Lessons from David Bonderman

David Bonderman built TPG Capital by diving into the distressed corporate messes that most investors avoid. Since saving Continental Airlines in 1993, he has treated legal and structural complexity as a moat rather than a deterrent. His approach pairs aggressive operational turnarounds with a conviction that solo travel is a prerequisite for independent thinking.

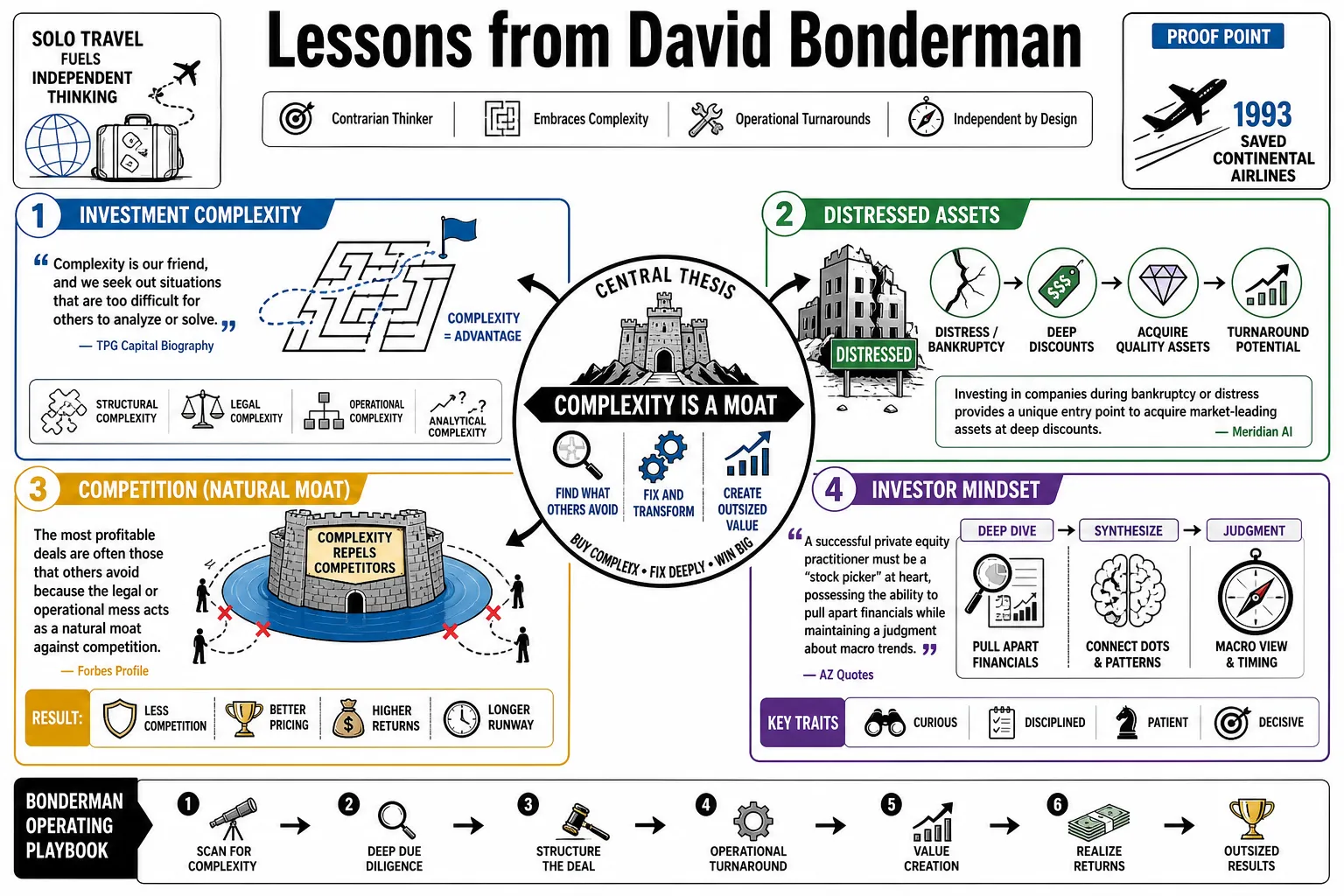

Part 1: Contrarianism and Complexity

- On Investment Complexity: "Complexity is our friend, and we seek out situations that are too difficult for others to analyze or solve." — Source: TPG Capital Biography

