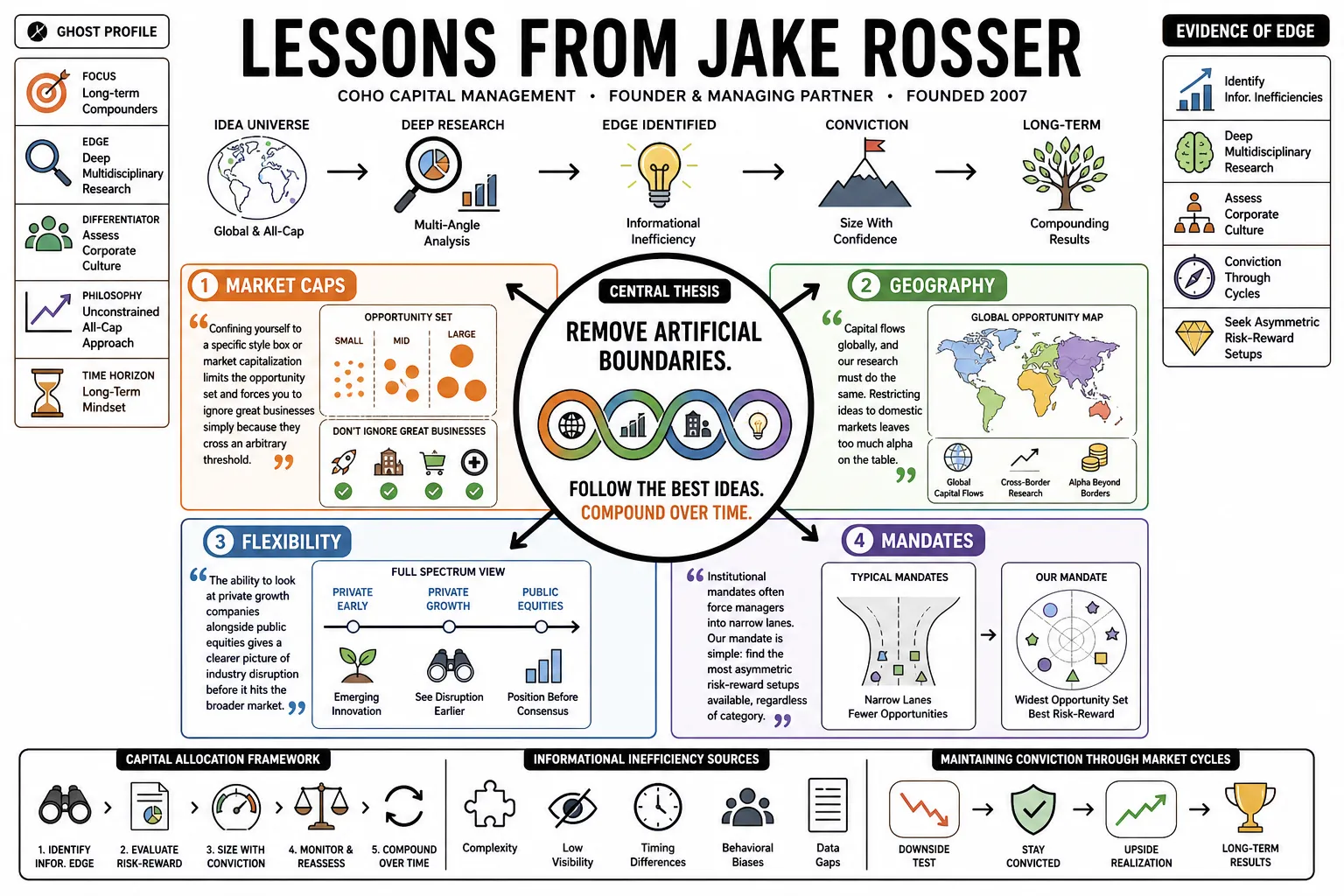

Jake Rosser is the founder and managing partner of Coho Capital Management, an investment firm he started in 2007. He is known for an unconstrained, all-cap investment approach that prioritizes long-term compounders, deep multidisciplinary research, and assessing corporate culture. This profile compiles his frameworks on capital allocation, identifying informational inefficiencies, and maintaining conviction through market cycles.

