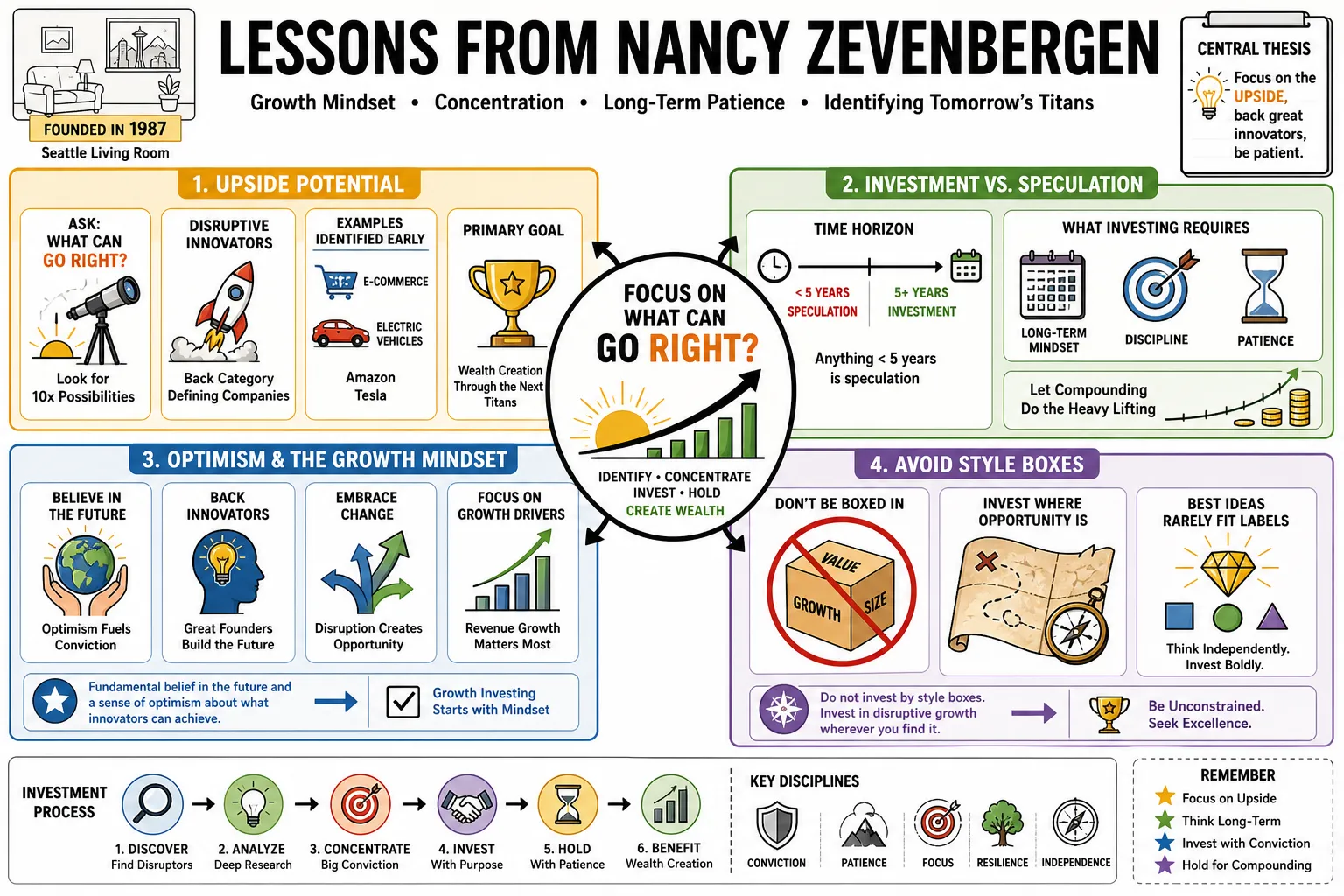

Nancy Zevenbergen is the founder of Zevenbergen Capital Investments, which she launched from her Seattle living room in 1987. She is known for identifying disruptive companies like Amazon and Tesla long before they became market leaders by focusing on the "What can go right?" potential of business growth. This profile outlines her strategies for aggressive growth investing, the discipline of concentration, and the art of long-term patience.

