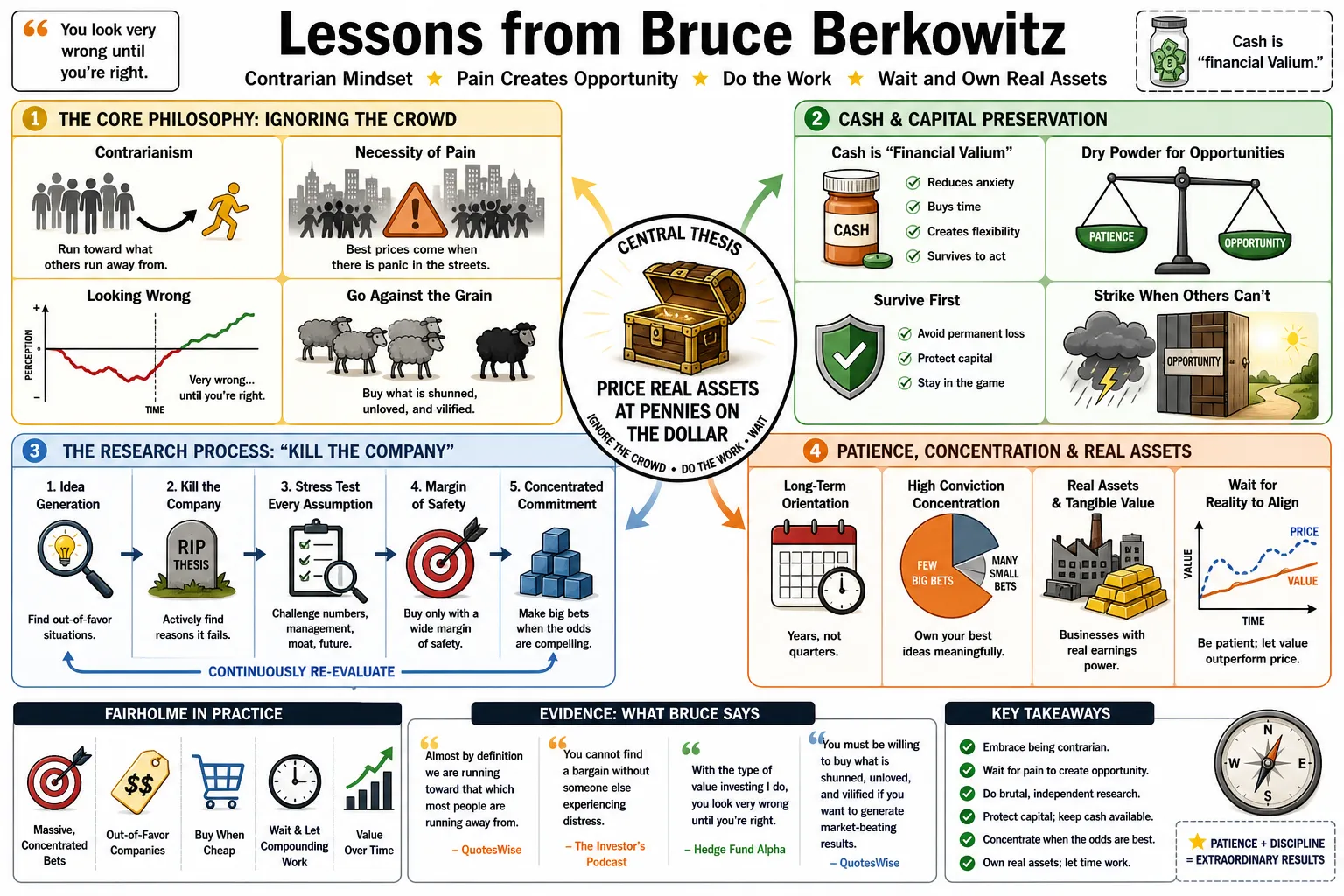

Lessons from Bruce Berkowitz

Bruce Berkowitz built Fairholme Capital Management on massive, concentrated bets on out-of-favor companies. He treats cash as "financial Valium" and relies on a strict "kill the company" research process, actively trying to break his own thesis before committing capital. The lessons below cover his method for pricing actual risk and waiting out the market to buy real assets for pennies on the dollar.

