Lessons from David Harding

David Harding built Winton Group and AHL by ditching subjective forecasts for the logic of statistical patterns. He treated trend following as a scientific problem, proving that rigorous math beats market intuition. These lessons focus on his approach to risk, skepticism, and the blunt requirement for statistical literacy.

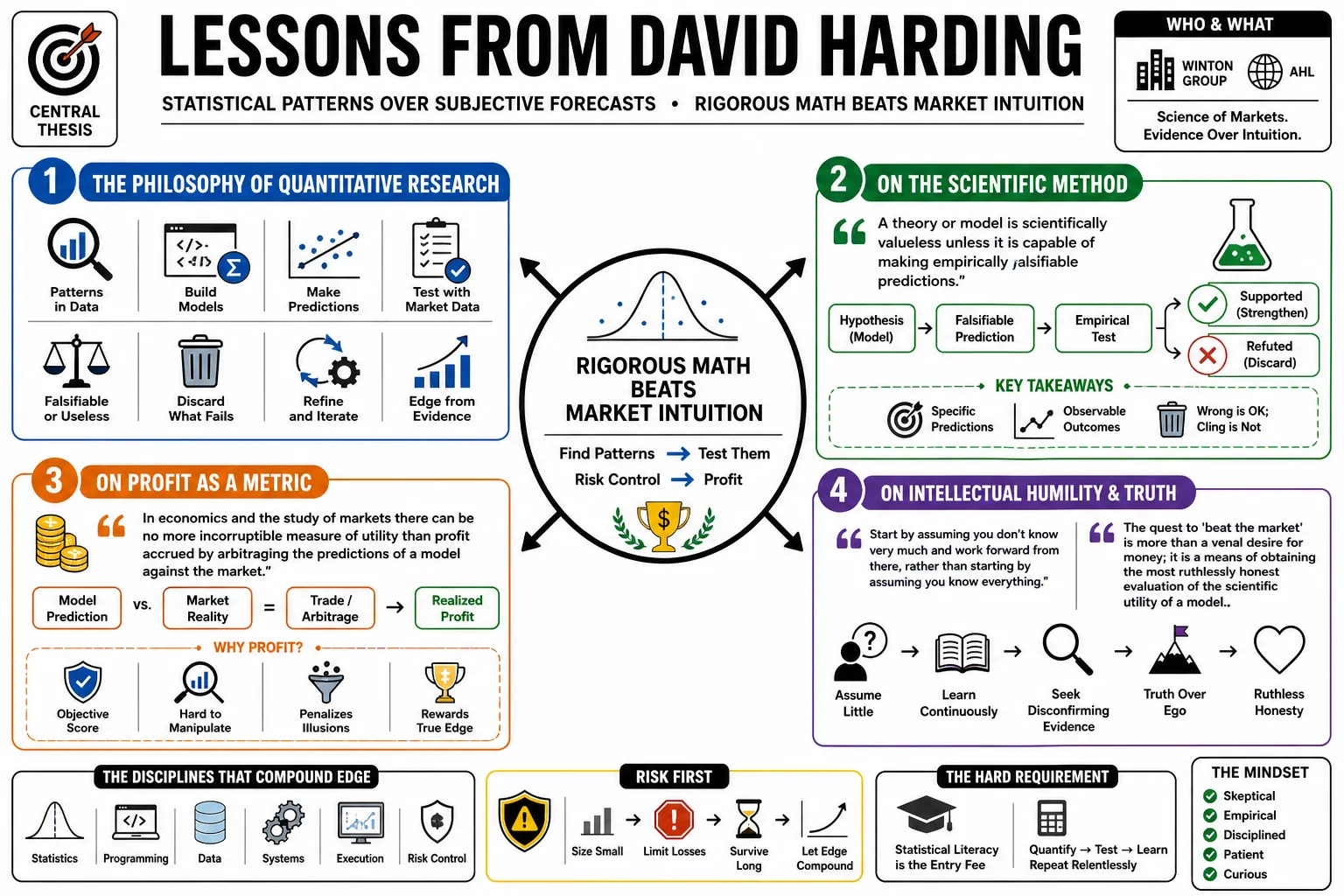

Part 1: The Philosophy of Quantitative Research

- On the Scientific Method: "A theory or model is scientifically valueless unless it is capable of making empirically falsifiable predictions." — Source: Winton Archive: Making Money from Mathematical Models

