Lessons from Jeremy Grantham

Jeremy Grantham co-founded the investment firm GMO and made his name studying financial bubbles and mean reversion. He has since directed his wealth and focus toward climate change and environmental decay. This collection outlines his views on how markets behave at the extremes and why capitalism struggles to handle slow-moving planetary crises.

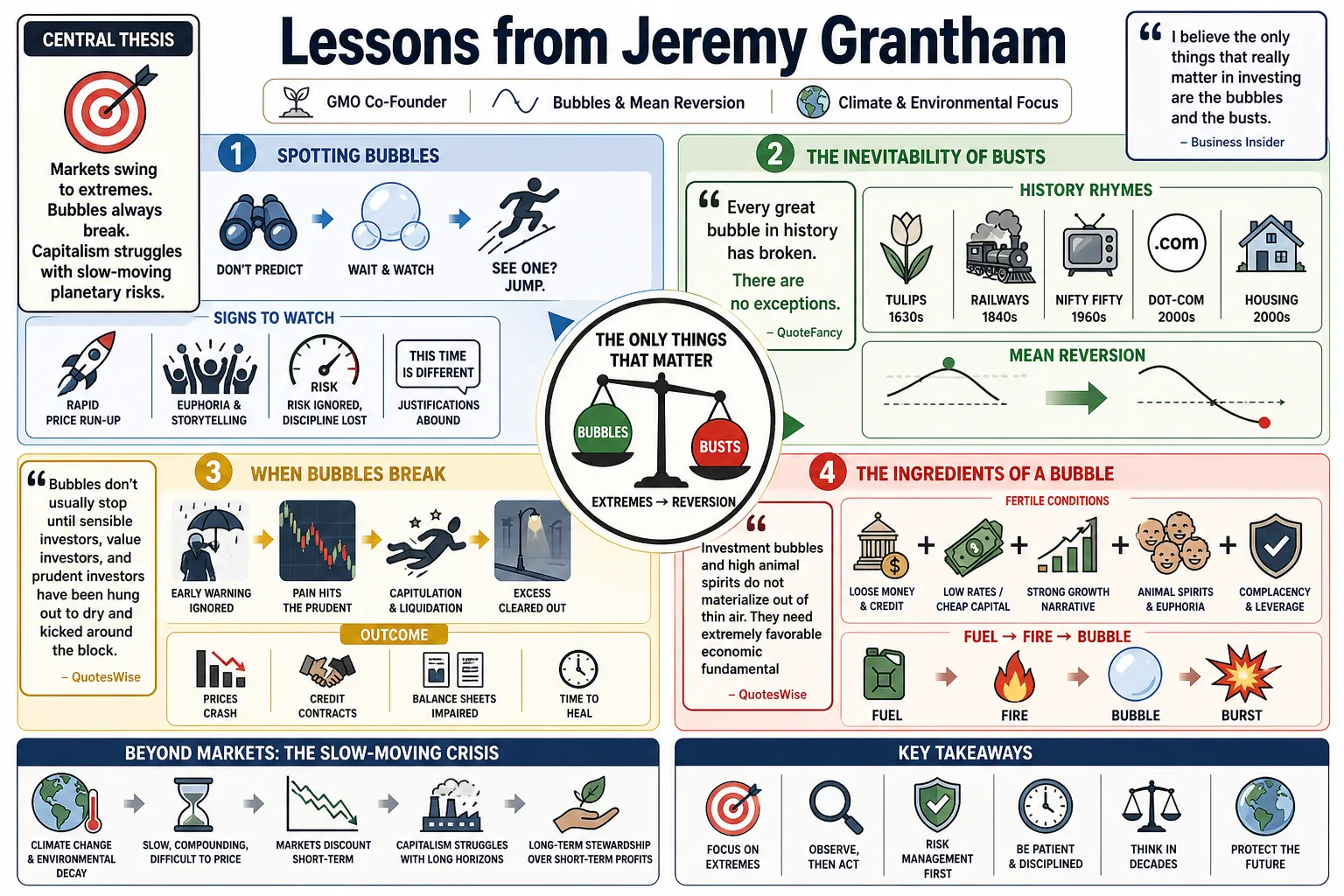

Part 1: Identifying Market Bubbles

- On The Only Things That Matter: "I believe the only things that really matter in investing are the bubbles and the busts." — Source: Business Insider

