Lessons from Don Valentine

Don Valentine founded Sequoia Capital in 1972 and backed early tech companies like Apple, Atari, and Cisco. He cared more about market size than a founder's resume, arguing that great markets build great companies. These notes cover his approach to venture capital, business survival, and market mechanics.

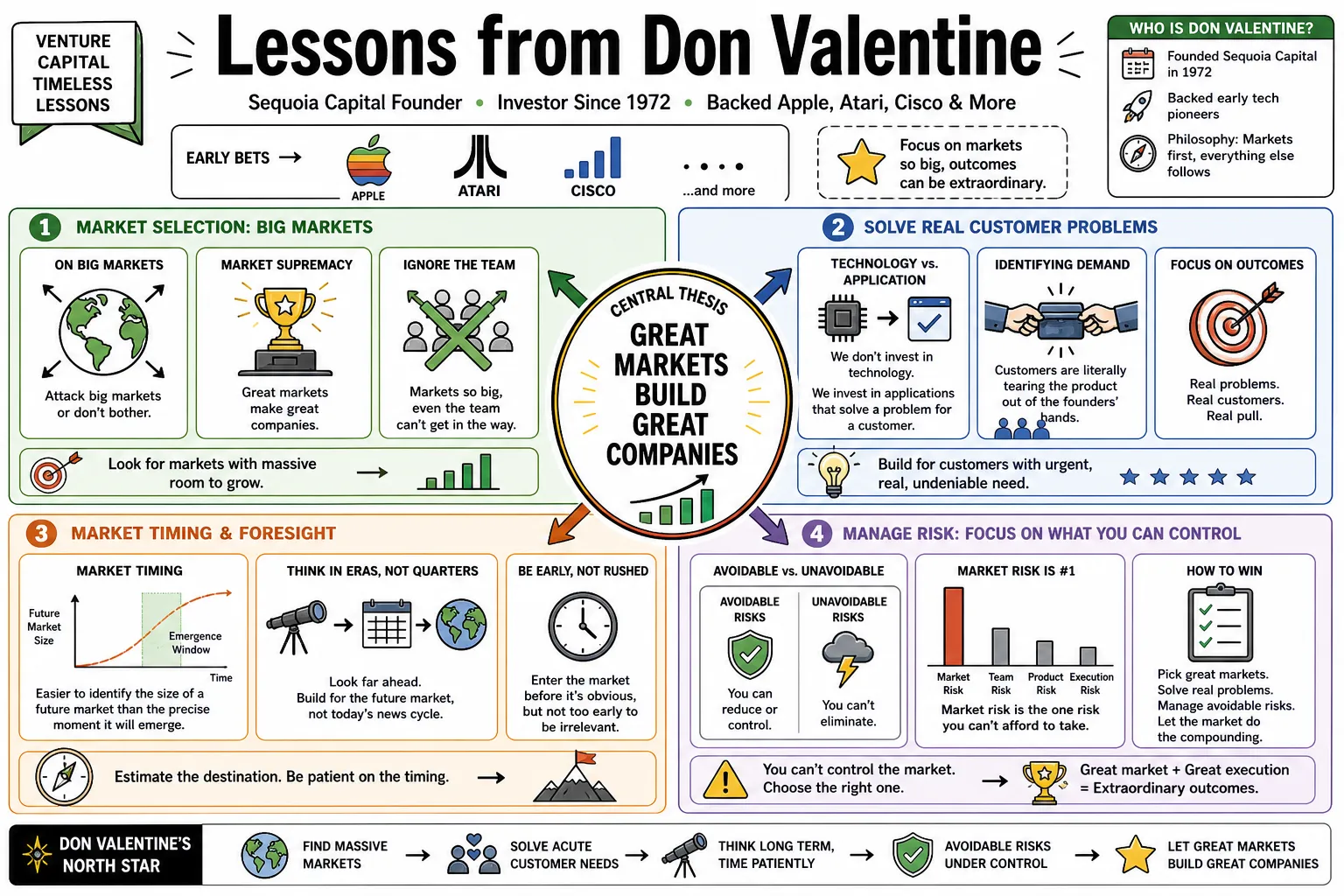

Part 1: Market Selection

- On Big Markets: "If you don't attack a big market, you're highly unlikely to build a big company." — Source: [Stanford GSB: Target Big Markets]

