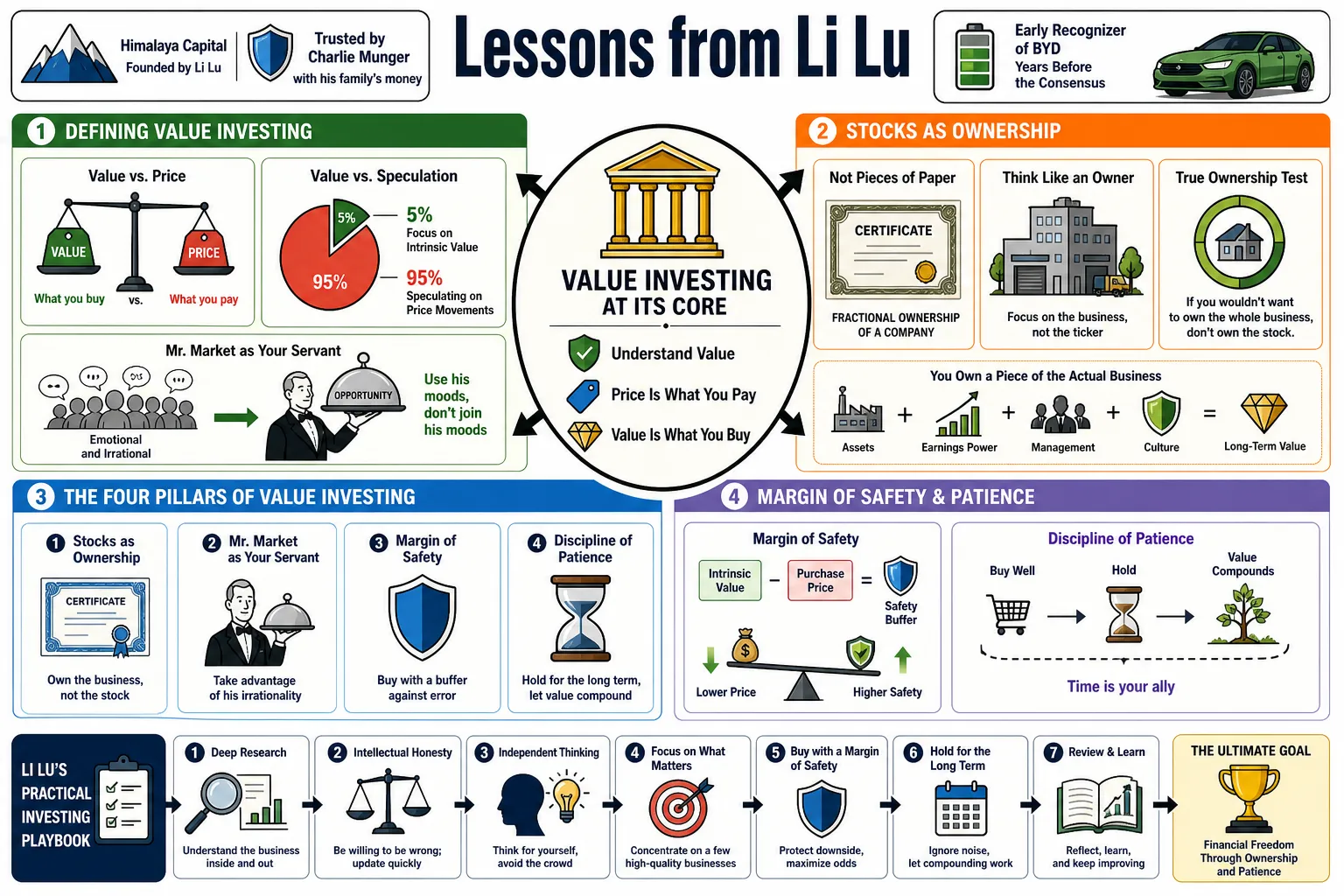

Li Lu founded Himalaya Capital and is the only outside manager Charlie Munger ever trusted with his family's money. He adapted traditional value investing for Chinese markets, famously spotting battery maker BYD years before the consensus. This collection covers his practical rules for deep research, intellectual honesty, and the actual discipline of holding for the long term.

