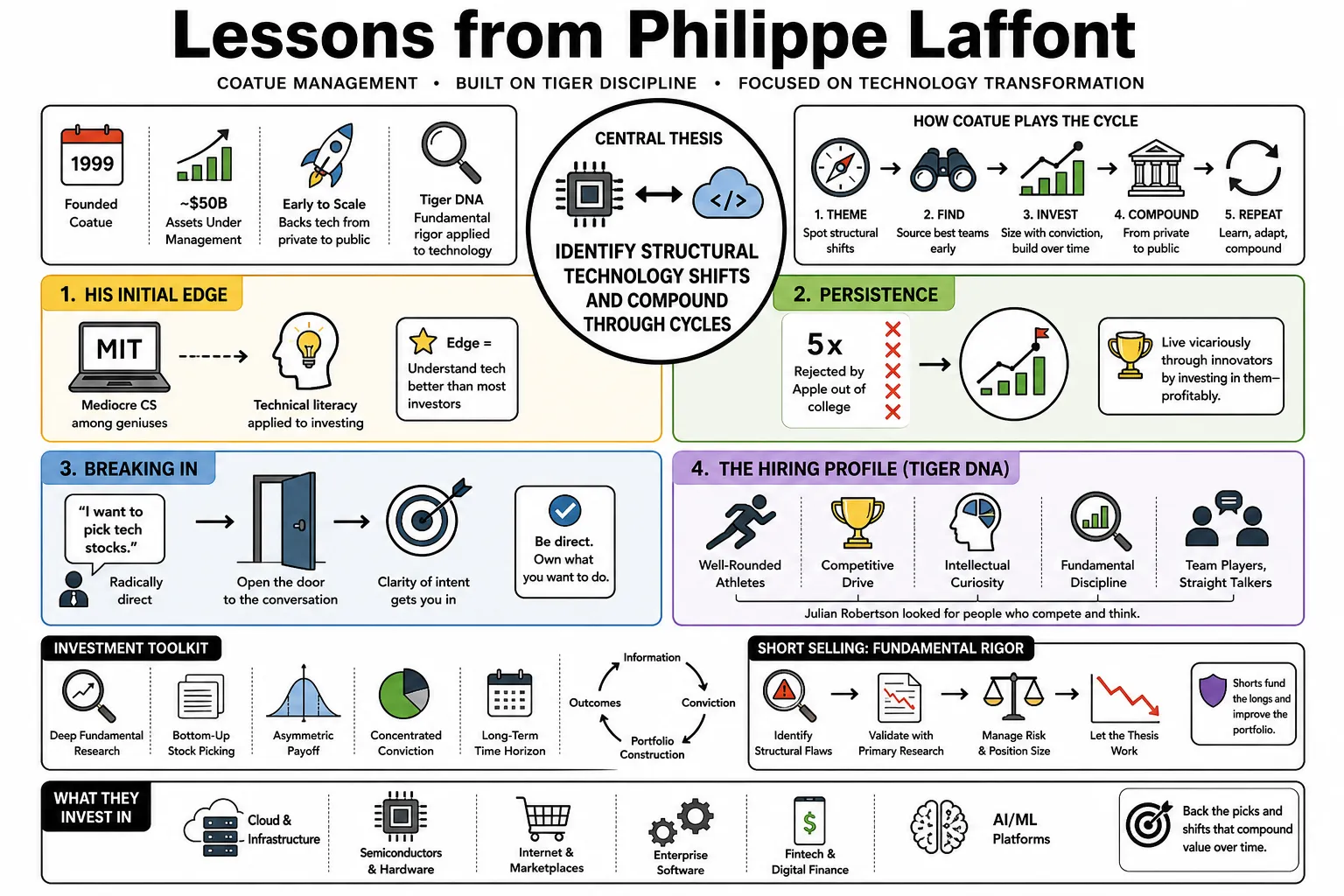

Philippe Laffont founded Coatue Management in 1999 and built it into a $50 billion fund by backing technology companies from their early private rounds through the public markets. As a former analyst under Julian Robertson, he applies fundamental hedge fund mechanics to evaluate structural technology shifts. This compilation organizes his public ideas on portfolio construction, short selling, and artificial intelligence to illustrate how his firm evaluates hardware and software cycles.