Part 1: Unconstrained Investing

- On Market Caps: "Confining yourself to a specific style box or market capitalization limits the opportunity set and forces you to ignore great businesses simply because they cross an arbitrary threshold." — Source: [MOI Global Interview]

- On Geography: "Capital flows globally, and our research must do the same. Restricting ideas to domestic markets leaves too much alpha on the table." — Source: [Investment Masters Class]

- On Flexibility: "The ability to look at private growth companies alongside public equities gives a clearer picture of industry disruption before it hits the broader market." — Source: [Latticework Interview]

- On Mandates: "Institutional mandates often force managers into narrow lanes. Our mandate is simple: find the most asymmetric risk-reward setups available, regardless of category." — Source: [Coho Capital 2021 Annual Letter]

- On Stage Agnosticism: "Evaluating a mature cash-generator requires a different lens than a hyper-growth compounder, but the core question remains the same: how much cash will this asset produce over its life?" — Source: [Investment Masters Class]

- On Benchmarks: "Benchmarking against a specific index often leads to closet indexing. True active management means your portfolio should look nothing like the index." — Source: [MOI Global Interview]

- On Sector Limits: "We don't try to fill out a portfolio with representation from every sector. If a sector lacks companies with durable competitive advantages, we simply don't invest there." — Source: [Coho Capital 2020 Performance Review]

- On Idea Generation: "The best ideas rarely come from screening tools. They come from reading broadly across industries and observing where value is migrating." — Source: [Latticework Interview]

- On Structural Advantages: "Our size and structure allow us to traffic in smaller, less liquid names that large funds cannot buy without moving the market." — Source: [MOI Global Interview]

Part 2: Multidisciplinary Thinking

- On Reading Habits: "Investing is fundamentally a multidisciplinary endeavor. You cannot build conviction solely by reading 10-Ks; you have to study history and behavioral psychology." — Source: [Latticework Interview]

- On Mental Models: "Relying on a single framework for evaluating businesses is dangerous. You need a lattice of mental models to avoid forcing a square peg into a round hole." — Source: [Investment Masters Class]

- On Synthesizing Information: "The edge in modern markets is rarely having better data. It is the ability to synthesize disparate pieces of public information into a coherent thesis." — Source: [MOI Global Interview]

- On Pattern Recognition: "Studying past business failures is often more instructive than studying successes. It helps build a mental database of red flags." — Source: [Coho Capital 2021 Annual Letter]

- On Intellectual Curiosity: "If you view research as a chore rather than a natural extension of your curiosity, you will eventually burn out or get outworked by someone who doesn't." — Source: [Latticework Interview]

- On First Principles: "When evaluating a new technology or business model, strip away the narrative and ask whether the unit economics make sense from a physics or math perspective." — Source: [Investment Masters Class]

- On Cross-Pollination: "Insights from studying consumer behavior can often be applied to enterprise software sales. Human psychology remains the common denominator." — Source: [MOI Global Interview]

- On Avoiding Echo Chambers: "Talking only to other investors leads to consensus thinking. I get more value from speaking with industry operators and former employees." — Source: [Coho Capital 2020 Performance Review]

- On Continuous Learning: "The half-life of knowledge in some sectors is incredibly short. Your research process must be dynamic enough to update priors as new facts emerge." — Source: [Latticework Interview]

Part 3: Identifying Compounders

- On Moats: "A competitive advantage is only as good as its durability. If a moat is widening, the current valuation often understates the company's true worth." — Source: [Coho Capital 2021 Annual Letter]

- On Reinvestment Rates: "The holy grail of investing is a business that can reinvest large amounts of capital at high rates of return for a long time." — Source: [MOI Global Interview]

- On Total Addressable Market (TAM): "Companies often define their TAM too broadly to appease investors. We look for businesses with high penetration in a specific, growing niche before they expand adjacently." — Source: [Investment Masters Class]

- On Network Effects: "Once a business achieves a true network effect, the cost to acquire the next customer drops precipitously, leading to non-linear margin expansion." — Source: [Coho Capital 2020 Performance Review]

- On Switching Costs: "High switching costs create a captive customer base, allowing a company to raise prices at or above the rate of inflation without losing volume." — Source: [S&P Global: A Collection of Great Businesses]

- On Organic Growth: "We prefer businesses that grow organically through product excellence rather than those that rely heavily on debt-fueled roll-ups." — Source: [Latticework Interview]

- On Scalability: "Software and asset-light models are attractive because revenue can double or triple with only a marginal increase in operating expenses." — Source: [MOI Global Interview]

- On Capital Intensity: "Heavy capital requirements act as a drag on compounding. We actively seek out businesses with low capital intensity and high free cash flow conversion." — Source: [Coho Capital 2021 Annual Letter]

