Lessons from Geraldine Weiss

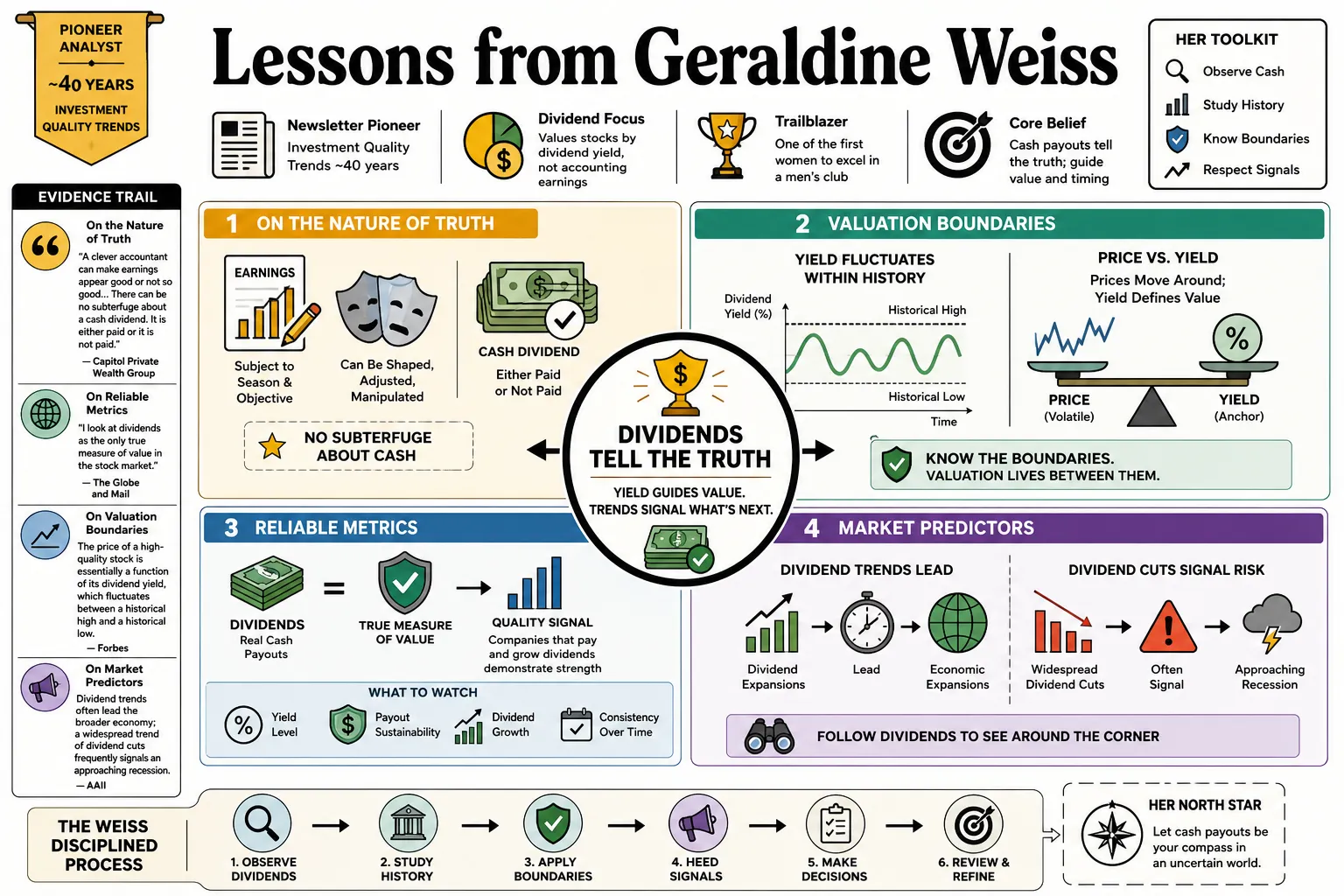

Geraldine Weiss managed the newsletter Investment Quality Trends for nearly forty years, valuing stocks by their dividend yields rather than accounting earnings. By focusing on cash payouts, she became one of the first women to find major success in a professional stock analysis world that was almost exclusively a men’s club.

