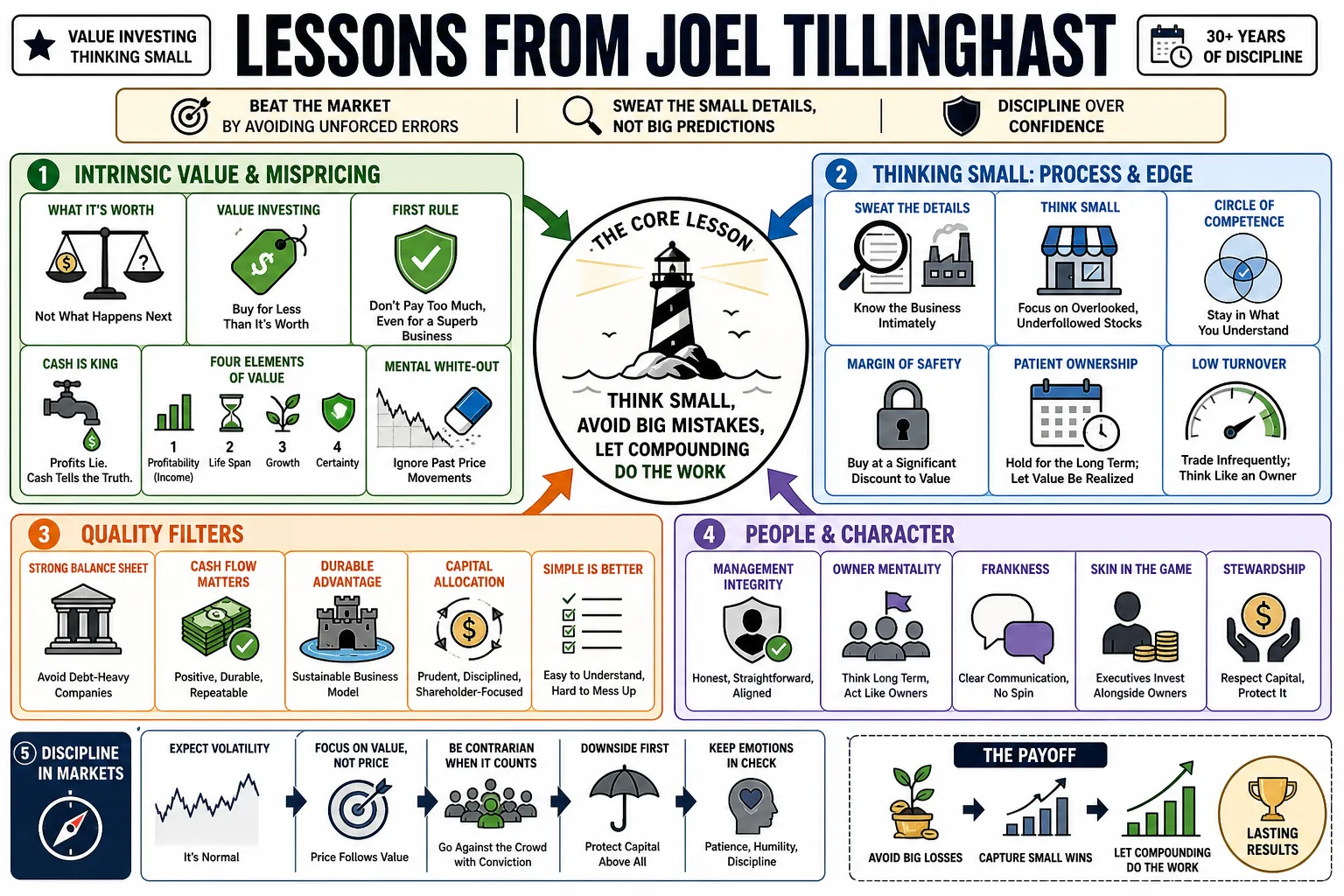

Lessons from Joel Tillinghast

Joel Tillinghast ran the Fidelity Low-Priced Stock Fund for over three decades, beating the market by avoiding unforced errors instead of chasing bold predictions. His "thinking small" approach relies on sweating granular business details, rejecting debt-heavy companies, and strictly respecting his own circle of competence. This collection outlines his practical rules for finding mispriced assets, judging management integrity, and staying disciplined when markets turn.

