Lessons from Cliff Sosin

Cliff Sosin founded CAS Investment Partners, an investment firm known for its highly concentrated portfolio. He built his track record on primary field research into unit economics and a willingness to hold core positions through severe drawdowns. The notes below outline his approach to evaluating businesses and managing risk.

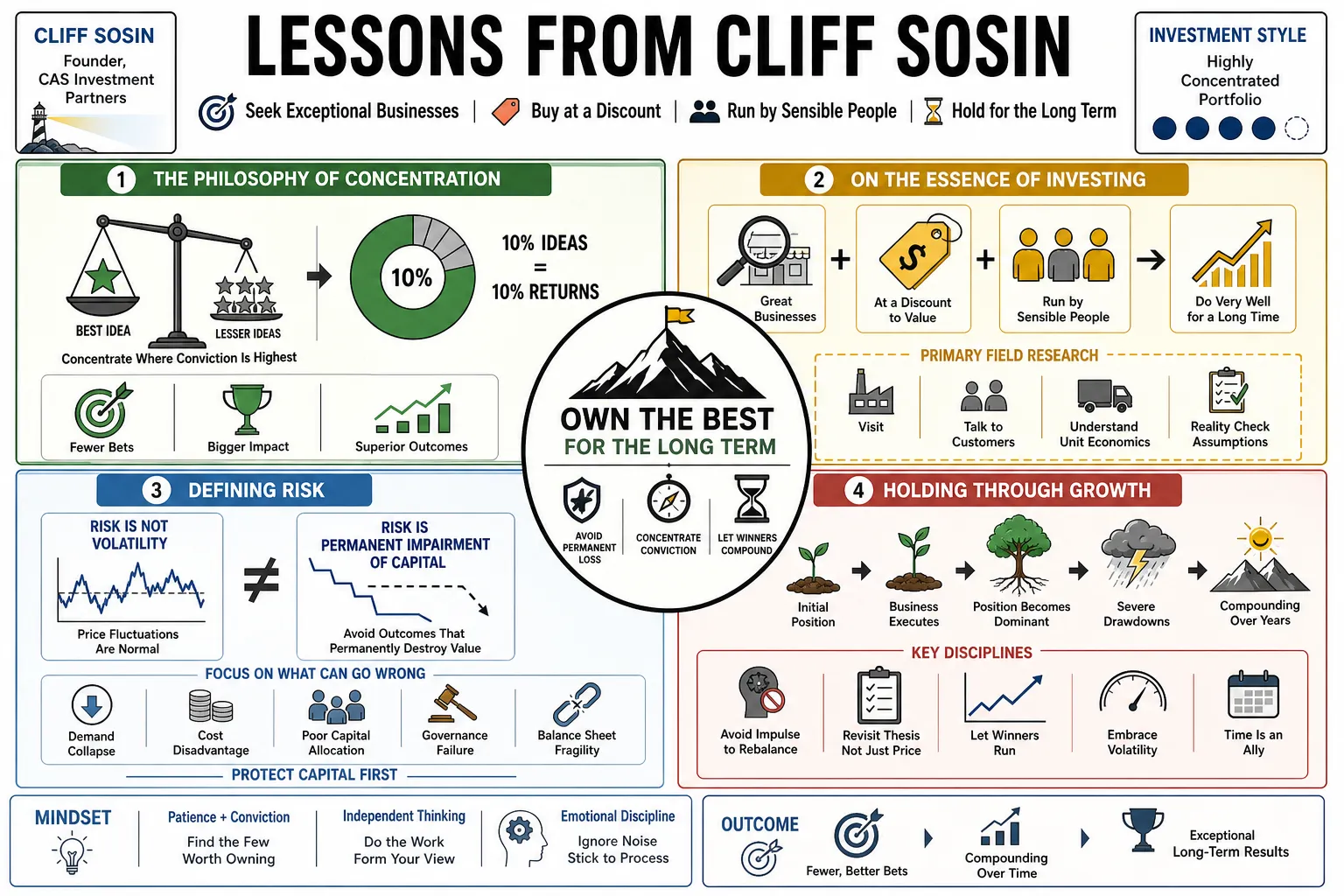

Part 1: The Philosophy of Concentration

- On the Essence of Investing: "I'm looking for businesses that are going to do very well for a very long time, that I can get at a price that doesn't reflect that, that are run by sensible people. I don't think there's anything more to it than that." — Source: Good Investing Interview

- On Dilution of Ideas: "Your best idea is inherently better than your tenth best idea, so allocating capital away from your highest conviction bet to a lesser one diminishes returns." — Source: Capital Allocators

- On Defining Risk: "Risk is not volatility; risk is a permanent impairment of capital in an underlying business." — Source: CAS Investment Partners Letter

- On Holding Through Growth: "Allowing a successful investment to become a dominant position in the portfolio requires avoiding the temptation to blindly rebalance." — Source: Invest Like the Best

- On Sizing: "Position sizing should reflect the magnitude of the asymmetry and the depth of your conviction, not a predetermined target weight." — Source: Yet Another Value Podcast

