Lessons from Cliff Asness

Cliff Asness co-founded AQR Capital Management to turn academic finance theories into practical trading strategies. He built his reputation by proving that combining value and momentum investing works better than relying on either approach alone. Beyond building quantitative models, Asness is known for calling out the manufactured stability of private equity and detailing the stubborn discipline required to survive the markets.

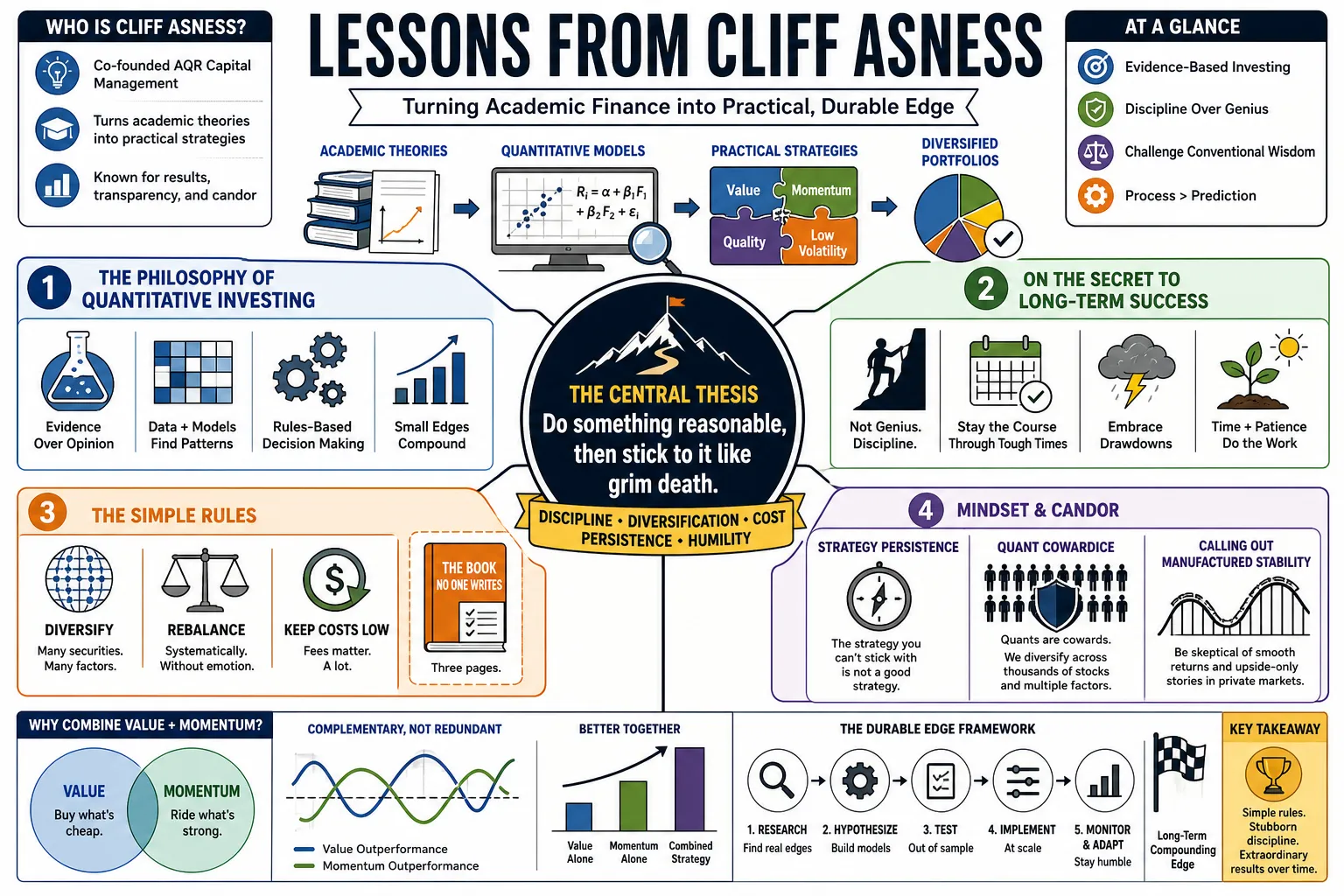

Part 1: The Philosophy of Quantitative Investing

- On the Secret to Long-Term Success: "I used to think that being great at investing long-term was about genius... more and more I think it's about doing something reasonable, that makes sense, and then sticking to it like grim death through the tough times." — Source: Masters in Business