Part 1: The Foundations of Value Investing

- On Defining Value Investing: "The core of value investing is to understand value. What you pay is price—and what you buy is value." — Source: [12mv2.com]

- On the Nature of Stocks: "Stocks aren’t just little pieces of paper that you buy and sell. Each one is in fact a certificate bestowing fractional ownership of a company." — Source: [12mv2.com]

- On True Ownership: "If you wouldn't want to own the whole business, you shouldn't own the stock." — Source: [Scribd]

- On Value vs. Speculation: "If you look at the entire stock market, 95% of the people are playing a game of speculating on price movements. Only 5% are looking at the intrinsic value." — Source: [Medium]

- On the Four Pillars: "Value investing is built on four pillars: stocks as ownership, Mr. Market as your servant, the margin of safety, and the circle of competence. This is the only true way." — Source: [MOI Global]

- On Changing Styles: "When you start out with a small amount of capital, looking for cheap 'cigar butts' is a great way to learn. But over time, you must evolve to finding wonderful companies at fair prices." — Source: [Substack]

- On Economic Moats: "We seek companies with sustainable competitive advantages that can protect high returns on capital over decades." — Source: [Hedge Fund Alpha]

- On Assessing Management: "Meeting management is often less useful than studying their past actions. Actions speak louder than words." — Source: [WordPress]

- On Return Expectations: "In the long run, an investor's return will mirror the company's Return on Invested Capital. If a business earns 6% on capital over 40 years, your return will be about 6%." — Source: [Mike Gorlon]

- On the Primary Question: "The most important question for an investor is whether a business can grow its intrinsic value infinitely alongside the economy." — Source: [GuruFocus]

Part 2: The Stock Market and Human Nature

- On Market Volatility: "Value investors believe the market is only there to serve you. The market is composed of individuals, and human nature pursues short-term goals—so people tend to treat stocks as chips for short-term transactions." — Source: [Kingswell]

- On Mr. Market: "The market exists to serve you, not to instruct you. Price fluctuations are opportunities to buy or sell, not signals of a company's true worth." — Source: [MOI Global]

- On the Herd Mentality: "The market is a place designed for people who want to trade, which is why it is often irrational. To succeed, you must stand on your own and ignore the opinions of others." — Source: [Medium]

- On Emotional Discipline: "If you can avoid being lured by short-term gains and hold onto long-term investments, you will have fewer competitors and a higher probability of success." — Source: [Substack]

- On Being in the Minority: "To be a better investor, you have to stand on your own. You just can’t copy other people’s insights." — Source: [Good Investing]

- On Trading vs. Investing: "There’s little traffic on the main path of investing because many investors take shortcuts. The right and main path takes too long." — Source: [Michelle Marki]

- On Shorting: "Shorting is fundamentally different and more difficult than long investing. In a long position, your downside is 100% but your upside is unlimited; in shorting, your upside is capped at 100% while your downside is infinite." — Source: [WordPress]

- On Market Declines: "If you truly understand a company's value creation, you won't panic during a 50% price drop. If you do panic, it is a sign that your circle of competence was an illusion." — Source: [Compound with Rene]

- On the True Source of Returns: "You profit from the market's irrationality, not by following its lead." — Source: [MOI Global]

Part 3: Margin of Safety and Risk

- On Defining Risk: "Risk is not the volatility of the stock price. Real risk is the permanent loss of capital." — Source: [Mike Gorlon]

- On Downside Protection: "Being a value investor means you look at the downside before looking at the upside. Before becoming an investor, you need to look at how you can fail in this game." — Source: [12mv2.com]

- On the Margin of Safety: "Investing is inherently about predicting the future. But predictions can never reach 100% accuracy. So when we make a judgment, we need to leave a large buffer. This is called the margin of safety." — Source: [12mv2.com]

- On Probability: "If you buy a stock with a sufficient margin of safety, the probability is with you." — Source: [Substack]

- On Management Quality: "A deep discount provides a margin of safety even if management is only average, but a truly great management team creates a margin of safety on its own." — Source: [WordPress]

- On Avoiding Errors: "Most mistakes come from inaccurate or incomplete information. By doing more work than anyone else, you gain the conviction to hold through volatility." — Source: [Mike Gorlon]

