Lessons from Philip Fisher

Philip Fisher is best known for his 1958 book Common Stocks and Uncommon Profits, which pushed the financial industry away from pure statistical bargains and toward modern growth investing. He formalized the "scuttlebutt" method of research, arguing that investors should buy a concentrated portfolio of fast-growing companies and hold them for decades.

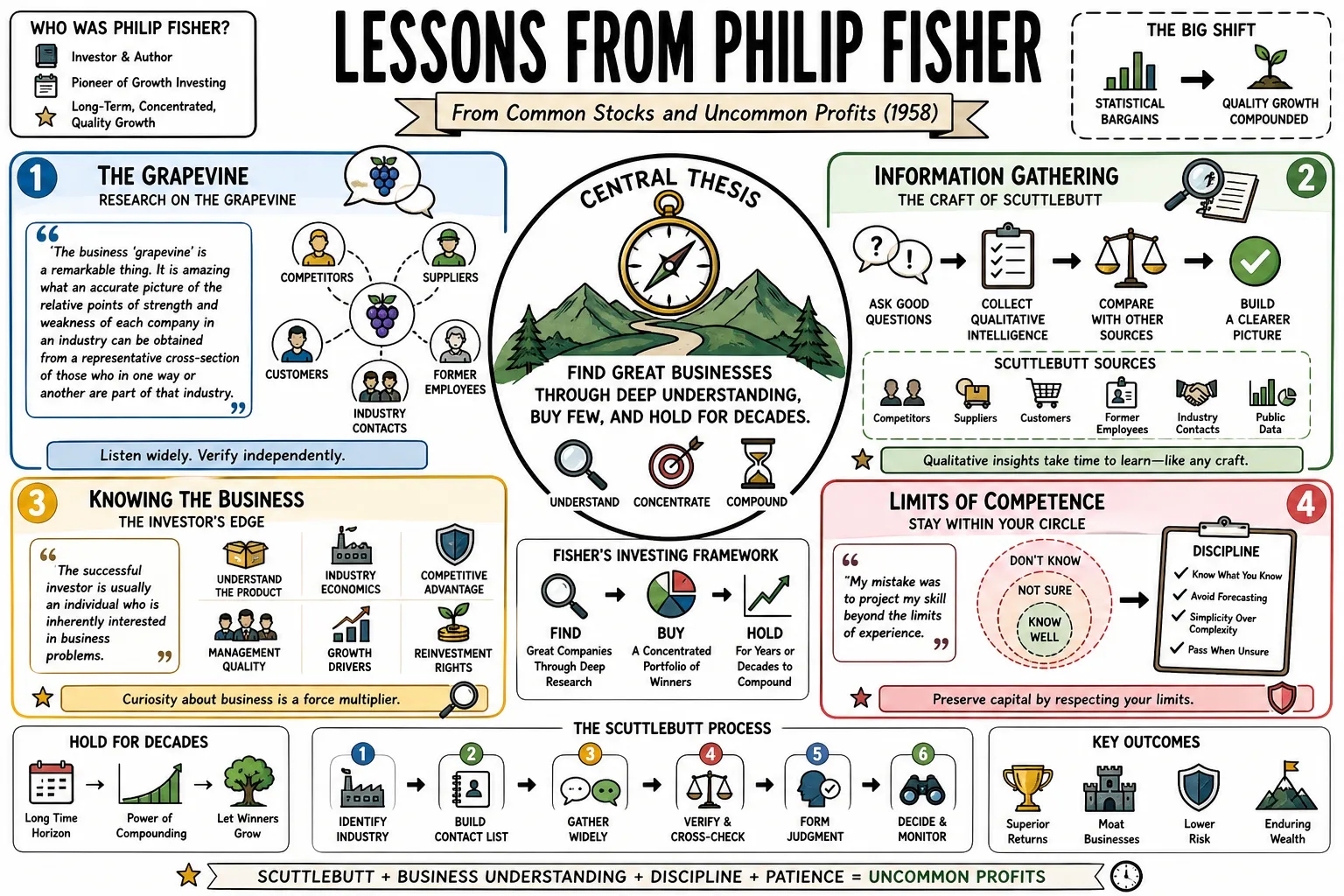

Part 1: The Scuttlebutt Method & Research

- On The Grapevine: "The business 'grapevine' is a remarkable thing. It is amazing what an accurate picture of the relative points of strength and weakness of each company in an industry can be obtained from a representative cross-section of those who in one way or another are part of that industry." — Source: [Investopaper]