- On the Simple Rules: "The rules are quite simple: Diversify. Rebalance. Keep costs low. There aren't many others. But no one writes that book because it's three pages." — Source: AQR Perspectives

- On Strategy Persistence: "The strategy you can't stick with is not a good strategy." — Source: Twitter/X

- On Quant Cowardice: "Quants are cowards. We diversify across thousands of stocks and multiple factors rather than betting on a single gut feeling." — Source: Forbes

- On Indexing: "Market-cap based indexing will never be driven from its deserved perch as core and deserved king of the investment world. It is what we should all own in theory." — Source: AQR Perspectives

- On Intellectual Honesty: "If you have a three-year period where something doesn't work, it ages you a decade. You face an immense pressure to change your models... I cannot really convey the amount of discipline you need." — Source: Invest Like the Best

- On Data over Story: "Keep an open mind, but not so much that your brains fall out." — Source: CFA Institute

- On Factor Investing: "We don't buy companies; we buy attributes. Value, momentum, carry, and quality are the pillars." — Source: Masters in Business

- On Adapting to Markets: "You have to be willing to change your mind when the data changes, but not so gullible that you chase every new trend without a first-principles understanding." — Source: Invest Like the Best

- On the Perfect Portfolio: "The ideal approach is not to find a single perfect asset, but a collection of uncorrelated positive expected return streams." — Source: AQR Research

Part 2: Value and Momentum

- On the Core Premise: "Value is buying what's cheap based on fundamentals; momentum is buying what's going up. Both work, but together they are magic." — Source: University of Chicago Dissertation

- On Negative Correlation: "Value and momentum are beautifully negatively correlated. When value is having a terrible time, momentum often helps carry the portfolio, and vice versa." — Source: Conversations with Tyler

- On Momentum's Insanity: "A momentum investing strategy is the rather insane proposition that you can buy a portfolio of what's been going up... sell what's been going down... and you beat the market. Unfortunately for the case of sanity, that seems to be true." — Source: AQR Perspectives

- On the Holy Grail: "Combining value and momentum creates a much smoother Sharpe ratio than using either one alone." — Source: Masters in Business

- On Value's Pain: "Value investing is simple to understand but agonizing to execute, because you are constantly buying what everyone else hates." — Source: Rational Reminder Podcast

- On Timing Factors: "Timing factors is a sin. It's extremely difficult to know exactly when value will rotate back into favor, so it's better to hold both through the cycles." — Source: Bloomberg Wealth

- On the 2018-2020 Value Drawdown: "We analyzed the data to see if value was never going to work again but concluded the world had simply gone crazy." — Source: Bloomberg Wealth

- On Defining Value: "Price-to-book was the original metric, but true quant value uses a robust set of indicators like P/E and cash flow to avoid value traps." — Source: AQR Research

- On Behavioral Momentum: "Momentum is hard to explain rationally and likely stems from behavioral biases like underreaction to news initially, and overreaction later." — Source: Conversations with Tyler

Part 3: Market Inefficiency and Behavioral Biases

- On the Less-Efficient Market: "Markets have actually become less efficient over the last 30 years due to social media and the gamification of trading." — Source: The Less-Efficient Market Hypothesis

- On Bubble Logic: "The term bubble should indicate a price that no reasonable future outcome can justify." — Source: AQR Perspectives

- On Cash on the Sidelines: "Every time someone says, 'There is a lot of cash on the sidelines,' a tiny part of my soul dies. There are no sidelines... every buyer bought from a seller who now holds the cash." — Source: Twitter/X

- On Single Stock Bubbles: "A single stock can't be in a bubble. Bubbles require a broader systemic delusion." — Source: Twitter/X

- On Efficiently Inefficient Markets: "Markets are not perfectly efficient, but they are efficiently inefficient. They are just inefficient enough that professional managers can earn a profit to cover their costs." — Source: AQR Research

- On Social Media's Impact: "Has there ever been a better vehicle for turning a wise, independent crowd into a coordinated clueless even dangerous mob than social media?" — Source: Twitter/X

