Lessons from Gregory Zuckerman

Financial journalist Gregory Zuckerman investigates how outsiders navigate complex systems in markets, energy, and medicine. He is known for deeply reported books that unpack the mechanics behind Jim Simons' quantitative trading, John Paulson's housing short, and the race to develop mRNA vaccines. This compilation collects his observations on how these unconventional thinkers manage extreme risk.

Part 1: The Mathematics of the Market

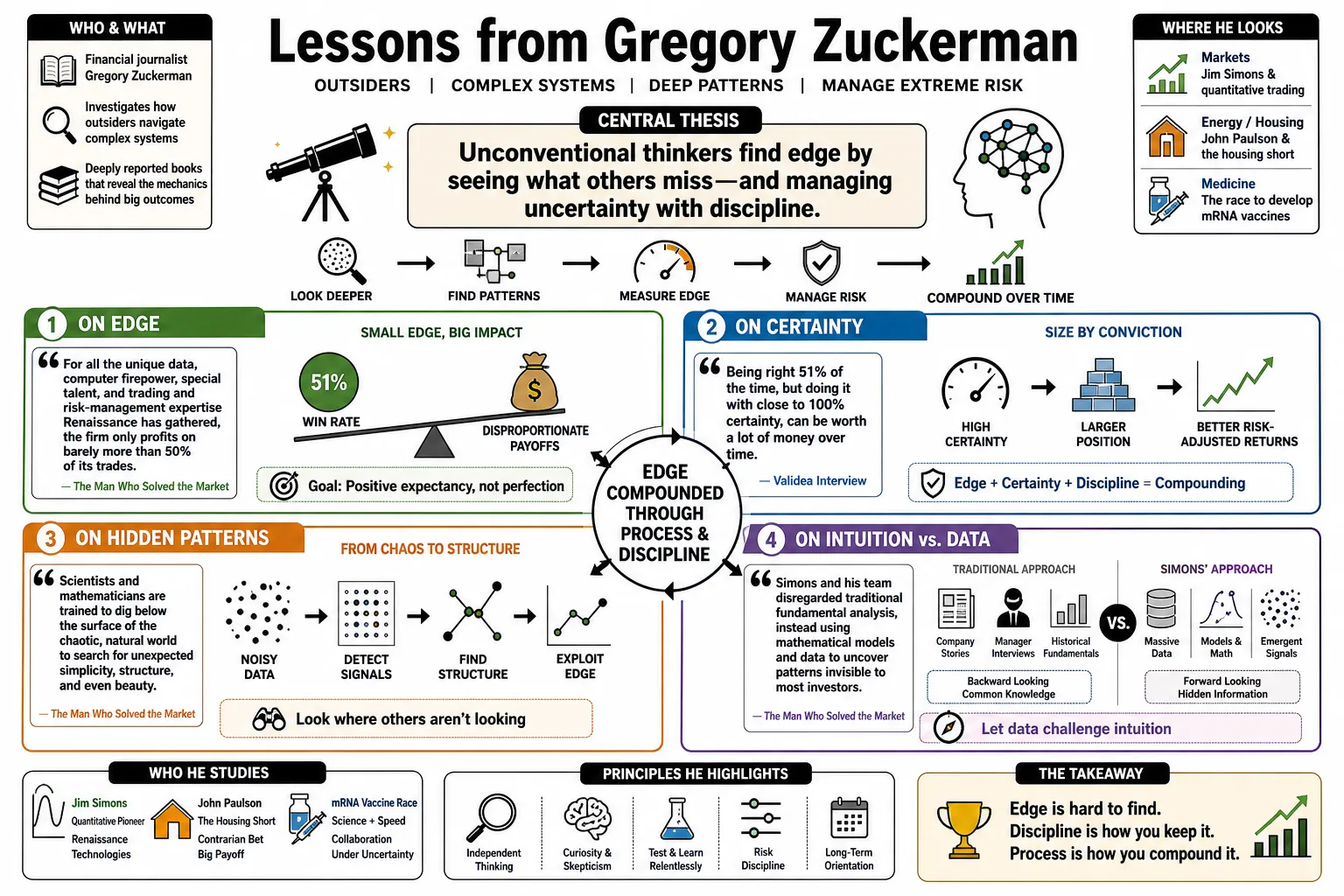

- On Edge: "For all the unique data, computer firepower, special talent, and trading and risk-management expertise Renaissance has gathered, the firm only profits on barely more than 50 percent of its trades." — Source: The Man Who Solved the Market

