Lessons from Mason Hawkins

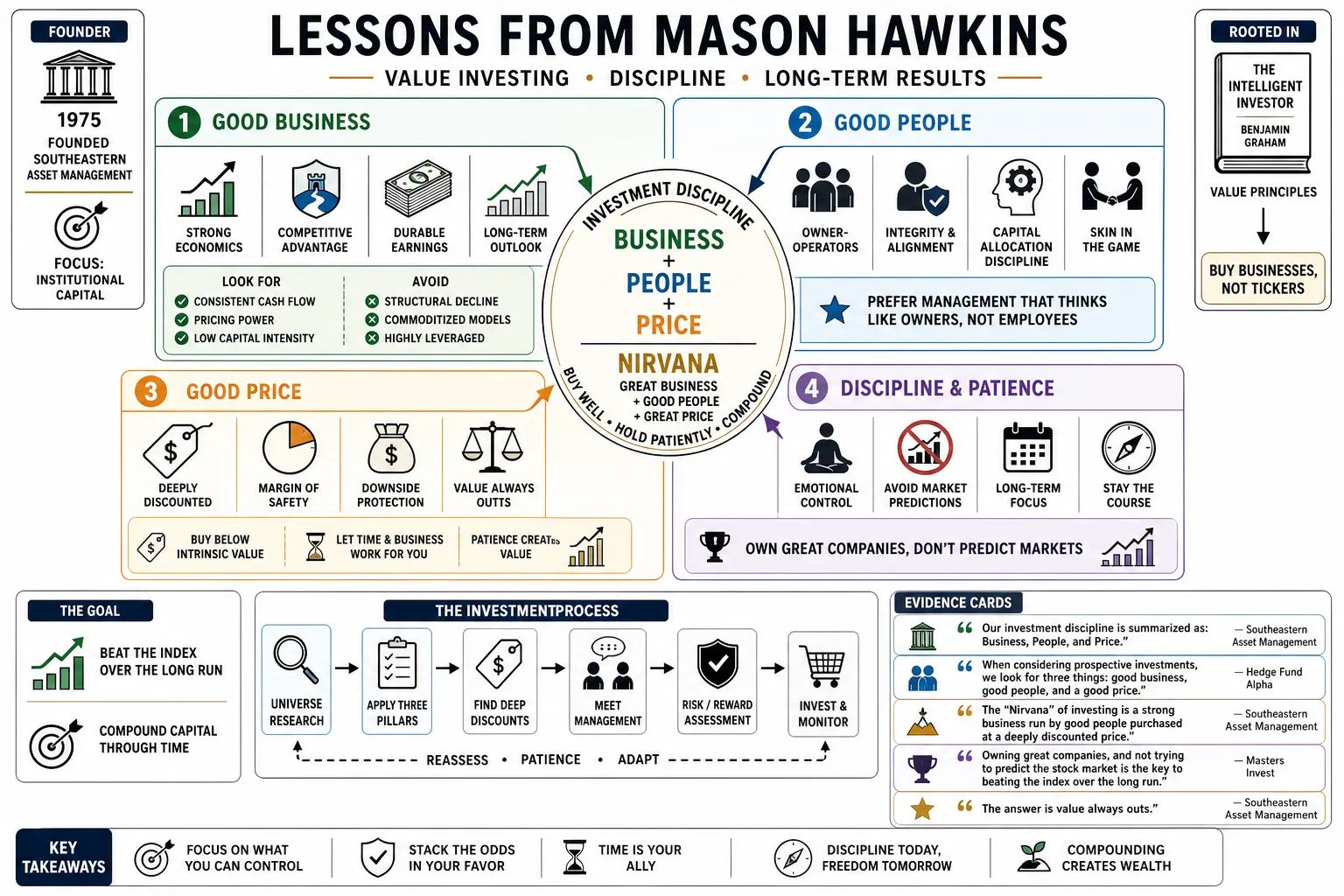

Mason Hawkins founded Southeastern Asset Management in 1975 to manage institutional capital using Benjamin Graham’s value principles. He built the firm around a straightforward "Business, People, Price" framework, buying heavily discounted companies run by capable owner-operators. This collection covers his mechanics for allocating capital and maintaining the psychological discipline required for long-term investing.