Part 1: The Growth Mindset and Optimism

- On Upside Potential: "Most of the investment world is focused on what can go wrong, but we have built our firm by asking what can go right." — Source: Zevenbergen Capital Insights

- On Investment vs. Speculation: "Anything with a timeframe of less than five years is not investing; it is speculation." — Source: Forbes Profile

- On the Goal of Investing: "The primary goal of our strategy is wealth creation through the identification of the next titans of the industry." — Source: Virtus Portfolio Manager Insights

- On Optimism: "Growth investing requires a fundamental belief in the future and a sense of optimism about what innovators can achieve." — Source: University of Washington Foster School

- On Style Boxes: "Don't let rigid style boxes prevent you from owning the best companies in the world just because they don't fit a specific numerical filter." — Source: Business Insider Interview

- On the Gap in Expectations: "We look for the gap between conservative market expectations and the massive potential of a truly disruptive business model." — Source: Zevenbergen Capital Insights

- On Secular Growth: "Seek out secular growth trends that can persist regardless of whether the broader economy is moving up or down." — Source: University of Washington Foster School

- On Aggressive Equity: "Aggressive growth is not about taking reckless risks, but about having the conviction to back the most ambitious ideas." — Source: Forbes Profile

- On Imagination: "Successful investing involves the imagination to see what a company could become in a decade, not just what it is today." — Source: Virtus Portfolio Manager Insights

- On Future Orientation: "The stock market is a forward-looking mechanism; if you are looking at the past, you are already behind." — Source: Zevenbergen Capital Insights

Part 2: Evaluating Founders and Visionaries

- On Founder Leadership: "I would much rather buy a company and go to a desert island for five years knowing that a founder was leading it." — Source: Forbes Profile

- On Vision and Passion: "Founders possess a level of vision and passion that professional 'rent-a-CEOs' simply cannot replicate." — Source: Business Insider Interview

- On Skin in the Game: "We prefer leaders who have their own wealth tied up in the company, as it aligns their long-term interests with ours." — Source: Zevenbergen Capital Insights

- On 'Crazy' Ideas: "Many of the best investments we've ever made started with a founder who had a vision that others called crazy." — Source: University of Washington Foster School

- On Listening to Entrepreneurs: "One of our greatest advantages is simply listening to what entrepreneurs tell us about their plans for the future." — Source: Forbes Profile

- On Management Agility: "In a disruptive environment, the ability of a leader to pivot and adapt is more valuable than a fixed five-year plan." — Source: Virtus Portfolio Manager Insights

- On the Human Element: "While numbers matter, it is ultimately people who create the performance of a business." — Source: Zevenbergen Capital Insights

- On Resilience: "Founders have the grit to drive a company through the inevitable ups and downs of a business cycle." — Source: University of Washington Foster School

- On Long-Term Conviction: "A founder-led firm is more likely to stay focused on the ten-year goal rather than the quarterly earnings beat." — Source: Business Insider Interview

- On Shared Vision: "We don't try to tell CEOs how to run their businesses; we find the best ones and let them do their jobs." — Source: Forbes Profile

Part 3: Identifying Disruptive Innovation

- On Architecting the Future: "We look for the companies that are not just participating in a market, but are architecting the future of their industry." — Source: Zevenbergen Capital Insights

- On Perpetual Disruption: "Innovation and disruption are not one-time events; they are perpetual forces that constantly create new winners." — Source: Virtus Portfolio Manager Insights

- On Lifestyle-Based Research: "To find the next great company, watch how younger generations are changing the way they shop, communicate, and live." — Source: University of Washington Foster School