- On Diversification: "Over-diversification often masks a lack of true understanding about the businesses you own." — Source: MOI Global

- On Opportunity Cost: "Every new investment must be measured against the future compounding potential of what you already hold." — Source: CAS Investment Partners Letter

- On Finding Outliers: "Truly exceptional businesses are rare; when you find one, you should own enough of it to matter." — Source: Good Investing Interview

- On Portfolio Structure: "A concentrated portfolio forces an investor to conduct much more rigorous due diligence before making an allocation." — Source: Capital Allocators

Part 2: Seeking Ground Truth

- On Scuttlebutt: "Talking to people who worked at, competed with, or are customers of the companies that you're studying is definitely, by far the best way that I found to get a sense of how things actually work on the ground." — Source: Good Investing Interview

- On Financials vs. Reality: "Financial statements tell you what happened in the past; field research tells you why it happened and whether it can continue." — Source: Yet Another Value Podcast

- On Primary Research: "You cannot outsource the work of understanding a company's culture and operational cadence." — Source: Invest Like the Best

- On Customer Behavior: "Observing how customers interact with a product often reveals more about unit economics than the management's presentation deck." — Source: Good Investing Interview

- On Employee Perspectives: "Former employees are often the most accurate source of a company's unvarnished operational strengths and weaknesses." — Source: Capital Allocators

- On Competitive Dynamics: "The true test of a business moat is found in how difficult it is for a well-funded competitor to steal a single customer." — Source: MOI Global

- On Discarding Noise: "Most daily market news is irrelevant to the structural reality of the businesses you are studying." — Source: CAS Investment Partners Letter

- On Validating Claims: "Whenever a company claims an operational advantage, you must find a way to independently verify it in the physical world." — Source: Invest Like the Best

- On First-Hand Experience: "Using the product yourself is a necessary prerequisite to modeling its long-term adoption curve." — Source: Good Investing Interview

- On Synthesis: "The edge in investing comes from synthesizing hundreds of minor observations into a singular, accurate view of the business reality." — Source: Capital Allocators

Part 3: Enduring Market Volatility

- On Drawdowns: "The simple fact is stocks do not rise in straight lines. We are in the midst of one of the more substantial drawdowns... That these sorts of drawdowns are to be expected and are a normal part of investing over the long term does not make them fun." — Source: CAS Investment Partners Letter

- On Mark to Market Contradictions: "There is something contradictory about an investment partnership premised on the idea that market prices are wrong, measuring its gains and losses based on market pricing." — Source: CAS Investment Partners Letter

- On Price vs. Value: "A declining share price only alters the intrinsic value of a business if that business relies on capital markets to fund its operations." — Source: Yet Another Value Podcast

- On Volatility as a Toll: "Emotional distress during drawdowns is simply the price of admission for long-term compounding." — Source: Invest Like the Best

- On Overcoming Panic: "When a stock drops severely, the initial reaction should be to revisit the original thesis, not to sell out of fear." — Source: MOI Global

- On Market Perception: "The market frequently extrapolates temporary operational hiccups as permanent structural failures." — Source: Good Investing Interview

- On Holding Periods: "A true long-term horizon means accepting that you will occasionally look foolish for extended periods." — Source: Capital Allocators

- On Averaging Down: "Adding to a position during a drawdown is only rational if the underlying unit economics have remained intact or improved." — Source: Invest Like the Best

- On Retrospective Clarity: "It is my observation from business history that few great businesses are built without mistakes, setbacks and challenges. In retrospect, these challenges appear obviously soluble... In the moment, however, they can appear insurmountable." — Source: CAS Investment Partners Letter

Part 4: Evaluating Management and Culture

- On Ideal Managers: "Look for leaders who are smart, energetic, honest, humble, and good capital allocators." — Source: Medium Profile

- On Humility: "A management team that openly admits mistakes is far less likely to destroy capital to protect their ego." — Source: Good Investing Interview

- On Capital Allocation: "The primary job of a CEO is deciding how to deploy the cash the business generates." — Source: MOI Global

- On Cultural Durability: "A strong internal culture is a massive competitive advantage because it reduces friction and accelerates problem-solving." — Source: Capital Allocators

- On Incentive Structures: "How employees are compensated tells you exactly what the business actually values." — Source: CAS Investment Partners Letter

- On Founder-Led Companies: "Founders often possess a long-term orientation and risk tolerance that hired executives lack." — Source: Invest Like the Best

- On the Operator Mindset: "You want managers who are obsessed with the granular details of their product, not just their stock price." — Source: Yet Another Value Podcast

- On Integrity: "If a management team is willing to mislead investors on small issues, they will eventually mislead them on large ones." — Source: Good Investing Interview

- On Energy: "Building a disruptive business requires an extraordinary, sustained level of energy from its leadership team." — Source: Capital Allocators

Part 5: Loyalty Economics and Unit Economics

- On Loyalty Economics: "Businesses that systematically retain their customers experience compounding advantages in lower acquisition costs." — Source: MOI Global

- On Customer Acquisition: "The true cost of acquiring a customer must be measured against the lifetime gross profit they generate." — Source: Invest Like the Best

