Pat Dorsey is the founder of Dorsey Asset Management and former Director of Equity Research at Morningstar. He is best known for developing a clear framework to identify "economic moats," the structural advantages that protect a company's profits from competitors. This profile distills his practical approach to competitive strategy, capital allocation, and valuation.

Part 1: The Philosophy of Economic Moats

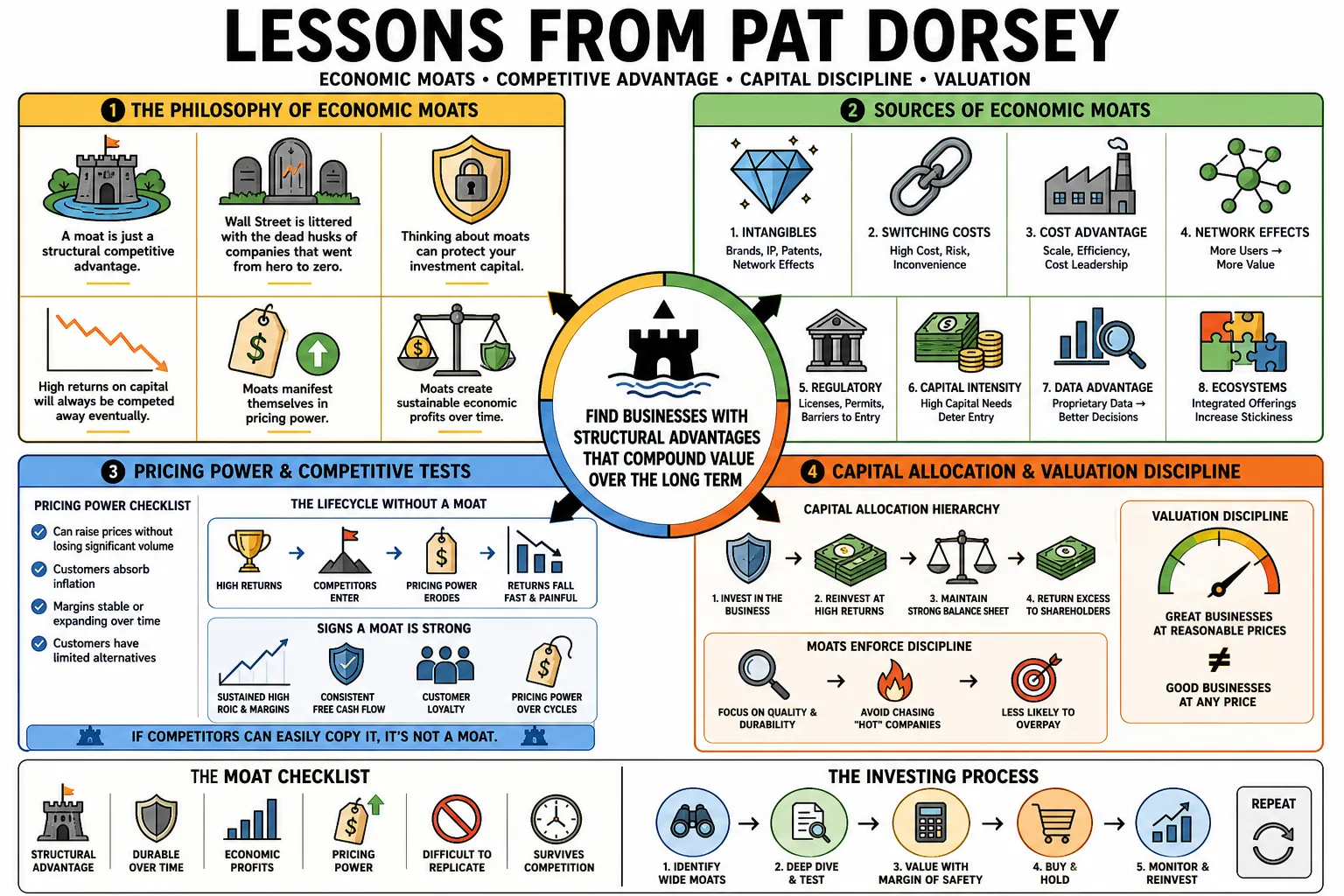

- On the nature of moats: "A moat is just a structural competitive advantage, something that's an attribute of a business that makes it difficult to compete with them." — Source: [Morningstar]

