Lessons from Peter Cundill

Over forty years, Canadian investor Peter Cundill traveled the globe buying heavily discounted companies for half their liquidation value. He adapted Benjamin Graham’s mechanical net-net strategy for international markets, anchoring his process with obsessive journaling and a strict "Sell Half" rule. This collection breaks down how Cundill found hidden assets and handled the psychological grind of deep value investing.

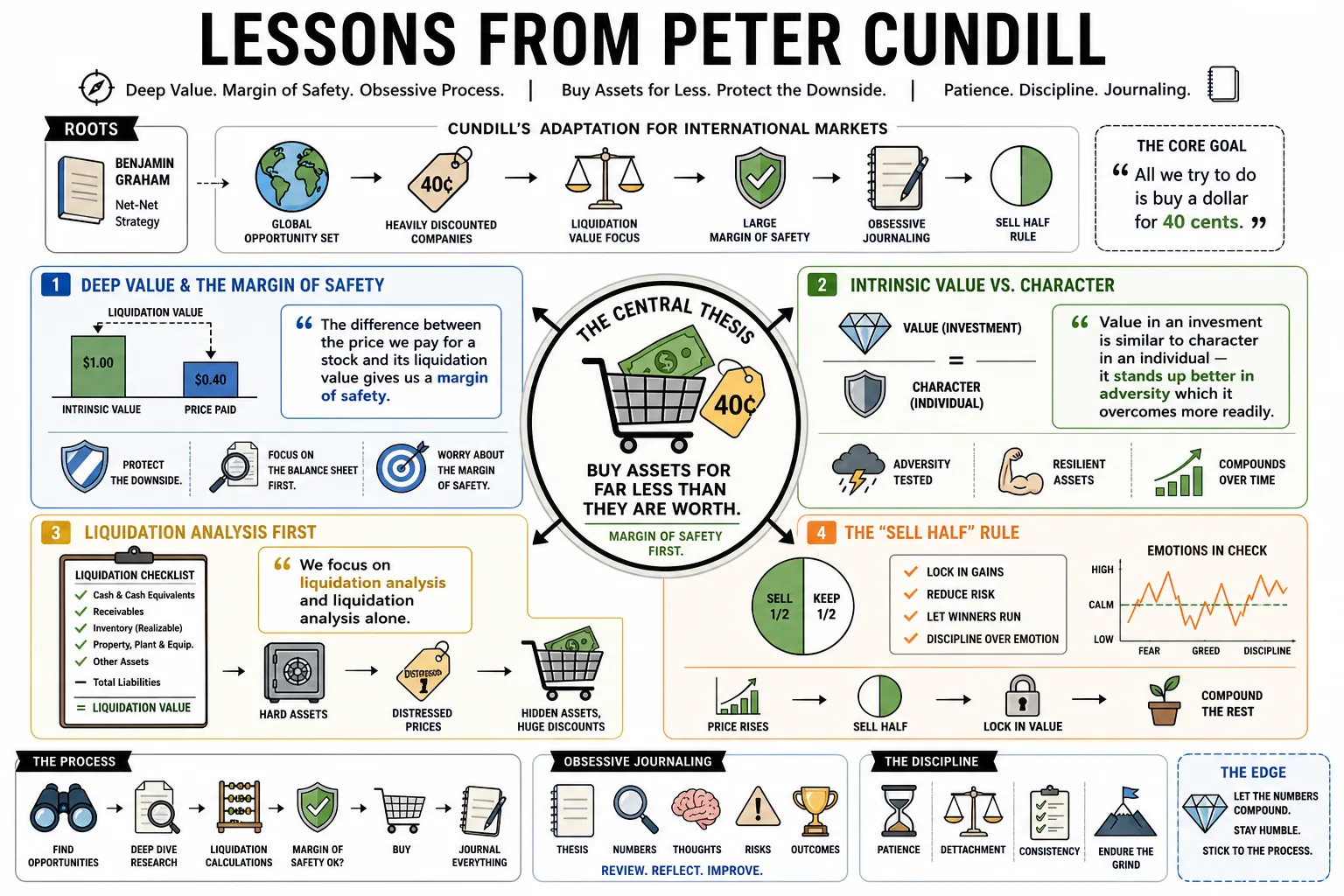

Part 1: Deep Value & The Margin of Safety

- On the Core Goal: "All we try to do is buy a dollar for 40 cents." — Source: [There's Always Something to Do]

