Lessons from Boaz Weinstein

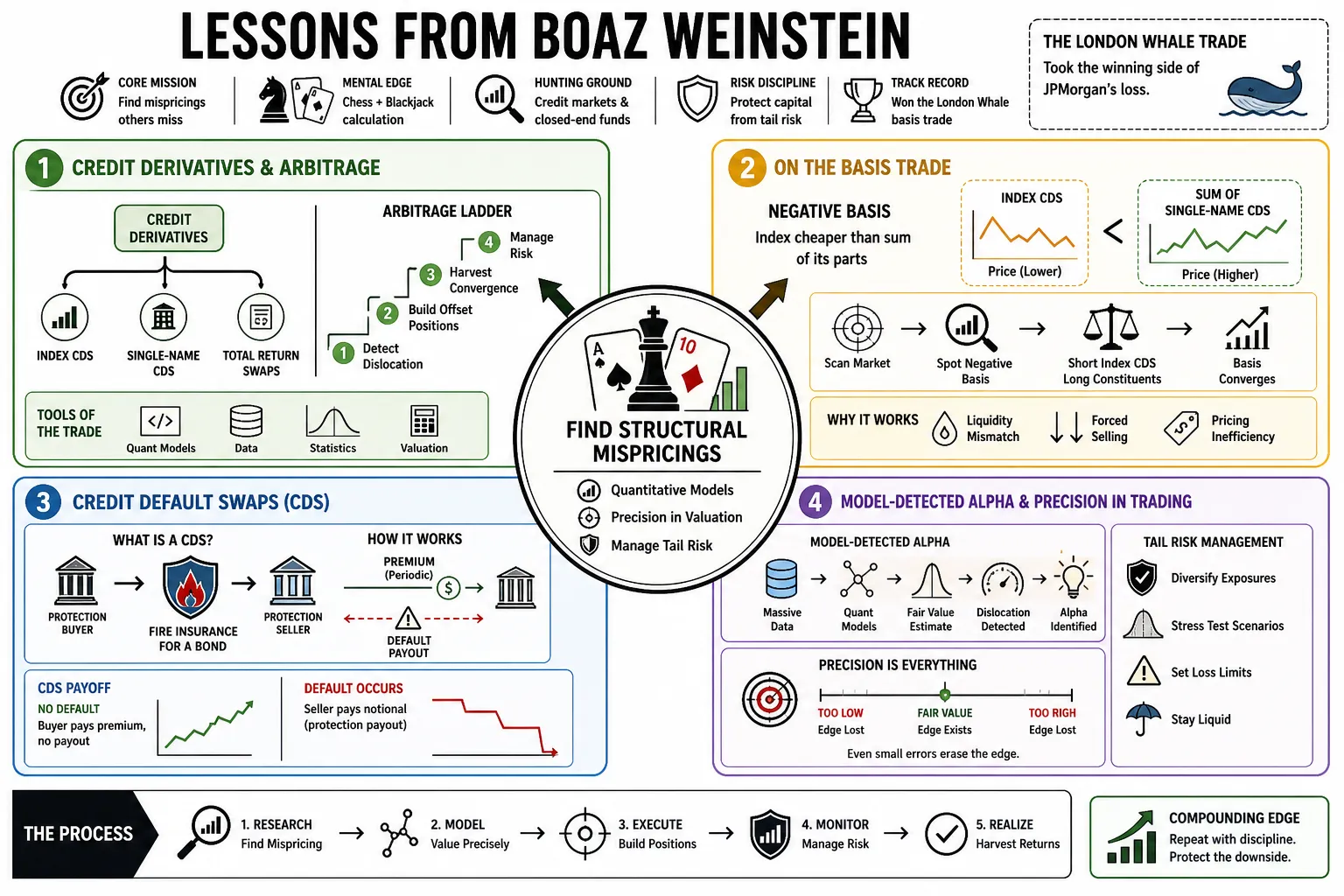

Boaz Weinstein founded Saba Capital after famously taking the winning side of JPMorgan’s "London Whale" trade. He applies the calculation of master-level chess and blackjack to hunt for mathematical edges in credit markets and closed-end funds. This profile breaks down his methods for exploiting structural mispricings and managing tail risk.

