Lessons from Glenn Greenberg

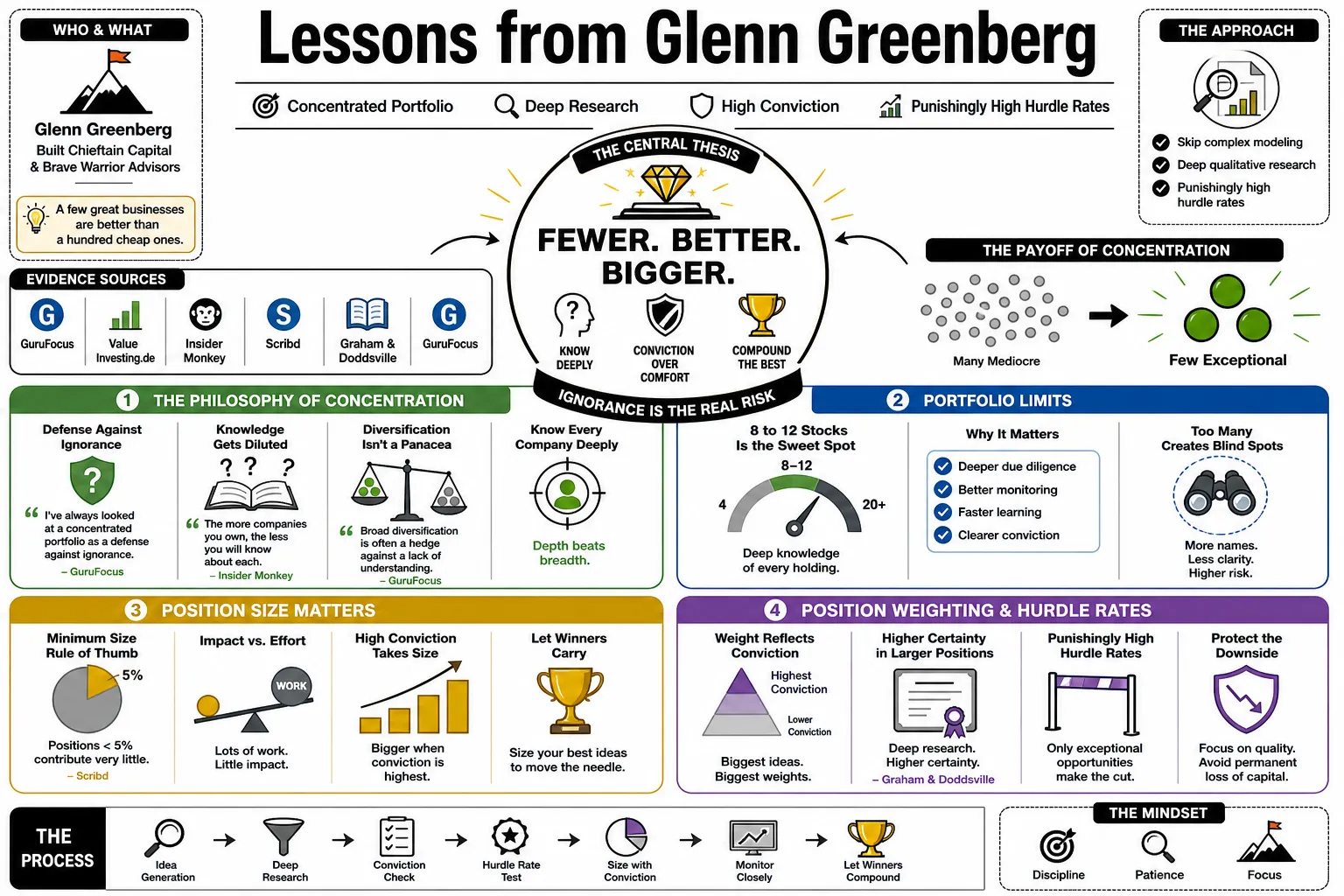

Glenn Greenberg built Chieftain Capital and Brave Warrior Advisors on the belief that a few great businesses are better than a hundred cheap ones. He runs a concentrated portfolio that skips complex modeling in favor of deep research and punishingly high hurdle rates.