- On the Margin of Safety: "The difference between the price we pay for a stock and its liquidation value gives us a margin of safety." — Source: [The Peter Cundill Journals]

- On Intrinsic Value vs. Character: "Value in an investment is similar to character in an individual — it stands up better in adversity which it overcomes more readily." — Source: [Rational Walk Review]

- On Downside Protection: "Protect the downside. Worry about the margin of safety." — Source: [There's Always Something to Do]

- On the Balance Sheet: "We always look at the margin of safety in the balance sheet and then worry about the business." — Source: [Cundill Value Fund Archives]

- On Liquidation Analysis: "We focus on liquidation analysis and liquidation analysis alone." — Source: [The Peter Cundill Journals]

- On Cheap Stocks: "I bought stuff at 3.5 cents once and I thought it can't go down to zero. It can." — Source: [There's Always Something to Do]

- On the One Rule: "There is no investment rule that remains immutable except the margin of safety." — Source: [Rational Walk Review]

- On Benjamin Graham: Discovering Graham's Security Analysis in 1973 was his "Road to Damascus" moment, shifting him forever from a general money manager to a deep value purist. — Source: [There's Always Something to Do]

- On Unloved Assets: "One needs not just to smell the lion's carcass from afar but to be able to imagine that the bees may have made honey inside it." — Source: [There's Always Something to Do]

Part 2: The Mechanics of Net-Net Investing

- On Book Value: He demanded that a stock's share price trade strictly below its book value before it could be considered a candidate. — Source: [Cundill Value Fund Archives]

- On Net Working Capital: The ideal investment traded for less than its net working capital minus all long-term debt obligations. — Source: [There's Always Something to Do]

- On Historical Lows: A stock needed to trade at less than half of its former high, and ideally near its absolute all-time low. — Source: [The Peter Cundill Journals]

- On the P/E Ratio: He required the price-to-earnings multiple to be less than ten, or the inverse of the long-term corporate bond rate. — Source: [There's Always Something to Do]

- On Profitability: Companies had to be currently profitable, with absolutely no deficits recorded over the preceding five years. — Source: [Rational Walk Review]

- On Dividends: He preferred deep value stocks that still paid a regular dividend, especially one that had increased over time. — Source: [Cundill Value Fund Archives]

- On Earnings Predictions: "The trick is not necessarily to predict what the earnings are going to be but to have a clear conviction that the company isn't going bust." — Source: [There's Always Something to Do]

- On the Cigar Butt Approach: He comfortably embraced the "cigar butt" label, favoring a wonderful price for a fair business over a fair price for a wonderful business. — Source: [The Peter Cundill Journals]

- On Systemizing Value: By strictly adhering to predefined mechanical screens, he bypassed the emotional trap of falling in love with a company's narrative. — Source: [There's Always Something to Do]

Part 3: Global Travel & Uncovering Bargains

- On "There's Always Something to Do": The phrase, originally borrowed from Irving Kahn, became his mantra—if domestic markets are overvalued, look internationally. — Source: [There's Always Something to Do]

- On Geographic Contrarianism: He made a habit of physically traveling to the country whose stock market had performed the absolute worst in the prior year. — Source: [The Peter Cundill Journals]

- On International Bargains: While most of his peers stayed in North America, he believed that accounting principles translated globally if you did the hard forensic work. — Source: [Rational Walk Review]

- On Japan in the 1990s: He successfully identified massive net-net opportunities in Japan after the bubble burst, taking advantage of heavily depressed balance sheets. — Source: [Cundill Value Fund Archives]

- On Boot-on-the-Ground Research: He believed traveling to obscure markets provided a qualitative edge that purely reading reports in an office could not match. — Source: [There's Always Something to Do]

- On Scandinavia and Africa: No market was too obscure; he hunted for value wherever the discrepancy between price and liquidation value was the widest. — Source: [The Peter Cundill Journals]