- On Certainty: "Being right 51% of the time, but doing it with close to 100% certainty, can be worth a lot of money over time." — Source: Validea Interview

- On Hidden Patterns: "Scientists and mathematicians are trained to dig below the surface of the chaotic, natural world to search for unexpected simplicity, structure, and even beauty." — Source: The Man Who Solved the Market

- On Intuition vs. Data: "Simons and his team disregarded traditional fundamental analysis, instead using mathematical algorithms to identify hidden, often non-intuitive, patterns in market data." — Source: Medium Book Review

- On Unified Systems: "Despite the immense complexity of their models, the firm prioritized a unified, monolithic approach to test new signals." — Source: A Wealth of Common Sense

- On High-Frequency Trading: "While Renaissance holds many positions for relatively short periods, they do not engage in typical High-Frequency Trading." — Source: Masters in Business

- On Winning Fractions: "We're right 50.75 percent of the time... but we're 100 percent right 50.75 percent of the time. You can make billions that way." — Source: The Man Who Solved the Market

- On Algorithm Design: "The Medallion fund's performance blows away other legendary investors like Warren Buffett, driven purely by an algorithmic approach." — Source: Rational Reminder Podcast

- On Structural Efficiency: "The market is generally efficient, but there are anomalies and behavioral biases that mathematical models can exploit if you have the computing power." — Source: Two Blokes Trading

- On Capacity Constraints: "Renaissance maintained its edge by capping the size of the Medallion Fund, preventing the performance degradation often seen in larger funds." — Source: Rational Reminder Podcast

Part 2: The Jim Simons Method

- On Beauty in Data: "Be guided by beauty... it can be the way a company runs, or the way an experiment comes out, or the way a theorem comes out, but there's a sense of beauty when something is working well." — Source: The Man Who Solved the Market

- On Talent Acquisition: "Simons famously recruited scientists, mathematicians, and PhDs from outside the world of finance, valuing raw intellectual ingenuity over traditional Wall Street experience." — Source: InvestmentNews

- On Privacy: "God gave me a tail to keep off the flies. But I'd rather have had no tail and no flies." — Source: The Man Who Solved the Market

- On Life Choices: "Do what you like in life, not what you feel you 'should' do. It's something I never forgot." — Source: Scribd Reviews

- On Retention: "Simons used the Medallion fund as an ultimate talent attraction and retention tool, returning outside capital and allowing only employees to participate." — Source: The Big Picture

- On Luck and Skill: "While Simons is a stock market genius, his success was also built on a probabilistic approach that embraced the realities of luck." — Source: Rational Reminder Podcast

- On Academic Culture: "He managed Renaissance more like a university math department than a traditional hedge fund, encouraging collaboration and open debate." — Source: Masters in Business

- On Delegation: "Simons was comfortable hiring people smarter than himself in specific domains and letting them build the systems." — Source: Two Blokes Trading

- On Crisis Persistence: "The initial versions of their models failed to beat the market; it took years of refining before the Medallion fund achieved its famous consistency." — Source: The Man Who Solved the Market

Part 3: The Greatest Trade and Contrarian Bets

- On Independent Thinking: "Paulson relied on meticulous research to conclude that the U.S. housing market was a ticking time bomb, ignoring colleagues who dismissed his ideas." — Source: The Greatest Trade Ever

- On Conviction: "Before the market collapsed in 2007, Paulson’s fund initially lost tens of millions of dollars. Rather than backing down, he redoubled his bet." — Source: HF Law Report

- On Scale: "It was the largest one-year payout in the history of the financial markets." — Source: The Greatest Trade Ever

- On Financial Engineering: "Complex instruments like credit default swaps allowed investors to profit from the housing decline, functioning as insurance policies that paid out when mortgage-backed securities defaulted." — Source: The Guardian

- On Timing: "Being early and right is often insufficient in the markets; success requires the capital and patience to survive until the thesis plays out." — Source: Scribd Reviews

- On The Human Element: "He was still special to John Paulson, after all... 'Wow,' his wife said quietly, still staring at the ATM which showed a balance of $45 million." — Source: The Greatest Trade Ever

