Lessons from Bill Nygren

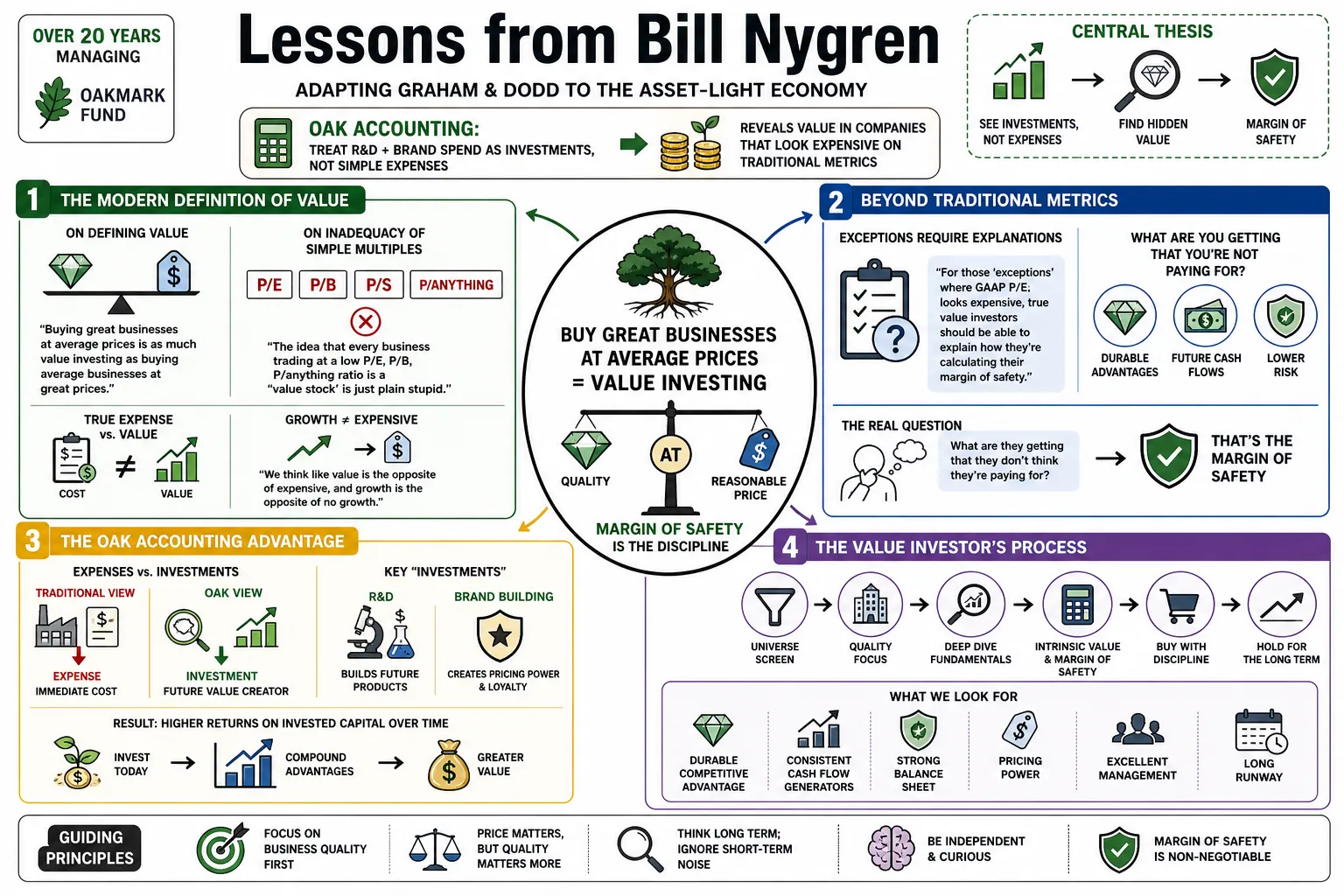

Bill Nygren has managed the Oakmark Fund for over two decades by adapting classic Graham and Dodd principles to an asset-light economy. His "Oak accounting" framework treats R&D and brand spending as investments rather than simple expenses, revealing value in companies that look expensive on traditional metrics.