- On Spotting Bubbles: "The nice thing about bubbles is you don't have to predict them, you just wait and see. And when you see one you jump." — Source: QuotesWise

- On The Inevitability of Busts: "Every great bubble in history has broken. There are no exceptions." — Source: QuoteFancy

- On When Bubbles Break: "Bubbles don't usually stop until sensible investors, value investors, and prudent investors have been hung out to dry and kicked around the block." — Source: QuotesWise

- On The Ingredients of a Bubble: "Investment bubbles and high animal spirits do not materialize out of thin air. They need extremely favorable economic fundamentals together with free and easy, cheap credit, and they need it for at least two or three years." — Source: AZQuotes

- On The Everything Bubble: "The trouble with this bubble is it's an everything bubble." — Source: Business Insider

- On Volatility as a Symptom: "Volatility is a symptom that people have no idea of the underlying value—that they have stopped playing the asset game. They're buying because the price is rising." — Source: AZQuotes

- On The Late Stage: The final phase of a bubble is characterized by explosive, nearly vertical price increases that are completely divorced from any fundamental economic improvement. — Source: GMO Quarterly Letter

- On Rationality During Bubbles: Maintaining a rational view during a euphoric bubble guarantees that you will look like a fool to the rest of the market until the break finally happens. — Source: Institutional Investor

- On The Pressure to Be Bullish: "There is an enormous pressure in the investment business to deliver good news... To go out there in a bubble and talk about badly overpriced markets and downside risks is an invitation to get fired." — Source: QuotesWise

Part 2: The Gravity of Mean Reversion

- On The Most Dependable Force: "I used to call profit margins the most dependably mean-reverting series in finance. And they were through 1997." — Source: Bookey

- On Glorious Inefficiency: "The market is gloriously inefficient and wanders far from fair price but eventually, after breaking your heart and your patience... it will go back to fair value." — Source: Business Insider

- On The Strength of Value: "Although value is a weak force in any single year, it becomes a monster over several years. Like gravity, it slowly wears down the opposition." — Source: AZQuotes

- On The Four Most Dangerous Words: "We value investors have bored momentum investors for decades by trotting out the axiom that the four most dangerous words are, 'This time is different.'" — Source: Fortune Financial Advisors

- On The Corollary to Dangerous Words: "Conversely, it can be very dangerous indeed to assume that things are never different." — Source: Fortune Financial Advisors

- On Regression to the Mean: If you believe in history, you must believe that extreme outliers will eventually regress to their long-term average over time. — Source: GMO Quarterly Letter

- On The Speed of Reversion: Mean reversion is a certainty in finance, but the timeline over which it occurs is entirely out of the investor's control. — Source: Institutional Investor

- On Surviving the Wait: "Your task is to survive until [mean reversion] happens." — Source: Business Insider

- On The Numbers Winning: In the end, despite all narrative and hype, the fundamental numbers will win out against market sentiment. — Source: GMO Quarterly Letter

- On The Delusion of New Eras: Every market cycle features proponents of a new era paradigm, and every cycle ends with mean reversion asserting its mathematical dominance. — Source: Institutional Investor

Part 3: Value Investing Principles

- On Buying Cheap Assets: "You don't get rewarded for taking risk; you get rewarded for buying cheap assets." — Source: AZQuotes

- On The Punishment of Risk: "And if the assets you bought got pushed up in price simply because they were risky, then you are not going to be rewarded for taking a risk; you are going to be punished for it." — Source: AZQuotes

- On The Definition of an Idiot: "If stocks are attractive and you don't buy, you don't just look like an idiot, you are an idiot." — Source: QuoteFancy

- On Market Timing: "Market timing, by the way, is a tag some buy-and-hold investors use to put down anything that involves using your brain." — Source: AZQuotes

- On The Discipline Excuse: "These are the same people who like to watch the locomotive coming and get run down in the name of discipline." — Source: AZQuotes