Part 1: Credit Derivatives & Arbitrage

- On the Basis Trade: "The core of our strategy is identifying the 'negative basis' where the price of a credit index is significantly cheaper than the individual credit default swaps of the companies inside it." — Source: Medium

- On Credit Default Swaps (CDS): "Think of a CDS as fire insurance for a bond; you pay a premium to protect against the possibility that a company defaults on its debt." — Source: Bloomberg

- On Model-Detected Alpha: "Our edge comes from using quantitative models to detect when even the largest banks have allowed a pricing dislocation to become irrational." — Source: Wikipedia

- On Precision in Trading: "Precision is the most important thing in this game; if you are even slightly off in your calculation of fair value, your edge disappears." — Source: Hedge Fund Alpha

- On Relative Value: "We look for 'straddle' opportunities in the credit curve, such as when the cost of short-term insurance is nearly identical to long-term insurance despite vastly different risks." — Source: Financial Times

- On Capital Structure Complexity: "I avoid instruments like AT1 bonds because their terms are so ambiguous that they are essentially impossible to value mathematically." — Source: Twitter/X

- On Market Efficiency: "Markets are generally efficient, but they are not that efficient; structural constraints often prevent institutions from closing obvious gaps." — Source: Masters in Business

- On Liquidity in Credit: "In credit markets, liquidity is often a mirage that disappears exactly when you need it most to exit a crowded trade." — Source: Bloomberg Invest

- On Structural Mispricings: "We look for situations where a market participant is forced to trade for reasons other than profit, such as regulatory requirements or size constraints." — Source: Business Insider

- On the Lure of Yield: "Many investors focus so much on the coupon that they ignore the 'tail risk' embedded in the underlying credit default probability." — Source: CNBC

Part 2: Tail Hedging & Volatility

- On Tail Risk Insurance: "The goal is to buy 'fire insurance' for your portfolio when it is cheap, not when the building is already on fire." — Source: Bloomberg Podcasts

- On the Cost of Hedging: "You can finance the cost of your tail hedges by selling protection on high-quality, investment-grade names that are extremely unlikely to default." — Source: Saba Capital Management

- On Asymmetrical Returns: "We look for trades where we lose a little bit every day if nothing happens, but make 50 to 100 times our money if a black swan event occurs." — Source: YouTube

- On Volatility as an Asset Class: "Volatility is not just a risk measure; it is a commodity that can be bought when the market is complacent and sold when it is panicked." — Source: Institutional Investor

- On the 2020 COVID Crash: "During the 2020 crash, our tail fund returned 99% because we were long volatility and credit protection at a time when the market had priced in zero risk." — Source: Financial Times

- On Defensive Positioning: "Maintaining 'dry powder' is not just about having cash; it is about having positions that will actually appreciate in value during a liquidation." — Source: The Compound and Friends

- On the Failure of Traditional Hedges: "Traditional equity puts can fail during a bear market if correlations break down; credit-based hedges are often more direct." — Source: Ritholtz - The Big Picture

- On Complacency: "The most dangerous time in the market is when everyone agrees that a 'V-shaped recovery' is guaranteed." — Source: Podscripts

- On Market Regimes: "You have to understand the regime you are in; a strategy that works during Quantitative Easing will likely blow up during Quantitative Tightening." — Source: Bloomberg News

- On Hedging for the 'Unthinkable': "We build portfolios to survive events that most people think are impossible, because those are the only events that truly move the needle." — Source: Investment Week

Part 3: Closed-End Fund (CEF) Activism

- On Buying Dollars for 80 Cents: "Buying a closed-end fund at a 20% discount is literally buying a dollar for 80 cents; our job is to make it a dollar again." — Source: SEC.gov

- On the 'Magic Button': "Fund boards have a 'magic button' they can press to turn a closed-end fund into an open-ended one, instantly closing the discount for shareholders." — Source: Bloomberg Invest

- On Permanent Capital: "Asset managers love 'permanent capital' because they collect fees forever regardless of whether the fund trades at a massive discount to its actual value." — Source: Money Stuff Podcast

- On Shareholder Rights: "Our activism is about ensuring that boards fulfill their fiduciary duty to shareholders rather than simply acting as a rubber stamp for management fees." — Source: Saba Capital Press Release

- On Activism vs. Arbitrage: "In CEF activism, you control your own destiny; you don't have to wait for a buyer, you just have to win the proxy vote." — Source: YouTube