Part 1: The Core Philosophy

- On the investment discipline: "Our investment discipline is summarized as: Business, People, and Price." — Source: Southeastern Asset Management

- On the three pillars: "When considering prospective investments, we look for three things: good business, good people, and a good price." — Source: Hedge Fund Alpha

- On the ideal scenario: The "Nirvana" of investing is a strong business run by good people purchased at a deeply discounted price. — Source: Southeastern Asset Management

- On defining success: "Owning great companies, and not trying to predict the stock market is the key to beating the index over the long run." — Source: Masters Invest

- On the ultimate truth: "The answer is value always outs." — Source: Southeastern Asset Management

- On Graham's influence: "Graham talks about all good investments... have to qualify quantitatively. As we say in our shop: P2V (Price to Value)." — Source: Advisor Perspectives

- On risk: Risk is not volatility, but the permanent loss of capital. — Source: Southeastern Asset Management

- On hugging benchmarks: "We try to hug good investments, not benchmarks." — Source: Southeastern Asset Management

- On compounding value: "If you buy a business that's capable of compounding its intrinsic value at 12%, and you buy it at half the value, you pick up another 17 points a year over a five-year period of time by just having Mr. Market weigh the intrinsic value fairly." — Source: Southeastern Asset Management

Part 2: Defining a Good Business

- On growth as an eraser: "Valuable growth is the great eraser if you misprice your purchase. Buying good businesses is critical to profitable long-term equity investing." — Source: Columbia Business School

- On circle of competence: "You play an easier game when you're very selective and you just go for companies you understand." — Source: Masters Invest

- On qualitative moats: "We want to own companies with unique assets having distinct and sustainable competitive advantages that enable pricing power, long-term earnings growth, and stable or increasing profit margins." — Source: Hedge Fund Alpha

- On free cash flow predictability: A business must be "assured to grow its free cash flow production into the future." — Source: Southeastern Asset Management

- On financial durability: A good business requires a "strong balance sheet" and a "long record of profitability." — Source: Masters Invest

- On tracking returns: "High returns on capital and on equity should be measured by free cash flow rather than earnings." — Source: 25iq

- On intrinsic value: "Values are not nearly as volatile as prices, which obviously gives us opportunity at times when fear is driving prices." — Source: Advisor Perspectives

- On evaluating free cash flow: "We use three methods to arrive at an appraisal. The first and most predominant is determining the value of the free cash flow." — Source: Advisor Perspectives

- On long-term viability: "Time is the friend of the good business and the enemy of the bad. The good business will produce more free cash flow than its cost of capital... the bad business will not." — Source: YouTube

Part 3: The Owner-Operator Partnership

- On alignment of interests: "The owner-operator partnership model aligns interests... Since Southeastern's Code of Ethics requires employees to use the Longleaf Partners Funds for common stock investments, we are the largest ownership group across the Funds and our incentives are aligned with all Fund investors." — Source: Scribd

- On historical outperformance: "In over three-and-one-half decades our investments that have outperformed most have been due in large part to capable, vested owner-operators who made decisions that increased business quality as well as value per share." — Source: SEC

- On identifying good people: Management must be "honorable and trustworthy," "skilled operators," and "capable capital allocators" who are "shareholder-oriented." — Source: SEC

- On the difficulty of assessment: "The qualitative assessment of management is by far the hardest thing we do... We want to be in business with Good People—those who are honorable, trustworthy, and treat us as partners." — Source: Southeastern Asset Management

- On bad management: "We believe it’s impossible to do a good deal with a bad person." — Source: Hedge Fund Alpha

- On the dual requirement of management: "The people must be accountable good capital allocators. They also must possess the operating skills needed to produce a growing stream of cash." — Source: Scribd

- On active engagement: "We believe it's incredibly important to be engaged with our company's managements... to help them make intelligent capital allocation decisions." — Source: Buy Side Digest