- On Inflection Points: "The most lucrative time to invest is when a company’s growth is just beginning to inflect and move toward mass adoption." — Source: Business Insider Interview

- On the Space Economy: "The intersection of AI, robotics, and the space economy represents the next major frontier for disruptive growth." — Source: Zevenbergen Capital Insights

- On Infrastructure vs. Application: "Sometimes the best growth is found in the infrastructure that makes other innovations possible, like data centers for AI." — Source: Virtus Portfolio Manager Insights

- On Organic Growth: "We avoid companies that grow primarily through acquisitions; we want to see organic, unit-volume growth driven by demand." — Source: Business Insider Interview

- On Challenging Wisdom: "Don't be afraid to invest in something that challenges the conventional wisdom of Wall Street." — Source: University of Washington Foster School

- On the 'Everything Store': "Early on, it was clear that the internet would change the retail landscape forever; Amazon was the logical outcome of that shift." — Source: Forbes Profile

- On Scaling Potential: "We look for businesses that can double or triple in size over the next decade because their addressable market is so vast." — Source: Zevenbergen Capital Insights

Part 4: The Discipline of Concentration

- On Building Wealth: "Wealth is created through concentrated positions, not through broad diversification across hundreds of names." — Source: University of Washington Foster School

- On the Bill Gates Example: "Did Bill Gates make his billions by being diversified? No. He owned one company and he created wealth." — Source: Forbes Profile

- On Diversification for Preservation: "Diversification is for wealth preservation, but concentration is for wealth creation." — Source: Zevenbergen Capital Insights

- On Portfolio Size: "We maintain a concentrated portfolio of 30 to 50 names because those are the only companies we have the highest conviction in." — Source: Business Insider Interview

- On High Active Share: "To outperform the market, your portfolio must look very different from the index." — Source: Virtus Portfolio Manager Insights

- On Owning the Best: "Our strategy is to own the best of the best and let them represent the majority of our exposure." — Source: Zevenbergen Capital Insights

- On Index Hugging: "If you want the returns of the index, buy the index; if you want to create wealth, you have to be willing to be wrong and be different." — Source: Forbes Profile

- On Conviction: "Conviction is the filter that allows us to stay concentrated when others are panicking and diversifying." — Source: Virtus Portfolio Manager Insights

- On Over-Diversification: "Spreading your capital too thin across mediocre companies is one of the quickest ways to erode your long-term potential." — Source: University of Washington Foster School

Part 5: The Art of Extreme Patience

- On Holding Winners: "The biggest sell decision you have is actually the decision not to sell and to stay invested in a winning company." — Source: Forbes Profile

- On Being Patient: "We strive to be the most patient investors in the room, often holding positions for ten years or more." — Source: Zevenbergen Capital Insights

- On Quarterly Noise: "Quarterly earnings misses are often just noise; if the long-term thesis remains intact, we stay the course." — Source: Virtus Portfolio Manager Insights

- On Compounding Power: "The real power of compounding only happens in the later years of a long-term holding." — Source: University of Washington Foster School

- On Time Horizon as an Edge: "Our edge is our time horizon; while others are trading on seconds, we are thinking about the next decade." — Source: Business Insider Interview

- On Doing Nothing: "In growth investing, the hardest thing to do is often nothing—simply letting your winners run." — Source: Forbes Profile

- On Horizon Arbitrage: "Market volatility creates opportunities for those who can look past the next few months to the next few years." — Source: Virtus Portfolio Manager Insights

- On Powering Through: "You have to have the stomach to hold through 50% drawdowns if you want to see a 100-fold return." — Source: University of Washington Foster School

- On Consistency: "Our investment process is consistent because the forces of innovation are consistent over time." — Source: Zevenbergen Capital Insights

Part 6: Revenue, Valuation, and Growth Metrics

- On Revenue as a Mantra: "Our primary focus is revenue, revenue, revenue—it is the purest indication of customer demand." — Source: Forbes Profile