- On Trapped Capital: "Many closed-end funds are 'forever funds' where investors are trapped unless an activist forces the manager to offer a tender." — Source: SEC.gov Transcript

- On the 'Robin Hood' Element: "There is a social good to our engagement; we are helping retail investors recover value that big managers have essentially locked away." — Source: Bloomberg News

- On Discount Persistence: "If a fund trades at a discount for years, it is a sign that the management has failed to provide a compelling reason for the market to value its assets correctly." — Source: Bluebell PWM

- On Fighting Industry Titans: "I don't need to be 'besties' with Larry Fink; my only priority is making sure my investors get the full value of the assets they own." — Source: Bloomberg TV

- On Proxy Contest Strategy: "The way to win a proxy fight is to show the other shareholders that the manager is being paid a fee on assets that the market only values at 75 cents." — Source: YouTube

Part 4: Private Credit & "Volatility Laundering"

- On Volatility Laundering: "Private credit managers practice 'volatility laundering' by keeping marks steady even when the market environment suggests a 20% decline." — Source: Altswire

- On Stale Pricing: "The lack of daily mark-to-market in private credit is a bug that the industry has cleverly marketed as a feature to retail investors." — Source: OPM Wire

- On the 'London Whale' Comparison: "The current situation in semi-liquid private credit funds looks exactly like the London Whale—massive positions with no way out when everyone wants to sell." — Source: Fox Business

- On Illiquidity Gates: "The promise of 5% quarterly redemptions is fire insurance that doesn't work if there's an actual fire and everyone hits the gate at once." — Source: Bloomberg Podcasts

- On 'Dumb Things' for Fees: "Managers will do 'dumb things' to maintain high Net Income figures just to justify their fees while the underlying asset value is eroding." — Source: CNBC Inside Alts

- On Retail Vulnerability: "Retail investors are being sold complex private credit products that they do not have the sophistication to value, especially when redemptions are restricted." — Source: Hedgeweek

- On Systemic Nightmares: "If the snowball of redemptions in private credit starts rolling, it could turn into a systemic nightmare because these funds are too large to liquidate quickly." — Source: Benzinga

- On the 'Lure' of Semi-Liquid Funds: "Wall Street always goes to excess, and the 'lure' of these semi-liquid funds was the ability to gather billions in assets that are functionally permanent." — Source: SEC.gov

- On Marking at Par: "You can mark a loan at 100 for as long as you want, but that doesn't mean a single person would actually buy it from you at that price." — Source: YouTube

Part 5: The London Whale & Institutional Logic

- On the London Whale Opportunity: "The London Whale trade was a once-in-a-generation example of a single institution becoming so large that they broke the market's equilibrium." — Source: Masters in Business

- On Harpooning the Whale: "When we saw that JPMorgan was selling protection at a massive discount, we didn't just buy some; we bought as much as the market would allow." — Source: Business Insider

- On Public Transparency: "I publicly recommended the London Whale trade because I wanted other hedge funds to bring more 'harpoons' to the fight and force the mispricing to close." — Source: Wikipedia

- On Institutional Inefficiency: "Large banks often have internal mandates that force them to trade against their own economic interest to manage a specific risk number." — Source: BSIC

- On the CDX IG9 Index: "The CDX index was trading so much cheaper than its constituents that it was essentially a mathematical arbitrage that couldn't last forever." — Source: The Guardian

- On Holding Through Losses: "We were down significantly on the Whale trade for months, but the math told us we were right, so we added to the position instead of folding." — Source: Medium

- On Smelling Blood: "Once the news broke that JPMorgan was 'stuck' in their position, the rest of the market moved in to pick them apart, which is how arbitrage works." — Source: CFA Institute

- On Modern-Day Whales: "Whenever you see an asset class where one player dominates 50% of the volume, you are looking at a potential London Whale-type opportunity." — Source: Bloomberg News

- On the Foundation of Saba: "The success of the Whale trade provided the foundational capital that allowed us to build Saba into the activist powerhouse it is today." — Source: Financial Times

Part 6: Risk Management & The Psychology of Loss

- On Emotional Regulation: "I get things wrong constantly, but the key is being able to handle it emotionally so it doesn't cloud your next decision." — Source: Bloomberg Invest