- On Capital Preservation: "You must buy at a price significantly below intrinsic value to protect against the inherent unpredictability of the future." — Source: [Kingswell]

- On Uncertainty: "The macro environment is an objective reality that must be accepted, though it should not drive the primary investment decision." — Source: [Compound with Rene]

- On Diversification: "Diversification is a hedge against ignorance. If you truly understand a business, you don't need to diversify into your twentieth best idea." — Source: [Hedge Fund Alpha]

Part 4: The Circle of Competence

- On Defining Your Boundaries: "If you stray outside of your circle of competence, or if your circle has no boundaries, or if you don’t know your boundaries—there will be some moment when the market takes you to the cleaners." — Source: [Substack]

- On the 10-Year Test: "You only enter a circle of competence when you can predict with high confidence how a business will behave in 10 years—through normal, good, and bad times." — Source: [GuruFocus]

- On Edge vs. Size: "The edge of your circle of competence is far more important than the size of it." — Source: [Livemint]

- On Building Competence: "A beginner’s circle is extremely narrow and requires years of relentless learning to build." — Source: [GuruFocus]

- On Deep Understanding: "If you just pretend you know a business well, you will be tested in difficult times." — Source: [MOI Global]

- On Personal Interest: "Let your personal interests define your circle rather than industry labels. When you are genuinely interested, the research feels like play rather than work." — Source: [Substack]

- On Single-Business Focus: "Pick just one business and understand it completely inside and out before moving to others." — Source: [GuruFocus]

- On Geographic Edge: "Expanding your circle to include geography, by leveraging native language skills and cultural understanding, can help you find deep-value opportunities others miss." — Source: [Net Net Hunter]

- On Self-Awareness: "The true insights a person can get in life are still very limited, so correct decision-making must necessarily be confined to your circle of competence." — Source: [Substack]

Part 5: Research and Intellectual Honesty

- On Intellectual Honesty: "The most important thing in our business is intellectual honesty. Intelligent investors are the ones who are always intellectually honest." — Source: [Kingswell]

- On the Necessity of Truth: "Intellectual honesty is a good life philosophy to begin with, and it is crucial, vital when it comes to investment." — Source: [Substack]

- On Arguing the Other Side: "You are not entitled to an opinion unless you can argue against your own position better than the most intelligent person who disagrees with you." — Source: [GuruFocus]

- On Investigative Research: "Approach research as if you are an investigative journalist. Do not rely on Wall Street reports; visit factories, talk to competitors, study lawsuits, and dig into decades of history." — Source: [Scribd]

- On Information Gathering: "I learn and I’m curious about all businesses. That’s why when opportunities come, within a few seconds you can smell it. The only way to really do that is just reading page after page." — Source: [12mv2.com]

- On the Daily Work: "The game of investment is really continuous learning. I’d have remained an investing ape without continuous learning." — Source: [Good Investing]

- On Intellectual Arrogance: "The market eventually destroys those who are intellectually arrogant or who cannot identify the boundaries of their knowledge." — Source: [Scribd]

- On Uncomfortable Truths: "Intellectual honesty requires having the discipline to accept complete and accurate information, even when it forces you to be in the minority." — Source: [Wikipedia]

- On the 100% Owner Perspective: "Most people treat stocks as pieces of paper. A 100% owner seeks to deeply understand how the business is run, how it makes money, and what its competitive edge is." — Source: [GuruFocus]

- On Defining Yourself: "The game of investing is a process of discovering who you are, then magnifying that until you gain a sizable edge over all the other people." — Source: [What Should I Read Next]

Part 6: Patience and Long-Term Compounding

- On Inaction vs. Action: "The art of investment is the discipline of inaction in the absence of a good opportunity, but aggressive action when one is identified." — Source: [12mv2.com]

- On the Fat Pitch: "Divide the strike zone into 77 cells and only swing at the fat pitches in the sweet spot. You don't need to swing at everything." — Source: [Himalaya Capital]

- On Waiting: "The big money is not in the buying and the selling, but in the waiting. Spend most of your time reading and thinking." — Source: [GuruFocus]