- On solving agency problems: "We believe that the best way to eliminate conflicts is to require managers to put 100% of their net worth into the funds that they manage. As owner-operators... their stock picking will be laser-focused." — Source: Buy Side Digest

- On management selling reasons: We will sell an investment "when we were wrong on management." — Source: 25iq

- On stewardship: "When assessing 'People,' we seek to partner with responsible management teams that practice good stewardship on behalf of shareholders while growing value per share over time." — Source: Southeastern Asset Management

Part 4: The Margin of Safety

- On the one immutable rule: "There is no investment rule that remains immutable except the margin of safety. There are always breaks and the trick is to begin to anticipate, if you can, where the break points will be and shift." — Source: Masters Invest

- On business quality reducing risk: "If you understood a business perfectly and the nature of the business, you would need very little in the way of margin of safety. So the more vulnerable the business is... the larger the margin of safety you'd need." — Source: YouTube

- On the bridge analogy: "If you're driving a truck across a bridge that holds 10,000 lbs and you've got a 9,800 lb load, if the bridge is 6 inches above the crevice it covers, you feel okay. But if it's across the Grand Canyon you need a much larger margin of safety." — Source: YouTube

- On the 60 percent rule: "We only want to buy when we can pay less than 60% of a conservative appraisal of a company's value." — Source: Buy Side Digest

- On passing on opportunities: "It is very important to pass on opportunities when you can't calculate a conservative assessment of the business's value." — Source: 25iq

- On asset value as protection: "If you could acquire a business for half of its assets, it is a safe investment and should definitely be pursued." — Source: Hedge Fund Alpha

- On selling discipline: "We sell businesses when they approach their intrinsic value and there is no longer a margin of safety." — Source: Southeastern Asset Management

- On structural safety: A good business provides a structural margin of safety because its value is less likely to evaporate. — Source: Southeastern Asset Management

- On avoiding permanent loss: Using the margin of safety is the primary mechanism to avoid permanent loss of capital, which is the only true definition of risk. — Source: Southeastern Asset Management

- On valuation checks: We use comparable transactions checking our longhand math against a database of private market transactions over the last 30 years to remain conservative. — Source: Advisor Perspectives

Part 5: Capital Allocation & Value Creation

- On the necessity of wisdom: "Wise deployment of a company's cash is a paramount necessity to achieving an acceptably profitable long-term investment return." — Source: YouTube

- On high prices turning good ideas bad: "Capitalism has a way of turning a good idea at a low price into a bad idea at a high price. It makes sense to buy at 6x operating cash flow, but at 14x operating cash flow it is very problematic and harmful to do so using massive leverage." — Source: 25iq

- On share repurchases: "Most of our corporate partners see minimal growth but believe that their strong business prospects over the intermediate term make repurchasing today's discounted shares the optimal capital allocation choice." — Source: Scribd

- On shrinking the share count: "Not only have strengthened balance sheets and strong cash flow given companies the arsenal to steal shares, beneficial capital allocation work over the last year has significantly grown the value of our remaining shares." — Source: Scribd

- On reinvesting profits: Reinvesting in the existing business is preferred only if the internal returns on capital remain high. — Source: Southeastern Asset Management

- On M&A vs Buybacks: Management should acquire other businesses only if they are cheaper and fundamentally better than repurchasing their own discounted stock. — Source: Southeastern Asset Management

- On adjusting book values: "The second method calculates net asset value by adjusting book values... marking old real estate to market or adjusting liabilities." — Source: Advisor Perspectives

- On dividend hierarchies: Paying dividends is the correct capital allocation choice only if no other value-creative options exist for the cash. — Source: Southeastern Asset Management

- On future earnings power: A primary reason to sell is "when the future earnings power is impaired." — Source: 25iq

- On engaged ownership: "We believe it's incredibly important to be engaged with our company's managements... not only to support them when it's warranted, but to help them make intelligent capital allocation decisions." — Source: Scribd

Part 6: The Psychology of Value Investing

- On looking foolish: "If you are not willing to look stupid in the short run, you are not likely to be a successful investor in the long-run." — Source: 25iq

