Lessons from Jonathan Knee

Jonathan Knee is a Columbia Business School professor and former investment banker who studies the strategic failures of major industries. His four books detail how structural realities undermine the ambitions of Wall Street executives, media moguls, education philanthropists, and tech founders. This profile gathers his arguments on competitive advantage, capital allocation, and why heavily hyped business models routinely lose money.

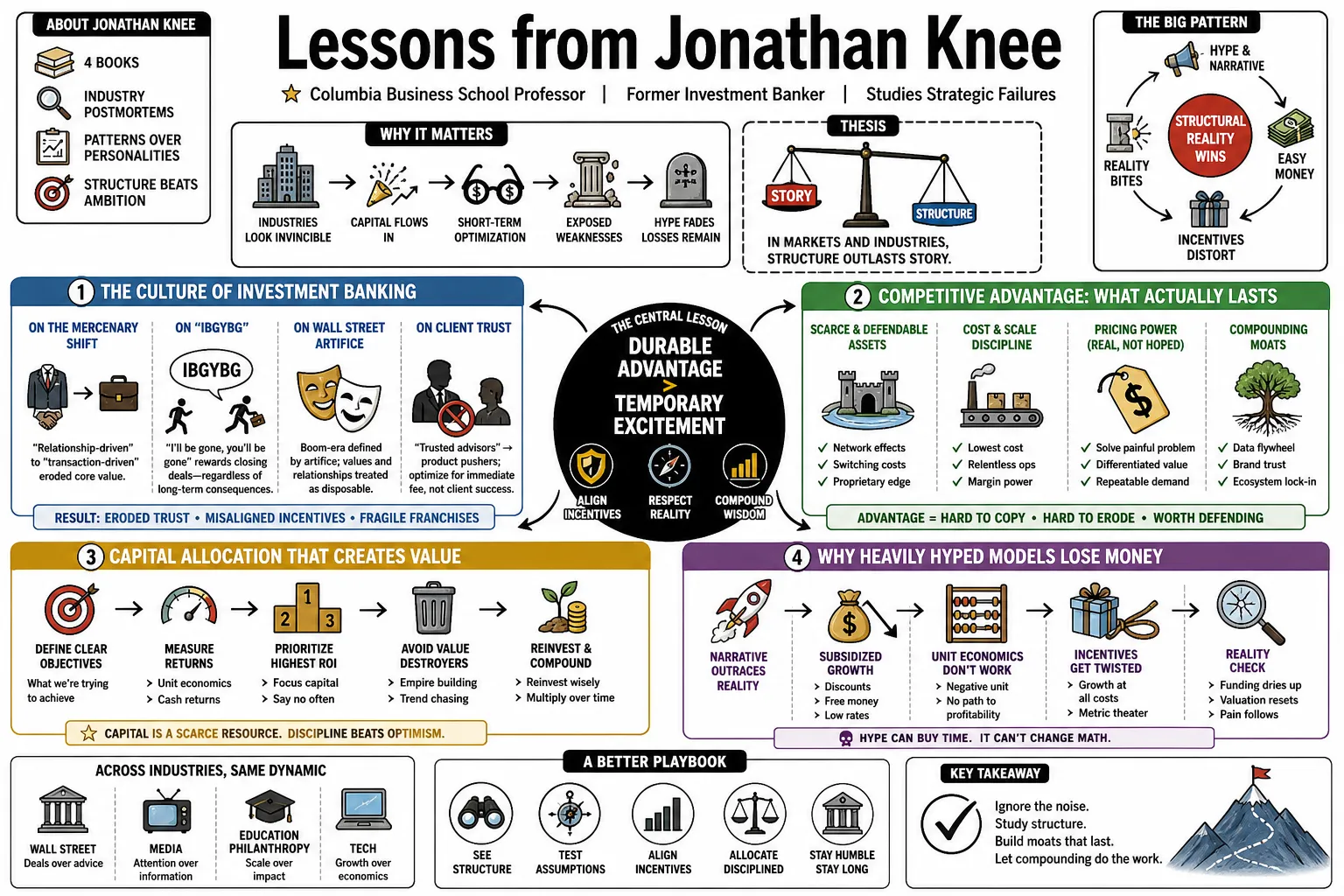

Part 1: The Culture of Investment Banking

- On the Mercenary Shift: "The transition from a relationship-driven model to a transaction-driven one fundamentally eroded the core value of investment banking." — Source: [The Accidental Investment Banker]