- On Market Supremacy: "Great markets make great companies." — Source: [Sequoia Capital History]

- On Ignoring the Team: "I like opportunities that are addressing markets so big that even the management team can't get in its way." — Source: [Something Ventured]

- On Technology vs. Application: "We don't invest in technology. We invest in applications that solve a problem for a customer." — Source: [Stanford Silicon Genesis Project]

- On Market Timing: It is easier to identify the size of a future market than it is to identify the precise moment that market will emerge. — Source: [Acquired Podcast]

- On Identifying Demand: The best investments are those where customers are literally tearing the product out of the founders' hands because the underlying need is so acute. — Source: [The Founders' Tribune]

- On Avoidable Risks: Market risk is the one risk you cannot fix; if the market isn't there, no amount of engineering brilliance will save the company. — Source: [Stanford GSB: Target Big Markets]

- On Assessing Size: A market isn't large unless you can articulate clearly who the millions of buyers are and exactly why they will buy. — Source: [25iq]

- On Competition: Early competition in a new sector often validates the market size rather than threatening your investment. — Source: [UC Berkeley Regional Oral History]

- On Enduring Value: Enduring companies are built as a response to massive structural shifts in how people or businesses operate. — Source: [Stanford GSB: Target Big Markets]

Part 2: Product and Problem Solving

- On Problem Clarity: "The first question I ask is: who cares?" — Source: [Stanford GSB: Target Big Markets]

- On Creating Necessity: The goal is to build a product that transitions from being a novelty to an absolute necessity. — Source: [Sequoia Capital History]

- On Technical Elegance: Customers do not buy technical elegance; they buy a solution to a problem that is costing them time or money. — Source: [The Founders' Tribune]

- On Incremental Improvements: Marginal improvements on existing products rarely build standalone companies; you need a step-function change in utility. — Source: [Acquired Podcast]

- On Feature Creep: Focus on the single feature that the customer is willing to pay for today, and build the rest later. — Source: [Stanford Silicon Genesis Project]

- On Pricing: If a product truly solves a massive headache, price resistance is usually much lower than the founders assume. — Source: [25iq]

- On User Feedback: Early customers will tell you exactly what your product actually is, which is often different from what you thought you built. — Source: [UC Berkeley Regional Oral History]

- On Simplicity: Complexity is the enemy of adoption. The best products require almost no explanation to their core demographic. — Source: [Stanford GSB: Target Big Markets]

- On Moore's Law: Leverage underlying technological curves to make your product cheaper and faster every year without changing the core value proposition. — Source: [Stanford Silicon Genesis Project]

- On Product Validation: The ultimate proof of a product is a purchase order, not a beta test. — Source: [The Founders' Tribune]

Part 3: Founder Traits and Psychology

- On Second-Time Founders: "The trouble with the first-time entrepreneur is that he doesn't know what he doesn't know. After a failure, he does know what he doesn't know and can beat the hell out of people who still have to learn." — Source: [Something Ventured]

- On Disobedience: "The world of technology thrives best when individuals are left alone to be different, creative, and disobedient." — Source: [Something Ventured]

- On Founder Arrogance: A certain level of arrogance is required to believe you can change an entire industry, but it must be paired with extreme market awareness. — Source: [Acquired Podcast]

- On Steve Jobs: He backed a young Steve Jobs not because he was polished, but because his absolute conviction about the future of personal computing was impossible to ignore. — Source: [Stanford GSB: Target Big Markets]

- On Listening: The best founders are aggressive in their vision but surprisingly paranoid and attentive when it comes to early market feedback. — Source: [UC Berkeley Regional Oral History]