Part 1: The Modern Definition of Value

- On defining value: "Buying great businesses at average prices is as much value investing as buying average businesses at great prices." — Source: [Oakmark Funds]

- On the inadequacy of simple multiples: "The idea that every business trading at a low P/E, P/B, P/anything ratio is a 'value stock' is just plain stupid." — Source: [Oakmark Insights]

- On true expense vs. value: "We think like value is the opposite of expensive, and growth is the opposite of no growth. Usually high growth companies bring high prices." — Source: [WealthTrack]

- On exceptions to the rule: "For those 'exceptions' where GAAP P/E looks expensive, true value investors should be able to explain how they're calculating their margin of safety: What are they getting that they don't think they're paying for?" — Source: [Forbes]

- On what makes a value stock: A value stock is simply a business trading at a significant discount to what a private buyer would pay in an all-cash transaction. — Source: [Morningstar]

- On adapting the value framework: Value investing isn't about buying dying industries on the cheap; it's about buying cash flows at a discount, regardless of the sector. — Source: [Barron's]

- On the danger of strict screens: Relying purely on statistical screens for low P/E ratios often leads you straight into value traps, which are businesses whose underlying value is deteriorating as fast as their stock price. — Source: [The Motley Fool]

- On market overreactions: The market frequently misprices businesses facing short-term headwinds, creating opportunities for those willing to look past immediate quarterly earnings. — Source: [CNBC]

- On avoiding dogmatism: The label of "growth" or "value" matters less than the mathematical reality of what you are paying versus what you are getting in future cash generation. — Source: [Value Investing Substack]

Part 2: Intangibles and Oak Accounting

- On rethinking GAAP: "We redo GAAP accounting to 'Oak accounting'... so much of the value today is in intangible assets." — Source: [Oakmark Official YouTube]

- On hidden cheapness: "A stock that doesn't look cheap on the surface might be one of the cheapest once you account for what the income statement treats as an expense." — Source: [Morningstar]

- On the value of brands: "A brand is a very valuable asset, but is usually not on the balance sheet." — Source: [QuotesWise]

- On R&D spending: When a company like Alphabet or Merck spends heavily on R&D, treating it entirely as an expense punishes the current earnings of a company that is actively building future value. — Source: [Barron's]

- On customer acquisition: Customer acquisition costs for software businesses are often expensed immediately, masking the true profitability of the recurring revenue those customers generate. — Source: [Invest Like the Best]

- On book value's limits: Price-to-book ratio has lost much of its relevance because modern businesses require far less physical capital and rely far more on intellectual property. — Source: [Oakmark Commentary]

- On capitalizing intangibles: By adjusting the financial statements to capitalize brand advertising and research, you get a much clearer picture of a company's true economic earnings. — Source: [Behind the Balance Sheet]

- On economic reality: The goal of accounting adjustments isn't to make a stock look cheaper, but to align the financial numbers with the economic reality of the business. — Source: [Value Investors Club]

- On competitive moats: Intangible assets like consumer trust and habit are often the most durable competitive advantages, yet they are entirely invisible on standard accounting statements. — Source: [Natixis]

Part 3: Margin of Safety and Intrinsic Value

- On the core definition: "The difference between a stock's current price and our estimate of the company's intrinsic value per share is the margin of safety." — Source: [Forbes]

- On the buy target: A stock becomes attractive when it trades at a substantial discount, typically around 60% of its intrinsic value. — Source: [Value Investing Substack]

- On the sell target: The standard discipline is to look to sell when the stock reaches 90% of its estimated intrinsic value. — Source: [Oakmark Funds]

- On future valuation: "Investing in businesses when their stock prices are low, relative to their intrinsic values, provides a margin of safety and an opportunity for significant returns when the market eventually corrects." — Source: [Natixis]

- On the required hurdle: "We require analysts to project business value seven years into the future. If the combination of expected annual value growth and dividend yield doesn't at least match the market, we won't buy them." — Source: [Oakmark Insights]

- On value traps: "We define value traps as companies where value does not increase with time." — Source: [Fox Business]