Part 1: The Core Philosophy: Ignoring the Crowd

- On Contrarianism: "Almost by definition we are running toward that which most people are running away from. Because how else are you going to get a very reasonable cheap price on a good company unless the market place believes something is terribly wrong." — Source: QuotesWise

- On the Necessity of Pain: "You cannot find a bargain without someone else experiencing distress; the best prices are found when there is panic in the streets." — Source: The Investor's Podcast

- On Looking Wrong: "With the type of value investing I do, you look very wrong until you're right." — Source: Hedge Fund Alpha

- On Going Against the Grain: "You must be willing to buy what is shunned, unloved, and vilified if you want to generate market-beating returns." — Source: Institutional Investor

- On Market Inefficiencies: "The market often misprices assets during a crisis because forced selling overwhelms fundamental valuation." — Source: Forbes

- On Solitary Decision Making: "Working alone or with a tiny team is often an advantage, as committees naturally revert to the safety of the consensus." — Source: WealthTrack

- On Early Movers: "Being too early is indistinguishable from being wrong, but it is often the price of admission for finding true value." — Source: The Business Brew

- On Popularity: "If everyone agrees with your investment thesis when you first make the purchase, you probably paid too much." — Source: Dataroma

- On Greed vs. Fear: "The time to get greedy is when everybody's running for the hills with fear. That's usually a great time to get the greed going." — Source: Economic Times

- On Enduring the Wait: "The gap between price and intrinsic value can take years to close, requiring a psychological stamina that most market participants lack." — Source: Advisor Perspectives

Part 2: Defining Risk and Surviving Volatility

- On the Definition of Risk: "Risk is not volatility or a fluctuating stock price; risk is the chance of a permanent loss of capital adjusted for inflation." — Source: Gracious Quotes

- On Volatility as Opportunity: "Volatility creates the false perceptions necessary for value investors to buy assets for pennies on the dollar." — Source: Medium

- On Survival First: "The trick in life is not to die. The trick in investing is not to lose." — Source: Arbor Investment Planner

- On Avoiding Catastrophe: "You should never take a risk that can result in financial death, no matter how favorable the odds appear to be." — Source: Advisor Perspectives

- On "Russian Roulette" Risks: "If a one-in-a-hundred chance kills you, the ninety-nine percent success rate does not matter. Keep away from existential risks." — Source: The Investor's Podcast

- On Price Drops: "I don't see how a security if it goes down 50% in price is riskier than it was when it was double that price." — Source: QuotesWise

- On Political Risk: "Relying on the government or regulators to behave rationally or honor contracts introduces a severe, unquantifiable risk, as seen in the GSE investments." — Source: Business Insider

- On Debt and Ruin: "Over-leveraged balance sheets are the most common cause of a permanent loss of capital, transforming a temporary problem into a fatal one." — Source: Economic Times

- On Downside Focus: "The investment process must always start by looking down at what can go wrong, rather than looking up at how much money can be made." — Source: Medium

- On Staying in the Game: "The investors who win over decades are the ones who deliberately structure their portfolios to survive the worst possible scenarios." — Source: Institutional Investor

Part 3: Cash, Free Cash Flow, and Financial Valium

- On Financial Valium: "Cash is the equivalent of financial Valium; it keeps you cool, calm, and collected when everyone else is panicking." — Source: Hedge Fund Alpha

- On Optionality: "Maintaining high cash levels—often double digits—provides the exact wherewithal needed to take focused positions when liquidity dries up." — Source: WealthTrack

- On Counting the Cash: "You should ignore accounting gimmicks and focus strictly on free cash flow, which is the only money actually left in the till." — Source: Dataroma

- On Complex Valuations: "If you cannot value a business using sixth-grade math on the back of a postcard, you should pass on the investment." — Source: Economic Times

- On Distributable Cash: "The true measure of a company is how much cold, hard cash it can send to its owners without impairing its own operations." — Source: The Investor's Podcast

- On Equities as Bonds: "A common stock can be viewed as a junior bond where the free cash flow represents the coupon with no maturity date." — Source: Hedge Fund Alpha