- On Pedigree: An Ivy League degree is far less interesting than a track record of building things and breaking rules. — Source: [25iq]

- On Obsession: Look for founders who are pathologically obsessed with their specific problem, rather than those who just want to be entrepreneurs. — Source: [The Founders' Tribune]

- On Self-Awareness: Great founders recognize their own limitations quickly and hire executives who are better than them in specific functional areas. — Source: [Stanford Silicon Genesis Project]

- On Resilience: The default state of a startup is failure; the founder's primary job is to refuse that default state every single day. — Source: [Sequoia Capital History]

- On Visionaries: True visionaries can explain how the world will look ten years from now, and exactly what the first step is tomorrow morning. — Source: [Stanford GSB: Target Big Markets]

Part 4: Storytelling and Communication

- On the Function of Stories: "The money flows as a function of the stories." — Source: [Stanford GSB: Target Big Markets]

- On Explaining Strategy: "The art of storytelling is incredibly important... it's how an entrepreneur explains the strategy, the competition, and the necessity of the product." — Source: [Stanford GSB: Target Big Markets]

- On Clarity: If you cannot explain your business to a smart person in a different field within two minutes, your story is too complicated. — Source: [Acquired Podcast]

- On Pitching: A pitch should not be a technical manual; it should be a narrative about how a massive market is currently suffering and how you will relieve that suffering. — Source: [25iq]

- On Raising Capital: Investors do not fund spreadsheets; they fund compelling narratives backed by plausible math. — Source: [The Founders' Tribune]

- On Recruiting: The same story used to raise money must be weaponized to recruit top-tier talent who are currently comfortable at established companies. — Source: [Stanford Silicon Genesis Project]

- On Brevity: Use fewer slides and fewer words. Confidence is usually inversely correlated with the length of a presentation. — Source: [Stanford GSB: Target Big Markets]

- On the Core Question: Every story must ultimately answer: "Why this, why now?" — Source: [UC Berkeley Regional Oral History]

- On Evolving the Narrative: As the company scales, the story must shift from the promise of the technology to the reality of the business metrics. — Source: [Sequoia Capital History]

Part 5: The Mechanics of Venture Capital

- On VC's Role: "Real VCs help build great companies." — Source: [The Founders' Tribune]

- On Active Involvement: Venture capital is not passive asset management; it requires active, sometimes uncomfortable interventions in the companies you fund. — Source: [Stanford Silicon Genesis Project]

- On Contrarianism: You make the most money when you are right and the rest of the market completely disagrees with you. — Source: [Acquired Podcast]

- On Deal Flow: The best deals rarely come from business plans mailed to the office; they come from a network of engineers and former founders who know who the smartest person in the room is. — Source: [UC Berkeley Regional Oral History]

- On Board Seats: A venture capitalist on a board should ask the hard questions that the management team is avoiding, not just cheerlead. — Source: [25iq]

- On Sunk Costs: Know when to stop funding a mistake. Pouring more money into a company with a fundamentally flawed market thesis will not fix the thesis. — Source: [Stanford GSB: Target Big Markets]

- On Portfolio Returns: Venture is a business of extreme outliers. One massive success must pay for the dozens of failures and still return the fund. — Source: [Sequoia Capital History]

- On the Dot-Com Bubble: He heavily criticized the late-90s era where venture capitalists funded quick flips instead of focusing on long-term business fundamentals. — Source: [The Founders' Tribune]

- On Assessing Risk: Technical risk is acceptable if the market is huge. Market risk is unacceptable regardless of how good the technology is. — Source: [Stanford GSB: Target Big Markets]

Part 6: Cash and Survival

- On Business Mortality: "All companies that go out of business do so for the same reason – they run out of money." — Source: [Something Ventured]

- On Cash Management: Managing cash burn is not a finance function; it is the core existential responsibility of the CEO. — Source: [Acquired Podcast]

- On Profitability: Revenue is a vanity metric if the unit economics do not eventually lead to cash flow generation. — Source: [Stanford GSB: Target Big Markets]