- On compounding intrinsic value: The margin of safety isn't a static number. If the business grows its intrinsic value per share every year, your margin of safety actually widens over time. — Source: [The Investors Podcast]

- On the ultimate buyer: Value is best estimated by asking what a rational corporate buyer would pay for the entire enterprise in cash, rather than what a trader will pay for a slip of paper tomorrow. — Source: [Barron's]

- On business quality: A deep discount on a melting ice cube is not a margin of safety. True safety comes from a growing intrinsic value. — Source: [Morningstar]

- On price vs value: Price is what you pay today. Intrinsic value is the discounted stream of cash the business will generate over its lifetime. — Source: [QuotesWise]

Part 4: Managing Risk and Mistakes

- On the true meaning of risk: "We define risk as losing money, not as volatility." — Source: [Morningstar]

- On handling errors: "A big part of any investor's success or failure in this business is how they manage mistakes." — Source: [QuotesWise]

- On cutting losses: "Generally, the sooner you can admit them, the more likely you minimize their impact on your performance." — Source: [QuotesWise]

- On lumpy returns: "We would much rather earn a lumpy 15% than a stable 12%." — Source: [Morningstar]

- On non-consensus bets: "To make excess profits, you need to hold a non-consensus view and be right." — Source: [The Motley Fool]

- On permanent capital loss: The greatest risk in investing is paying a high multiple for a business that subsequently experiences a permanent decline in its growth rate. — Source: [Oakmark Commentary]

- On avoiding macro predictions: "We think it is much easier to find an individual stock that the market thinks is worth less than we do than it is to make correct non-consensus forecasts about the economy." — Source: [Oakmark Letters]

- On conviction: When a stock drops, you must have the analytical rigor to know whether the thesis is broken or if the market is simply offering you the same business at a better price. — Source: [CNBC]

- On thesis drift: The most dangerous mistake is subtly changing your original investment thesis to justify holding onto a stock that has fallen for fundamental reasons. — Source: [Invest Like the Best]

- On humility: Even the best analysts will be wrong on a third of their picks. Success depends entirely on making sure the losers don't wipe out the compounding of the winners. — Source: [Value Investors Club]

Part 5: Time Horizon and Market Psychology

- On emotional arbitrage: "Taking advantage of the values created by emotional investors is the cornerstone of the Oakmark Fund's approach to investing." — Source: [QuotesWise]

- On trading partners: "We try to buy from fearful or bored investors and sell to greedy investors who want excitement." — Source: [QuotesWise]

- On gambling vs. investing: "Short-term price speculation is really gambling." — Source: [QuotesWise]

- On time arbitrage: "The longer it takes for the market to realize the potential of one of our companies, the greater my return is." — Source: [Morningstar]

- On looking far ahead: "Our advice is always think about what a company might be worth 7 years from now. And try and buy it at a very significant discount to that today." — Source: [WealthTrack]

- On Wall Street's myopia: Most of the market is optimizing for the next quarter. If you can underwrite the next five to seven years, you are playing a game with far less competition. — Source: [The Investors Podcast]

- On holding periods: Extending your holding period allows you to ignore the quarterly noise and let the fundamental compounding of the business do the heavy lifting. — Source: [Barron's]

- On geopolitical noise: Macro events and geopolitical crises create short-term panic but very rarely alter the seven-year intrinsic value of a well-capitalized business. — Source: [Barron's]

- On patience: The hardest part of value investing is the psychological endurance required to look wrong for years before the market agrees with you. — Source: [Value Investing Substack]

Part 6: Assessing Management and Capital Allocation

- On owner-operators: The ideal management team thinks and acts like owners, treating shareholder capital as a precious resource instead of a tool for empire building. — Source: [Oakmark Insights]

- On returning capital: "A company should return capital to its owners when that adds more to per-share value than would reinvestment in the business." — Source: [Fox Business]

- On the power of buybacks: "Our preference for how that capital is returned is repurchase of undervalued shares." — Source: [Fox Business]

- On the impact of leadership: "It is really amazing to see over the course of our holding period... how much value a great management can add that never was incorporated in our model, and conversely, how much value a bad management can destroy." — Source: [Oakmark Insights]