- On Profit as a Metric: "In economics and the study of markets there can be no more incorruptible measure of utility than profit accrued by arbitraging the predictions of a model against the market." — Source: HedgeNordic

- On Intellectual Humility: "Start by assuming you don't know very much and work forward from there, rather than starting by assuming you know everything." — Source: Talks at GS

- On the Pursuit of Truth: "The quest to 'beat the market' is more than a venal desire for money; it is a means of obtaining the most ruthlessly honest evaluation of the scientific utility of a model." — Source: Philosophical Transactions of the Royal Society

- On Empirical Validation: "A model is not a fact; it is a hypothesis that must be constantly tested against the cold reality of market data." — Source: Winton Research Briefs

- On Human Bias: "Systematic trading is designed to protect the investor from the consequences of their own opinions." — Source: Bloomberg Front Row

- On Market Complexity: "Investing is not a physical science, yet a lot of scientists who go into markets make the mistake of treating it like one." — Source: The Hedge Fund Journal

- On the Role of the Researcher: "We are a heavily research-oriented organization, based on the principle that superior knowledge holds the key to consistent success." — Source: Winton Corporate Profile

- On Models vs. Reality: "Models are approximations of reality, not reality itself; the danger lies in forgetting the difference." — Source: Michael Covel's Trend Following Podcast

Part 2: Trend Following and Market Inefficiency

- On the Existence of Trends: "Trends are a real, persistent feature of financial markets caused by human behavioral biases and institutional constraints." — Source: AHL Founding Principles

- On the Efficient Market Hypothesis: "The idea that markets perfectly discount all information instantly is a religious belief, not a scientific one." — Source: Winton Insight

- On Over-crowded Signals: "As soon as a simple signal like a moving average crossover becomes a commodity, its alpha begins to evaporate." — Source: Bloomberg

- On Weak Signals: "To stay ahead, we have shifted our focus toward 'weak signals'—patterns that are harder to detect and less likely to be exploited by the masses." — Source: Winton 2024 Strategy Update

- On Market Inefficiency: "Markets are only efficient until someone finds a way to profit from their inefficiency." — Source: TurtleTrader

- On the Mechanics of Momentum: "Prices do not move instantaneously to their new equilibrium; they trend because information travels at a finite speed through human networks." — Source: Winton Research

- On Crisis Alpha: "Trend following is one of the few strategies that provides 'crisis alpha' by profiting when traditional assets fall in tandem." — Source: FinNotes

- On the Longevity of Trends: "Human nature hasn't changed in thousands of years, which is why market patterns like trends continue to repeat." — Source: Top Traders Unplugged

- On Competitive Advantage: "Our source of competitive advantage is mainly developing trading strategies based on a deep understanding of bias and statistics." — Source: Winton Archive

Part 3: Risk, Uncertainty, and Statistics

- On Expecting the Unexpected: "You can't bulletproof your funds against the death of humanity, but you can bulletproof them against an overnight 35% drop in the stock market." — Source: Bloomberg Interview

- On Fat-Tail Events: "History is punctuated by terrifically unexpected episodes; relying on a Bell Curve is a recipe for disaster." — Source: THINKpod Podcast

- On Leverage: "Leverage is the primary enemy of survival in finance; we maintain a low-leverage approach to survive the shocks others cannot." — Source: Winton Risk Policy

- On the Predictability of Risk: "Returns are not predictable, but risk is. If an investor asks us to produce a specific annual variance, we can get it exactly right." — Source: The Hedge Fund Journal

- On Cutting Losses: "The trading rules I live by are simple: 1. Cut losses. 2. Cut losses. 3. Cut losses." — Source: Hinchilla Quotes