- On Raising Funds: Raise money when you don't need it, because capital is rarely available when you are desperate for it. — Source: [25iq]

- On Milestone Funding: Capital should be tied to specific technical or market milestones, forcing the company to prove its thesis before getting more cash. — Source: [Stanford Silicon Genesis Project]

- On Frugality: A culture of extreme frugality in the early days sets a precedent that survives even when the company becomes wildly profitable. — Source: [UC Berkeley Regional Oral History]

- On the Runway: Every decision in a startup must be weighed against how many months of runway it consumes versus how much value it creates. — Source: [The Founders' Tribune]

- On Gross Margins: High gross margins are the ultimate shock absorber for a growing business, giving you the room to make mistakes and survive. — Source: [Stanford GSB: Target Big Markets]

- On Financial Discipline: Startups die from indigestion, not starvation; too much money often leads to sloppy execution and a loss of focus. — Source: [Sequoia Capital History]

Part 7: Building the Team and Culture

- On Hiring: The hardest transition for a technical founder is realizing their primary job has shifted from writing code to recruiting people. — Source: [Acquired Podcast]

- On Executive Experience: Bring in experienced management not to replace the founder's vision, but to scale the operational mechanics of the business. — Source: [Stanford Silicon Genesis Project]

- On Sales Teams: Engineering builds the product, but a relentless, process-driven sales organization is what actually builds the business. — Source: [Stanford GSB: Target Big Markets]

- On Replacing Founders: If a founder cannot transition from a product visionary to a company operator, it is the board's duty to bring in a CEO who can. — Source: [UC Berkeley Regional Oral History]

- On Culture: Company culture isn't ping-pong tables; it is the shared understanding of how decisions are made when the CEO is not in the room. — Source: [25iq]

- On Talent Density: A-players hire A-players, while B-players hire C-players to protect their own standing. — Source: [The Founders' Tribune]

- On Alignment: Every employee must understand exactly how their specific daily tasks map to the survival and growth of the company. — Source: [Sequoia Capital History]

- On Firing: Firing fast is an act of mercy for both the company and the employee who is clearly in the wrong role. — Source: [Stanford GSB: Target Big Markets]

- On Complementary Skills: The best founding teams have non-overlapping skill sets; two brilliant engineers are often less effective than one engineer and one ruthless salesperson. — Source: [Acquired Podcast]

Part 8: Silicon Valley and Technological Change

- On Geography: Silicon Valley's advantage is not the weather; it is a dense, high-trust network of risk-tolerant capital and engineering talent. — Source: [UC Berkeley Regional Oral History]

- On the Semiconductor Roots: The disciplined, manufacturing-heavy culture of the early semiconductor industry laid the pragmatic foundation for modern venture capital. — Source: [Stanford Silicon Genesis Project]

- On Legacy Systems: Every major incumbent eventually becomes paralyzed by their own legacy revenue, creating a permanent structural opportunity for startups. — Source: [Stanford GSB: Target Big Markets]

- On Platform Shifts: The biggest companies are built during rare transitional moments, like the shift from minicomputers to PCs, or from desktop to mobile. — Source: [Acquired Podcast]

- On Hardware vs. Software: While he started in hardware, he recognized early that software would eventually command higher margins and faster distribution. — Source: [Sequoia Capital History]

- On the Value of Fairchild: Fairchild Semiconductor acted as the ultimate training ground for an entire generation of founders and investors who learned how to build scale. — Source: [Stanford Silicon Genesis Project]

- On Cycles: The technology sector is inherently cyclical; great investors maintain their discipline during booms and aggressively deploy capital during busts. — Source: [The Founders' Tribune]

- On Institutional Memory: Sequoia's longevity comes from institutionalizing the lessons of past failures so that new partners don't make the same mistakes. — Source: [25iq]

- On the Future: The specific technologies will always change, but the fundamental mechanics of identifying huge markets and backing unyielding founders will remain permanent. — Source: [Stanford GSB: Target Big Markets]