Part 1: Intrinsic Value and Mispricing

- On true value: "Invest based on 'What's it worth?' rather than 'What happens next?'" — Source: [Goodreads]

- On core definitions: "Value investing is buying something for less than it's worth, full stop." — Source: [Excess Returns Podcast]

- On the first rule of investing: "Don't pay too much, even for a superb business." — Source: [Fidelity]

- On cash flow reality: "When companies report profits but bleed cash, believe the cash." — Source: [Novel Investor]

- On the primary elements of value: "The four elements of value are (1) profitability or income, (2) life span, (3) growth, and (4) certainty." — Source: [Big Money Thinks Small]

- On ignoring price history: "Investors should apply a 'mental white-out' to a stock's past price movements to focus exclusively on whether it is undervalued relative to its future earnings." — Source: [Masters in Business]

- On missing the boat: "Never mistake a rapidly falling share price for a bargain without first confirming the intrinsic value and underlying cash flow." — Source: [The Investor's Podcast]

- On Wall Street's blind spots: "Boring, unglamorous stocks are often inefficiently priced because analysts are distracted by flashy, high-growth narratives." — Source: [Morningstar]

- On the momentum trap: "A common trap is switching to 'value' only after momentum stocks have crashed, rather than adhering to absolute intrinsic value." — Source: [Excess Returns Podcast]

- On filtering for value: "The good news is that stock pickers can outperform simply by cutting out the stuff that drags down returns." — Source: [Naos Asset Management]

Part 2: The Art of Thinking Small

- On reducing error severity: "A small mistake is generally easier to repair. Thinking small not only reduces the severity and frequency of errors, but also puts you in a better frame of mind to expect them and fix them." — Source: [Big Money Thinks Small]

- On macro vs. micro: "Instead of trying to predict the global economy, focus your analytical energy on the granular details of individual business fundamentals." — Source: [Masters in Business]

- On diagnostic simplicity: "One advantage of investing in simple businesses is that if outsiders can diagnose the issues, skilled managers already know whether they can be fixed and how." — Source: [Big Money Thinks Small]

- On finding opportunity: "'Big money' institutional funds frequently ignore smaller, less-covered companies, which creates structural mispricing that individual investors can exploit." — Source: [Advisor Analyst]

- On the small-cap advantage: "Small capitalization stocks often trade outside the glare of heavy analyst coverage, allowing diligent researchers to secure a wider margin of safety." — Source: [Fidelity]

- On avoiding standard stupidities: "Success in investing relies far less on making brilliant predictions and far more on methodically avoiding unforced errors." — Source: [The Investor's Podcast]

- On understanding causality: "Every skilled investor I've met has been curious and a lifelong learner; they read broadly and constantly. For anticipating the future, it's more important to understand why things happen than what happened." — Source: [Big Money Thinks Small]

- On avoiding grand theories: "The most treacherous speculations are usually those based on crowd psychology, commodity prices, and high-level macroeconomic shifts." — Source: [Advisor Analyst]

- On actionable data: "While having more data is generally useful, the key is focusing exclusively on the most important variables rather than being distracted by the most recent noise." — Source: [Morningstar]

Part 3: Assessing Management Quality

- On basic filters: "Don't invest with crooks and idiots." — Source: [Big Money Thinks Small]

- On corporate character: "Look for companies that exhibit a distinctive, authentic character, as this often indicates leadership with a clear, long-term vision." — Source: [Investing.com]

- On assessing executives: "When meeting a CEO, begin by asking questions about their long-term strategy rather than interrogating them about the current quarter's earnings." — Source: [Masters in Business]

- On management integrity: "An investor should actively avoid companies that stretch the truth or rely on opaque accounting, regardless of their purported growth metrics." — Source: [The Investor's Podcast]

- On fiduciary alignment: "Seek out management teams that act like fiduciaries and treat their shareholders as actual partners, not just as sources of capital." — Source: [Fidelity]

- On surrogation bias: "Beware of corporate cultures where hitting a specific numerical metric becomes more important than the health of the underlying business, as this invites toxic behavior." — Source: [Big Money Thinks Small]