- On Meaningful Risk: "Risk no more than you can afford to lose, but risk enough so that a win is meaningful." — Source: Winton Risk Philosophy

- On the Biased Coin: "Investing is like tossing a biased coin. We believe our coin will land profit-side up 60 percent of the time over the long run." — Source: Trend Following Archive

- On Survival as Skill: "True skill in finance is the discipline to stay in the game long enough for your statistical edge to manifest." — Source: Bloomberg Front Row

- On Volatility: "We do not fear volatility; we view it as the raw material from which we extract profit." — Source: Winton White Papers

Part 4: Data Science and Information Processing

- On Manual Data Work: "The act of laboriously hand-drawing 400 charts every day forced me into a close contemplation of market behavior that computers cannot replicate." — Source: Winton History

- On Historical Perspective: "To understand the statistical properties of a strategy, you must look back decades—even centuries—to find the scenarios a 5-year backtest would miss." — Source: Winton History Department

- On the Variety of Markets: "Being long on British stocks is just one out of 200 investment choices we can make. This range is our greatest advantage." — Source: The Hedge Fund Journal

- On Data as a Laboratory: "We treat the world's financial history as a laboratory for testing our ideas about human behavior." — Source: Winton Corporate Message

- On Measurement: "If you can't measure it, you probably can't manage it. Things you measure tend to improve." — Source: Harding Center for Risk Literacy

- On Noise vs. Signal: "Most of what people call news is actually noise. Our systems are designed to ignore the narrative and follow the data." — Source: Talks at GS

- On Information Speed: "The edge is no longer in getting information first; it is in processing the vast amount of existing information more effectively." — Source: Winton Insight

- On Systematic Discipline: "The system protects me from the consequences of my own opinions, which I have learned are often wrong." — Source: Bloomberg

- On Scientific Rigor: "Quantitative research is like molecular biology; it requires proceeding very patiently over long periods." — Source: Bloomberg Front Row

Part 5: Business Building and Organizational Culture

- On Resilience: "I attribute my success not to being the smartest person in the room, but to the fact that I simply didn't quit." — Source: Winton Archive

- On Avoiding Complacency: "Anyone who's complacent in my business is waiting to have their head handed to them." — Source: The Hedge Fund Journal

- On Responsibility: "Regulators should punish those who 'blame the computer' for failures. Responsibility always lies with the humans who oversaw the system." — Source: Bloomberg TV

- On Execution: "Execution research is just as important as signal research; a great strategy can be ruined by poor implementation and slippage." — Source: Winton White Papers

- On Scaling: "The bigger you get, the more you have to worry about your own market impact. Scale is a tax on your alpha." — Source: Bloomberg Front Row

- On Institutional Discipline: "The hardest part of systematic trading is sticking to the models during a long drawdown when every instinct tells you to tinker." — Source: Winton Insight

- On Firm Identity: "We are not a hedge fund in the traditional sense; we are a scientific research firm that happens to apply its findings to finance." — Source: Winton About Us

- On Hiring quants: "We look for scientists who are comfortable with the idea that they might be wrong most of the time." — Source: Talks at GS

- On Psychological Discomfort: "Diversification is psychologically unhappy because you will always have a losing position somewhere, but it is mathematically necessary." — Source: Trend Following Archive

Part 6: Critical Thinking and Skepticism

- On Spurious Certainty: "Beware of anyone who offers black-and-white answers to market movements; the truth is always a shade of gray." — Source: Harding Center for Risk Literacy

- On the Illusion of Skill: "If you choose stocks at random and weight them equally, you will beat the S&P 500 in 99.99 percent of cases. Most active management is just noise." — Source: William Poundstone

- On Expert Innumeracy: "Risk illiteracy is not just a problem for the public; many doctors, judges, and bankers struggle to interpret basic statistics." — Source: Harding Center for Risk Literacy

- On News Narrative: "The narrative 'why' a market moved is almost always a story made up after the fact to satisfy our desire for order." — Source: Michael Covel Podcast