Part 1: The Philosophy of Concentration

- On Concentration: "I’ve always looked at a concentrated portfolio as a defense against ignorance." — Source: GuruFocus

- On Portfolio Limits: A typical portfolio should contain only 8 to 12 stocks to ensure the manager knows every company deeply. — Source: ValueInvesting.de

- On the Knowledge Gap: "The more companies you own, the less you will know about each." — Source: Insider Monkey

- On Minimum Sizing: Positions smaller than 5% contribute very little to results relative to the maintenance work required to track them. — Source: Scribd

- On Position Weighting: Large positions have greater certainty because they represent the highest level of conviction and research depth. — Source: Graham & Doddsville

- On Diversification: Broad diversification is often a hedge against a lack of understanding rather than a true risk management tool. — Source: GuruFocus

- On Conviction: Investors must be willing to put at least 5% of their assets into any new idea or it is not worth owning. — Source: Hedge Fund Alpha

- On Risk: Real risk comes from not knowing what you own, not from owning a small number of businesses. — Source: MoneyWeek

- On Maintenance: It is impossible to personally immerse yourself in the numbers of 50 different companies at once. — Source: Scribd

- On Emotional Defense: Deep knowledge of a few businesses prevents mistakes driven by fear and greed during market volatility. — Source: Insider Monkey

Part 2: The Art of Business Analysis

- On Survival: The first question for any investment is whether the business could survive a severe economic downturn. — Source: Greg Speicher

- On ROIC: Look for businesses that produce high returns on invested capital and have little to no competition. — Source: GuruFocus

- On Moats: A strong business has a durable competitive advantage that protects its profit margins over long periods. — Source: ValueInvesting.de

- On Pricing Power: High-quality businesses possess the ability to raise prices without losing their customer base. — Source: Masters Invest

- On Simplicity: "If you can’t write down on a yellow pad why you’re buying a stock, you shouldn’t buy it." — Source: ValueInvesting.de

- On Market Position: Prefer businesses that have a dominant market position in a consolidated industry. — Source: Scribd

- On Management Quality: Look for managers who are personally focused on the business and excel at capital allocation. — Source: Graham & Doddsville

- On Industry Structure: Seek out industries where the capital cycle is favorable and competitors are rational. — Source: GuruFocus

- On Economic Reality: Focus on the free cash flow generated by the business rather than reported accounting earnings. — Source: Scribd

- On Business Types: Avoid complex businesses where success depends on a treadmill of acquisitions funded by debt. — Source: Masters Invest

Part 3: The Disciplined Research Process

- On Handwritten Notes: Jotting down notes on a yellow legal pad helps an investor internalize the financials of a business. — Source: GuruFocus

- On Primary Sources: Always read the 10-K and proxy statements personally rather than relying on summaries. — Source: Greg Speicher

- On Models: "Complicated computer models are worthless" because they often obscure the core drivers of a business. — Source: GuruFocus

- On Numbers: Do not use numbers prepared by others; generating them yourself teaches you which variables to focus on. — Source: Greg Speicher

- On The Truth Serum Test: Imagine you can ask a CEO only three questions under truth serum to find the strategic "make or break" factors. — Source: Substack

- On Key Drivers: Every business performance is typically driven by a small set of three or four key variables. — Source: Scribd

- On Data Services: Avoid automated data providers that distance you from the intimacy of the original financial filings. — Source: GuruFocus

- On Research Intensity: Deep research requires scrubbing the numbers to ensure they reflect economic reality, not accounting mirages. — Source: Scribd

- On Sell-Side Research: Ignore Wall Street analysts who are paid to think in short-term increments rather than long-term franchise value. — Source: ValueInvesting.de

- On Immersion: Personal immersion in the data is the only way to truly understand the unit economics of a business. — Source: Greg Speicher

Part 4: Valuation, Hurdle Rates, and the Margin of Safety

- On Hurdle Rates: Historically, an investment should offer a 15% to 20% expected return to justify the risk of a concentrated position. — Source: MoneyWeek

- On Discount Rates: Using a 20% discount rate ensures that even if growth predictions are too optimistic, the investment can remain profitable. — Source: Insurance News Net

- On Calculation: Valuation is simply adding current free cash flow yield to a conservative estimate of the growth rate. — Source: Scribd

- On Selling: Consider selling a position when the expected internal rate of return drops below 10%. — Source: YouTube

- On the Margin of Safety: A high hurdle rate acts as the primary protection against errors in judgment or unforeseen events. — Source: Scribd

- On Relative Valuation: Avoid price-to-earnings ratios; focus instead on what an owner would receive in cash over the life of the business. — Source: Scribd

- On Conservative Estimates: Assume a "no-growth" or stagnant scenario to find the floor of an investment's value. — Source: Greg Speicher

- On Cheapness: A business is only truly cheap if its franchise value is not deteriorating while the stock price falls. — Source: Scribd

- On Opportunity: Value often exists in widely followed large caps because analysts are too focused on the next quarter to see the long-term runway. — Source: ValueInvesting.de

Part 5: Navigating Market Cycles and Psychology

- On Market Noise: "The market is a giant distraction... You make the most money when the sky is falling." — Source: Scribd

- On Volatility: Stock price drops are temporary opportunities to buy great businesses at lower prices if the moat remains intact. — Source: Scribd

- On the Dot-Com Bubble: Avoiding the tech crash required ignoring "eyeballs" and focusing only on businesses that generated free cash flow. — Source: Hedge Fund Alpha