- On Information Gathering: The craft of investing lies heavily in "scuttlebutt," gathering qualitative intelligence from competitors, suppliers, and former employees, which like all crafts takes time to learn. — Source: [Bookey]

- On Knowing the Business: "The successful investor is usually an individual who is inherently interested in business problems." — Source: [AZ Quotes]

- On Limits of Competence: "My mistake was to project my skill beyond the limits of experience. I began investing outside the industries which I believe I thoroughly understood." — Source: [Gracious Quotes]

- On Curiosity: Real research requires looking past financial statements and seeking out the raw, unvarnished opinions of people in the field. — Source: [Novel Investor]

- On Trade Associations: Executives at trade associations and industry groups often provide the most objective view of which competitors are truly innovating. — Source: [Investopaper]

- On Ex-Employees: Former employees are often a goldmine of information, provided one filters out personal grievances to find structural business insights. — Source: [Stockopedia]

- On Supplier Insights: A company’s suppliers usually know exactly how well a business is managing its operations and paying its bills long before the market does. — Source: [Novel Investor]

- On Competitor Respect: The highest praise a company can get often comes from a competitor who grudgingly admits they are losing market share to them. — Source: [Stockopedia]

Part 2: Business Quality & The 15 Points

- On True Growth: "The greatest investment reward comes to those who by good luck or good sense find the occasional company that over the years can grow in sales and profits far more than industry as a whole." — Source: [Goodreads]

- On Market Potential: Look for companies with products or services that have sufficient market potential to make a sizable increase in sales possible for at least several years. — Source: [Novel Investor]

- On Profit Margins: It is not enough to just grow sales; a truly outstanding company must have a worthwhile profit margin and a plan to maintain it. — Source: [Old School Value]

- On Research & Development: A company's research and development efforts must be effective in relation to its size, ensuring future product cycles. — Source: [Trustnet]

- On Sales Organization: Even the best products cannot generate uncommon profits without an above-average sales organization to deliver them to the market. — Source: [Novel Investor]

- On Industry Moats: "Constant leadership in engineering, not patents, is the fundamental source of protection." — Source: [Quoteswise]

- On Accounting Controls: An outstanding company must have precise cost analysis and accounting controls to know exactly where its profits are coming from. — Source: [Old School Value]

- On Marketing Mastery: "For a company to be a truly worthwhile investment, it must not only be able to sell its products, but also be able to appraise changing needs and desires of its customers." — Source: [Goodreads]

- On Equity Dilution: Avoid companies whose growth requires so much equity financing that the increased share count cancels out the benefits to existing stockholders. — Source: [Stockopedia]

- On Risk and Reward: "The true investment objective of growth is not just to make gains but to avoid loss." — Source: [Investopaper]

Part 3: The Importance of Management

- On Transparency: Outstanding management talks freely to investors when things are going well, but doesn't "clam up" when troubles or disappointments occur. — Source: [Novel Investor]

- On Integrity: A company must have management of unquestionable integrity; without it, all other business advantages are moot. — Source: [Trustnet]

- On Promoting Talent: "Never promote someone who hasn't made some bad mistakes, because if you do, you are promoting someone who has never done anything." — Source: [Gracious Quotes]

- On Execution: "Regardless of size, what really counts is a management having both a determination to attain further important growth and an ability to bring its plans to completion." — Source: [Goodreads]

- On Micromanagement: "Those organizations where the top brass personally interfere with and try to handle routine day-to-day operating matters seldom turn out to be the most attractive type of investments." — Source: [Quoteswise]

- On Executive Relations: A healthy corporate culture requires outstanding executive relations, where promotions are based on merit and internal politics are minimized. — Source: [Old School Value]