- On Mr. Market's role: "As we have said often, Mr. Market is there to serve you, not to determine your outcome. When he is fearful, you should be greedy... When he is greedy, you should be cautious and use those times to sell businesses at full appraisal." — Source: 25iq

- On emotional selling: "If you were forced to sell because you were fearful... you took a permanent loss, and you used Mr. Market to your detriment." — Source: Southeastern Asset Management

- On ignoring noise: "We could care less what the market pundits are saying... if you don't have that discipline and patience... you'll always be sucked into this vacuum of illogical behavior." — Source: 25iq

- On pricing over predicting: "We were not forecasting or predicting, we were pricing." — Source: Southeastern Asset Management

- On emotion vs logic: "Market value is influenced by the same factors that affect intrinsic value but even more so by the human emotions of fear and greed." — Source: Southeastern Asset Management

- On the 15 percent rule: "About 85% of the time, the markets are in some close proximity to central value. It's that other 15% of the time that you need to concern yourself with." — Source: 25iq

- On temperament: An investor's edge comes from emotional discipline and the ability to remain rational when others are panicking. — Source: Southeastern Asset Management

- On business ownership mindset: By viewing a stock as a partial interest in a business rather than a ticker symbol, an investor detaches from the daily psychological noise of the market. — Source: Southeastern Asset Management

Part 7: Patience and Time Horizon

- On the 5-year perspective: The ideal holding period is approximately five years, effectively engaging in time horizon arbitrage against short-term market participants. — Source: Southeastern Asset Management

- On the enemy of bad businesses: "Time is the friend of the good business and the enemy of the bad." — Source: YouTube

- On liquidating bad businesses: "The bad business will not produce free cash flow... and thus will be slowly liquidating." — Source: YouTube

- On concentration: "Why invest in your 22nd favorite stock when you can just own more of your favorite?" — Source: Southeastern Asset Management

- On holding few names: He believes in a concentrated portfolio, typically holding only 10 to 22 stocks to ensure high conviction over a long holding period. — Source: Southeastern Asset Management

- On portfolio turnover: The average holding period translates to a portfolio turnover of under 20 percent, reflecting extreme patience. — Source: Southeastern Asset Management

- On waiting for the right pitch: Holding cash is acceptable when nothing meets the firm's strict price criteria, as value calculation takes precedence over market timing. — Source: Southeastern Asset Management

- On upgrading the portfolio: A reason to sell is "when the portfolio's risk/return profile can be significantly improved" by reallocating to better long-term opportunities. — Source: 25iq

- On long-term economic contribution: "The collective welfare of our workers, savers and successors depends upon successful new business formations." — Source: SOE Memphis

Part 8: The Role of the Liquidity Provider

- On the historical advantage: "The great investors throughout history... were always in a position to be liquidity providers." — Source: 25iq

- On holding cash strategically: "Each was willing to hold cash until someone was in distress, under duress, and they could provide that liquidity at very attractive prices." — Source: 25iq

- On capitalizing on volatility: "The primary frustration... has been the lack of volatility in the markets. Without volatility we get few opportunities to steal businesses and lay the foundation for future compounding." — Source: Advisor Perspectives

- On acting when fear dominates: Extreme market divergence and fear create the ideal environment for the disciplined liquidity provider to acquire assets at a deep margin of safety. — Source: Advisor Perspectives

- On structural market advantages: By standing ready to buy when index funds, margin calls, or panicking individuals are forced to sell, value investors capture the illiquidity premium. — Source: Southeastern Asset Management

- On the necessity of free markets: "A free, open-market society spawns entrepreneurship and increases the rights and responsibilities of each citizen. Perpetuating an entrepreneurial environment is one of America's greatest challenges as well as our brightest hope." — Source: SOE Memphis

- On the ultimate goal of capital: "Without the revenue from these dynamic, rapidly growing enterprises, the regnant demands of our body politic will clearly go unfunded." — Source: SOE Memphis

- On exploiting forced selling: When someone is under duress and must sell, the liquidity provider is there not out of charity, but to secure absolute returns. — Source: 25iq

- On outlasting the panic: You can only be a liquidity provider if your capital base is stable and your investors share your long-term horizon. — Source: Southeastern Asset Management