- On Distressed Assets: Investing in companies during bankruptcy or distress provides a unique entry point to acquire market-leading assets at deep discounts. — Source: Meridian AI

- On Competition: The most profitable deals are often those that others avoid because the legal or operational mess acts as a natural moat against competition. — Source: Forbes Profile

- On the Investor Mindset: A successful private equity practitioner must be a "stock picker" at heart, possessing the ability to pull apart financials while maintaining a judgment about macro trends. — Source: AZ Quotes

- On Barriers to Entry: Complexity is a competitive advantage; if a deal cannot be sketched on a napkin, it might be too hard for most, which is exactly why it should be pursued. — Source: Silicon Flatirons Interview

- On Risk Appetite: Bonderman was famously described as a "contrarian par excellence," thriving in "complex, ridiculously treacherous transactions" that public markets were too timid to handle. — Source: Financial Post

- On Financial Rigor: The ability to take a company's financials apart to find intrinsic value is the foundation of every successful buyout. — Source: The Harbus Interview

- On "Messy" Deals: Messy corporate spin-offs and regulatory hurdles are opportunities for those with the patience to solve structural puzzles. — Source: TPG Investor Relations

- On Market Inefficiency: "Prices are always lower when the troops are in the street," illustrating the value of buying during periods of peak uncertainty. — Source: Business Insider

- On Information-Light Investing: Bonderman viewed venture capital as "thesis-driven and information-light," preferring the data-rich environment of private equity turnarounds. — Source: Unit Ventures Podcast

Part 2: The Art of the Turnaround

- On the Continental Model: The $66 million investment in the twice-bankrupt Continental Airlines succeeded by focusing on management and route profitability rather than just cost-cutting. — Source: TPG History

- On Management Fixes: "A good business with a bad management team is fixable; a bad business with a good management team is a harder problem to solve." — Source: Forbes Dealbook

- On Industry Passion: "People fall in love with the airline business... we leave that to the pros," emphasizing the need for financial detachment from the asset. — Source: Los Angeles Times

- On Operational vs. Financial Engineering: Simple leveraged buyouts are a dying strategy; true value comes from in-house operations teams partnering with management to drive growth. — Source: AP News

- On the Ryanair Strategy: Bonderman transformed Ryanair by insisting it list on the NASDAQ to attract U.S. investors who already understood the low-cost carrier model. — Source: The Irish Times

- On "Sticking to Your Knitting": He famously opposed Ryanair's expansion into long-haul flights, arguing that it would dilute the efficiency of their point-to-point European model. — Source: Travel Extra

- On Brand Revitalization: The Ducati deal taught that a world-class brand trapped in a small-company structure can be revitalized by shifting from selling motorcycles to selling a "lifestyle." — Source: Scribd TPG Case Study

- On Burger King: The turnaround at Burger King succeeded by reviving "The King" mascot and improving franchisee relations to restore brand health. — Source: Wikipedia - Burger King Acquisition

- On Operational Discipline: Fleet commonality and secondary airports are not just cost-savers but competitive moats in the airline industry. — Source: Ryanair Corporate Governance

- On Delegating Operations: The role of the investor is to set the parameters and provide the capital, not to attempt to fly the planes. — Source: Semafor

Part 3: Investment Discipline and Macro Strategy

- On Government Divestiture: "When governments are selling, you should be buying," as these transactions are often motivated by political necessity rather than maximum price. — Source: AZ Quotes

- On Market Timing: Private equity historically performs better in bad markets than in good markets due to the availability of distressed pricing. — Source: Milken Institute Global Conference

- On the Retail Apocalypse: Bonderman predicted the decline of physical stores in 2017, noting that the country had more storefronts than the population required. — Source: Business Insider

- On Global Pockets of Opportunity: "Returns tend to be better in places where either the troops are in the street, or the prices are low." — Source: The Irish Times

