyers tell you to list every possible thing you can dream of in the 10-K just as a protection. They kill you with quantity." — Source: Business Insider

- On the permanence of stewardship: "When an institution cannot sell a stock because it tracks an index, its only option to improve performance is to aggressively improve the company's governance." — Source: Harvard Law School Forum

Part 7: Client-Centricity and the Mutual Structure

- On predicting strategy: "If you want to predict our next move, think about what would benefit our funds' shareholders." — Source: Vanguard Q4 Transcript

- On structural alignment: "A mutual ownership structure eliminates the conflict between serving the people who buy the funds and the people who own the management company." — Source: Masters in Business

- On the consumer mentality: "Investors want to know what they are buying and how much they are paying for it." — Source: ETF Strategy

- On trust as currency: "In the financial industry, client trust is not just a soft metric. It is the fundamental economic engine of the business." — Source: Financial Planning

- On sharing economies of scale: "When a fund grows, the resulting cost savings must be returned to the investor in the form of lower expense ratios." — Source: ETF Strategy

- On democratizing investing: "Low-cost index funds have fundamentally leveled the playing field, allowing retail investors to capture the same returns as large institutions." — Source: Vanguard

- On fiduciary duty: "The obligation to place the client's interests first is absolute, requiring managers to reject profitable products if they don't serve the investor." — Source: Masters in Business

- On clarity in communication: "When you create fee schedules and investment strategies that clients can understand, everyone wins." — Source: Financial Planning

- On the ultimate scorecard: "A financial firm's success is not measured by its assets under management, but by the net returns actually delivered to its clients' pockets." — Source: 401(k) Specialist

Part 8: The Future of Advice, Technology, and Simplicity

- On the role of AI: McNabb argues that AI is a now-or-never operating shift: boards should push companies to stop over-deliberating, test practical use cases, learn from experiments, and build fluency before competitors turn the technology into an advantage. — Reference: Valence AI and the Workforce Summit transcript where McNabb urges companies to experiment with AI, build fluency, and avoid inaction

- On the limits of technology: "AI can help us do our jobs better, but it will never supplant the humanity of this profoundly personal profession." — Source: Wealth Management

- On the enduring value of advisors: "The role of the advisor is paramount, and it's what creates real, long-lasting impact." — Source: Wealth Management

- On the humanity of finance: "Wealth management is a profoundly personal profession. Clients ultimately need a human being to help them navigate life transitions." — Source: Retirement Income Journal

- On building sustainable practices: "Nurture existing clients because creating that trust will help advisors build better, more sustainable businesses." — Source: Financial Planning

- On the obsolescence of complex products: "The era of selling unnecessarily complicated investment vehicles is ending. Transparency is the new standard." — Source: Financial Planning

- On behavioral coaching: "The highest-value service an advisor provides is preventing clients from making emotional, destructive decisions when the market drops." — Source: Wealth Management

- On technological adoption: McNabb treats waiting for certainty on AI as the larger risk: the more experience, testing, and pivoting organizations do now, the more likely they are to capture opportunities instead of becoming victims of the technology shift. — Reference: Valence AI and the Workforce Summit transcript where McNabb says inaction on AI is the biggest mistake and early experimentation builds advantage

- On the ultimate goal: "The integration of better technology and simpler products should always serve one purpose: making it easier for everyday people to achieve financial security." — Source: Financial Planning