- On Compounders: "We focus effort on rare long-term compounders. We wait patiently for prices to fall into our comfort zone, then buy aggressively and hold for the long term." — Source: [Substack]

- On the 15-Year Horizon: "If you stay the course for 15 years, you will become stellar investors." — Source: [Michelle Marki]

- On Portfolio Concentration: "Hold a very concentrated portfolio. If you truly understand a business, holding fewer than 10 positions is perfectly rational." — Source: [Hedge Fund Alpha]

- On True Returns: "Over a long enough timeline, the combination of free markets and modern science creates a continuous compounding machine for human civilization." — Source: [LongRiver Investment]

- On Sitting Still: "Once you find a wonderful business, the hardest but most profitable work is simply sitting on your hands and letting it compound." — Source: [Borsgade]

- On Health and Compounding: "A long life and good health are prerequisites for compounding wealth over many decades." — Source: [LongRiver Investment]

Part 7: Mentorship and Charlie Munger

- On Munger as a Role Model: "Charlie’s most significant meaning to me was that he was an authentic role model. I lived alongside Charlie for over twenty years and I never once found anything he did disappointing." — Source: [Compound with Rene]

- On Munger's Rationality: "Charlie lived his entire life according to his own clock, never changing—working and spending time with family until his very last moment." — Source: [Compound with Rene]

- On Character: "Munger believed that if you are a better person, you are likely to be a better investor; if you are a wiser person, you are likely to be a better investor." — Source: [Tao Value]

- On Universal Wisdom: "Charlie pursued what I call Universal Wisdom. He applied a Confucian approach to life and business, constantly refining his understanding of reality." — Source: [MOI Global]

- On Trust: "Munger told me he observed me for seven years before finally deciding to invest, stating he wanted to be absolutely sure of my total integrity." — Source: [Tao Value]

- On Munger's Singular Bet: "I'm 95 years old. I've given Munger money to some outsider to run once in 95 years. That's Li Lu." — Source: [Business Insider]

- On the Chinese Warren Buffett: "He’s sort of a Chinese Warren Buffett... there aren’t that many people better than Li Lu." — Source: [Arigato Investor]

- On Finding Opportunities: "The first rule in fishing has always been fish where the fish are... Li Lu just went where the fishing was good." — Source: [YouTube]

- On the BYD Discovery: It was Li Lu who introduced Munger to BYD, leading Munger to describe the founder as a combination of "Thomas Edison and Jack Welch." — Source: [Quartr]

- On Long-Only Investing: "Under Munger's advice, I moved away from short-selling early in my career, focusing exclusively on long-term ownership of excellent businesses." — Source: [Wikipedia]

Part 8: China and the "3.0 Civilization"

- On the Transition Phase: "China is at an interim stage between Civilization 2.0 (agrarian/industrial) and Civilization 3.0 (scientific/technological), or at 2.5." — Source: [Michelle Marki]

- On Market Inefficiency in China: "70% of the players in the Chinese capital market are retail investors focusing on short trades. Prices are detached from intrinsic value, creating very unique investment opportunities." — Source: [Michelle Marki]

- On the Chinese Opportunity: "China remains one of the best markets if you are a value investor. There is still an enormous amount of inefficiency in the security market." — Source: [Substack]

- On the Economic Shift: "China will transition from manufacturing and exports to more of a service and consumption-based economy." — Source: [GuruFocus]

- On Cultural Tailwinds: "If you have a good understanding of China's culture, people and history, you will agree that China will forge forward." — Source: [Michelle Marki]

- On the Rules of the Game: "There is almost no chance of China leaving the common market, and the probability of China changing its market rules is also very small." — Source: [Michelle Marki]

- On Civilization 3.0: "The combination of free markets and modern science creates a virtuous cycle of sustainable compound growth. Modernization is a result of this formula." — Source: [Mike Gorlon]

- On Frugality and Education: "China’s unique combination of a massive domestic market, high-quality labor, and a culture of frugality and education provides a fertile ground for value investors." — Source: [Peking University]

- On the Future of Value Investing: "As China's financial markets mature from 'gambling houses' to rational systems, the discipline of value investing will generate massive long-term wealth." — Source: [MarketFolly]