- On Avoiding Leverage: "If you borrow to invest, it will interfere with your survivability. Unleveraged portfolios cannot be stopped out, leveraged portfolios can." — Source: Business Insider

- On Diversification for Resilience: "Several different investments, the more the merrier, will give your portfolio resilience, the ability to withstand shocks." — Source: Business Insider

- On Focusing on What You Know: Try to strictly contain the number of your investments to those specific areas where you possess actual competence. — Source: GMO Quarterly Letter

- On Bravery at the Extremes: When the fundamental numbers reach extreme valuations, you must grit your teeth and act decisively against the crowd. — Source: GMO Quarterly Letter

Part 4: Patience and Risk Management

- On The Individual's Advantage: "The individual is far better-positioned to wait patiently for the right pitch while paying no regard to what others are doing, which is almost impossible for professionals." — Source: AZQuotes

- On Leverage as the Enemy: "Leverage reduces the investor’s critical asset: patience." — Source: Business Insider

- On Irrationality vs. Solvency: "The market can stay irrational longer than the investor can stay solvent." — Source: AZQuotes

- On Agency and Patience: "For us agents, [Keynes] might better have said 'The market can stay irrational longer than the client can stay patient.'" — Source: AZQuotes

- On The True Definition of Risk: "The biggest risk in investing is not volatility, but permanent loss of capital." — Source: Bookey

- On Embracing Volatility: Volatility should be welcomed by the patient value investor as the sole mechanism that occasionally offers mispriced assets. — Source: GMO Quarterly Letter

- On The Futility of Predictions: You cannot predict the exact top or bottom of a cycle; effective risk management is about positioning yourself so you don't have to guess perfectly. — Source: Institutional Investor

- On Surviving Critical Periods: Portfolio construction must ensure you survive the critical periods when your largest bets temporarily move heavily against you. — Source: Business Insider

- On Ignoring the Crowd: True patience requires paying absolutely no regard to what the broader herd is doing, a feat structural constraints make nearly impossible for institutional managers. — Source: AZQuotes

Part 5: Career Risk and Institutional Herding

- On The Central Truth of Investing: "The central truth of the investment business is that investment behavior is driven by career risk." — Source: GMO Quarterly Letter

- On The Cause of Herding: "This creates herding, or momentum, which drives prices far above or far below fair price." — Source: GMO Quarterly Letter

- On Institutional Constraints: Professionals are largely prevented from acting rationally at market extremes because looking wrong alone is the fastest way to get fired. — Source: Institutional Investor

- On Failing Conventionally: In the institutional finance world, it is overwhelmingly safer to fail conventionally than to succeed unconventionally. — Source: Institutional Investor

- On The Freedom of the Amateur: Amateurs possess a profound structural advantage over professionals simply because they cannot be fired for underperforming a benchmark in the short term. — Source: Business Insider

- On The Illusion of Expertise: Much of the financial industry's perceived expertise is merely the sophisticated packaging of safe, benchmark-hugging strategies. — Source: GMO Quarterly Letter

- On The Pressure to Participate: The institutional mandate to stay fully invested forces professional managers to participate in bubbles even when they know prices are absurd. — Source: QuotesWise

- On The Asymmetry of Rewards: The career rewards for calling a bubble correctly are vastly outweighed by the career destruction of being early and underperforming your peers. — Source: Institutional Investor

- On The Scarcity of True Value Managers: Genuine value managers are scarce because the business model of asset management rarely tolerates the extended periods of underperformance required to practice the strategy. — Source: GMO Quarterly Letter

Part 6: Climate Change as the Ultimate Risk

- On The Primary Challenge: "Climate change [is] the most important issue in the investing world for the next few decades." — Source: Morningstar

- On The Race of Our Lives: "We are in 'the race of our lives' to stave off the worst effects of climate change... It’s a race against time to mitigate the destabilizing consequences of global warming." — Source: Morningstar

- On Inevitable Decarbonization: "We will completely de-carbonize our economy this century, and it will be the biggest economic event since the Industrial Revolution." — Source: Advisor Perspectives

- On The Fate of Fossil Fuels: "Fossil fuels will either run out, destroy the planet, or both. The only possible way we can avoid this outcome is, frankly, to complete de-carbonize of our economy." — Source: Advisor Perspectives