- On "IBGYBG": "The acronym 'I’ll be gone, you’ll be gone' encapsulates the dangerous, short-term incentive structure that rewarded closing deals regardless of their long-term consequences." — Source: [Ritholtz Interview]

- On Wall Street Artifice: "The environment during the boom era was defined by artifice, where personal relationships and values were frequently treated as disposable or merely trendy." — Source: [Columbia Business School]

- On Client Trust: "Bankers stopped being trusted advisors and became product pushers, optimizing for the immediate fee rather than the health of the client's business." — Source: [unSILOed Podcast Episode 265]

- On the Syndicate System: "The historical syndicate system, though clubby, at least aligned the long-term reputational interests of banks with the pricing of their offerings." — Source: [The Accidental Investment Banker]

- On Compensation: "When compensation became entirely divorced from the long-term performance of the advised entity, the moral hazard on Wall Street became systemic." — Source: [OUPblog Interview]

- On the Lure of Prestige: "The industry masterfully weaponizes prestige and compensation to attract top talent, only to burn them out in an environment largely devoid of mentorship." — Source: [The Accidental Investment Banker]

- On the Evolution of Partnerships: "The shift from private partnerships to publicly traded corporations transferred the risk from the bankers themselves to anonymous shareholders." — Source: [The Accidental Investment Banker]

- On the Banker's Actual Role: "The public fundamentally misunderstands what investment bankers actually do, assuming a level of complex financial wizardry that often masks simple aggressive salesmanship." — Source: [OUPblog Interview]

- On Information Asymmetry: "The traditional advantage of the investment bank was access to information; as information democratized, the banks had to rely on increasingly complex, opaque products." — Source: [unSILOed Podcast Episode 265]

Part 2: Media Moguls and Ego

- On Content vs. Distribution: "The prevailing industry narrative that 'content is king' is a persistent myth; competitive advantage in media usually stems from distribution and scale, not the content itself." — Source: [The Curse of the Mogul]

- On Executive Tenure: "Long-serving media moguls with great consistency do seem to 'lose the plot' at some point in their careers." — Source: [The Wrap Interview]

- On Random Returns: "For all the excitement, glamour, drama, and publicity they produce, why can't these moguls and their companies manage to deliver the kind of returns you'd get from closing your eyes and throwing a dart?" — Source: [The Curse of the Mogul]

- On the Exception of 'Creative' Management: "Moguls have successfully propagated a myth that both makes them appear indispensable to the business and justifies their lousy performance." — Source: [The Curse of the Mogul]

- On Avoiding Accountability: "Because they manage 'creative talent and artistic product,' moguls argue that subjecting them to traditional strategic, financial, or operational metrics is inherently unfair." — Source: [The Curse of the Mogul]

- On Growth for Growth's Sake: "The assumption that 'growth is good' has led media conglomerates to pursue massive acquisitions that reliably destroy shareholder value." — Source: [Accrued Interest]

- On Ego-Driven Strategy: "In media, capital allocation is too often driven by the personal ego of the executive rather than rational economic analysis of competitive moats." — Source: [The Atlantic]

- On Hollywood Economics: "The glamour of the entertainment industry systematically blinds investors to its fundamentally poor structural economics." — Source: [Museum of American Finance]

- On Conglomeration: "Synergy in media is usually an illusion used to justify the overpaying for assets that would be better managed independently." — Source: [The Curse of the Mogul]

- On the Fear of Missing Out: "Media executives frequently make panic-driven acquisitions out of a fear of being left behind, rather than from a position of strategic strength." — Source: [The Atlantic]

Part 3: The Tech Platform Fallacy

- On the Platform Trend: "The 'platform delusion' is the dangerous belief among tech leaders that striving for a platform model is the universal and necessary key to business success." — Source: [Better Product Podcast]

- On Misunderstanding Platforms: "Many companies aspire to be platforms due to the perceived benefits of network effects, but these advantages are often wildly overstated." — Source: [unSILOed Podcast Episode 265]

- On Platform Viability: "Not every successful company is a platform, and crucially, not every platform is a great business." — Source: [The Platform Delusion]

- On Strategy vs. Structure: "The laws of economics and strategy do not change, but the industry structures to which they are applied are constantly evolving." — Source: [unSILOed Podcast Episode 265]

- On Winning Without a Platform: "Tech leaders frequently fail to recognize that they may not need to be a platform at all to win definitively in their specific product category." — Source: [Better Product Podcast]

- On True Network Effects: "True network effects are rare; most platforms merely benefit from basic economies of scale rather than compounding user-to-user value." — Source: [The Platform Delusion]