Part 1: The Tiger Foundation and Early Career

- On His Initial Edge: "Realizing I was a mediocre computer scientist among geniuses at MIT pushed me to finance, where I could use my technical literacy to pick stocks rather than write code." — Source: [Bloomberg Wealth]

- On Persistence: "Being rejected by Apple five times out of college taught me that you can live vicariously and profitably through innovators by investing in them rather than working for them." — Source: [Bloomberg Wealth]

- On Breaking In: "The best way to get hired in this industry early on was to be radically direct; I simply told the partners I wanted to pick tech stocks." — Source: [Invest Like the Best]

- On The Hiring Profile: "Julian Robertson looked for well-rounded athletes who were competitive, extroverted, and deeply curious people, rather than narrow financial specialists." — Source: [Marcellus Investment Managers]

- On The Ultimate Management Test: "The first question we learned to ask at Tiger was always whether the management was decent and honest. Character due diligence matters as much as financial modeling." — Source: [Hedge Fund Alpha]

- On Building Intellectual Environments: "The special sauce of Tiger Management was creating a culture of high-energy, continuous intellectual exchange." — Source: [Marcellus Investment Managers]

- On Trial By Fire: "Starting the fund in January 2000 with $50 million, just before the NASDAQ crashed 80 percent, was a brutal but invaluable lesson in extreme resilience." — Source: [Bloomberg Wealth]

- On Professional Restraint: "When people who refused to invest in me early on later realized their mistake, I found that vengeance is often best served by simply not saying anything." — Source: [Bloomberg Wealth]

- On The Nature of the Work: "Investing is a craft that requires immense risk and hard work; I am incredibly proud of that craft." — Source: [Bloomberg Wealth]

Part 2: The Philosophy of Long-Term Tech Investing

- On Identifying The Edge: "Few people in the market genuinely think about the long term. Patience and longer-term thinking are our primary competitive advantages." — Source: [12mv2]

- On The Time Horizon: "What can be great investments over three to five years? We try to ignore the short term and see the forest from the trees." — Source: [12mv2]

- On Paying For Growth: "Can you buy stocks at one times earnings many years out? How many years it takes is almost irrelevant if you latch onto truly great companies." — Source: [Coatue]

- On Finding The Next Era: "There are plenty of great ideas out there, but the winners in the next ten years are not going to be the same stocks that dominated the mobile and cloud era." — Source: [All-In Podcast]

- On Thematic Conviction: "Public investors generally want things to stay the way they were, but great entrepreneurs see massive new businesses and go for it. We have to invest where the entrepreneurs are going." — Source: [Invest Like the Best]

- On The Infrastructure Layer: "Do not limit investments to consumer applications. Buy the underlying hardware and infrastructure that makes the new technological cycle possible." — Source: [BG2 Podcast]

- On Compounders: "The biggest mistake an investor makes is usually selling a true ten-bagger early, rather than holding it through its inevitable volatility." — Source: [Invest Like the Best]

- On Ignoring The Noise: "While day-to-day fluctuations matter for trading, the fund's ultimate success relies on focusing on the big ideas and multi-year structural shifts." — Source: [Bloomberg Wealth]

- On The Resilience Of Platforms: "Winners tend to keep winning in technology. Massive scale and research advantages mean that selling out of platform monopolies too early is a profound error." — Source: [Institutional Investor]

- On Tech Multiples: "A high price-to-earnings ratio is not inherently a warning sign. In technology, exponential growth and structural monopolies can fully justify what looks like a steep multiple." — Source: [Seeking Alpha]

Part 3: Portfolio Construction and Risk Management

- On Capital Deployment: "To manage volatility, invest one-third of your capital immediately, keep one-third in reserve for a 15 percent drop, and save the final third for a major 30 percent correction." — Source: [12mv2]

- On Surviving To Fight: "If we lose money at some point, we always raise cash. I always need to know I have got another day to fight." — Source: [Invest Like the Best]

- On Productive Paranoia: "A great investor must constantly wake up asking what could go wrong and prepare relentlessly for tail-risk events." — Source: [The Motley Fool]

- On Macroeconomic Forecasting: "I have always been wrong on macro. I think I have predicted seven of the last three recessions. Our edge is in individual companies, not timing the broader economy." — Source: [BG2 Podcast]

- On Data Velocity: "By processing over 100 million credit card receipts daily, we operate on a three-day view of consumer spending, giving us a speed advantage over official economic reports." — Source: [Bloomberg Wealth]

- On Respecting Cycles: "The 2022 tech drawdown taught us that you must respect interest rate environments and macroeconomic cycles, even when the underlying technology of the companies is revolutionary." — Source: [Institutional Investor]

- On Software Multiples: "Staying too aggressive for too long in high-multiple software stocks as interest rates rose was a critical error we had to learn from." — Source: [Institutional Investor]