- On leadership red flags: "Tiny audit firms, insider-heavy boards, and a lack of independent oversight are clear signs that a management team should not be trusted." — Source: [Masters in Business]

- On acquisition sprees: "Be highly skeptical of glamorous rollups where a company attempts to manufacture growth entirely through aggressive, debt-fueled acquisitions." — Source: [The Investor's Podcast]

- On the limits of good businesses: "Even the most robust business model can be permanently impaired if it is placed in the hands of incompetent or dishonest leadership." — Source: [Big Money Thinks Small]

Part 4: Navigating the Circle of Competence

- On knowing your limits: "Don't invest in things you don't understand." — Source: [Fidelity]

- On business comprehension: "If you cannot easily explain how a company makes its money and what its individual segments do, you have no business owning the stock." — Source: [Masters in Business]

- On avoiding binary outcomes: "Avoid sectors like biotech where a company's entire destiny hinges on binary events, such as FDA trials, which are impossible to predict with certainty." — Source: [Advisor Analyst]

- On the predictability requirement: "True value investing requires a baseline of certainty; if a business operates in a field that changes too rapidly, its intrinsic value cannot be reliably calculated." — Source: [The Investor's Podcast]

- On commodities: "Generally steer clear of businesses where price is the only differentiator, as commodity producers lack the pricing power necessary to protect long-term margins." — Source: [Big Money Thinks Small]

- On the oil exception: "While avoiding most commodities, oil can sometimes be an exception due to its hard supply limits and deeply inelastic global demand." — Source: [Big Money Thinks Small]

- On faddish industries: "Fast-changing industries driven by fickle consumer tastes, such as teen fashion, offer terrible odds for the long-term, fundamental investor." — Source: [Goodreads]

- On informational edges: "Stick to areas where your research or operational experience gives you a genuine analytical advantage over the broader market." — Source: [Masters in Business]

- On simplifying choices: "By avoiding the bad-guy stocks—and it's a short list—I slash the possibility of a disastrous outcome but scarcely reduce my opportunity set." — Source: [Big Money Thinks Small]

Part 5: Business Quality and Moats

- On obsolescence: "Don't go for businesses that are prone to obsolescence and destruction." — Source: [Novel Investor]

- On customer stickiness: "Investors have fared best in industries that cater to daily needs where customers can't or won't switch." — Source: [Goodreads]

- On pricing power: "The most resilient companies are those with sufficient pricing power to safely pass on inflationary costs to their customers without destroying demand." — Source: [The Investor's Podcast]

- On technological disruption: "Be extremely wary of companies whose core products can be easily replicated or replaced by emerging, lower-cost technologies." — Source: [Big Money Thinks Small]

- On the Sun Tzu framework: "Evaluate businesses through five critical factors: their mission, their timing, the competitive marketplace, the quality of leadership, and their internal systems." — Source: [Big Money Thinks Small]

- On adaptive structures: "Prioritize companies whose fundamental business structures are adaptable enough to survive prolonged periods of inflation and economic stress." — Source: [Masters in Business]

- On continuous monitoring: "A successful investor is one who holds on for the long term and continues to monitor the fundamental story, and if it remains in place you stay, and if not you move on." — Source: [Goodreads]

- On high cash flow yields: "Even in the technology sector, the safest bets are those businesses that combine a strong competitive position with high free cash flow yields." — Source: [Fidelity]

- On avoiding fragile balance sheets: "Debt is often the final straw that turns a temporary operational struggle into a total, unrecoverable capital loss." — Source: [Big Money Thinks Small]

- On business maturity: "A business that has survived multiple market cycles and proven its ability to adapt is inherently less risky than a newly public, unproven disruptor." — Source: [The Investor's Podcast]

Part 6: Portfolio Strategy and Diversification

- On turning over rocks: "The investor who investigates the most companies and turns over the most rocks is the one most likely to find the hidden gems." — Source: [Masters in Business]

- On the rewards of patience: "When I started, I didn't realize that the biggest profits usually come from sitting on a great position — from doing what looks like nothing to the outside world." — Source: [Goodreads]