- On Predictability: "A high degree of recurring revenue allows management to plan for the long term instead of managing earnings quarter-to-quarter." — Source: [Investment Masters Class]

- On Unit Economics: "If the unit economics are flawed, scaling the business will only accelerate cash burn. Profitability must work at the micro level first." — Source: [Coho Capital 2020 Performance Review]

Part 4: The Role of Culture

- On Management Alignment: "We look for management teams that have a significant portion of their net worth tied up in the company. Skin in the game changes behavior." — Source: [MOI Global Interview]

- On Decentralization: "Organizations that push decision-making down to the lowest possible level tend to move faster and respond better to local market conditions." — Source: [Latticework Interview]

- On Brookfield's Culture: "Brookfield Asset Management exemplifies how a strong culture of ownership and contrarian capital allocation can drive decades of outperformance." — Source: [Coho Capital 2021 Annual Letter]

- On Founder-Led Companies: "Founders often retain a long-term mindset and a willingness to cannibalize existing product lines to secure the company's future, traits rarely found in hired CEOs." — Source: [Investment Masters Class]

- On Compensation Structures: "Show me the incentive, and I will show you the outcome. We avoid companies where executives are rewarded for short-term stock price bumps rather than return on invested capital." — Source: [MOI Global Interview]

- On Corporate Bureaucracy: "As companies scale, bureaucracy is the natural enemy of innovation. We try to identify firms that maintain a day-one mentality despite their size." — Source: [Coho Capital 2020 Performance Review]

- On Employee Retention: "High turnover is a silent tax on a business. Companies that treat their employees well usually enjoy lower training costs and higher productivity." — Source: [Latticework Interview]

- On Transparency: "Management teams that speak candidly about their mistakes earn our trust. Those that blame external factors for poor execution are an immediate red flag." — Source: [Coho Capital 2021 Annual Letter]

- On Capital Allocation Skills: "A CEO's primary job is capital allocation, yet most reach the top based on operational skills. We seek leaders who understand how to deploy capital efficiently." — Source: [Investment Masters Class]

Part 5: Informational Inefficiencies

- On Market Efficiency: "Markets are mostly efficient, but they systematically misprice businesses undergoing complex structural changes or temporary distress." — Source: [MOI Global Interview]

- On Time Arbitrage: "The most persistent edge available to public market investors is time arbitrage: the willingness to hold an asset for three to five years while others obsess over the next quarter." — Source: [Coho Capital 2021 Annual Letter]

- On Spinoffs: "Corporate spinoffs frequently create forced selling by institutions, generating opportunities for those willing to do the work on the newly independent entity." — Source: [Investment Masters Class]

- On Complexity: "Complicated capital structures or dense accounting often scare away casual analysts, leaving mispriced assets for those willing to parse the footnotes." — Source: [Latticework Interview]

- On Contrarianism: "Being a contrarian for its own sake is a quick way to lose money. You must be contrarian and right, which requires a variant perception backed by facts." — Source: [MOI Global Interview]

- On Hidden Assets: "Real estate and under-monetized data sets are frequently ignored by models that focus strictly on near-term earnings." — Source: [Coho Capital 2020 Performance Review]

- On Institutional Constraints: "Large funds cannot invest in micro-caps due to size constraints. This artificial limit creates a structural inefficiency at the bottom of the market capitalization spectrum." — Source: [Investment Masters Class]

- On Geographic Blindspots: "U.S. investors often apply domestic multiples to international businesses without accounting for local market dominance or regulatory environments." — Source: [Latticework Interview]

- On Evaluating Intangibles: "Traditional accounting treats R&D and customer acquisition as expenses rather than investments, masking the true underlying profitability of modern digital businesses." — Source: [Coho Capital 2021 Annual Letter]

- On Primary Research: "Reading broker reports is a waste of time. Your edge comes from calling suppliers, former executives, and competitors to build an independent mosaic." — Source: [MOI Global Interview]

Part 6: Market Volatility and Patience

- On Drawdowns: "Volatility is a feature of public markets, not a bug. If you cannot stomach a 30 percent drawdown in a high-quality name, you will never realize its long-term compounding benefits." — Source: [Coho Capital 2021 Annual Letter]

- On Inactivity: "Most of the time, the correct action in investing is to do absolutely nothing. Over-trading is a tax on your returns." — Source: [Investment Masters Class]

- On Market Timing: "We do not attempt to time the macroeconomic cycle. We prefer to buy businesses that can survive a recession and emerge with higher market share." — Source: [MOI Global Interview]