- On Geographic Advantages: "The United States remains unparalleled for capital formation. An entrepreneur here can get a term sheet in weeks, whereas raising money in Europe is vastly more difficult." — Source: [Bloomberg Wealth]

- On Portfolio Concentration: "We build concentrated portfolios around the definitive winners of secular trends, accepting volatility in exchange for long-term compound growth." — Source: [Invest Like the Best]

- On Shifting Allocations: "When public market valuations become disconnected from reality, we dynamically shift our capital allocation toward venture and private growth." — Source: [All-In Podcast]

Part 4: The Art of Short Selling Tech

- On The Disproof Method: "It is mathematically much easier to disprove a company's success than to prove it. We short where the opposite of the bull case is easily demonstrable." — Source: [12mv2]

- On Structural Disruption: "The best short opportunities are legacy tech companies situated on the wrong side of a massive technological shift, actively being cannibalized by new platforms." — Source: [Institutional Investor]

- On Cyclical Overearners: "We look for companies that have overearned due to temporary macroeconomic tailwinds or supply chain bottlenecks, shorting them as conditions inevitably normalize." — Source: [Institutional Investor]

- On The Valuation Trap: "Shorting a tech stock simply because it looks expensive on a spreadsheet is incredibly dangerous; you need a fundamental breakdown in the business model as a catalyst." — Source: [Seeking Alpha]

- On Agility In Shorting: "If a short position moves against us because the fundamental thesis changes, we must be quick to cover or even flip the position to long." — Source: [Institutional Investor]

- On Sleepy Sectors: "Disruption extends beyond Silicon Valley software. We look for sleepy sectors like industrials or energy where incumbent complacency makes them prime targets for tech disruption." — Source: [Institutional Investor]

- On The Math Of Shorting: "The asymmetry of shorting means your maximum upside is 100 percent, but your downside is infinite. Position sizing and extreme discipline are mandatory." — Source: [Hedge Fund Alpha]

- On Long/Short Synergy: "Our deep fundamental research into the technological winners directly informs our conviction on which incumbents will be the definitive losers." — Source: [Kingswell]

- On Squeezes: "Maintaining sufficient liquidity and avoiding over-leverage on crowded shorts is the only way to survive inevitable market irrationality." — Source: [Hedge Fund Alpha]

Part 5: Macro Cycles and Market Mechanics

- On Tokens Versus Tariffs: "The productivity gains generated by artificial intelligence compute represent a more powerful long-term economic force than the negative frictions introduced by geopolitical tariffs." — Source: [All-In Podcast]

- On The US Debt Burden: "The current trajectory of US debt is a severe, under-acknowledged crisis that will force shifts in how infrastructure and growth are financed." — Source: [BG2 Podcast]

- On Bitcoin As An Asset Class: "Bitcoin's volatility is decreasing, and it is maturing into an institutional asset class comparable to digital gold, with room to double as adoption widens." — Source: [Bloomberg Wealth]

- On Institutional Adoption: "Retail investors were remarkably faster to understand and adopt digital assets than traditional financial institutions, who are only now opening the floodgates." — Source: [CNBC Squawk Box]

- On Stablecoins: "Stablecoins represent a foundational shift in the global financial infrastructure, providing a frictionless dollar-pegged settlement layer." — Source: [CNBC Squawk Box]

- On Market Leadership: "The composition of market leadership is constantly turning over; we suspect that search giants may struggle to remain in the top tier over the next five years." — Source: [CNBC Squawk Box]

- On The Risk Of Tax Flight: "Aggressive tax hikes on high earners in places like New York risk accelerating a structural migration of wealth and talent to low-tax states." — Source: [CNBC Squawk Box]

- On City Resilience: "Despite current political and economic friction, New York has historically demonstrated an incredible ability to reinvent itself and withstand generational shifts." — Source: [CNBC Squawk Box]

- On Interest Rate Realities: "When the consumer remains resilient and the broader economy holds up, the Federal Reserve lacks a compelling structural reason to aggressively cut rates." — Source: [Bloomberg Wealth]

Part 6: Venture Capital and the Life Cycle Approach

- On The Spectrum Of Investing: "To capture maximum value in modern technology, you have to be a life cycle investor crossing the boundaries between early venture, late-stage growth, and public markets." — Source: [Invest Like the Best]

- On Market Utility: "When the public market goes up and is highly receptive, I am definitively a public investor. But when it doesn't do well, I switch my focus to venture and growth." — Source: [Invest Like the Best]

- On The Private Resurgence: "The coming years represent a pivotal thawing of the IPO market and a resurgence for private equity and venture-backed companies that survived the previous downturn." — Source: [CNBC Squawk Box]