Part 1: The Dividend Yield Theory

- On the Nature of Truth: "A clever accountant can make earnings appear good or not so good, depending on the season or the objective. There can be no subterfuge about a cash dividend. It is either paid or it is not paid." — Source: Capitol Private Wealth Group

- On Valuation Boundaries: The price of a high-quality stock is essentially a function of its dividend yield, which fluctuates between a historical high and a historical low. — Source: Forbes

- On Reliable Metrics: "I look at dividends as the only true measure of value in the stock market." — Source: The Globe and Mail

- On Market Predictors: Dividend trends often lead the broader economy; a widespread trend of dividend cuts frequently signals an approaching recession. — Source: AAII

- On the Price-Yield Relationship: While stock prices are volatile, the yield provides a "valuation signature" that reveals whether a company is objectively cheap or expensive. — Source: GuruScreener

- On Capital Gains: The greatest capital gains are achieved by purchasing stocks at their historical yield peaks and waiting for the market to bid them back to historical lows. — Source: Compounding Dividends

- On Yield as a Floor: A historically high dividend yield acts as a "floor" for a stock price because it eventually attracts value investors who recognize the yield's attractiveness. — Source: Canadian Dividend Investing

- On Accounting Fiction: Earnings are a matter of opinion influenced by depreciation and inventory methods, but a dividend check deposited in a bank account is a hard fact. — Source: The Dividend Guy Blog

- On the Catalyst for Growth: Consistently rising dividends are the most reliable long-term catalyst for rising stock prices in quality companies. — Source: AAII

Part 2: Defining the Blue-Chip Standard

- On Longevity: A company must have at least 25 years of uninterrupted dividend payments to be considered an "investment quality" blue chip. — Source: Wikipedia

- On Credit Quality: Quality stocks should maintain an S&P Quality Ranking of "A-" or higher to ensure they can withstand economic downturns. — Source: AAII

- On Operational Consistency: Earnings must have improved in at least seven of the last 12 years to verify the company's underlying business health. — Source: Stock Screening 101

- On Growth Trajectory: To keep pace with inflation and provide real value, dividends must have been raised at least five times in the last 12 years. — Source: AAII

- On Market Liquidity: An investment-grade stock should have at least 5 million shares outstanding to ensure investors can enter and exit positions easily. — Source: Stock Screening 101

- On Institutional Support: A high-quality stock should be held by at least 80 institutional investors, indicating a broad base of professional confidence. — Source: Stock Screening 101

- On Defensive Selection: Confining selections to blue-chip stocks significantly reduces the risk of a total loss of capital. — Source: The Economic Times

- On Financial Soundness: "Basically sound" companies are the only vehicles for which dividend yield theory reliably predicts price action. — Source: Compounding Dividends

- On the Dividend Trap: High yield alone is a warning sign; it only becomes an opportunity if the company meets rigorous quality and safety screens. — Source: Compounding Dividends

Part 3: Strategic Market Timing

- On Entry Points: "Never is there a better time to buy a stock than when a basically sound company, for whatever reason, temporarily falls out of favor." — Source: Capitol Private Wealth Group

- On Recognizing Value: A "Buy" signal is triggered when a blue-chip stock’s yield is within 10% of its historical high. — Source: GuruScreener

- On Exit Discipline: When a stock’s yield reaches its historical low, the market has likely overvalued it, and the capital should be "recycled" into a new undervalued position. — Source: Forbes

- On Contrarianism: Buying when "bad things happen to good companies" allows investors to secure yields that the market rarely offers during optimistic periods. — Source: Capitol Private Wealth Group

- On Required Growth Rates: The dividend should ideally have a compound annual growth rate (CAGR) of at least 10% over the previous 12 years to be truly attractive. — Source: Stock Screening 101

- On Waiting for the Cycle: Investment success requires the patience to wait for the yield cycle to move from undervaluation to overvaluation, a process that can take years. — Source: Compounding Dividends

- On Market Noise: Investors should ignore short-term price fluctuations and focus exclusively on where the current yield sits relative to historical yield boundaries. — Source: The Dividend Guy Blog