- On Long-Termism: The greatest strength of private equity is the ability to wait for a company to reach its potential without public market quarterly pressure. — Source: Private Equity International

- On Capital Allocation: "Generally speaking, you like to dance with the girl that brung you, and if you can't sometimes you have to shoot her." — Source: Quotes Wise

- On Industry Reality: "This is a financial services business, it's not brain surgery," highlighting the importance of execution over overly intellectualized theories. — Source: Financial Times

- On Cross-Border Arbitrage: Globalizing Chinese business via deals like Lenovo's acquisition of IBM’s PC division showed that PE could bridge manufacturing and distribution. — Source: TPG Asia History

- On Macro Awareness: Successful investing requires a "nose for value" paired with a deep understanding of where global thematic shifts are heading. — Source: Harbus Interview

- On Resilience: The most resilient business models are those that provide essential services at the lowest possible cost, regardless of economic cycles. — Source: Unit Ventures

Part 4: Operational Excellence and Management

- On Management Red Flags: "If you think you have a management problem, you do," and you should act before the company's value deteriorates. — Source: Forbes

- On Leadership Quality: A bad business with a good management team is often harder to fix than a good business with bad management because the fundamentals are flawed. — Source: AZ Quotes

- On Replacing Management: Do not be afraid to professionalize the leadership early in the investment cycle to ensure operational rigor. — Source: Bloomberg - Bonderman Legacy

- On Relationship Value: Private equity is a small world built on trust; long-term relationships are more valuable than squeezing the last dollar out of a single deal. — Source: TPG Annual Report

- On Delegation Rules: Hire the best management possible, set the strategic guardrails, and then get out of their way. — Source: Semafor Obituary

- On "Proprietary" Deals: Building a reputation for closing complex deals allows a firm to secure proprietary transactions that aren't open to public auction. — Source: TPG Website

- On Growth Partners: Private equity should act as a catalyst for growth-stage companies, providing the capital necessary to scale using commercial rigor. — Source: The Rise Fund Strategy

- On "Low-Hanging Fruit": The era of simple cost-cutting LBOs is over; sustainable returns now require active operational partnership. — Source: Private Equity International

- On Corporate Culture: Establishing a "culture of curiosity" within an investment firm encourages the discovery of non-obvious opportunities. — Source: Washington Education Blog

Part 5: Lessons from Legendary Deals

- On Seagate's Structural Arbitrage: Separating a "high-flying" volatile asset from a "steady-eddy" core business can unlock hidden shareholder value. — Source: Github - Seagate Analysis

- On the J.Crew Trapdoor: Moving intellectual property into a subsidiary can protect assets from creditors but risks leaving the company with unsustainable debt. — Source: Forbes - J.Crew Bankruptcy

- On Uber as a Disruptor: Early investments in technology "disruptors" like Uber and Airbnb represented a pivot for TPG toward high-growth, venture-style bets. — Source: Bloomberg

- On Lenovo's Global Synergy: Using IBM's established enterprise sales network to push low-cost hardware was a landmark in cross-border revenue synergy. — Source: TPG - Lenovo Case Study

- On Ducati Lifestyle: By expanding a brand into apparel and accessories, a niche product can become a "cult-like" global lifestyle brand. — Source: Federico Minoli Memoirs

- On Petco and Consumer Trends: Success in pet retail was driven by the "humanization of pets" trend and shifting consumer spending toward premium services. — Source: Forbes - TPG Petco Deal

- On Caesars Entertainment: Aggressive leverage in highly cyclical industries like gaming can lead to protracted legal and financial restructuring. — Source: Reuters

- On Braniff Airways: Legal expertise in bankruptcy proceedings can provide the foundation for identifying value in subsequent business careers. — Source: Fort Worth Business

- On Asian Market Pioneering: Founding Newbridge Capital in 1994 positioned TPG to capture the rise of the emerging Asian consumer class before competitors. — Source: TPG Asia

- On Tech Buyouts: The privatization of tech market leaders requires a deep understanding of hardware cycles and structural mispricing. — Source: TPG History