- On Process vs. Outcome: "You must judge yourself by your process, not the outcome; you can make a perfect bet and still lose because of bad luck." — Source: YouTube

- On Learning to Lose: "Growing up playing chess and blackjack taught me how to lose frequently and move on without it affecting my ego." — Source: Hedge Fund Alpha

- On Signal vs. Noise: "Successful trading is about sifting through the constant noise of the market to find the few probabilistic signals that actually matter." — Source: Saba Capital Management

- On Booking a Loss: "The 'surrender' move in blackjack is exactly like booking a loss in trading; you take the hit now to preserve your capital for a better count." — Source: YouTube

- On Sizing Best Ideas: "Many traders fail because they size their biggest, high-conviction ideas too small relative to their average position." — Source: The Compound and Friends

- On Over-Diversification: "Diversification can be a form of laziness if you are buying 60 things where you have no edge instead of five things where you do." — Source: YouTube

- On Intellectual Honesty: "If the facts change and your original thesis is no longer supported by the math, you have to be honest enough to exit immediately." — Source: Bloomberg News

- On the Tortoise Strategy: "I am more of the tortoise than the hare; I prefer steady, repeatable gains from structural mispricings over chasing a 10x long shot." — Source: YouTube

Part 7: Chess, Blackjack & Decision Strategy

- On Long-Range Planning: "Chess is the ultimate game of long-range strategy, teaching you to think five or ten moves ahead of your opponent." — Source: YouTube

- On Pattern Recognition: "My background in chess helps me recognize recurring patterns in market distress that others might see as isolated incidents." — Source: Ritholtz - The Big Picture

- On the Kelly Criterion: "I apply the Kelly Criterion to my trading—betting more when the 'count' is high and the odds are overwhelmingly in our favor." — Source: Scribd

- On Blackjack as a Laboratory: "Blackjack is the perfect laboratory for understanding risk; the odds are fixed and the only variable is your discipline to bet correctly." — Source: Hedge Fund Alpha

- On Poker vs. Chess: "Poker is a game of deception, but chess is a game of pure logic; I find the logic of chess much more applicable to credit trading." — Source: YouTube

- On the 'True Count': "In card counting, you wait for the true count to turn positive; in trading, you wait for the discount to become so large that the downside is capped." — Source: Bloomberg News

- On Discipline Under Pressure: "In blackjack, you can't look like you're counting; in the market, you can't look like you're panicked if you want to get your orders filled." — Source: Hedge Fund Alpha

- On Precision vs. Creativity: "Chess requires a mix of precision and creativity, whereas blackjack is pure calculation; trading requires both." — Source: YouTube

- On Betting Your Edge: "You should never make a big bet unless you can quantify your edge down to the second decimal point." — Source: Saba Capital Management

Part 8: Advice to Traders & Macro Outlook

- On Finding Your Edge: "The first question every trader should ask is: 'Why am I the one being offered this trade, and what is my specific edge?'" — Source: Bloomberg TV

- On Avoiding 'Shots at Glory': "Don't chase the meme stocks or the 100x options; find a repeatable system that returns 10-15% and let it compound." — Source: YouTube

- On Managing Your 'Tail': "Always be aware of what happens if you are 100% wrong; ensure that a single mistake doesn't end your career." — Source: Hedge Fund Alpha

- On the Carousel of Nightmares: "The current credit market feels like a 'carousel of nightmares' where risks are piling up but everyone is too distracted by the bull market to notice." — Source: Podscripts

- On Quantitative Tightening: "The undoing of QE is going to be far more violent than people expect because we have never lived in a world with this much debt and rising rates." — Source: Bloomberg News

- On Permanent Capital Risks: "The biggest risk for retail investors today is being lured into 'permanent capital' vehicles that they cannot exit when the macro tide turns." — Source: SEC.gov

- On Buying Pessimism: "My favorite strategy is buying pessimism and selling optimism—betting that the market's fear is greater than the actual risk of the underlying assets." — Source: Benzinga

- On the Importance of Humility: "You have to be humble enough to realize that the market can stay irrational longer than you can stay solvent, even if you are right." — Source: YouTube

- On the Future of Credit: "The next credit cycle will be driven by the realization that private credit marks were inflated, leading to a massive wave of forced selling." — Source: Bloomberg News