- On Labor Relations: Good labor and personnel relations are an underrated asset, saving a company from costly strikes and high turnover. — Source: [Stockopedia]

- On Outside Leadership: "A large company's need to bring in a new chief executive from the outside is a damning sign of something basically wrong with the existing management." — Source: [AZ Quotes]

- On Trust: "Getting to know the management of a company is like getting married. You never really know the girl until you live with her." — Source: [Investment Talk]

Part 4: Concentration vs. Diversification

- On High Standards: "I don't want a lot of good investments; I want a few outstanding ones." — Source: [Investopaper]

- On Over-Diversification: "Investors have been so oversold on diversification that fear of having too many eggs in one basket has caused them to put far too little into companies they thoroughly know and far too much in others which they know nothing about." — Source: [Gracious Quotes]

- On Portfolio Size: "Usually a very long list of securities is not a sign of the brilliant investor, but of one who is unsure of himself." — Source: [Investopaper]

- On Focus: "Practical investors usually learn their problem is finding enough outstanding investments, rather than choosing among too many." — Source: [Quoteswise]

- On Deep Knowledge: "I think a weakness of many people's approach to investment is that they try to be jacks of all trades and masters of none." — Source: [Investment Talk]

- On Finding the Few: "The heart of successful investing is knowing how to find the minority of stocks that in the years ahead will have spectacular growth in their per-share earnings." — Source: [Gracious Quotes]

- On Conviction: When you find an outstanding company, you must have the courage to buy a meaningful amount of it. — Source: [Novel Investor]

- On Knowing What You Own: It is far less risky to own a handful of businesses you understand intimately than dozens of businesses you only vaguely comprehend. — Source: [Goodreads]

- On Diluting Excellence: Adding mediocre companies to a portfolio merely to reduce volatility often ends up diluting the returns of your best ideas. — Source: [AZ Quotes]

Part 5: Market Timing & Patience

- On Predicting Prices: "It is often easier to tell what will happen to the price of a stock than how much time will elapse before it happens." — Source: [Goodreads]

- On Waiting for Returns: "There is the need for patience if big profits are to be made from investment." — Source: [Gracious Quotes]

- On Corrections: "More money has probably been lost by investors attempting to anticipate corrections than has been lost in the corrections themselves." — Source: [Novel Investor]

- On Waiting for the Perfect Moment: "Postponing an attractive purchase because of fear of what the general market might do will, over the years, prove very costly." — Source: [Gracious Quotes]

- On Volatility: "Finding the really outstanding companies and staying with them through all the fluctuations of a gyrating market proved far more profitable... than did the more colorful practice of trying to buy them cheap and sell them dear." — Source: [AZ Quotes]

- On Short-Term Trading: "I remember my sense of shock... when I read a recommendation to sell shares of a company... not based on any long-term fundamentals. Rather, it was that over the next six months the funds could be employed more profitably elsewhere." — Source: [Goodreads]

- On Inaction as an Action: Often, the most profitable decision an investor can make during a period of market turbulence is to do absolutely nothing. — Source: [Investopaper]

- On Time Horizons: The genuinely worthwhile profits in stock investing come from holding stocks that multiply in value over decades, not months. — Source: [Goodreads]

- On Ignoring the Noise: The day-to-day news cycle is built to trigger action, but the best investors train themselves to ignore it. — Source: [Novel Investor]

- On Natural Growth: Businesses take years to execute their strategies; investors must give them the time required to compound. — Source: [AZ Quotes]

Part 6: When to Buy and When to Sell

- On the Perfect Sell Time: "If the job has been correctly done when a common stock is purchased, the time to sell it is—almost never." — Source: [Investopaper]

- On Breaking Even: "More money has probably been lost by investors holding a stock they really did not want until they could 'at least come out even' than from any other single reason." — Source: [Gracious Quotes]

- On Taking Profits: "The inherently deceptive nature of the stock market... as such a stock rises to, say, 50 or 60 or 70, the urge to sell and take a profit now that the stock is 'high' becomes irresistible to many people." — Source: [Goodreads]