- On aligned incentives: We look for management teams whose compensation structures heavily weight long-term per-share value creation over short-term revenue growth. — Source: [Morningstar]

- On capital discipline: A company that shrinks its share count by 5% a year can generate significant shareholder wealth even if its underlying revenue growth is entirely stagnant. — Source: [CNBC]

- On value-destroying acquisitions: The biggest red flag is a CEO who routinely overpays for large acquisitions simply to increase the absolute size of the company they manage. — Source: [The Motley Fool]

- On dividend policy: Dividends are fine, but when a stock is trading at a deep discount to intrinsic value, share repurchases are mathematically vastly superior for long-term holders. — Source: [Forbes]

- On strategic patience: Good management teams are willing to endure a depressed stock price and Wall Street criticism if it means making the right long-term capital allocation decisions. — Source: [Barron's]

- On track records: We judge management by the historical returns on invested capital they have achieved over the last cycle, rather than by their investor day presentations. — Source: [Invest Like the Best]

Part 7: Concentration and Portfolio Construction

- On stock selection: A portfolio should be concentrated enough that your best ideas can meaningfully drive performance, instead of being diluted by your fiftieth-best idea. — Source: [Oakmark Funds]

- On conviction weightings: We construct portfolios based on conviction and the depth of the discount. The cheaper the stock relative to its intrinsic value, the larger the position size. — Source: [Morningstar]

- On benchmark hugging: If you own a hundred stocks, you are basically buying an expensive index fund and guaranteeing you won't outperform the market. — Source: [The Investors Podcast]

- On sector constraints: We don't believe in rigid sector weighting. If we find the best values in financials and consumer discretionary, that is where the portfolio will be concentrated. — Source: [CNBC]

- On tracking error: You cannot beat the market without looking different from the market, which means you have to be comfortable with periods of significant tracking error. — Source: [Oakmark Commentary]

- On the threshold for inclusion: Every new stock added to the portfolio must fight its way in by offering a better risk-adjusted return profile than the stocks we already own. — Source: [Barron's]

- On cash positions: We do not hold cash to time the market. Cash is simply the byproduct of a lack of qualifying investment opportunities at our required margin of safety. — Source: [Fox Business]

- On letting winners run: If a business is compounding its intrinsic value rapidly, we are happy to hold it even as its multiple expands, provided it still trades below our estimate of its future value. — Source: [Forbes]

- On forced diversification: Diworsification happens when managers buy mediocre businesses just to hit a quota for a specific industry exposure. — Source: [Value Investors Club]

Part 8: The Growth vs. Value Dichotomy

- On false categories: The industry's strict division of growth versus value creates artificial silos that blind investors to highly profitable crossover opportunities. — Source: [Oakmark Insights]

- On growth as a component: Growth is simply one input into the calculation of value. A rapidly growing company can be a deep value stock if the market underestimates the durability of that growth. — Source: [WealthTrack]

- On the momentum train: Investors are frequently rewarded in the short term for the belief that what goes up keeps going up, which eventually leads to severe mispricing. — Source: [Oakmark Letters]

- On valuation spreads: When the gap between the most expensive stocks and the cheapest stocks reaches historic extremes, it creates a generational opportunity for disciplined value investors. — Source: [Morningstar]

- On the S&P 500's risk: The broader market index has increasingly become a concentrated growth fund, embedding far more risk for passive investors than in previous decades. — Source: [CNBC]

- On high-multiple opportunities: Sometimes a stock with a high P/E is actually a value stock, provided its long-term cash generation potential vastly exceeds what the current multiple implies. — Source: [Barron's]

- On the danger of consensus: Paying a premium for the market's favorite growth stories leaves no margin of safety for execution missteps or a change in macroeconomic conditions. — Source: [The Motley Fool]

- On tech as value: Technology companies with recurring revenue, strong moats, and massive free cash flow generation can absolutely fit the strict criteria of a value investor. — Source: [Invest Like the Best]

- On enduring principles: The nature of the businesses may change from industrial to digital, but the mathematical law that you must pay less than a business is worth remains undefeated. — Source: [Natixis]