- On Valuation Agnosticism: "High initial valuations at an IPO rarely matter if the company has the potential to grow its revenue at 30% for a decade." — Source: Virtus Portfolio Manager Insights

- On Revenue as Fuel: "Revenue growth provides the fuel for a company to reinvest in itself and stay ahead of the competition." — Source: Zevenbergen Capital Insights

- On Conservative Estimates: "We look for situations where Wall Street’s conservative expectations provide a margin for outperformance when the company executes." — Source: Business Insider Interview

- On Unit Volume: "We look for unit volume growth rather than price increases, as it shows real market penetration." — Source: University of Washington Foster School

- On Financial Flexibility: "A strong balance sheet is a tool that allows a growth company to be aggressive when others are being defensive." — Source: Zevenbergen Capital Insights

- On Ignoring P/E Multiples: "P/E multiples are a snapshot of the past; we are focused on the cash flow and earnings potential of the future." — Source: Virtus Portfolio Manager Insights

- On Adoption Metrics: "The most important metric is how quickly a new technology or service is being adopted by its target customers." — Source: Business Insider Interview

- On Bottom-Up Research: "Our research is intensely bottom-up; we care more about the individual company's metrics than the sector's average." — Source: Zevenbergen Capital Insights

Part 7: Navigating Volatility and Macro Noise

- On Macro Distractions: "Stay above the fray of interest rates, tariffs, and trade wars—they are often just temporary distractions from long-term fundamentals." — Source: Zevenbergen Capital Insights

- On Volatility as Opportunity: "We view elevated stock price volatility as an opportunity for long-term wealth creation, not a risk to be avoided." — Source: Virtus Portfolio Manager Insights

- On Bear Markets: "Recognize that you will have bear markets, but set that aside and ask: what kind of companies do I want to be invested in regardless?" — Source: Forbes Profile

- On Sentiment as a Signal: "When headline news is overwhelmingly negative, it often means there is an opportunity for those with conviction." — Source: University of Washington Foster School

- On Defining Risk: "Risk is not volatility; risk is the permanent loss of capital because a business failed to execute." — Source: Zevenbergen Capital Insights

- On Ignoring Headlines: "Headlines are written for the day; we invest for the decade." — Source: Business Insider Interview

- On Market Timing: "Market timing doesn't work; staying invested in great businesses is the only way to capture their full potential." — Source: Forbes Profile

- On Internal Focus: "Focus on what is happening inside the company's four walls rather than the external macroeconomic noise." — Source: Virtus Portfolio Manager Insights

- On Resilience in Crashes: "The 1987 crash taught me that a major market disruption can be the perfect equalizer for a new, independent firm." — Source: University of Washington Foster School

Part 8: Lessons on Career and Resilience

- On Creating Opportunity: "If you can't find the job you want, you have to be willing to create it for yourself." — Source: University of Washington Foster School

- On the Glass Ceiling: "The thick glass ceiling of traditional banking in the early 80s was the primary motivator for me to start my own firm." — Source: Forbes Profile

- On Never Learning to Type: "I figured if I never learned to type, they’d eventually have to let me sit up front and read the Wall Street Journal." — Source: University of Washington Foster School

- On Starting Small: "We started with just $500,000 and one client; you don't need a massive institution behind you to be a great investor." — Source: Business Insider Interview

- On Wearing Many Hats: "Early in your career, join a startup or a small firm where you can learn how every part of the business works." — Source: University of Washington Foster School

- On Responsibility of Wealth: "Giving back to the community is not just a duty; it ensures the health of the economic environment we all work in." — Source: Forbes Profile

- On Education: "Education is the bedrock of community health and the ultimate driver of long-term economic prosperity." — Source: University of Washington Foster School

- On Active Management: "Long live active management—there will always be a place for those who can find the next generation of winners." — Source: Zevenbergen Capital Insights

- On Taking the Path Less Traveled: "Don't be afraid to take the startup path; you have nothing to lose when you are young and everything to gain in experience." — Source: University of Washington Foster School