- On The Green Opportunity: "I think the green VC will move the dial for our well-being as much as anything... How often do you get to do what you think is exactly the right thing to do and to make money?" — Source: GMO Climate Change Webcast

- On Environmental Toxicity: "I think we've made our planet unfavorable to life in every form including Homo sapiens... they threaten perhaps the existence of a stable Global Society." — Source: GMO Race of Our Lives Revisited

- On Chemicals vs. Climate: "I think chemicals will turn out to be a hotter button than climate change... we've created a toxic environment apparently not conducive to life." — Source: Advisor Perspectives

- On Unpleasant Data: "I find the parallels between how some investors refuse to recognize the trends and our reaction to some of our environmental challenges very powerful. There is an unwillingness to process unpleasant data." — Source: QuoteFancy

- On Fiddling While Rome Burns: "When we sit here discussing the stock market, we're a little like Emperor Nero fiddling while Rome burns." — Source: Morningstar

- On The Illusion of Stability: The physical foundations of our stable global society are being severely threatened by fast-moving environmental changes that markets refuse to price correctly. — Source: GMO Race of Our Lives Revisited

Part 7: Resource Depletion and the Finite Planet

- On The Fundamental Limit: "We live on a finite planet. We have finite resources, and we're running out of good, arable land." — Source: QuoteFancy

- On The Economic Blind Spot: "There is no single theory that is used in economics that considers the finite nature of resources. It's shocking." — Source: QuoteFancy

- On Modern Agriculture: "Modern agriculture has been accurately described as a way of turning oil into food." — Source: QuoteFancy

- On The Future of Food Prices: "As the price of oil continues to rise, so will the price of food." — Source: QuoteFancy

- On The Permanent Shift: "The world is using up its natural resources at an alarming rate, and this has caused a permanent shift in their value." — Source: Business Insider

- On Adjusting Behavior: "We all need to adjust our behavior to this new environment. It would help if we did it quickly." — Source: QuoteFancy

- On The End of Cheap Commodities: The century-long trend of broadly declining commodity prices has definitively ended as we begin hitting hard planetary extraction boundaries. — Source: GMO Quarterly Letter

- On Soil Degradation: The rapid depletion and chemical degradation of topsoil poses a catastrophic risk to future global food security that markets currently ignore. — Source: Advisor Perspectives

- On Resource Efficiency: The future global economy will be defined not by infinite extraction, but by radical efficiency and circular resource management out of pure necessity. — Source: Prime Coalition

Part 8: Capitalism, Externalities, and the Long View

- On Systemic Failure: "Capitalism's complete inability to deal with externalities, tragedies of the common, and the very long term helped cause these problems and is ill-suited to helping solve them." — Source: Morningstar

- On The Value of Grandchildren: "Anything that happens to a corporation over 25 years out doesn't exist for them; therefore, as I like to say, grandchildren have no value to them." — Source: Morningstar

- On Human Inertia: "The ability of Homo sapiens to avoid long-term, slow-burning issues is truly profound." — Source: Conversations with Tyler

- On The Flaws of GDP: Gross Domestic Product is a deeply flawed metric that routinely counts the rapid liquidation of our natural capital as a net increase in societal wealth. — Source: GMO Quarterly Letter

- On The Need for Government: Free markets are structurally incapable of pricing long-term existential risks; strong government regulation and intervention are absolutely required for planetary survival. — Source: Morningstar

- On The Cost of Growth: Infinite economic growth on a planet with strictly finite physical boundaries is a mathematical and physical impossibility that economists refuse to accept. — Source: Advisor Perspectives

- On Discount Rates: Applying standard financial discount rates to environmental catastrophes is a fundamental failure that guarantees we drastically underinvest in our own survival. — Source: GMO Quarterly Letter

- On True Wealth: True societal wealth is not measured by inflated paper asset prices, but by the health of our ecosystems, social stability, and sustainable infrastructure. — Source: Prime Coalition

- On The Ultimate Obligation: Investors with long horizons have a moral and financial obligation to direct their capital toward solving the existential crises threatening the habitability of the planet. — Source: GMO Sustainability or Bust