- On Hidden Moats: "High customer retention is often the mathematical byproduct of a superior customer experience." — Source: Yet Another Value Podcast

- On Operating Leverage: "A business model is only truly attractive if incremental revenue generates disproportionately higher margins." — Source: CAS Investment Partners Letter

- On Logistics as a Moat: "Building physical infrastructure and logistics networks creates a barrier to entry that software alone cannot replicate." — Source: Invest Like the Best

- On Friction Reduction: "Companies that remove friction from legacy consumer transactions often capture massive market share." — Source: Good Investing Interview

- On Cohort Analysis: "Evaluating the behavior of customer cohorts over time is the most accurate way to project future revenue." — Source: Capital Allocators

- On Scale Advantages: "True scale advantages occur when a company's per-unit costs decline continuously as their volume increases." — Source: Yet Another Value Podcast

- On Pricing Power: "A business with true loyalty can selectively raise prices without suffering a corresponding drop in volume." — Source: CAS Investment Partners Letter

- On Local Economics: "National scale is often just a collection of highly profitable, localized unit economic models." — Source: Invest Like the Best

Part 6: Hypothesis Testing and Conviction

- On Disproving Ideas: "The goal of research is not to confirm your initial bias, but to actively try to break your own investment hypothesis." — Source: Substack Analysis

- On Conviction Building: "True conviction is forged only after you have understood and refuted the best arguments against your position." — Source: Capital Allocators

- On Updating Priors: "When new, contradictory information arises, you must be willing to adjust your models immediately." — Source: Good Investing Interview

- On Intellectual Honesty: "Admitting you are wrong early saves capital; defending a broken thesis destroys it." — Source: MOI Global

- On Contrarianism: "You do not make outsized returns by agreeing with the consensus; you make them by being correct when the consensus is wrong." — Source: Invest Like the Best

- On Thesis Drift: "Be wary of changing the reasons you own a stock simply to justify a declining share price." — Source: CAS Investment Partners Letter

- On the Null Hypothesis: "Assume the market is pricing the asset correctly until you have overwhelming evidence to the contrary." — Source: Yet Another Value Podcast

- On Information Asymmetry: "Your edge comes from a deeper understanding of the qualitative factors, not from having faster access to data." — Source: Good Investing Interview

- On Independent Thinking: "You must physically separate yourself from the noise of Wall Street to maintain independent thought." — Source: Capital Allocators

Part 7: Mental Models and Psychological Fortitude

- On Inversion: "Figure out what would kill the business, and then determine how likely that scenario actually is." — Source: Invest Like the Best

- On Second-Order Effects: "Always ask what the consequence of a consequence will be, especially regarding technological disruption." — Source: Good Investing Interview

- On Patience: "Action for the sake of action is the enemy of compounding." — Source: CAS Investment Partners Letter

- On Cognitive Biases: "Acknowledging your own susceptibility to psychological biases is the first step in mitigating them." — Source: Capital Allocators

- On Stamina: "The hardest part of value investing is the stamina required to sit on your hands and do nothing." — Source: MOI Global

- On Rationality: "You must divorce your emotional state from the daily fluctuations of your portfolio." — Source: Yet Another Value Podcast

- On Simplicity: "If a business model requires a 100-tab spreadsheet to understand, it is probably too fragile to invest in." — Source: Good Investing Interview

- On Probabilistic Thinking: "Investing is about assigning probabilities to future outcomes, not seeking absolute certainty." — Source: CAS Investment Partners Letter

- On Dealing with Criticism: "When you hold a highly concentrated, contrarian position, you must be comfortable looking like an idiot to your peers." — Source: Invest Like the Best

- On Focus: "Dedicate your cognitive load to understanding the few variables that actually matter to the business's long-term success." — Source: Capital Allocators

Part 8: Long-Term Horizons and Value Creation

- On Compounding: "The math of compounding demands that you leave the capital alone for as long as the business continues to execute." — Source: Invest Like the Best

- On Horizon Arbitrage: "The market's obsession with the next quarter creates mispricings for investors willing to look five years ahead." — Source: Yet Another Value Podcast

- On Value Creation: "A business only creates value if its return on invested capital exceeds its cost of capital." — Source: MOI Global

- On Disruption: "Incumbents rarely survive a platform shift because their incentive structures prohibit them from cannibalizing their existing profits." — Source: Good Investing Interview

- On Reinvestment Rates: "The best businesses can reinvest large amounts of their own cash flow back into the business at high rates of return." — Source: Capital Allocators

- On Margin Expansion: "In disruptive businesses, current margins are often artificially depressed by the heavy investments required for future growth." — Source: Invest Like the Best

- On Enduring Franchises: "A business that consistently delivers superior value to the consumer will inevitably capture a larger share of the profit pool." — Source: CAS Investment Partners Letter

- On the Passage of Time: "Time is the friend of the wonderful company and the enemy of the mediocre one." — Source: Good Investing Interview

- On Ultimate Success: "Investment success is not about trading well; it is about partnering with exceptional businesses and letting them do the heavy lifting over decades." — Source: Yet Another Value Podcast