- On Human Nature: "The market is a reflection of human nature, and human nature does not change just because we have faster computers." — Source: Masters in Business

- On Overreaction: "People extrapolate recent trends too far into the future, which is why value works. They think the bad news will last forever." — Source: Conversations with Tyler

- On Mispricings: "Mispricings can last for years, making alpha strategies incredibly painful to stick with." — Source: The Less-Efficient Market Hypothesis

- On the Straw Man: "The idea that markets are perfectly efficient is a straw man. Even my mentor Eugene Fama admits they aren't perfect." — Source: Capitalisn't Podcast

Part 4: Risk Management and Diversification

- On the Buffet Analogy: "Investing without diversification is like going to a buffet and only eating dessert—satisfying in the short term but disastrous in the long term." — Source: AQR Perspectives

- On Worst-Case Scenarios: "You've got to guess at worst cases: No model will tell you that. My rule of thumb is double the worst that you have ever seen." — Source: Invest Like the Best

- On Pulling the Goalie: "The hockey coach who pulls his goalie down 0-2 with ten minutes to go and loses 0-5 will face harsh criticism. Commit the sin and risk losing ugly when the math dictates it." — Source: Excess Returns Podcast

- On Global Diversification: "Global diversification to us is about the chance that it turns out that your country is the world's basket case." — Source: The Meb Faber Show

- On Volatility: "Not marking something doesn't make it low risk. It just makes it unpriced." — Source: AQR Perspectives

- On Bonds as Diversifiers: "Bonds are a great diversifier until they aren't. When inflation is the shock, stocks and bonds go down together." — Source: The Meb Faber Show

- On True Risk: "Risk is not volatility. True risk is the permanent loss of capital or failing to meet your long-term objectives." — Source: Rational Reminder Podcast

- On Leverage: "Leverage is neither good nor bad. It is a tool. Used on a highly diversified, low-risk portfolio, it can be safer than a concentrated, unlevered equity portfolio." — Source: AQR White Papers

- On the Danger of Comfort: "If your portfolio makes you completely comfortable, it is probably dangerously undiversified." — Source: Masters in Business

Part 5: Hedge Funds and Fees

- On Asness's Law of Fees: "If I ever get an economic law named after me I want it to be: 'There is no investment product so good gross, that there isn't a fee that could make it bad net.'" — Source: Rational Reminder Podcast

- On Hedge Fund Reality: "Hedge funds are investment pools that are relatively unconstrained... charge very high fees, will not necessarily give you your money back when you want it, and will generally not tell you what they do." — Source: AQR Perspectives

- On Alpha Fees for Beta: "I think a tremendous amount of the private world, and hedge funds, are charging massive alpha fees for beta." — Source: Bloomberg Money Stuff Podcast

- On 2 and 20: "Charging a 2 and 20 fee on the portion of returns that comes from the market simply going up is highway robbery." — Source: Hedge Fund Alpha

- On What to Pay For: "Investors should only pay high fees for pure alpha—returns that are truly uncorrelated with the stock market." — Source: Morningstar Podcast

- On the 100-Year Flood: "Every three or four years, hedge funds deliver a one-in-a-hundred year flood." — Source: AQR Perspectives

- On Mutual Funds vs. Hedge Funds: "A hedge fund that doesn't hedge is just an expensive mutual fund." — Source: Hedge Fund Alpha

- On the Cost of Efficiency: "Hedge fund fees are the cost of keeping the market efficient. If fees were too low, the profit would vanish; if too high, no one would trade." — Source: Efficiently Inefficient

- On Evaluating Managers: "If a manager's returns look exactly like the S&P 500 but with a 2% fee, fire them." — Source: Masters in Business

Part 6: The Reality of the Markets

- On Volatility Laundering: "The amount people will pay to an industry to make decently less than a moderately levered S&P 500 index fund, so they don't have to watch the S&P 500 index fund, is staggering." — Source: Twitter/X

- On Illiquidity as a Feature: "If I'm right that people love the fact that they don't have to look at the volatility, that means illiquidity is no longer a bug, it is now a feature." — Source: Bloomberg Money Stuff Podcast