- On Real-Time Opportunities: Use the "Timely 10" list to identify the best value opportunities available at any given moment in the market cycle. — Source: Investment Quality Trends

- On Sector Rotation: The "Lucky 13" annual portfolio often features sectors that are temporarily unloved but fundamentally strong. — Source: Investment Quality Trends

Part 4: The Psychology of the Dividend Detective

- On Defying Gender Bias: Weiss used the pseudonym "G. Weiss" for 11 years because the 1960s financial community refused to take investment advice from a woman. — Source: Wikipedia

- On Professional Rejection: After graduating from UC Berkeley, Weiss was repeatedly told by brokerage firms that they only hired women for secretarial roles. — Source: Capitol Private Wealth Group

- On the Reveal: When she finally appeared on Wall Street Week with Louis Rukeyser in 1977, her subscribers discovered she was a woman but didn't care because her advice was making them money. — Source: Wikipedia

- On Simplicity: "Successful investing in the stock market is not brain surgery. Anyone can be a successful investor." — Source: Capitol Private Wealth Group

- On Education: Her early interest in finance was sparked by studying the foundational texts of value investing, Benjamin Graham’s Security Analysis and The Intelligent Investor. — Source: Compounding Dividends

- On Overcoming Adversity: Her father changed the family name from Schmulowitz to Small during her high school years to help her avoid anti-Semitic prejudice. — Source: Capitol Private Wealth Group

- On Risk Perception: Fear in the market is often the precursor to the best buying opportunities for disciplined dividend investors. — Source: The Economic Times

- On Logic vs. Emotion: A rules-based system removes the emotional stress of investing by providing clear, mathematical signals for when to act. — Source: Compounding Dividends

- On Mid-Life Success: Weiss launched her professional advisory career at age 40, demonstrating that it is never too late to start a successful investment journey. — Source: Wikipedia

- On Longevity of Strategy: The core principles established in 1966 remained effective and unchanged through her retirement in 2002 and beyond. — Source: Investment Quality Trends

Part 5: Financial Discipline and Metrics

- On the Payout Ratio: For most companies, the dividend payout ratio should be 50% or less to ensure the payment is sustainable and has room to grow. — Source: AAII

- On the Utility Exception: Utility companies are permitted a higher payout ratio, up to 85%, because their cash flows are exceptionally stable and predictable. — Source: AAII

- On Valuation Limits: A Price-to-Earnings (P/E) ratio of 20:1 or less is required to ensure the investor isn't overpaying for the company's current income. — Source: Stock Screening 101

- On Debt Management: Total debt should be 50% or less of the company's total capitalization to protect the "sanctity" of the dividend during credit crunches. — Source: Stock Screening 101

- On Book Value: As a secondary measure of safety, a stock should generally trade at no more than two times its book value. — Source: Stock Screening 101

- On Strict Value Screens: In more conservative market conditions, a price-to-book-value ratio as low as 1.3 is preferred for maximum downside protection. — Source: Capitol Private Wealth Group

- On Financial Strength: Liquidity and a strong balance sheet are necessary to ensure that dividends are paid from earnings, not from borrowed money. — Source: Compounding Dividends

- On Double Net Assets: Seeking companies trading below twice their net asset value provides a safety margin that typical growth investors ignore. — Source: Capitol Private Wealth Group

- On Cash Flow Integrity: Free cash flow yield should be monitored to confirm that the business generates enough actual cash to support its stated dividend. — Source: Investment Quality Trends

- On the Cost of Debt: High debt levels are often the first sign that a dividend cut is imminent, regardless of what the management says. — Source: Compounding Dividends

Part 6: Portfolio Management and Execution

- On Concentration: Weiss recommended a focused portfolio of 10 to 20 high-quality stocks to allow for meaningful gains without excessive complexity. — Source: Capitol Private Wealth Group

- On Diversification Risks: Over-diversification into dozens of stocks often leads to the inclusion of lower-quality companies that dilute the portfolio’s overall safety. — Source: Capitol Private Wealth Group

- On the Immediate Sell Rule: If a company cuts or eliminates its dividend, the fundamental reason for holding the stock has failed, and it should be sold immediately. — Source: AAII