Part 6: Governance and Boardroom Dynamics

- On Board Accountability: Board members must be vigilant in monitoring corporate culture, especially in high-growth "disruptor" environments. — Source: Forbes - Uber Resignation

- On Cultural Sensitivity: Careless or inappropriate remarks in the boardroom can undermine years of work toward improving a toxic corporate culture. — Source: CNN Business

- On Corporate Governance: Governance is the "easiest nut to crack" in ESG because private equity firms usually have the direct power to install better management. — Source: Private Equity International

- On Board Refreshment: As a company matures from a disruptor to an incumbent, the governance requirements must evolve to handle new stakeholders. — Source: The Irish Times - Ryanair Governance

- On Sage and Visionary Partnerships: A successful firm needs a balance between a combative CEO and a chairman who provides calm, strategic thinking. — Source: Ryanair 2019 Annual Report

- On Shareholder Revolts: Long-tenured board members risk being seen as too "cosy" with management, highlighting the need for regular board turnover. — Source: The Guardian

- On Legal Theory and the SEC: "The problem with the SEC's theory is that it's wrong," showing a willingness to challenge regulatory bodies in the Supreme Court. — Source: Dirks v. SEC Case Summary

- On Insider Trading Precedent: The Dirks case established the "personal benefit" test, a cornerstone of securities law that protects legitimate market research. — Source: Fort Worth Business

- On Boardroom Diversity: Increasing board diversity is essential for better decision-making and avoiding the blind spots of a monolithic culture. — Source: Bloomberg

Part 7: Pragmatic ESG and Impact Investing

- On Prohibited Industries: "Things that kill people, we try to stay away from," leading to TPG’s long-standing avoidance of guns and tobacco. — Source: TPG - Social Responsibility

- On ESG as Advantage: Sensitivity to environmental and social issues is a competitive advantage, functioning similarly to a lower cost of capital. — Source: Private Equity International

- On Human-Centric Conservation: "If you can’t make things work for the people, you won’t make things work for the animals." — Source: Butler Nature

- On Measuring Impact: The Rise Fund aims to "take the religion out of impact investing" by using rigorous data to quantify social value. — Source: The Rise Fund - IMM Methodology

- On the Impact Multiple of Money (IMM): Quantifying the social or environmental value created per dollar invested creates a clear hurdle rate for impact deals. — Source: TPG - Impact Measurement

- On Non-Concessionary Returns: Impact investing should not require a trade-off in financial performance; market-rate returns are necessary to attract institutional capital. — Source: Shockwave.org

- On Evidence-Based Underwriting: Every impact investment must be backed by third-party, peer-reviewed research to prevent "impact washing." — Source: TPG - Y Analytics

- On Scaling Solutions: Impact technology must be scalable to be meaningful; growth-stage commercial capital is the best vehicle for this scaling. — Source: TPG Rise Strategy

- On Conservation Pragmatism: Wildlife conservation is fundamentally a human issue; solutions must provide sustainable livelihoods for local communities. — Source: Mongabay Interview

Part 8: Curiosity, Travel, and Life Lessons

- On Solo Travel: Unstructured, solo travel is a powerful catalyst for personal growth, removing the safety net of familiar peers. — Source: Bonderman Travel Fellowship

- On Radical Independence: "Here is the money—go figure it out," reflecting a belief in the value of radical independence and self-reliance. — Source: University of Washington

- On Non-Academic Growth: The goal of exploration is not to produce research or internships, but to simply "be" in the world. — Source: The Daily UW

- On Cultural Relativity: A profound lesson is moving from thinking "That's just how things are" to "That's just how things are around here." — Source: UW Bonderman Philosophy

- On the Value of Discomfort: "Not knowing is the point," as uncertainty forces a deeper engagement with unfamiliar cultures and systems. — Source: The Daily UW

- On Big Thinking: "Small thinking leads to small results, but big thinking can change the world." — Source: Time Magazine Obituary

- On Respect for Others: Treat everyone—from heads of state to restaurant waiters—with the same level of intellectual respect. — Source: TPG - Remembering David Bonderman

- On Career Choices: "Don't do something you don't like. Look for a job that makes you excited to get up and go to work everyday." — Source: AZ Quotes