- On the Illusion of Clicks: "When companies start measuring success by clicks that doesn't compute to us, the only thing that computes to us is cash." — Source: Gracious Quotes

- On Cash vs. Drag: "Cash is only a drag on returns in a bull market; in a bear market, the value of cash increases exponentially when no one else has it." — Source: Marram LLC

- On Capital Requirements: "Avoid businesses that require massive, continuous capital expenditures just to stand still; prefer those that generate excess cash naturally." — Source: WealthTrack

Part 4: Concentration vs. Diversification

- On Non-Diversification: "We're non-diversified. We focus. Why not buy more of your best idea rather than your 60th best idea?" — Source: QuoteFancy

- On Knowing the Business: "How many companies can I really know well over time and focus on, on a daily basis?" — Source: Gracious Quotes

- On the Risk of Diversification: "Diversification can actually increase risk if it forces an investor to buy mediocre businesses they do not fully understand just to fill out a portfolio." — Source: Medium

- On Superior Knowledge: "Concentrated investing implies less risk of permanent loss as long as you maintain superior knowledge about the companies you own." — Source: Economic Times

- On Extreme Conviction: "It is perfectly rational to hold upwards of 80% of a portfolio in a single asset, like St. Joe, if the research proves it is significantly undervalued and safe." — Source: WealthTrack

- On Ignoring Categories: "Do not diversify merely to check a box for large-cap, small-cap, or sector exposure; invest purely where the economics make sense." — Source: Invest Wizardry

- On Handling Mistakes: "When you run a concentrated portfolio, your mistakes will be glaring and painful, which forces a much higher standard of initial research." — Source: The Business Brew

- On the Index Mindset: "Most mutual funds are essentially closet indexers charging high fees; true outperformance requires radically diverging from the index weights." — Source: Forbes

- On Monitoring the Basket: "It is much easier to watch a few eggs in one basket with intense scrutiny than to keep track of a hundred eggs scattered everywhere." — Source: Institutional Investor

Part 5: "Kill the Company": Inversion and Stress Testing

- On the Murder Board: "We try every which way to kill our best ideas. If we can't kill it, maybe we're on to something." — Source: Economic Times

- On Inversion: "Do not start by looking for reasons to buy a stock; start by actively hunting for reasons to reject it." — Source: Dataroma

- On Stress Testing: "Assume the worst-case macroeconomic scenario—spiking interest rates, severe recessions—and see if the balance sheet can survive without external help." — Source: Hedge Fund Alpha

- On Hidden Vulnerabilities: "You must dig into the footnotes and look for hidden liabilities, regulatory threats, or off-balance-sheet risks that could instantly sink the thesis." — Source: Forbes

- On Self-Sufficiency: "A company that relies on the kindness of strangers, banks, or the government to survive a panic is an inherently flawed idea that should be killed early." — Source: The Investor's Podcast

- On Being Surprised by Upside: "If you have priced in all the worst-case scenarios and the asset is still cheap, you position yourself to be surprised only by good news." — Source: Finbox

- On Asset Destruction: "Learn from mistakes like Sears: a cash-burning operating business can destroy an underlying asset base faster than a distressed investor can unlock it." — Source: The Business Brew

- On Obvious Flaws: "If it takes complex models to prove why an idea shouldn't be killed, it is probably too fragile to own in a concentrated portfolio." — Source: Medium

- On Confirmation Bias: "The goal of the 'kill the company' exercise is to explicitly fight your own confirmation bias when you fall in love with an investment narrative." — Source: Dataroma

Part 6: Margin of Safety and Deep Value

- On Defining Margin of Safety: "A true margin of safety exists when you buy tangible, productive assets at a massive discount to their liquidation value." — Source: Finbox

- On Distressed Real Estate: "Real estate plays succeed because physical, irreplaceable land provides a solid floor beneath the stock price." — Source: Carver Corporation

- On "Indigestion" Stocks: "Deep value is often found in complex, murky, or legally troubled companies that cause 'indigestion' for institutional investors who cannot hold them." — Source: The Investor's Podcast