- On corporate mortality: "Wall Street is littered with the dead husks of companies that went from hero to zero in a heartbeat." — Source: [The Little Book That Builds Wealth]

- On investment discipline: "Thinking about moats can protect your investment capital... it enforces investment discipline, making it less likely that you will overpay for a hot company." — Source: [The Little Book That Builds Wealth]

- On regression to the mean: "High returns on capital will always be competed away eventually, and for most companies, and their investors, the regression is fast and painful." — Source: [The Little Book That Builds Wealth]

- On pricing power: "Moats manifest themselves in pricing power. A company that can't raise prices is unlikely to have a strong moat." — Source: [Morningstar]

- On confusing the business with the stock: "If you avoid the mistake of confusing a great company with a great investment, you'll already be ahead of many of your investing peers." — Source: [The Five Rules for Successful Stock Investing]

- On cash flow protection: "When you buy shares of the company with the moat, you're buying a stream of cash flows that is protected from competition for many years." — Source: [The Little Book That Builds Wealth]

- On predictability: "Moats give you time. They make the future a little bit more predictable." — Source: [The Little Book That Builds Wealth]

- On structural truths: "Moats are structural characteristics inherent to a business. It's not a hot product, it's not a great CEO, and it's not a large market share." — Source: [Dorsey Asset Management]

- On finding hidden value: "If you can see moats where others don't, you'll pay bargain prices for the great companies of tomorrow." — Source: [The Little Book That Builds Wealth]

Part 2: Intangible Assets and Brands

- On the reality of brands: "A brand creates an economic moat only if it increases the consumer's willingness to pay or increases customer captivity." — Source: [The Little Book That Builds Wealth]

- On brand popularity: "Brands can create durable competitive advantages, but the popularity of the brand matters much less than whether it actually affects consumers' behavior." — Source: [The Little Book That Builds Wealth]

- On pricing premiums: "If a company can charge more for the same product than its peers just by selling it under a brand, that brand very likely constitutes a formidable economic moat." — Source: [The Little Book That Builds Wealth]

- On search costs: "A brand is only a moat if it allows the company to charge more for a similar product or if it reduces the customer's search costs." — Source: [Invest Like the Best]

- On patents: "Patents are a great source of economic moats, but you have to make sure the company has a portfolio of them, rather than relying on just one or two blockbusters." — Source: [The Little Book That Builds Wealth]

- On regulatory licenses: "Regulatory moats can be incredibly powerful because the government is actively keeping competitors out of your market." — Source: [The Five Rules for Successful Stock Investing]

- On niche dominance: "You'll have better odds hunting for ideas in industries where managers only need to hurdle one-foot bars to succeed than you will looking for long-term winners in industries where the barriers to success are much higher." — Source: [The Little Book That Builds Wealth]

- On empty brands: "If a brand doesn't lead to higher returns on capital, it's just a name, not a moat." — Source: [Invest Like the Best]

- On continuous innovation: "Patents in technology frequently expire or are engineered around, making the true underlying moat the accumulated institutional know-how rather than a single filing." — Source: [Morningstar]

Part 3: Switching Costs

- On defining switching costs: "A business with a switching cost moat is secured by the fact that the benefits of switching to a competitor's products or services are outweighed by the disadvantages of sticking with the company." — Source: [The Little Book That Builds Wealth]

- On customer captivity: "When a business relies on switching costs, it might not have a happy customer base. The customers stay because they are captive, not because they are loyal." — Source: [Dorsey Asset Management]

- On enterprise software: "People don't use SAP because they have a huge affinity for the brand. They use it because the switching costs are really high." — Source: [Morningstar]

- On risk as a switching cost: "The cost of switching comes in many forms, including the explicit costs and the risk of product failure." — Source: [The Little Book That Builds Wealth]

- On the power of inertia: "Switching costs boil down to a simple question of whether the monetary and operational cost of adopting a competing product outweighs the immediate benefits." — Source: [Morningstar]

- On integration: "The switching costs of an Oracle database are inherent to the way databases are used in business. Contrast that with a hot product that may come or go." — Source: [Dorsey Asset Management]

- On absent switching costs: "Switching from the nearby gas station to the cheaper one costs you maybe 5 to 10 minutes extra of time. That's it." — Source: [The Little Book That Builds Wealth]