- On level-setting positions: "Holding a large number of stocks allows an investor to use small positions to level-set and compare the relative quality of different companies within the same sector." — Source: [The Investor's Podcast]

- On radical diversification: "Maintaining a portfolio of hundreds of stocks can effectively neutralize the idiosyncratic risk of being wrong about any single management team or product cycle." — Source: [Morningstar]

- On low turnover: "The lowest-friction path to wealth is holding high-quality winners for decades, allowing the underlying business compounding to do the heavy lifting." — Source: [Fidelity]

- On upgrading the portfolio: "The best rationale for selling an excellent stock is solely to make room in the portfolio for a truly superb one." — Source: [Masters in Business]

- On surviving cycles: "You can never predict when the excitement or exuberance for a specific type of stock will end... But I can tell you that the market's style leadership—value versus growth—has historically rotated over multi-year periods." — Source: [LiveMint]

- On Peter Lynch's math: "If you systematically review ten stocks, you will typically find two to buy, two to sell, and six that require more patient observation." — Source: [The Investor's Podcast]

- On margin debt: "Never use borrowed money to invest; using margin ensures that you will eventually become a forced seller at the absolute worst possible moment." — Source: [Big Money Thinks Small]

Part 7: Psychological Traps and Emotions

- On baseline expectations: "If you are average, don't count on superior results." — Source: [Goodreads]

- On emotional balance: "Stoic detachment combined with emotional awareness is the perfect combination for stocks. Feel the fear, but let reason decide." — Source: [Novel Investor]

- On knowledge and emotion: "The degree of one's emotion varies inversely with one's knowledge." — Source: [Goodreads]

- On independent thought: "In investing, where doing nothing often prevents blunders, a certain style of laziness is adaptive, but mental laziness isn't, and not thinking independently is absolutely toxic." — Source: [Novel Investor]

- On recognizing limits: "Don't invest in what you don't know and stay away from your own craziness." — Source: [Fidelity]

- On false confidence: "Confidence in investing is frequently derived more from ignorance of the risks than from a genuine understanding of the business." — Source: [Big Money Thinks Small]

- On controlling the controllable: "If you want to be superior, that's difficult. But what you won't do is easier to control and more attainable." — Source: [Fidelity]

- On anchoring bias: "Investors must actively fight the urge to anchor their valuation of a company to the price they originally paid for it." — Source: [Masters in Business]

- On crowd madness: "It is critical to remain emotionally detached when the broader market gets swept up in speculative manias or unjustified panics." — Source: [The Investor's Podcast]

- On confirmation bias: "Successful investors train themselves to actively seek out contradictory information that challenges their original investment thesis." — Source: [Masters in Business]

Part 8: Mistakes, Failures, and Learning

- On honesty in failure: "Call it humility, call it honesty with yourself, but failing to admit to investment mistakes means failing investing." — Source: [Novel Investor]

- On extracting lessons: "I don't think it's productive to wallow in regret. But if you've lost money in a stock and you don't learn anything, that's wasted money. Figure out what it is that you did wrong and don't do it again." — Source: [Novel Investor]

- On changing your mind: "The best investors I've seen all have an above-average ability to change their mind." — Source: [Novel Investor]

- On the reality of loss: "People who have had success in other parts of their lives have difficulty accepting how much failure there is in the stock market." — Source: [Goodreads]

- On unforced errors: "An investor's primary job is not to find the perfect stock, but to ruthlessly eliminate the predictable, unforced errors from their decision-making process." — Source: [Big Money Thinks Small]

- On being cruel to yourself: "You must be willing to ruthlessly audit your past trades and be cruel to yourself when diagnosing why a particular thesis failed." — Source: [The Investor's Podcast]

- On enduring underperformance: "True discipline requires the willingness to endure periods of massive underperformance—such as avoiding the late-1990s tech bubble—when the market abandons rational valuation." — Source: [Morningstar]

- On the danger of debt: "Viewing corporate debt casually is a recurring mistake; debt accelerates both gains and losses, often turning minor operational hiccups into bankruptcies." — Source: [Big Money Thinks Small]

- On flexibility: "The hallmark of a master investor is an extreme flexibility of thought, allowing them to pivot instantly when the underlying facts of a business change." — Source: [Masters in Business]