Eric Mandelblatt is the founder and Chief Investment Officer of Soroban Capital Partners, where he manages a concentrated equity portfolio. He is known for his thesis on the chronic underinvestment in the physical economy and his activist campaigns to reform major industrial companies. This collection organizes his insights on capital allocation, commodity cycles, and the realities of the energy transition.

Part 1: The Industrial Economy

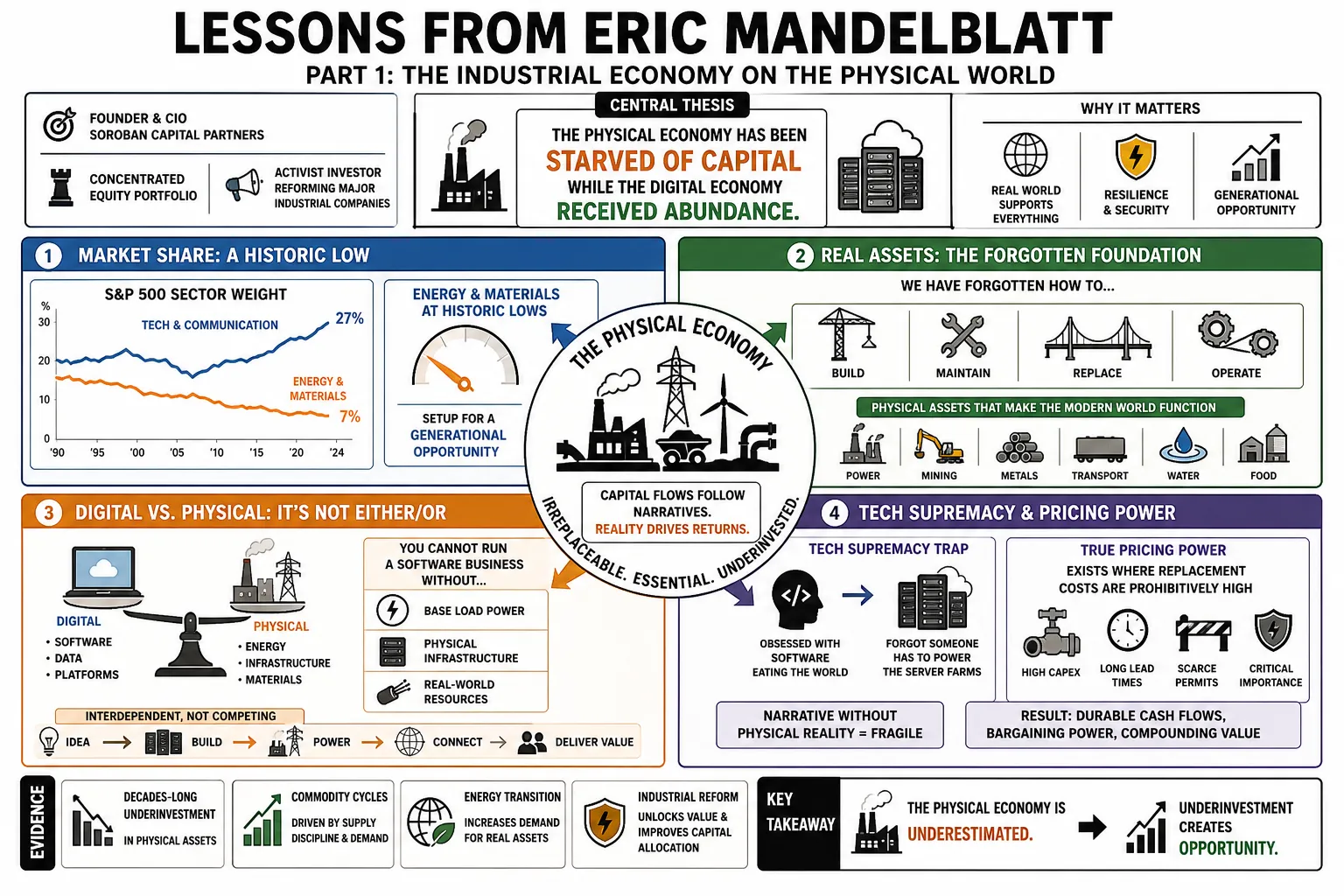

- On The Physical World: "The physical economy has been starved of capital while the digital economy received abundance." — Source: [Invest Like the Best: Episode 266]

