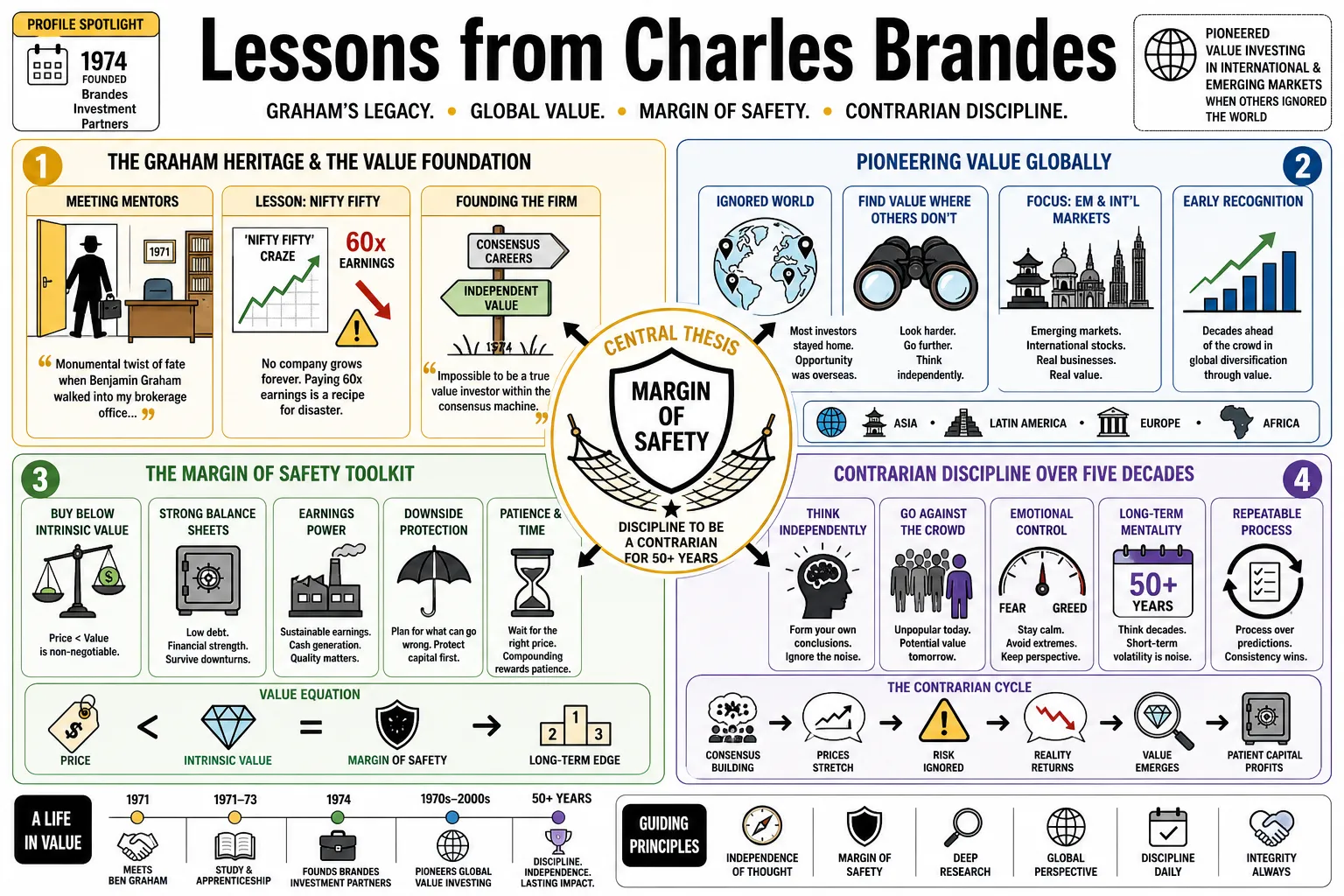

Charles Brandes founded Brandes Investment Partners in 1974 after a chance encounter with Benjamin Graham shaped his entire professional trajectory. He is recognized for pioneering the application of classic value investing principles to international and emerging markets during an era when global diversification was largely ignored. This profile explores his commitment to the "margin of safety" and the psychological discipline required to remain a contrarian over five decades.