- On Vertical Specialization: "Vertical specialization often yields a more defensible competitive moat than attempting to build a broad, horizontal platform." — Source: [unSILOed Podcast Episode 265]

- On the Amazon Exception: "Companies look at Amazon Marketplace and assume they can replicate it, ignoring the unique, historically specific structural advantages that allowed it to scale." — Source: [The Platform Delusion]

- On the Costs of Scaling: "The race to establish a platform often involves subsidizing growth so heavily that the business model never actually achieves profitability." — Source: [The Platform Delusion]

- On First-Mover Advantage: "The idea that the first mover in a platform market always wins is a myth; fast followers with better capital allocation often overtake the pioneers." — Source: [unSILOed Podcast Episode 265]

Part 4: Misguided Education Investments

- On Market Arrogance: "Investors approach education with a deep belief in the curative powers of the market, entirely failing to understand the specific structural realities of the education ecosystem." — Source: [Class Clowns]

- On the Source of Failure: "Financial failures in education are rarely due to a lack of good intentions; they stem from a fundamental misunderstanding of industry structure and competitive advantage." — Source: [Education Next]

- On Emotional Investing: "Profound emotional connection to an investment thesis often prevents investors from adapting when new data emerges, leading them to double down on flawed ideas." — Source: [EdSurge]

- On Personal Epiphanies: "Everyone comes to the subject of education with deep preconceptions from their formative life experiences; distinguishing which of these provide useful investment ideas is complicated." — Source: [EdSurge]

- On the 'Clown' Premise: "Otherwise brilliant billionaires routinely waste hundreds of millions of dollars on ill-conceived utopian education schemes." — Source: [Class Clowns]

- On Technology in Schools: "The education sector requires better governance structures rather than simply dropping technological or academic innovation into broken systems." — Source: [Holistic Equity]

- On Rupert Murdoch’s Amplify: "Amplify was a multi-billion dollar attempt to reshape elementary education through technology that dramatically misjudged the procurement realities of school districts." — Source: [Politics & Prose Book Talk]

- On Scaling Education Models: "The assumption that a successful charter school model can be seamlessly scaled nationally ignores the highly localized nature of educational politics and talent." — Source: [Class Clowns]

- On the Pace of Change: "Education operates on generational timelines, making it fundamentally incompatible with the quarterly return expectations of venture capital and private equity." — Source: [Museum of American Finance]

Part 5: The Nature of Strategic Advantage

- On Enduring Principles: "While technological mediums shift constantly, the fundamental principles that define a durable competitive advantage remain remarkably static." — Source: [unSILOed Podcast Episode 265]

- On Barriers to Entry: "A strategy without a clear, structural barrier to entry is just a temporary operating plan." — Source: [Columbia Business School]

- On Local Economies of Scale: "The most robust advantages are often found in local or niche economies of scale, not in massive, global market share." — Source: [unSILOed Podcast Episode 265]

- On Operational Effectiveness: "Operational effectiveness is necessary for survival, but it is not a strategy; strategy is about making structural choices that competitors cannot easily replicate." — Source: [The Curse of the Mogul]

- On Customer Captivity: "True customer captivity is created not by flashy marketing, but by high switching costs and ingrained habituation." — Source: [The Platform Delusion]

- On the Illusion of Disruption: "Incumbents are rarely disrupted by better products; they are disrupted by new business models that fundamentally alter the industry's cost structure." — Source: [Columbia Business School]

- On Supply-Side Advantages: "Companies over-index on demand-side network effects while neglecting the profound, defensive power of supply-side cost advantages." — Source: [The Platform Delusion]

- On Niche Dominance: "It is vastly more profitable to be a monopolist in a small, unglamorous niche than a minor player in a massive, exciting market." — Source: [Class Clowns]

- On the Limits of Innovation: "Innovation without structural protection merely serves to educate the market for a larger, better-capitalized competitor to eventually steal." — Source: [unSILOed Podcast Episode 265]

Part 6: Dealmaking and Mergers

- On Deal Momentum: "Once an M&A deal gains internal momentum, it becomes nearly impossible to stop, regardless of how aggressively the financial realities deteriorate." — Source: [The Accidental Investment Banker]

- On Valuation Gymnastics: "Bankers are incredibly skilled at reverse-engineering financial models to justify whatever valuation is required to get a deal approved." — Source: [The Accidental Investment Banker]

- On the Illusion of Synergies: "Synergies are the magical fairy dust sprinkled over spreadsheet projections to justify an unjustifiable acquisition premium." — Source: [The Curse of the Mogul]