- On Market Share: "Energy and materials make up a historically low share of the S&P 500, setting up a generational opportunity." — Source: [Invest Like the Best: Episode 266]

- On Real Assets: "We have forgotten how to build and maintain the physical assets that make the modern world function." — Source: [Invest Like the Best: Episode 266]

- On Digital vs Physical: "You cannot run a software business without base load power and physical infrastructure." — Source: [Invest Like the Best: Episode 266]

- On Tech Supremacy: "The market became so obsessed with software eating the world that it forgot someone has to power the server farms." — Source: [Invest Like the Best: Episode 266]

- On Pricing Power: "True pricing power exists where replacement costs are prohibitively high and new capacity is structurally constrained." — Source: [Invest Like the Best: Episode 266]

- On Industrial Moats: "Regulatory barriers and massive capital requirements create the strongest modern economic moats." — Source: [Invest Like the Best: Episode 266]

- On Underinvestment: "Decades of underinvestment in the industrial base cannot be reversed overnight with new capital." — Source: [Invest Like the Best: Episode 266]

- On Essential Services: "In times of inflation, companies that provide essential daily services to the economy outperform." — Source: [Invest Like the Best: Episode 266]

- On Supply Chains: "The fragility of global supply chains has reminded the market of the value of domestic industrial capacity." — Source: [Invest Like the Best: Episode 266]

Part 2: Commodity Cycles and Capital Cycles

- On Capital Cycles: "Commodity supercycles are born out of prolonged periods of capital starvation." — Source: [Invest Like the Best: Episode 266]

- On CAPEX: "You can forecast the next decade of commodity prices by looking at the last decade of capital expenditure." — Source: [Invest Like the Best: Episode 266]

- On Supply Destruction: "Low prices don't simply stimulate demand; they actively destroy future supply capacity." — Source: [Invest Like the Best: Episode 266]

- On Capital Discipline: "Shareholders have finally forced energy management teams to prioritize return of capital over growth at any cost." — Source: [Invest Like the Best: Episode 266]

- On the Shale Boom: "The era of debt-fueled production growth in American shale is permanently over." — Source: [Invest Like the Best: Episode 266]

- On Mining Constraints: "It takes a decade or more to permit and build a new copper mine, making supply highly inelastic to short-term price signals." — Source: [Invest Like the Best: Episode 266]

- On Free Cash Flow: "The shift from growth to free cash flow generation in cyclical industries is a fundamental regime change." — Source: [Invest Like the Best: Episode 266]

- On Inflation: "Commodities are highly effective inflation hedges, but today their supply constraints are a primary driver of inflation itself." — Source: [Invest Like the Best: Episode 266]

- On Reinvestment Risk: "Companies that refuse to reinvest in new supply today are guaranteeing higher prices for their existing assets tomorrow." — Source: [Invest Like the Best: Episode 266]

- On Cycle Duration: "Because it takes so long to bring new physical supply online, industrial upcycles will last longer than the market expects." — Source: [Invest Like the Best: Episode 266]

Part 3: The Energy Transition and Decarbonization

- On Green Energy Reality: "You cannot transition the global economy to renewable energy without massive quantities of traditional industrial materials." — Source: [Invest Like the Best: Episode 266]

- On Copper: "Copper is the indispensable metal of the energy transition; there is no decarbonization without it." — Source: [Invest Like the Best: Episode 266]

- On ESG Constraints: "ESG mandates have had the unintended consequence of restricting capital to the very industries needed to build green infrastructure." — Source: [Invest Like the Best: Episode 266]

- On Fossil Fuels: "Traditional energy sources will be required to bridge the multi-decade gap to a fully decarbonized economy." — Source: [Invest Like the Best: Episode 266]

- On Carbon Taxes: "Implicit or explicit carbon pricing will radically alter the cost curve of industrial production globally." — Source: [Invest Like the Best: Episode 266]