- On Cash Balances: "Holding cash in a zero-interest environment is painful, but it is necessary dry powder to exploit the inevitable dislocations when panic sets in." — Source: [Latticework Interview]

- On Averaging Down: "Adding to a losing position is dangerous unless your original thesis remains intact and the intrinsic value of the business has genuinely grown." — Source: [Coho Capital 2020 Performance Review]

- On Noise: "The daily financial news cycle is designed to provoke anxiety and prompt action. Turning off the screen and reading a book is often the best defense." — Source: [Investment Masters Class]

- On Selling Winners: "Trimming a position simply because it has doubled is a mistake if the underlying fundamentals continue to compound at a high rate." — Source: [MOI Global Interview]

- On Patience: "It takes years for a thesis to fully play out. The gap between recognizing a mispricing and the market correcting it tests your conviction." — Source: [Coho Capital 2021 Annual Letter]

- On Surviving: "The primary rule of compounding is to never interrupt it unnecessarily. To finish first, you must first finish." — Source: [Latticework Interview]

Part 7: Assessing Quality

- On Pricing Power: "The single most important metric when evaluating a business is pricing power. If you have to hold a prayer session before raising prices, you have a terrible business." — Source: [S&P Global: A Collection of Great Businesses]

- On S&P Global: "S&P Global is the quintessential toll bridge. It operates in an oligopoly where debt issuers must pay for ratings regardless of the economic environment." — Source: [S&P Global: A Collection of Great Businesses]

- On Margins: "High gross margins indicate that customers value the product significantly more than it costs to produce, providing a buffer against input inflation." — Source: [Investment Masters Class]

- On Commodities: "We generally avoid companies that sell undifferentiated products. If you compete solely on price, you are entirely at the mercy of the macro cycle." — Source: [MOI Global Interview]

- On Franchise Value: "A strong brand lowers customer acquisition costs and provides a baseline level of demand even when competitors launch similar products." — Source: [Coho Capital 2020 Performance Review]

- On Industry Structure: "We prefer fragmented industries where a well-capitalized, disciplined operator can consolidate competitors and drive margin expansion." — Source: [Latticework Interview]

- On Customer Captivity: "When a software product integrates deeply into a customer's daily workflow, removing it becomes an operational hazard. That is the definition of stickiness." — Source: [Coho Capital 2021 Annual Letter]

- On Value Proposition: "The best businesses offer a product that costs a fraction of a customer's total budget but provides an outsized benefit to their operations." — Source: [S&P Global: A Collection of Great Businesses]

- On R&D: "Companies that consistently outspend their peers on research and development often widen their moats invisibly before it shows up in the revenue numbers." — Source: [Investment Masters Class]

- On Capital Returns: "Share repurchases are only value accretive if the stock is trading below intrinsic value. Otherwise, management is destroying shareholder wealth." — Source: [MOI Global Interview]

Part 8: The Psychology of Investing

- On Discipline: "The hardest part of value investing is not the math; it is maintaining the discipline to hold your cash when nothing meets your criteria." — Source: [Coho Capital 2021 Annual Letter]

- On Confirmation Bias: "It is easy to find evidence that supports your thesis. The real work is actively seeking out disconfirming evidence to stress-test your assumptions." — Source: [Latticework Interview]

- On Humility: "The market has a way of humbling anyone who thinks they have it entirely figured out. Acknowledge your mistakes quickly and move on." — Source: [Investment Masters Class]

- On Emotional Control: "Intellect gets you to the starting line, but emotional temperament dictates whether you cross the finish line. Panic selling is the destruction of capital." — Source: [MOI Global Interview]

- On Envy: "Watching other people get rich on speculative assets is a psychological test. You have to stay focused on your own process and ignore the noise." — Source: [Coho Capital 2020 Performance Review]

- On Overconfidence: "A few years of outperformance can breed dangerous arrogance. Keep your position sizing grounded in reality, not recent success." — Source: [Latticework Interview]

- On Independence: "If you need the validation of the crowd to hold a position, you will never capture the outsized returns that come from being early and alone." — Source: [Investment Masters Class]

- On Decision Fatigue: "We keep our portfolios concentrated because tracking 50 different companies dilutes your attention and degrades the quality of your decision-making." — Source: [MOI Global Interview]

- On Long-Term Thinking: "Most errors in investing stem from shrinking your time horizon to match the market's anxiety. Stretch your perspective to decades, and the math changes completely." — Source: [Coho Capital 2021 Annual Letter]