- On Deal Fees: "The structure of M&A advisory fees, paid only upon completion, intrinsically biases the advisor toward pushing the deal forward, no matter the strategic fit." — Source: [OUPblog Interview]

- On Corporate Hubris: "Most transformative acquisitions are born not from strategic necessity, but from the CEO's fear of mortality and desire for a legacy." — Source: [The Curse of the Mogul]

- On the Role of the Board: "Boards of directors are rarely equipped to challenge the complex, optimistic assumptions presented by a unified team of executives and investment bankers." — Source: [The Accidental Investment Banker]

- On Integration Failure: "The spreadsheet models never account for the brutal, value-destroying reality of attempting to merge two entirely different corporate cultures." — Source: [The Accidental Investment Banker]

- On Bidding Wars: "Winning a highly contested auction is often a reliable leading indicator of the winner's impending financial underperformance." — Source: [The Curse of the Mogul]

- On Divestitures: "The most value-creating deals are often unglamorous divestitures, which bankers rarely pitch because they generate smaller fees than massive acquisitions." — Source: [unSILOed Podcast Episode 265]

Part 7: Mentorship and Institutional Memory

- On Professional Isolation: "The modern financial institution is marked by profound professional isolation, where employees function as independent contractors rather than members of a firm." — Source: [Reddit AMAs]

- On Rare Mentorship: "Lauren Bessette was a rare figure at Morgan Stanley who helped others without needing to establish an up-front quid pro quo." — Source: [The Accidental Investment Banker]

- On the Loss of Memory: "The rapid turnover and structural changes on Wall Street have led to a dangerous lack of institutional memory regarding past financial crises." — Source: [OUPblog Interview]

- On Training vs. Doing: "Banks stopped training their junior staff in the art of judgment, replacing it entirely with a relentless focus on modeling mechanics and output." — Source: [The Accidental Investment Banker]

- On Firm Culture: "A true firm culture requires the willingness of senior partners to sacrifice some current income for the long-term health and stability of the institution." — Source: [The Accidental Investment Banker]

- On the Disposable Analyst: "The two-year analyst program institutionalized the idea that junior talent is fundamentally disposable, damaging the long-term pipeline of leadership." — Source: [The Accidental Investment Banker]

- On Toxic Leadership: "When rainmakers are allowed to operate outside the rules of standard decency due to their revenue generation, the entire cultural fabric of the firm rots." — Source: [The Accidental Investment Banker]

- On Knowledge Hoarding: "In a transaction-driven environment, information is hoarded by individuals for leverage rather than shared to build the institution's collective wisdom." — Source: [OUPblog Interview]

- On Authentic Relationships: "The few bankers who survive and thrive over decades do so by building authentic, low-pressure relationships that outlast the current deal cycle." — Source: [unSILOed Podcast Episode 265]

Part 8: Market Myths and Financial Returns

- On Market Corrections: "Market downturns do not create new structural weaknesses; they merely expose the strategic flaws that were papered over by cheap capital." — Source: [unSILOed Podcast Episode 265]

- On the Valuation of Tech: "Valuations decoupled from fundamental cash flow generation rely entirely on the presence of a 'greater fool' to validate the investment." — Source: [The Platform Delusion]

- On Return on Invested Capital: "Return on invested capital is the single most important metric that executives continually try to obscure with vanity metrics like adjusted EBITDA." — Source: [The Curse of the Mogul]

- On the Role of Luck: "Executives routinely confuse a favorable macroeconomic tailwind with their own strategic genius." — Source: [The Curse of the Mogul]

- On Risk Management: "Risk models in finance fail precisely because they use historical data to predict unprecedented psychological panics." — Source: [The Accidental Investment Banker]

- On Capital Allocation: "The primary job of a CEO is capital allocation, yet most are promoted for their salesmanship and have zero formal training in the discipline." — Source: [unSILOed Podcast Episode 265]

- On the Cult of Disruption: "The obsession with 'disruption' leads investors to systematically overvalue unproven models while undervaluing highly cash-generative, mature businesses." — Source: [The Platform Delusion]

- On Market Efficiency: "Markets are highly efficient at pricing in the short term, but incredibly inefficient at pricing the long-term decay of a competitive moat." — Source: [Columbia Business School]

- On the Ultimately Unavoidable Math: "You can defer the laws of economic gravity through clever accounting and narrative spin, but you can never escape them indefinitely." — Source: [The Curse of the Mogul]