- On Valuation: "The only true test of whether a stock is 'cheap' or 'high' is not its current price in relation to some former price... but whether the company's fundamentals are significantly more or less favorable than the current financial-community appraisal of that stock." — Source: [Goodreads]

- On Selling Mistakes: If the original reasons for buying a stock are no longer valid, or if you made a factual error in your analysis, the stock should be sold immediately. — Source: [Novel Investor]

- On Selling Because of Price: Never sell an outstanding company simply because its price has run up and looks temporarily expensive. — Source: [Investopaper]

- On Buying Opportunities: The best time to buy an exceptional company is when it faces temporary, solvable problems that the market has dramatically overreacted to. — Source: [Stockopedia]

- On Missing Out: Selling a great company to lock in a 100% gain often means missing out on a 10,000% gain over the next two decades. — Source: [AZ Quotes]

- On Changing Fundamentals: The only legitimate reason to sell an outstanding business is if its management loses its drive or if its target market becomes fundamentally exhausted. — Source: [Old School Value]

Part 7: Contrarianism & Independent Thinking

- On Following the Crowd: "Doing what everybody else is doing at the moment, and therefore what you have an almost irresistible urge to do, is often the wrong thing to do at all." — Source: [Goodreads]

- On Independent Judgment: "The wise investor can profit if he can think independently of the crowd and reach the rich answer when the majority of financial opinion is leaning the other way." — Source: [Quoteswise]

- On Price vs. Value: "The stock market is filled with individuals who know the price of everything, but the value of nothing." — Source: [Stockwatch]

- On Wall Street Darlings: "Be extra careful when buying into companies and industries that are the current darlings of the financial community." — Source: [Investopaper]

- On Moral Courage: The basic ingredient in outstanding management is "the moral courage to act 'in opposition to the crowd' when your judgment tells you you are right." — Source: [Goodreads]

- On Blind Contrarianism: True independent thinking doesn't mean rejecting the prevailing view just to be contrary for the sake of being contrary; it means being right on the facts. — Source: [SFU]

- On Zigging and Zagging: "This matter of training oneself not to go with the crowd but to be able to zig when the crowd zags, in my opinion, is one of the most important fundamentals of investment success." — Source: [Quoteswise]

- On Herd Instinct: The human instinct to seek safety in the herd is the single greatest obstacle to achieving uncommon profits. — Source: [Gracious Quotes]

- On Recognizing Fads: An investor must learn to distinguish between a genuine structural shift in an industry and a temporary financial fad. — Source: [Novel Investor]

- On Emotional Discipline: The math behind investing is relatively simple, but the emotional discipline required to stand alone is exceptionally rare. — Source: [Investment Talk]

Part 8: The Philosophy of Long-Term Wealth

- On Peace of Mind: "Conservative investors sleep well." — Source: [Stockwatch]

- On Two Approaches: "There's the approach Ben Graham pioneered, which is to find something intrinsically so cheap that there is little chance of it having a big decline... Then there is my approach, which is to find something so good—if you don't pay too much for it—that it will have very, very large growth." — Source: [Investment Talk]

- On Mediocrity: "The company that doesn't pioneer, doesn't take chances, and merely goes along with the crowd is liable to prove a rather mediocre investment in this highly competitive age." — Source: [AZ Quotes]

- On Doing Things Right: "Nothing is worth doing unless it is worth doing right." — Source: [Gracious Quotes]

- On Conservative Investing: True conservatism in investing isn't about buying mature, slow-growing utility stocks; it's about buying heavily moated businesses with durable growth. — Source: [Novel Investor]

- On Future Orientation: Financial statements are backward-looking; the best investors spend their time trying to understand the realities of the future. — Source: [Stockopedia]

- On Innovation: Companies that rest on their laurels will inevitably lose their competitive edge; continuous innovation is the only true margin of safety. — Source: [Trustnet]

- On Knowledge as Protection: The deepest protection against investment loss is not a low price-to-earnings ratio, but an exhaustive understanding of the business. — Source: [Goodreads]

- On the Ultimate Goal: The pursuit of investing is not about endless trading, but about finding a few magnificent compounding machines and getting out of their way. — Source: [Investopaper]