Part 1: The Graham Heritage and the Value Foundation

- On Meeting Mentors: "It was a monumental twist of fate when Benjamin Graham walked into my brokerage office in 1971; he was looking for research on a troubled manufacturer and stayed to teach me the essence of value." — Source: Ben Graham Centre Newsletter

- On the Nifty Fifty: "Graham helped me see the danger in the 'Nifty Fifty' craze of the early 1970s, proving that no company grows forever and paying 60 times earnings is a recipe for disaster." — Source: Ivey Business School Lecture

- On the Founding of the Firm: "I started Brandes Investment Partners in 1974 because Graham told me it was impossible to be a true value investor while working within the constraints of a traditional brokerage firm." — Source: Institutional Investor

- On Graham’s Formality: "Benjamin Graham would sit at his desk in a coat and tie even at home, treating the study of securities with the same analytical rigor and respect as a scientist in a laboratory." — Source: Gary Carmell Blog

- On the 75/25 Rule: "Graham taught me to adjust equity exposure based on market levels—holding 75% in stocks when they are cheap and reversing that ratio when they become expensive." — Source: Ivey Business School

- On the 1974 Bear Market: "Launching a value fund during the 1974 crash was terrifying for most, but it provided the cheapest entry points I would see for the next several decades." — Source: Financial Post

- On the Master’s Support: "I keep a framed letter from Graham dated 1974 in my office where he expressed regret for missing our firm's opening, a constant reminder of the discipline he expected." — Source: Brandes Investment Partners

- On the Recovery of 1975: "After the brutal bear market of my firm's founding year, our flagship portfolio gained 75% in 1975, demonstrating how quickly value can be recognized once the panic subsides." — Source: Hendershot Investments

Part 2: The Mechanics of Intrinsic Value

- On Defining Value: "The intrinsic value is the real worth of a business based on its assets and earning power, not what the ticker tape says it is worth at ten o'clock in the morning." — Source: Brandes on Value: The Independent Investor

- On Tangible Assets: "Focusing on tangible book value provides a floor for your investment; it is the physical reality of the business that remains when the hype evaporates." — Source: Value Investing Today

- On the Debt-to-Equity Filter: "To protect against insolvency, we generally look for companies where total debt is less than 100% of tangible equity." — Source: Reddit - Value Investing Today Summary

- On Earnings Yield: "A stock is potentially attractive if its earnings yield is at least twice the yield of a long-term AAA bond, providing a clear premium for the risk of owning equity." — Source: Greenbackd

- On the Current Ratio: "A healthy margin of safety includes a current ratio of at least 2.0, ensuring the company has twice the assets it needs to cover its immediate liabilities." — Source: Value Investing Today

- On Five-Year Performance: "We avoid companies that have sustained a loss at any point in the last five years; consistency is the hallmark of an undervalued business rather than a distressed one." — Source: Reddit - Value Investing Today Summary

- On Earnings Stability: "Value is found in businesses with predictable earning power that has grown by at least 7% annually over a ten-year period." — Source: Value Investing Today

- On Dividend Yield: "A high dividend yield is not enough; it must be supported by low payout ratios and a price that is less than two-thirds of the business's intrinsic worth." — Source: The Brandes Institute

- On Net-Net Investing: "The ultimate value play is buying a company for less than two-thirds of its net current assets, essentially getting the long-term business and fixed assets for free." — Source: Greenbackd

- On Valuation Gaps: "When the gap between the cheapest 10% of stocks and the rest of the market reaches historic highs, the stage is set for a massive rotation back to value." — Source: Brandes Institute Research

Part 3: The Margin of Safety and Risk Management

- On the Margin of Safety: "The margin of safety is the distance between the price you pay and the value you receive; the wider that gap, the more room you have for errors in judgment." — Source: Brandes on Value: The Independent Investor

- On Purchase Price and Risk: "Contrary to modern finance theory, a lower purchase price relative to intrinsic value actually decreases risk while simultaneously increasing potential reward." — Source: QuotesWise

- On Permanent Loss of Capital: "True risk is not a fluctuating stock price; it is the permanent loss of capital that occurs when you overpay for a business or buy a company with failing fundamentals." — Source: Institutional Investor

- On the Zinc Venture Lesson: "A project requiring ten variables to go right, even if each has a 90% probability, has only a 35% chance of overall success; complexity destroys the margin of safety." — Source: Value Investing World

- On Diversification: "Diversification should not be used to mask ignorance; it is a byproduct of finding many uncorrelated companies that each offer an individual margin of safety." — Source: CFA Institute

- On Financial Engineering: "We stay away from financial engineering and complex derivatives because they obscure the actual assets and liabilities of the business we are trying to value." — Source: Institutional Investor