- On Private Equity: "Never have so many paid so much to so few for the privilege of being told so little." — Source: Institutional Investor

- On the Mirage of Stability: "It's a mathematical fact that I resent... The low volatility of private equity is nothing but a mirage." — Source: Morningstar Podcast

- On Public vs. Private Markets: "If we were private equity, none of the panic during our lean years would have happened because we simply wouldn't have reported the drop." — Source: Morningstar Podcast

- On the Negative Illiquidity Premium: "Investors are so desperate for smooth returns that they overpay for private assets, ultimately accepting lower returns than they could get in public markets." — Source: AQR Blog

- On Accounting Tricks: "Volatility laundering is the act of using infrequent valuations to hide the actual risk and price swings of investments." — Source: Institutional Investor

- On Smoothing Returns: "The preference for illiquid, infrequently priced assets that don't smash you in the face with their volatility is a powerful behavioral crutch." — Source: AQR Blog

- On True Reality: "The market marks public equities every second. Private markets mark them when it's convenient. Reality doesn't care about your accounting schedule." — Source: Masters in Business

Part 7: Career and Building AQR

- On Leaving Goldman Sachs: "We wanted to take rigorous academic theories and apply them to real-world trading independently. That was the genesis of AQR." — Source: Masters in Business

- On Launching during LTCM: "We launched AQR just as the Long-Term Capital Management crisis hit, which made for a hair-raising start as our quant strategies briefly decoupled." — Source: Invest Like the Best

- On Publish or Perish: "Our culture is more like a university than a traditional bank. We believe in intellectual honesty and publishing our research." — Source: CFA Institute

- On the Portfolio of a Career: "Don't over-index on a single bad meeting or project. Look at your career as a 30-year portfolio. If the total portfolio trends upward, line-item failures are noise." — Source: Invest Like the Best

- On Early Failure: "I was an underachiever in high school. Your early performance is not a permanent ceiling if you find a field that engages your inner geek." — Source: 25iq

- On Communication: "In an increasingly automated world, the ability to explain why something is happening, and to build trust through that explanation, is your most valuable currency." — Source: Bloomberg Wealth

- On Independence: "AQR was built on the belief that transparency and rigorous data analysis would ultimately win out over Wall Street salesmanship." — Source: Rational Reminder Podcast

- On Enduring the Tough Times: "Building a firm means surviving the drawdowns. The professionals who survive are those who don't abandon their core principles under pressure." — Source: Invest Like the Best

- On the Team: "You cannot build a quantitative firm alone. It requires a symphony of researchers, traders, and business builders who share the same empirical religion." — Source: Masters in Business

Part 8: Life, Opinions, and Miscellaneous Advice

- On Twitter Feuds: "99% of my tweets are about fintwit or stupid humor. 1% of the time after starting out reasonable and being treated unreasonably I get mad. I should do better." — Source: Twitter/X

- On Success Theater: "Just because a billionaire takes an ice bath doesn't mean the ice bath made them a billionaire. Focus on your actual work, not mimicking superficial habits." — Source: Invest Like the Best

- On Misattributed Quotes: "If you dare attribute a quote without a qualifier, trolls attack you because it was really said by Alexander Pushkin or Colonel Sanders." — Source: Twitter/X

- On Disconnecting: "My wife gave me the best advice: 'Stop looking at the screen. You'll be a happier man.'" — Source: Masters in Business

- On Dealing with Critics: "I find posturing fools beyond concerning. Bye bye." — Source: Twitter/X

- On Nassim Taleb: "You can deadlift all you want my still chubby friend, you are a bad, nasty, overrated man, and you are without honor." — Source: Twitter/X

- On Humor in Finance: "Finance is a dry subject. I put humor in my footnotes because if I don't laugh while writing this stuff, I'll cry." — Source: Masters in Business

- On "Ka nama kaa lajerama": "It's a Conan the Barbarian reference. It means facing impossible odds without surrender, which is exactly how market drawdowns feel." — Source: Invest Like the Best

- On Embracing the Geek: "Don't apologize for being a nerd about your profession. Obsession is the only way to survive the grind." — Source: 25iq

- On the Ultimately Unknowable: "We build models to understand the world, but we must always respect that the market is a complex, adaptive system that will occasionally break our models." — Source: AQR Perspectives