- On Contrarianism: "The central theme is Paulson’s willingness to act as a renegade when the rest of Wall Street was intoxicated by housing profits." — Source: HF Law Report

- On Asymmetric Bets: "The genius of the trade was finding an instrument where the downside was a fixed premium but the upside was a multiple of the initial investment." — Source: A Simple Model

- On the Aftermath: "It is incredibly difficult to achieve market-beating performance consistently after a massive windfall, as the market environment and the trader's psychology shift." — Source: Rational Reminder Podcast

- On Recognizing Bubbles: "When ordinary people start treating homes as speculative instruments rather than places to live, the fundamental rules of the market have broken down." — Source: The Greatest Trade Ever

Part 4: The Fracking Revolution

- On Motivations: "The successes of the architects of the shale era are attributable to creativity, bravado, and the strong desire to get really wealthy." — Source: EconTalk

- On Disruption: "The really crazy thing was that it was Oryx leading the pack, not bigger companies like Exxon, Mobil, and Amoco." — Source: The Frackers

- On Corporate Blindspots: "Major firms had largely dismissed the potential of domestic shale, believing that major elephant fields in the U.S. were exhausted." — Source: QuoteFancy

- On Economics: "Rates of return get pretty minimal below fifty dollars." — Source: Forbes

- On Geopolitics: "The revolution transformed the U.S. into the world's leading energy producer, reducing dependence on foreign oil and diminishing the leverage of OPEC." — Source: WWSG

- On American Culture: "It's still a huge part of our culture, that it's okay to get rich. And as you say, we still have some private property rights that allow wildcatting." — Source: EconTalk

- On Skepticism: "These innovators were often ridiculed by industry experts and colleagues, proving that determined individuals can alter global landscapes despite consensus." — Source: Carnegie Council

- On Work Ethic: "He couldn't understand why union rules prevented him from helping others at the refinery, or allowed employees to sleep on the job and then complain." — Source: The Frackers

- On Environmental Realities: "While fracking itself may not inherently contaminate groundwater, methane leaks are a valid concern that require stringent regulation." — Source: Forbes

Part 5: The Race for the Vaccine

- On Scientific History: "The first vaccines were, went and got yourself sick a little bit, not too much... you want to protect yourself from smallpox, give yourself some. Crazy idea." — Source: EconTalk

- On mRNA Innovation: "Over time, we realized that while the traditional approach is not always the best... it just takes a really long time to manufacture those kinds of vaccines." — Source: EconTalk

- On Outsiders: "The breakthroughs were often the result of years of overlooked research by daring, deranged, and damaged visionaries who stuck with mRNA when it was dismissed." — Source: Hoover Institution

- On Luck and Timing: "While the talent of the scientists was paramount, success in drug development is never guaranteed and often involves a significant degree of luck." — Source: Strategy+Business

- On Corporate Clashes: Ohio State Wexner Medical Center described Zuckerman's vaccine reporting as based on more than 300 key players and access to research labs, corporate conversations, and government negotiations behind the COVID-19 vaccine race. — Reference: Ohio State Wexner panel page on Zuckerman's A Shot to Save the World reporting

- On Future Medicine: "The horror of the COVID-19 pandemic catalyzed a turning point for medical science, proving the viability of a new approach to medicine." — Source: Strategy+Business

- On Persistence: "The story is a testament to human innovation and the critical, messy processes that occur inside top-secret laboratories when the world is faced with a crisis." — Source: BAOS Publication

- On Human Elements: "The psychological defenses and internal corporate pressures heavily influenced the decision-making of key players during the frantic race." — Source: NIH Review

- On Operation Warp Speed: "Government funding served as a necessary catalyst to de-risk the manufacturing process, allowing companies to build capacity before the clinical trials were even finished." — Source: A Shot to Save the World

- On the Broader Scientific Community: "The success of mRNA technology is expected to attract increased talent, financing, and further breakthroughs in the coming decades." — Source: Goodreads Reviews

Part 6: The Psychology of Investing

- On Billionaire Psychology: "Power, isolation, and 'yes-men' dynamics can lead even the most successful investors to make fundamental mistakes." — Source: Two Blokes Trading

- On Following Smart Money: "Blindly following 'smart money' hedge fund advice is dangerous, as their structural advantages and risk profiles differ entirely from retail investors." — Source: Rational Reminder Podcast