- On Utility Monopolies: "Regulated utilities are at the epicenter of the energy transition and possess guaranteed rates of return on massive new investments." — Source: [Invest Like the Best: Episode 266]

- On Grid Infrastructure: "Building wind and solar generation is useless without a historic rebuild of the electrical grid." — Source: [Invest Like the Best: Episode 266]

- On Clean Energy CAPEX: "The decarbonization of the global economy will require the largest capital expenditure cycle in human history." — Source: [Invest Like the Best: Episode 266]

- On Policy Uncertainty: "Ambiguous environmental regulations prevent companies from making 30-year capital commitments to new supply." — Source: [Invest Like the Best: Episode 266]

- On Paradoxical Outcomes: "Restricting fossil fuel supply faster than we can scale renewable alternatives guarantees structurally higher energy prices." — Source: [Invest Like the Best: Episode 266]

Part 4: Railroads and Infrastructure

- On Rail Franchises: "Class I railroads are irreplaceable assets with structural pricing power that cannot be replicated." — Source: [2023 Union Pacific Letter]

- On Operational Excellence: "A premier franchise is no excuse for poor operational performance; it should be the foundation for industry-leading efficiency." — Source: [2023 Union Pacific Letter]

- On Precision Scheduled Railroading: "The principles of PSR work, but they require relentless execution and cultural buy-in from leadership." — Source: [2023 Union Pacific Letter]

- On Volume Growth: "You cannot cut your way to prosperity forever; eventually, a railroad must provide reliable enough service to win back volume." — Source: [2023 Union Pacific Letter]

- On Safety and Efficiency: "Safety and operational efficiency are not opposing forces in railroading; they are the exact same metric." — Source: [2023 Union Pacific Letter]

- On Monopoly Complacency: "When a business operates as a duopoly, management can sometimes mistake structural advantage for personal genius." — Source: [Invest Like the Best: Episode 266]

- On Network Effects: "The value of a rail network grows exponentially with density, making asset utilization the ultimate driver of margins." — Source: [Invest Like the Best: Episode 266]

- On Trucking Substitution: "Railroads should be taking share from trucking given their environmental and cost advantages, but poor service has prevented it." — Source: [Invest Like the Best: Episode 266]

- On Maturing Assets: "Mature infrastructure assets should be aggressively returning capital to shareholders through buybacks, not engaging in empire-building." — Source: [Invest Like the Best: Episode 266]

Part 5: Capital Allocation and Corporate Governance

- On Shareholder Alignment: "The most important metric in any company is whether the leadership team is financially aligned with the equity holders." — Source: [2023 Union Pacific Letter]

- On Stock Buybacks: "Share repurchases are only value-accretive when the stock is cheap; doing them at peak multiples destroys intrinsic value." — Source: [2023 Union Pacific Letter]

- On Board Oversight: "Boards of directors too often act as cheerleaders for the CEO rather than representatives of the shareholders." — Source: [2023 Union Pacific Letter]

- On Executive Compensation: "If you pay a management team for volume growth, they will destroy return on invested capital to give you volume growth." — Source: [2023 Union Pacific Letter]

- On Capital Allocation: "The CEO's primary job is capital allocation, yet most reach the position with zero experience in it." — Source: [2023 Union Pacific Letter]

- On Value Destruction: "More shareholder wealth has been destroyed by hubristic M&A than by any operational failure." — Source: [2023 Union Pacific Letter]

- On Dividends vs Buybacks: "We prefer buybacks over dividends when management teams are highly convicted that their intrinsic value is deeply misunderstood by the public market." — Source: [2018 Investor Letter]

- On Corporate Bloat: "Years of easy money allowed management teams to build bloated cost structures that only become visible when the cycle turns." — Source: [2018 Investor Letter]

- On Return on Capital: "Growth without a return on capital exceeding the cost of capital is simply a mechanism for lighting money on fire." — Source: [2018 Investor Letter]

Part 6: Activist Investing and Driving Change

- On the Purpose of Activism: "Activism is about acting like an owner when the actual owners are too dispersed to act." — Source: [2023 Union Pacific Letter]