- On Paying Less: "The secret to investing is to figure out the value of something—and then pay a lot less." — Source: Medium

- On the Wrapper vs. the Asset: "Bankruptcy is often just a temporary 'wrapper' around a highly productive asset; if the core business is sound, the bankruptcy is an opportunity." — Source: The Investor's Podcast

- On Essential Services: "The best margin of safety is providing a product or service that the economy absolutely needs to function on a daily basis." — Source: Fairholme Capital

- On Avoiding Value Traps: "A low price-to-book ratio is meaningless if the book value is melting away due to poor management or a dying industry model." — Source: The Business Brew

- On Extreme Patience: "You must be prepared to hold deep value investments for several years before the market recognizes the intrinsic value you calculated." — Source: WealthTrack

- On "Fixable Problems": "Focus on companies where the current crisis is a fixable, temporary liquidity issue, not a permanent obsolescence of the core product." — Source: Economic Times

- On Fortress Balance Sheets: "A deep value investment must have a balance sheet strong enough to withstand the time it takes for the turnaround to materialize." — Source: Invest Wizardry

Part 7: Assessing Management and "The Jockey"

- On Partnering with Jockeys: "Investing is about betting on the jockey as much as the horse; you want to silently partner with owner-managers who have a track record of integrity." — Source: Dataroma

- On Skin in the Game: "The best executives treat the company's money like their own because a massive percentage of their personal net worth is tied up in the stock." — Source: Finbox

- On Capital Allocation: "A CEO’s most important job is capital allocation; poor decisions on buybacks or acquisitions can destroy an otherwise sound business." — Source: The Business Brew

- On Surviving Stress: "Look for managers who have successfully navigated extreme economic stress before; peacetime CEOs often fail during financial maelstroms." — Source: Institutional Investor

- On Executive Compensation: "Be wary of management teams that extract heavy compensation while shareholders suffer; true owner-managers align their rewards with shareholder returns." — Source: Fairholme Capital

- On Honesty in Mistakes: "You can trust a jockey who is willing to publicly admit mistakes and pivot, rather than one who defends a failing strategy to protect their ego." — Source: Advisor Perspectives

- On Board Alignment: "Having a seat on the board provides a harsh but necessary look into whether management is truly aligned with reality." — Source: The Business Brew

- On Finding the "Megamind": "An exceptional manager can turn a dying business model into a cash-generating machine through sheer operational discipline and focus." — Source: Institutional Investor

- On Unforced Errors: "The greatest danger a jockey poses is committing 'unforced errors,' such as buying back overvalued stock to boost short-term earnings." — Source: The Business Brew

Part 8: The Psychology of a Contrarian

- On Having Courage: "You have to have the courage of your convictions. That's what you are getting paid for. This is the time when I really earn my money." — Source: Arbor Investment Planner

- On Learning from Bookmaking: "Working as a teenage bookmaker taught me about odds, probabilities, and the perverse psychology of crowds that translates directly to the stock market." — Source: Forbes

- On Success Breeding Failure: "First comes success, then comes failure. Success can breed complacency, causing investors to stop doing the granular research that built their reputation." — Source: Advisor Perspectives

- On Managing Envy: "Greed and envy are the fastest paths to financial ruin; focusing on what others are making will force you out of your circle of competence." — Source: The Investor's Podcast

- On the Limitations of Delegation: "Sometimes it is better to recognize that you are a manager of investments, not a manager of people, and keep your operation small." — Source: The Investor's Podcast

- On Admitting Defeat: "Admitting to investors 'I was wrong' is a necessary psychological reset to stop compounding a losing thesis." — Source: Business Insider

- On the Pain of Deep Value: "Operating as a deep value investor means accepting that you will frequently look foolish to the broader market for extended periods." — Source: Hedge Fund Alpha

- On Ignoring the Macro: "Do not waste psychological energy trying to predict interest rates or macroeconomics; focus solely on the microeconomics of the specific business." — Source: WealthTrack

- On Staying Rational: "The ultimate psychological edge is recognizing that when a crowd is running in panic, they are reacting to emotion, leaving pure math and assets behind for you to buy." — Source: Institutional Investor