- On Holding Periods: The average winning position in a Weiss-style portfolio is held for approximately three years as it moves through its yield cycle. — Source: Compounding Dividends

- On Sector Balance: Portfolios should be diversified across different resilient industry sectors to avoid being wiped out by a downturn in a single area. — Source: Compounding Dividends

- On Reinvesting Income: The compounding effect of reinvesting dividends from undervalued blue chips is the most effective way to build long-term wealth. — Source: Compounding Dividends

- On "Recycling" Capital: Selling an overvalued stock and moving the proceeds into an undervalued one effectively resets the yield cycle in the investor’s favor. — Source: Forbes

- On Total Return: While the focus is on income, the real goal of the strategy is the total return—dividend yield plus the capital appreciation that occurs as the yield returns to historical lows. — Source: Compounding Dividends

- On Knowledge Concentration: It is better to know a small group of high-quality companies deeply than to have a superficial understanding of hundreds of stocks. — Source: Capitol Private Wealth Group

Part 7: Speculation versus Investment

- On Speculative Stocks: "If a company doesn't pay a dividend, it's a speculation." — Source: The Dividend Guy Blog

- On Growth Traps: High earnings growth rates are meaningless if they are not accompanied by cash dividends that allow shareholders to participate in the success. — Source: Compounding Dividends

- On Chasing Fads: Investors should avoid "hot" products or companies with unproven business models, focusing instead on firms with 25-year track records. — Source: Compounding Dividends

- On Market Hype: Management promises about future growth are no substitute for the tangible reality of a dividend payment. — Source: Compounding Dividends

- On Capital Preservation: Speculation is essentially gambling on the next person's willingness to pay a higher price; dividend investing is participating in a company's cash production. — Source: The Economic Times

- On Market Timing Speculation: Attempting to time the overall market is speculative; timing the yield cycle of an individual high-quality stock is a disciplined strategy. — Source: Compounding Dividends

- On Price vs. Value: The stock market often confuses price with value; the dividend yield is the anchor that pulls the price back toward reality. — Source: The Dividend Guy Blog

- On Debt as a Red Flag: Companies that fund growth primarily through debt rather than cash flow are speculative risks that should be avoided. — Source: Compounding Dividends

- On the Fallacy of Buy and Hold: The "buy and hold forever" mantra is dangerous; an investor must be willing to sell when a stock becomes overvalued and its yield is no longer competitive. — Source: Forbes

Part 8: Legacy and the Investor's Creed

- On Individual Empowerment: Anyone can beat the market by applying a disciplined, rules-based system that ignores gossip and focuses on yield. — Source: Capitol Private Wealth Group

- On the "Secret" to Wealth: "The secret is no secret. It is simply that you confine your selections to blue chip stocks, you buy them when they are undervalued and you sell them when they become overvalued." — Source: The Economic Times

- On Historical Context: A stock’s current yield has no meaning unless it is compared to its own historical range over at least two full market cycles. — Source: AAII

- On Trusting the Math: Math-based yield boundaries are far more reliable than the narratives provided by financial media or corporate executives. — Source: Compounding Dividends

- On the Importance of Yield Peaks: "We all hope for capital gains, but the only thing we can really count on is the dividend." — Source: Compounding Dividends

- On Financial Independence: Building a portfolio of rising dividends is the most direct path to personal financial freedom and retirement security. — Source: Compounding Dividends

- On the Resilience of Blue Chips: High-quality companies with decades of dividend history have already proven they can survive depressions, wars, and technological shifts. — Source: Compounding Dividends

- On Performance Benchmarks: Weiss’s strategies consistently delivered double-digit annual returns, outperforming the S&P 500 while exposing investors to less volatility. — Source: GoBankingRates

- On the Trailblazer Legacy: As the first woman to break the "glass ceiling" of investment advisory services, she proved that results are the only ultimate measure of professional capability. — Source: Wikipedia

- On the Eternal Cycle: The stock market will always cycle between irrational exuberance and unwarranted despair; the dividend yield remains the only constant guide. — Source: The Dividend Guy Blog