- On The Role Of Modern VC: "Traditional venture capital requires a steady ship that can continuously invest through boom and bust cycles without panicking." — Source: [All-In Podcast]

- On The Advantage Of Crossover Funds: "Our public market data and understanding of structural shifts give our venture arm a unique lens to identify which private startups are actually building sustainable public-scale businesses." — Source: [Invest Like the Best]

- On Founder Alignment: "Investing across the life cycle means we can partner with founders at the seed stage and remain their core capital partners all the way through their IPO and beyond." — Source: [Coatue]

- On The Illusion Of Private Stability: "Private market marks can create a false sense of security; eventually, every growth company must face the harsh, daily reality of public market valuation." — Source: [All-In Podcast]

- On Scaling Infrastructure: "The transition from a promising private startup to a public tech giant requires moving from product-market fit to relentless, scalable infrastructure and execution." — Source: [Coatue]

- On Margin Expansion: "We are entering an era where AI productivity tools will allow private and public companies alike to expand their margins without drastically increasing headcount." — Source: [BG2 Podcast]

Part 7: The AI Super Cycle and Future Infrastructure

- On The Historical Parallel: "After studying 400 years of market bubbles, we concluded that artificial intelligence is an early industrial revolution on par with electricity or the internet." — Source: [The VC Corner]

- On Measuring The Revolution: "The shift from the learning phase to the inference phase is evident in token throughput, with hyperscalers processing trillions of tokens per quarter." — Source: [All-In Podcast]

- On Replacing Architecture: "Over $100 trillion was historically invested in CPU-based infrastructure. Over the next decade, that will be systematically ripped out and replaced by GPU-based architecture." — Source: [Bloomberg Wealth]

- On Peeling The Onion: "To capitalize on the super cycle, you must look deeper and invest in the foundational bottlenecks: data centers, real estate, and power utilities." — Source: [Bloomberg Wealth]

- On The Fantastic 40: "The market by 2030 will be dominated by a new cohort of companies that leverage AI natively, disrupting the incumbents of the mobile era." — Source: [AI Supremacy]

- On The Threat To Search: "The advent of language models poses an existential, structural challenge to traditional search monopolies and ad-driven business models." — Source: [BG2 Podcast]

- On Energy Constraints: "The next growth engine is power generation. The electrical grids and industrial supply chains are the true limiters of scaling intelligence." — Source: [The VC Corner]

- On The Humanoid Frontier: "The new hardware frontier is embedding massive AI brains into physical bodies. Within twenty years, humans will work alongside humanoid robots." — Source: [Bloomberg Wealth]

- On Signal Versus Bubble: "High frequency of mentions about a technology is not always a sign of a bubble; it often signals a genuine shift in human behavior." — Source: [Bloomberg Wealth]

- On The Compute Shortage: "The allocation and availability of GPUs remain the definitive choke point of the tech economy, dictating which hyperscalers will win the cloud revenue wars." — Source: [BG2 Podcast]

Part 8: Leadership, Psychology, and Continuous Adaptation

- On The Necessity Of Humility: "To be a good investor, you have to be willing to change your mind constantly and possess the humility to admit when you have made a mistake." — Source: [BG2 Podcast]

- On Impatient Investing: "I am inherently impatient and I change my mind all the time. Counterintuitively, that mental flexibility is an asset in rapid-cycle tech investing." — Source: [BG2 Podcast]

- On Evolving Viewpoints: "My views on crypto completely shifted over time. Clinging to past assumptions when the data changes is lethal in this business." — Source: [BG2 Podcast]

- On Intellectual Honesty: "We foster an environment where the best argument wins, regardless of hierarchy. You must be willing to aggressively challenge your own highest-conviction ideas." — Source: [Invest Like the Best]

- On Handling Drawdowns: "When you suffer a massive drawdown, the psychological battle is harder than the financial one. You must reset to zero and analyze the board as it exists today." — Source: [Institutional Investor]

- On Avoiding The Echo Chamber: "The danger of being a successful firm is that people stop telling you that you are wrong. We actively cultivate dissenting opinions to break our own echo chambers." — Source: [Invest Like the Best]

- On The Pressure Of The Craft: "You do not get to rest on your laurels. Every morning, the market opens and demands that you prove your thesis all over again." — Source: [Bloomberg Wealth]

- On Learning From Failure: "The mistakes where we lost the most money—usually by misunderstanding macro cycles or overstaying our welcome in crowded trades—forged our current risk framework." — Source: [Institutional Investor]

- On The Ultimate Goal: "Our ambition is to actively fund and participate in the technological transformation of society, not just to generate returns." — Source: [Coatue]