- On Global Breadth: "There is always something to do. You just need to look harder, be creative and a little flexible." — Source: [There's Always Something to Do]

- On Physical Presence: Showing up in foreign countries helped him gauge the cultural reality of corporate governance and hidden assets. — Source: [Rational Walk Review]

- On Escaping the Crowd: Traveling globally naturally insulated him from the groupthink and media noise of Wall Street. — Source: [Cundill Value Fund Archives]

Part 4: The Psychology of Patience & Contrarianism

- On the Master Trait: "The most important attribute for success in value investing is patience, patience, and more patience." — Source: [There's Always Something to Do]

- On the Scarcity of Patience: "The majority of investors do not possess this characteristic." — Source: [The Peter Cundill Journals]

- On Patience vs. Stubbornness: "The difference between patience and stubbornness in investing is the ability to examine your assumptions." — Source: [Rational Walk Review]

- On Going it Alone: "Being out on a limb, alone and appearing to be wrong is just part of the territory of value investing." — Source: [There's Always Something to Do]

- On the Inevitability of Markets: "Sooner or later, the market will do what it has to do to prove the majority wrong." — Source: [Cundill Value Fund Archives]

- On Surviving Drawdowns: He accepted that even the greatest investments frequently experience 40% to 50% drawdowns, which investors must endure without panicking. — Source: [The Peter Cundill Journals]

- On Market Euphoria: When markets are widely euphoric, value investors should naturally be selling off assets and building cash reserves. — Source: [There's Always Something to Do]

- On Simplicity vs. Elegance: "Intellectually active people are particularly attracted to elegant concepts, which can have the effect of distracting them from the simpler, more fundamental truths." — Source: [Rational Walk Review]

- On Corporate Pasts: "I try to keep in mind Oscar Wilde's comment that 'saints always have a past and sinners always have a future,' so no investment should be ruled out simply on the basis of past history." — Source: [There's Always Something to Do]

- On Compound Interest: "Think long term and remember that the big rewards accrue with compound annual rates of return." — Source: [The Peter Cundill Journals]

Part 5: Sell Disciplines & Managing Gains

- On the "Sell Half" Rule: "When a stock doubles, sell half — then what you have is a free position." — Source: [There's Always Something to Do]

- On the Art of the Remainder: "Then it becomes more of an art form. When you sell depends on individual circumstances." — Source: [The Peter Cundill Journals]

- On Creating "House Money": Selling half upon a double effectively writes the cost basis of the remaining shares down to zero. — Source: [Cundill Value Fund Archives]

- On the Temptation to Sell Early: "This is a recurring problem for most value investors — that tendency to buy and to sell too early." — Source: [There's Always Something to Do]

- On the Relief of Breaking Even: "The virtues of patience are severely tested and you get to thinking it's never going to work and then finally your ship comes home and you're so relieved that you sell before it's time." — Source: [Rational Walk Review]

- On Automation: The "sell half" rule was implemented mechanically to override the human instinct to endlessly debate holding a winning position. — Source: [The Peter Cundill Journals]

- On the Tiffany & Co. Mistake: He formalized his exit rules after selling Tiffany at fair value, only to watch it get acquired for more than double his exit price shortly after. — Source: [There's Always Something to Do]

- On Timing: "The problem of the value investor is you have to be right on the timing side. And I am not sure value investors, for the most part, are very good at that." — Source: [Cundill Value Fund Archives]

- On Market Environments: "The 'value method of investing' will tend to give better results in slightly down to indifferent markets and less relatively sparkling results in a raging bull market." — Source: [There's Always Something to Do]

Part 6: Risk, Forecasting, and Uncertainty

- On Inside Information: "I do implicitly believe in Sir Sigmund Warburg's adage, 'All you get from inside information is a whiff of bad breath.'" — Source: [There's Always Something to Do]

- On the Paralysis of Rumors: He believed inside information "can actually paralyze reasoning powers; imperiling the cold detached judgement required so that the hard facts can shape decisions." — Source: [The Peter Cundill Journals]

- On the Purpose of Forecasting: "Forecasting should be used as a device to put both problems and opportunities into perspective." — Source: [Rational Walk Review]