- On retail vulnerability: "Consumer retail and restaurant chains inherently suffer from low switching costs, forcing them to rely heavily on scale or brand to survive." — Source: [The Little Book That Builds Wealth]

- On B2B advantages: "In B2B software, switching costs tends to be the most common source of competitive advantage." — Source: [Morningstar]

Part 4: Network Effects

- On the fundamental network effect: "The network effect occurs when the value of a product or service naturally increases as more people participate in using it." — Source: [The Little Book That Builds Wealth]

- On natural monopolies: "Businesses with strong network effects tend to become natural monopolies or oligopolies, like Visa, Mastercard, or eBay." — Source: [The Five Rules for Successful Stock Investing]

- On liquidity and marketplaces: "For marketplace businesses, liquidity acts as the ultimate moat. Buyers go where the sellers are, and sellers go where the buyers are." — Source: [Invest Like the Best]

- On digital advertising: "If God invented an advertising platform, it would be called Facebook. Digital advertising offers the holy grail that has been sought for decades: measurement of return." — Source: [Invest Like the Best]

- On non-linear scaling: "Network effects compound rather than scale linearly, which makes it exponentially harder for a new entrant to catch up to an established incumbent." — Source: [Morningstar]

- On local versus global networks: "Some network effects are geographically constrained, like regional classifieds, while others are global. The physical or digital boundaries define the limits of the moat." — Source: [Morningstar]

- On displacing networks: "It is extraordinarily difficult to break a network effect unless a fundamental technological shift renders the entire network obsolete." — Source: [Invest Like the Best]

- On data aggregation: "Aggregating data across thousands of users creates an analytical network effect where the insights become a product that smaller competitors cannot replicate." — Source: [Invest Like the Best]

- On physical networks: "Established logistical route networks act as a physical network effect because new competitors cannot match the existing routing density without massive upfront capital." — Source: [The Little Book That Builds Wealth]

Part 5: Cost Advantages and Scale

- On true cost advantages: "Cost advantages can stem from cheaper processes, better locations, unique assets, or massive scale." — Source: [The Little Book That Builds Wealth]

- On process advantages: "Process advantages are often the hardest to maintain, because competitors can usually copy a new process over time." — Source: [The Little Book That Builds Wealth]

- On location advantages: "A unique location is a fantastic moat. A garbage dump or an aggregate quarry near a major city is a localized monopoly." — Source: [The Little Book That Builds Wealth]

- On economies of scale: "Scale moats work because fixed costs are spread over a larger base. The bigger player can offer lower prices and still make a profit." — Source: [The Little Book That Builds Wealth]

- On scale in distribution: "Distribution scale is brutal to compete against. If you have a truck driving down the street dropping off 10 boxes, and the competitor is dropping off one, you win." — Source: [Invest Like the Best]

- On the limits of size: "Being large is not a moat on its own. The scale must translate into a structural cost advantage that competitors cannot buy their way into." — Source: [Morningstar]

- On niche dominance over absolute size: "Being the largest participant in a highly specialized, small market is frequently a stronger moat than being a medium player in a massive market." — Source: [The Little Book That Builds Wealth]

- On relative scale: "It is relative scale that matters most. A company needs to be significantly larger than its closest competitor in the specific market it serves." — Source: [Morningstar]

- On unique assets: "Owning an exclusive asset, such as a low-cost mine or a long-term lease at below-market rates, provides an unbreachable cost advantage for the life of the asset." — Source: [The Five Rules for Successful Stock Investing]

- On unit economics: "You can't assume high market share equates to a cost advantage; you have to unpack the unit economics." — Source: [Dorsey Asset Management]

Part 6: Management and Capital Allocation

- On betting on the horse: "A great business with a wide moat can survive mediocre management, but even the best management team in the world will struggle to generate high returns in a business with poor economics." — Source: [Invest Like the Best]

- On structural limits: "The smartest manager in the world will not make an airline have the economics of a software company." — Source: [Dorsey Asset Management]

- On the sandcastle analogy: "The best engineer in the world can't build a 10-story sandcastle." — Source: [The Little Book That Builds Wealth]

- On capital allocation: "While moats are critical, equally important is how companies allocate the capital generated, or made possible, by the existence of the moat." — Source: [Invest Like the Best]