- On Business Simplicity: "If you cannot explain a company’s business model to a ten-year-old in two minutes, it probably doesn't have the transparency required for a value investment." — Source: CleverTalks Speech

- On the Safety Filter: "We eliminate any company with debt exceeding twice its net current assets, ensuring that even in a liquidation scenario, the principal is largely protected." — Source: Value Investing Today

- On Valuation Accuracy: "No valuation is perfect, which is why we insist on buying at such a deep discount that even if our estimate of value is off by 20%, we still make money." — Source: CFA Institute

Part 4: Behavioral Economics and the Psychology of the Crowd

- On the Herd Instinct: "Human beings are hardwired to be herd animals, which makes the act of buying when everyone else is selling feel unnatural and physically uncomfortable." — Source: CFA Institute

- On Non-Herd Personalities: "To succeed as a value investor, you must possess a non-herd personality; you have to be comfortable being wrong and alone for long periods." — Source: ValuePickr

- On Human Inefficiency: "Market inefficiency is just a polite way of describing human inefficiency; people overreact to temporary bad news and create the bargains we seek." — Source: Brandes on Value: The Independent Investor

- On Extrapolation Bias: "Investors consistently make the mistake of believing that a company's recent high growth will continue indefinitely, leading them to pay absurd prices for 'glamour' stocks." — Source: The Brandes Institute

- On the Goalie Analogy: "Goalies who stay in the center stop more balls, yet 94% dive because they feel they must 'do something'; investors suffer from the same bias toward action over results." — Source: Ivey Business School Lecture

- On Overoptimism: "The crowd is always too optimistic during booms and too pessimistic during busts, which is why the most profitable path is usually the opposite of the popular one." — Source: Brandes on Value: The Independent Investor

- On Anchoring: "Investors often anchor their expectations to the highest price a stock has ever reached, failing to see that the underlying business value has changed." — Source: The Brandes Institute

- On Hindsight Bias: "In a bull market, everyone believes they knew exactly what was going to happen, which breeds a dangerous overconfidence that leads to speculative excess." — Source: Brandes on Value: The Independent Investor

- On Objectivity: "Maintaining an objective distance from the 'market noise' and consensus thinking is the only way to retain the clarity needed to buy out-of-favor stocks." — Source: CFA Institute

Part 5: Navigating Market Volatility and "Mr. Market"

- On Welcoming Volatility: "Volatility is not your enemy; it is the source of your opportunity. Without the fluctuations of 'Mr. Market,' there would be no bargains to buy." — Source: Financial Post

- On the Falling Knives Study: "Companies whose prices drop 60% often feel like falling knives, but our research showed these messy situations outperform the market by 18% over three years." — Source: Wikipedia - Charles Brandes

- On Fire-Sale Prices: "You should view market crashes the same way you view a department store sale; when the prices go down, it is time to buy more, not run for the exit." — Source: Value Investing Today

- On Reversion to the Mean: "Profits eventually revert to the mean; companies that are earning too much will see competition eat their margins, and those earning too little will recover." — Source: The Brandes Institute

- On 24-Hour News: "The constant stream of financial news is designed to create anxiety and trigger trades; for a long-term value investor, most of it is completely irrelevant." — Source: CleverTalks Speech

- On Market Misleading: "The stock market is inherently misleading because it reflects the current mood of the participants rather than the future cash flows of the companies." — Source: QuotesWise

- On Price Declines: "For a long-term investor who evaluates price in relation to business value, a price decline is a gift that allows you to lower your average cost." — Source: Value Investing Today

- On Market Inefficiency: "As long as people are prone to fear and greed, the market will remain inefficient enough for value investors to find significant mispricings." — Source: CFA Institute

- On Capitalizing on Panic: "The best time to buy is when there is maximum pessimism; when people are selling out of fear, they stop caring about valuation and just want out." — Source: Financial Post

- On Market Noise: "If you listen too closely to the daily chatter of the market, you will lose the ability to think independently about the long-term value of a business." — Source: Brandes on Value: The Independent Investor

Part 6: The Global Value Opportunity

- On Borderless Value: "Value investing works anywhere in the world; a low P/E ratio is just as attractive in Tokyo or Paris as it is in New York." — Source: Institutional Investor

- On the "Blue Shoes" Lesson: "When my first international client asked if value worked overseas, I told them 'of course'—because the laws of economics don't stop at the border." — Source: Brandes Investment Partners History

- On International Inefficiency: "Foreign markets are often less efficient than the U.S. market, providing even more frequent opportunities to find 'sleeping giants' that are unfairly ignored." — Source: Value Investing Today