- On the Danger of Forecasting: "It is a management tool, but it can never be a substitute for strategy, nor should it ever be used as the primary basis for portfolio investment decisions." — Source: [There's Always Something to Do]

- On Taking Gambles: "I will not take gambles, but it is part of my job description to be ready to take very carefully calculated risks." — Source: [Cundill Value Fund Archives]

- On Acceptable Odds: He only invested when "the downside is measurable and acceptable and the chances of a good profit appear to be better than 50%." — Source: [The Peter Cundill Journals]

- On Market Predictions: He distrusted macroeconomic prognostications, preferring bottom-up analysis of individual corporate balance sheets. — Source: [Rational Walk Review]

- On Consistency Over Sparkle: "What matters, however, is that the method will provide a consistent compound return." — Source: [There's Always Something to Do]

- On Evolution: "You never say you've got a system that's going to last forever. You always want to learn how to get it better." — Source: [Cundill Value Fund Archives]

Part 7: Hidden Assets & Adapting the Strategy

- On Moving Beyond Net-Nets: As pure net-nets became scarce in modern markets, he adapted his screens to hunt for off-balance-sheet assets. — Source: [There's Always Something to Do]

- On Historical Real Estate: He sought out old retailers and industrial firms that held physical real estate at its original historical cost rather than current market value. — Source: [The Peter Cundill Journals]

- On Overfunded Pensions: An overfunded corporate pension plan was treated as a hidden cash reserve that an activist or acquirer could eventually unlock. — Source: [Rational Walk Review]

- On Intangibles: He learned to recognize the latent value in brand names and patents that conservative accounting rules had entirely written down to zero. — Source: [Cundill Value Fund Archives]

- On Adjusting the Winning Game: Reflecting on advice from his peers, he understood that while value principles remain permanent, specific screening tactics must adapt to the era. — Source: [There's Always Something to Do]

- On Institutional Committees: "To my knowledge there are no good records that have been built by institutions run by committee." — Source: [The Peter Cundill Journals]

- On Benevolent Dictators: "In reality outstanding records are made by dictators, hopefully benevolent, but nonetheless dictators." — Source: [Rational Walk Review]

- On the One Great Opportunity: "I believe that there is probably one opportunity in every man's life which demands his knowledge, his guts, his self-esteem, and his judgement." — Source: [There's Always Something to Do]

- On Seizing the Moment: "If he seizes it with both hands and it is successful, he joins the first rank, if not he remains a mortal with feet of clay." — Source: [The Peter Cundill Journals]

Part 8: Journals, Habits, and the Examined Life

- On the Habit of Journaling: For 45 years, he maintained daily, meticulous handwritten journals to track his investments, psychology, and physical health. — Source: [There's Always Something to Do]

- On Auditing the Mind: The journals were used specifically as a forensic tool to combat emotional biases and review his past decision-making in real-time. — Source: [The Peter Cundill Journals]

- On Physical Discipline: He applied the same relentless discipline to his physical health, completing 22 marathons worldwide while traveling for investments. — Source: [Rational Walk Review]

- On Endowing History: He believed understanding history was so vital to markets that he endowed the Cundill History Prize at McGill University. — Source: [Cundill Value Fund Archives]

- On Clinical Detachment: Even when diagnosed with a rare neurodegenerative condition, he documented his physical symptoms in his journals with the same clinical detachment he used for stocks. — Source: [There's Always Something to Do]

- On Independent Thinking: The act of writing daily helped him form his own convictions away from the manic chatter of trading desks. — Source: [The Peter Cundill Journals]

- On the Power of Writing: Journaling forced his investment theses to be highly specific and falsifiable. — Source: [Rational Walk Review]

- On the "Indiana Jones" Persona: His combination of marathon running, global travel, and bargain hunting earned him a reputation as an adventurer rather than a typical desk-bound manager. — Source: [Cundill Value Fund Archives]

- On Long-Term Compounding in Life: He applied the concept of compounding to his physical health and intellect, viewing small daily inputs as the source of long-term outperformance. — Source: [There's Always Something to Do]

- On the Ultimate Goal: The mantra "there is always something to do" served as his philosophy for remaining engaged with the world as much as a stock-picking strategy. — Source: [The Peter Cundill Journals]