- On Leadership Upgrades: "Sometimes the only way to fix a premier asset is to install best-in-class leadership from the outside." — Source: [2023 Union Pacific Letter]

- On Public Letters: "A public campaign is a last resort, utilized only when private engagement fails to spur necessary urgency." — Source: [2023 Union Pacific Letter]

- On Operational Turnarounds: "You don't need a new strategy to fix a great business; you usually just need someone who knows how to execute the existing one." — Source: [2023 Union Pacific Letter]

- On Board Refreshment: "Tenured boards often lack the specific industry expertise required to hold management accountable for operational metrics." — Source: [2023 Union Pacific Letter]

- On Constructive Engagement: "The most successful activist campaigns are the ones where the board realizes the shareholders are right before a proxy fight becomes necessary." — Source: [2023 Union Pacific Letter]

- On Value Unlocking: "Activism doesn't create value; it simply acts as the catalyst to unlock the intrinsic value that was trapped by poor management." — Source: [2023 Union Pacific Letter]

- On Institutional Support: "An activist campaign only succeeds if the silent majority of index funds and long-only managers agree with the thesis." — Source: [2023 Union Pacific Letter]

- On Patience: "Driving operational change at a massive industrial company takes years, never quarters." — Source: [2023 Union Pacific Letter]

Part 7: Investment Philosophy and Concentration

- On Portfolio Concentration: "Taking all the firm's investment resources and concentrating them on a third of the positions frees up time for independent thinking." — Source: [2018 Investor Letter]

- On Conviction: "You cannot generate alpha by owning 50 positions; you must concentrate capital in your highest conviction ideas." — Source: [2018 Investor Letter]

- On Due Diligence: "Reducing position count allows us to deepen our due diligence on industries and portfolio companies to a level others cannot match." — Source: [2018 Investor Letter]

- On the Business Model of Investing: "We closed the master fund not as a market call, but as a business model call to preserve our edge." — Source: [2018 Investor Letter]

- On Skin in the Game: "The partners of our firm expect to be one of the largest investors, and each of us will invest a material portion of our liquid net worth in the fund." — Source: [2010 Launch Letter]

- On Independent Thinking: "The greatest risk to an investor is institutionalizing the process to the point where original thought is crowded out." — Source: [2018 Investor Letter]

- On Idiosyncratic Risk: "We search for investments where the outcome is dependent on specific corporate actions rather than macroeconomic tides." — Source: [2018 Investor Letter]

- On Long-Term Horizons: "The public market's obsession with quarterly earnings is the primary arbitrage opportunity for long-term capital." — Source: [2018 Investor Letter]

- On Deep Research: "True conviction only comes from understanding a business better than the people running it." — Source: [2018 Investor Letter]

Part 8: The Psychology of Markets

- On Market Myopia: "The market is incredibly efficient at pricing the next three months and incredibly inefficient at pricing the next three years." — Source: [Invest Like the Best: Episode 266]

- On Institutional Imperatives: "The pressure to hug the benchmark forces institutional capital to abandon fundamental valuation." — Source: [Invest Like the Best: Episode 266]

- On Consensus Thinking: "If you are reading the same sell-side research as everyone else, you cannot expect to generate a differentiated return." — Source: [Invest Like the Best: Episode 266]

- On Volatility vs Risk: "Volatility is the price of admission for long-term outperformance, never a measure of fundamental risk." — Source: [Invest Like the Best: Episode 266]

- On Contrarianism: "Being a contrarian is easy to say but agonizing to live through, as it requires looking wrong for extended periods." — Source: [Invest Like the Best: Episode 266]

- On Complexity: "Investors often confuse complex financial models with accurate financial models; the best theses can be explained simply." — Source: [Invest Like the Best: Episode 266]

- On Market Narratives: "The market loves a simple narrative, but industrial reality is usually messy, cyclical, and non-linear." — Source: [Invest Like the Best: Episode 266]

- On Patience and Action: "Most of investing is doing absolutely nothing, followed by moments of intense, decisive action when the facts change." — Source: [Invest Like the Best: Episode 266]

- On Humility: "The market has a unique ability to humble anyone who believes they have figured it out completely." — Source: [Invest Like the Best: Episode 266]