- On Intuition: "Be sensitive to the subtle differences between 'intuition' and 'into-wishing'." — Source: Hinchilla Quotes

- On the Power of Randomness: "Life is a game of chance. You've got to take the rough with the smooth because some years are simply beyond your control." — Source: Bloomberg TV

- On Simplicity: "In a complex world, simple decision rules—heuristics—can often be more accurate than complex calculations with too many variables." — Source: Harding Center: Gigerenzer Collaboration

- On Questions over Answers: "The value of a researcher is not in the answers they give, but in the quality of the questions they ask." — Source: Winton Corporate Message

- On Pride: "Pride is a great banana peel in this business, as are hope, fear, and greed." — Source: Hinchilla Quotes

Part 7: Philanthropy and Risk Literacy

- On Statistical Anxiety: "Much of the fear in society comes from a misunderstanding of relative risk vs. absolute risk." — Source: Harding Center for Risk Literacy

- On Absolute Risk: "Always ask for the absolute numbers. A drug that 'doubles' a risk of 1 in 7,000 to 2 in 7,000 has a negligible impact on the individual." — Source: Winton Centre for Risk and Evidence Communication

- On Transparency: "Fact boxes that show both benefits and harms in a balanced way are essential for informed decision-making in health and finance." — Source: Harding Center for Risk Literacy

- On the Giving Pledge: "Extreme wealth should be used for public good; my children do not need billions to live meaningful lives." — Source: The Giving Pledge

- On Scientific Progress: "Cambridge and other centers of learning address humanity's great challenges; supporting them is the best use of my resources." — Source: University of Cambridge Press Release

- On Misleading Statistics: "The media often cherry-picks data to create sensational headlines; learning to spot 'bad statistics' is a survival skill." — Source: Harding Center: Unstatistik des Monats

- On Risk Illiteracy: "A society of informed citizens who can calculate risks is less likely to be manipulated by fear." — Source: THINKpod Podcast

- On the Satisfaction of Giving: "Giving money has been surprisingly satisfactory; you meet people and enjoy experiences you wouldn't otherwise have had." — Source: Hinchilla Quotes

- On Statistical Understanding: "Society's inability to understand probability is a fundamental flaw that leads to medical errors and wrongful convictions." — Source: THINKpod Podcast

Part 8: The Future of Finance and Technology

- On AI Hype: "The public debate around AI is currently nine parts hype to one part substance." — Source: Winton 2024 Outlook

- On AI Predictions: "The idea that AI can perfectly predict market movements is for the birds; markets are not solvable equations." — Source: Winton 2023 Research Brief

- On Generative AI: "We view Generative AI as a digital assistant that automates repetitive research tasks, not a replacement for human scientific rigor." — Source: Winton Careers and Strategy 2024

- On the Death of 60/40: "The era where stocks and bonds provided mutual protection is over; the new regime requires much broader diversification." — Source: Winton 2023 Annual Letter

- On the New Macro Regime: "Higher interest rates and geopolitical shocks have created a 'prime time' for trend-following strategies." — Source: Winton Research Brief

- On Unpredictability Alpha: "We don't need to predict the future to win; we capture the 'alpha' that comes from the market's reaction to the unexpected." — Source: Winton Insight

- On Historical Tailwinds: "We must be humble; much of our industry's success came from a 40-year decline in interest rates that may not repeat." — Source: Winton Archive

- On Technological Evolution: "AI is an evolution of the statistical tools we have used for decades, not a revolutionary black box." — Source: Winton 2024 strategy

- On Human-AI Synergy: "The human touch remains critical for scientific rigor; AI surfaces data, but humans must interpret the 'why'." — Source: Winton Group

- On the Complexity of Human Systems: "AI struggles with markets because, unlike gravity, market rules change as soon as humans learn to exploit them." — Source: Winton Research Brief

- On Adaptation: "Anyone who thinks they have found the final answer to the markets is waiting to be proven wrong by history." — Source: Michael Covel Podcast

- On Final Perspective: "Life is a game of chance. You play the odds as best you can and accept the outcomes with grace." — Source: Bloomberg TV