- On Crisis Prices: During severe market crashes, essential businesses are often sold at "thievery" prices by panicked investors. — Source: Hedge Fund Alpha

- On Privacy: Disclosure requirements can be harmful because copycats front-run positions and discourage deep original research. — Source: SEC.gov

- On Proxy Systems: Shareholders should protect their rights to prevent the entrenchment of inefficient corporate executives. — Source: SEC.gov

- On Long-Term Thinking: The "gap" in market thinking is the difference between an analyst's one-year view and an owner's five-year view. — Source: ValueInvesting.de

- On Complexity: High debt combined with non-transparent operations is a recipe for permanent loss of capital in any market cycle. — Source: Masters Invest

- On Focus: Zero in on the make-or-break factors of an investment and avoid the minutiae that distract most market participants. — Source: Value Investing World

Part 6: Lessons from the Portfolio

- On Two-Inch Putts: Formative lessons include finding obvious opportunities, like a company whose timberland is worth three times its stock price. — Source: Greg Speicher

- On Cable Infrastructure: The late-90s bet on cable was based on the "two-way wire" being superior to satellite for the coming internet age. — Source: Hedge Fund Alpha

- On Google: The advertising thesis for Google relied on the fact that online ad spend would eventually catch up to time spent online. — Source: Hedge Fund Alpha

- On Ryanair: Analyzing Ryanair involves looking at the cash it would generate if it simply stopped growing and cherry-picked profitable routes. — Source: Greg Speicher

- On Abbott Laboratories: The protection of large-molecule drugs like Humira makes them much harder for generics to copy than traditional pills. — Source: Greg Speicher

- On OneMain Holdings: Underwriting discipline in the non-prime market allows the franchise to maintain resilience throughout credit cycles. — Source: Scribd

- On Elevance Health: Stable recurring revenue and dominant market share in managed care provide a moat that is regulatory-adaptable. — Source: Scribd

- On TD SYNNEX: Massive supply-chain scale creates a competitive barrier that generates significant free cash flow in technology logistics. — Source: Scribd

- On Comcast: Activism should focus on pushing management to use free cash flow for buybacks rather than dilutive acquisitions. — Source: Hedge Fund Alpha

Part 7: Learning from Mistakes and Complexities

- On Unlimited Pricing Power: "Nobody has unlimited pricing power," and pushing it too far can trigger permanent regulatory or social backlash. — Source: Masters Invest

- On Endowment Bias: Investors must avoid the psychological trap of overvaluing an asset simply because they already own it. — Source: Masters Invest

- On Complex Roll-Ups: When a company’s success depends entirely on the flawless execution of constant acquisitions, the margin of safety is thin. — Source: Masters Invest

- On Debt Risks: It is not prudent to have a massive position in a complex company that carries a large amount of debt. — Source: Masters Invest

- On Management Reliance: Avoid placing too much faith in the "genius" of a single manager to overcome poor industry economics. — Source: Hedge Fund Alpha

- On Shorting: Shorting during periods of government intervention is extremely dangerous, as seen with the 2008 financial crisis. — Source: Hedge Fund Alpha

- On Retail Challenges: Even the best managers cannot always overcome the structural decline of a dying industry like traditional retail. — Source: Hedge Fund Alpha

- On Objectivity: You must constantly re-evaluate your holdings as if you did not already own them to maintain objective judgment. — Source: Masters Invest

- On Thesis Breaks: When the original reason for buying a stock is proven wrong, an investor must be willing to "kill their darlings" immediately. — Source: Masters Invest

Part 8: The Investor's Mindset and Career

- On Career Preparation: Aspiring investors should spend ten years working for others to internalize the numbers before starting their own firm. — Source: Substack

- On Simplicity Mandates: If a thesis cannot be explained to a tenth-grader in a single paragraph, it is likely too complex to be safe. — Source: Greg Speicher

- On Firm Management: Avoid excessive marketing; it is better to have a small group of clients who understand and self-select into your process. — Source: GuruFocus

- On Experience: Long-term success requires the ability to distinguish between a temporary market mirage and an enduring business franchise. — Source: Greg Speicher

- On Common Sense: The most effective tools for valuation are common sense and a basic understanding of human behavior. — Source: GuruFocus

- On Intellectual Honesty: One must be honest about what they don't know, such as the complexities of foreign accounting or politics. — Source: GuruFocus

- On Domestic Focus: Concentrating on U.S. markets allows for a higher level of confidence in accounting rules and legal protections. — Source: GuruFocus

- On Franchise Value: Always focus on what the business will look like in five years rather than the fluctuations of next year's earnings. — Source: ValueInvesting.de

- On Being Iconoclastic: Successful investing requires the discipline to follow a simple, independent path regardless of the broader market trends. — Source: GuruFocus