- On evaluating allocation qualitative: "You can't trust that management will allocate capital rationally; you have to gather supporting evidence." — Source: [Dorsey Asset Management]

- On reinvestment runways: "A long runway for reinvestment maximizes the value of competitive advantage and lowers the risk of value-destructive capital allocation." — Source: [Dorsey Asset Management]

- On misaligned incentives: "Managers who are paid handsomely to misallocate capital will do so. Incentives matter." — Source: [Masters in Business]

- On executive ego: "Most people get to the top of organizations by having aggressive personalities and large egos, and those can be very dangerous when you're in charge of strategic decisions and capital allocation." — Source: [Dorsey Asset Management]

- On returning capital: "Dividends are not an admission of defeat, they are a declaration of victory for mature companies that can no longer reinvest at extremely high rates." — Source: [Dorsey Asset Management]

- On exceptional talent: "A tiny minority of managers can create enormous value via astute capital allocation if they don't start with great horses." — Source: [Morningstar]

Part 7: Valuation and Margin of Safety

- On price and quality: "Even the best company will hurt your portfolio if you pay too much for it. Price matters, always." — Source: [The Little Book That Builds Wealth]

- On the definition of safety: "The margin of safety is what allows you to be wrong and still not lose your shirt." — Source: [The Five Rules for Successful Stock Investing]

- On analytical limits: "At its core, investing is about predicting the future cash flows of a business, which means that investors like us are inevitably going to make mistakes." — Source: [The Five Rules for Successful Stock Investing]

- On avoiding disasters: "One person's hot growth stock is another's disaster waiting to happen... you're putting your money at risk, so you should know what you're buying." — Source: [The Five Rules for Successful Stock Investing]

- On measuring value: "Finding great companies is only half of the investment process, the other half is assessing what the company is worth." — Source: [The Five Rules for Successful Stock Investing]

- On the investment process: "The basic investment process is simple: Analyze the company and value the stock." — Source: [The Little Book That Builds Wealth]

- On cash machines: "If a firm's free cash flow as a percentage of sales is around 5 percent or better, you've found a cash machine." — Source: [The Five Rules for Successful Stock Investing]

- On when to sell: "Investors should sell when the business fundamentals deteriorate, the competitive advantage disappears, or the stock price drastically exceeds intrinsic value." — Source: [The Five Rules for Successful Stock Investing]

- On value tracking price: "In the short term, the market can be capricious, but over the long haul, stock prices tend to track the value of the business." — Source: [The Five Rules for Successful Stock Investing]

Part 8: The Psychology of the Investor

- On independent work: "Thoroughly investigate every stock you buy. Unless you understand the business inside and out, you shouldn't own it." — Source: [The Five Rules for Successful Stock Investing]

- On informational disadvantages: "If you buy from people who know more than you about what they're selling, and you sell to people who know more than you about what they're buying, you'll end up knowing much more than they do about being broke." — Source: [The Five Rules for Successful Stock Investing]

- On banning stock charts: "Stock charts provide zero information about the underlying future cash flows of a business and instead trigger cognitive biases that lead to reactive decision-making." — Source: [Dorsey Asset Management]

- On independent thinking: "You'll do better as an investor if you think for yourself and seek out bargains in parts of the market that everyone else has forsaken, rather than buying the flavor of the month in the financial press." — Source: [The Five Rules for Successful Stock Investing]

- On the scarcest resource: "The scarcest resource in investing is human capital, meaning time and focus, rather than financial capital." — Source: [Dorsey Asset Management]

- On the search for no: "When I analyze a stock, I try to find a reason to say 'no' as soon as possible. If you haven't found a reason to say no within a few minutes, you've found a potentially interesting stock." — Source: [Invest Like the Best]

- On flawed metrics: "Quantitative screens are much less useful than they were 20, 30 years ago, simply because returns on capital are a flawed metric... the worst software company in the world is going to have high returns on capital because it has no capital." — Source: [Morningstar]

- On portfolio concentration: "Investors who truly understand their holdings do not need to dilute their returns by investing in their thirtieth best idea." — Source: [Dorsey Asset Management]

- On humility: "Smart investors learn deeply from their own mistakes. A long-term approach requires balancing high conviction with the humility to admit when the initial analysis was wrong." — Source: [Dorsey Asset Management]