- On Acknowledging Error: "The best investors are completely devoid of ego when a trade goes against them; they care about making money, not proving their initial thesis right." — Source: Invest Resolve

- On Information Asymmetry: "Retail investors cannot compete on speed or data with quantitative funds; they must compete on time horizon and temperament." — Source: Two Blokes Trading

- On Overconfidence: "Past success in one domain, whether it is distressed debt or macro trading, often breeds an overconfidence that proves fatal in unfamiliar markets." — Source: Masters in Business

- On Navigating Losses: "How an investor handles a 20 percent drawdown tells you more about their long-term viability than how they handle a 100 percent gain." — Source: Rational Reminder Podcast

- On the Illusion of Control: "Investors frequently confuse a bull market with their own strategic genius, ignoring the macroeconomic tailwinds pushing their portfolios higher." — Source: Two Blokes Trading

- On Contrarian Exhaustion: "Being a contrarian is intellectually satisfying but emotionally exhausting, as you must endure periods where you look like an absolute fool." — Source: HF Law Report

- On Wealth and Satisfaction: "Many of the individuals who conquer the market find that the wealth itself does not resolve their underlying restlessness or drive." — Source: Masters in Business

Part 7: Financial Journalism and Investigation

- On Journalistic Impact: "You go through life hoping to have a chance to make a difference. I'm just grateful to have the strength left to have an impact." — Source: QuoteFancy

- On the Role of AI: "AI acts as a tool for clarity and craftsmanship in the writing process, even when only a fraction of its output is ultimately useful." — Source: Two Blokes Trading

- On Human Connection: In Two Blokes Trading, Zuckerman discusses AI as a useful but imperfect writing aid, while the episode frames thoughtful skepticism, accuracy, curiosity, persistence, and access to sources as essential to high-stakes financial journalism. — Reference: Two Blokes Trading interview with Gregory Zuckerman on AI, skepticism, sources, and financial journalism

- On Finding the Story: "The real story is rarely in the press release; it is hidden in the friction between what people say publicly and what they do privately." — Source: Masters in Business

- On the Value of Skepticism: "A financial journalist must operate from a default position of polite skepticism, assuming that every figure has an agenda." — Source: Rational Reminder Podcast

- On Explaining Complexity: "The challenge of financial journalism is translating complex mathematical or legal realities into narratives that a layman can digest without losing the nuance." — Source: Two Blokes Trading

- On Access vs. Independence: "Gaining access to secretive billionaires requires building trust, but retaining independence requires the willingness to burn that bridge if the truth demands it." — Source: Masters in Business

- On Narrative Arc: "Behind every massive financial event is a deeply human story of ambition, fear, and rivalry." — Source: Invest Resolve

- On the Draft Process: "Writing a book requires enduring the messy middle, where the mountain of research feels entirely disconnected and overwhelming." — Source: Two Blokes Trading

Part 8: Innovation, Talent, and Risk

- On Outsider Perspectives: "True disruption rarely comes from the established giants of an industry; it comes from hungry outsiders who don't know the traditional boundaries." — Source: The Frackers

- On Evaluating Talent: "The best organizations do not hire for specific skills that will be obsolete in five years; they hire for raw processing power and intellectual curiosity." — Source: The Man Who Solved the Market

- On Taking Risks: "Safety in an established career often masks the long-term risk of irrelevance; taking a calculated leap is sometimes the most conservative choice." — Source: A Shot to Save the World

- On the Nature of Consensus: "When all the experts in a room agree that something is impossible, they are usually describing a limitation of their own methodology, not a law of physics." — Source: EconTalk

- On Resilience: "The defining characteristic of the pioneers across finance, energy, and medicine is their ability to absorb repeated public failure." — Source: Hoover Institution

- On Incentive Structures: "If you want to understand why a company is failing to innovate, look at how it compensates its middle management." — Source: Masters in Business

- On Cross-Disciplinary Thinking: "Breakthroughs often occur at the intersection of different fields, where a concept from physics is applied to finance, or a concept from computing is applied to biology." — Source: The Man Who Solved the Market

- On Managing Geniuses: "You cannot manage a team of eccentrics with traditional corporate rules; you must provide them with the infrastructure to play and the freedom to be weird." — Source: The Big Picture

- On Legacy: "The people who leave a lasting mark are those who are driven by a burning obsession to solve a puzzle, rather than merely a desire for status." — Source: Rational Reminder Podcast