- On Emerging Markets Premium: "The value premium in emerging markets has historically been triple what we see in developed markets, rewarding those willing to look past the volatility." — Source: The Brandes Institute

- On ADRs and ORDs: "Using American Depositary Receipts allows domestic investors to access global value without the complexity of opening local brokerage accounts in every country." — Source: Value Investing Today

- On Currency Forecasting: "We do not believe anyone can accurately forecast currencies over the long term, so we focus entirely on the fundamental value of the companies themselves." — Source: Institutional Investor

- On Bottom-Up Analysis: "Global investing should be bottom-up; it is about finding a great business at a great price, regardless of which flag is flying outside their headquarters." — Source: CFA Institute

- On Small-Cap Global Value: "The value effect is most pronounced in smaller international stocks where there is very little analyst coverage and prices often lag behind fundamentals." — Source: The Brandes Institute

- On Global Diversification: "Investing globally provides the ultimate margin of safety by ensuring your portfolio is not dependent on the economic health of any single nation." — Source: International Value Investing (1996)

Part 7: Patience, Time Horizons, and the Business Cycle

- On the 3-5 Year Horizon: "Any holding period shorter than a full business cycle of three to five years is not investing; it is pure speculation." — Source: Investing.com

- On Thinking Like an Owner: "I treat every share like I own the whole company; owners do not sell their business because the price fluctuated 5% on a Tuesday." — Source: Value Investing Today

- On Patience as an Edge: "Patience is a competitive advantage in a world obsessed with quarterly earnings; the market will eventually recognize value, but it won't do it on your schedule." — Source: CFA Institute

- On Dividend Reinvestment: "For long-term investors, reinvesting dividends is the single most important factor for compounding wealth, often accounting for 60% of total returns." — Source: The Brandes Institute

- On the 20-Year Rule: "Over rolling 20-year periods, dividend income has historically provided the vast majority of real returns for disciplined equity investors." — Source: The Brandes Institute

- On Avoiding Speculation: "Speculation is buying something because you hope the price will go up; investing is buying something because the fundamentals prove it is worth more than the price." — Source: Brandes on Value: The Independent Investor

- On Compounding Power: "The power of compounding is a back-end loaded phenomenon; the greatest gains occur in the final years of a long-term holding period." — Source: The Brandes Institute

- On Waiting for the Turn: "Value stocks can stay out of favor for years, but when the turn comes, the recovery is often so fast that you cannot afford to be out of the market." — Source: Financial Post

- On Inaction as Strategy: "Sometimes the best thing you can do for your portfolio is absolutely nothing; constant trading is usually just a way to pay more in taxes and fees." — Source: Ivey Business School Lecture

- On Business Life Cycles: "Companies go through seasons; a value investor buys during the winter of a company's cycle and waits for the inevitable return of spring." — Source: Brandes on Value: The Independent Investor

Part 8: The Independent Mindset and the Path of the Contrarian

- On Independence: "If you are not different from the majority in the way you think, it is mathematically impossible for you to achieve better-than-average results." — Source: Brandes on Value: The Independent Investor

- On Being a Contrarian: "I have always been a contrarian; going with the crowd has never been a concern of mine if my head and my research lay elsewhere." — Source: Financial Post

- On the Airline Rule: "I once told my team to never buy an airline, but they ignored me and we made money on some and lost on others; flexibility is as important as discipline." — Source: ValuePickr

- On Forecasting Rejection: "We reject macroeconomic forecasting because the future is unpredictable; we prefer to base our decisions on the tangible assets we can see today." — Source: Institutional Investor

- On Analytical Rigor: "Fundamentals. Fundamentals. Fundamentals. There is no substitute for doing the hard work of reading annual reports and understanding the balance sheet." — Source: Financial Post

- On the Independent Path: "The path of the independent investor is lonely, but it is the only one that leads to true wealth creation that lasts through multiple market cycles." — Source: Brandes on Value: The Independent Investor

- On Rejection of Formulas: "Successful value investing is not just a formula you plug into a computer; it requires the judgment to know when a cheap stock is a bargain and when it is a trap." — Source: CFA Institute

- On Longevity: "The principles of value investing haven't changed in a century and they won't change in the next one because they are based on human nature and math." — Source: Value Investing Today

- On the Goal of Investing: "The ultimate goal is not to beat a benchmark every quarter, but to build substantial wealth for clients while protecting their principal at every turn." — Source: CleverTalks Speech