Lessons from Pierre Andurand

Pierre Andurand runs Andurand Capital Management, where he makes massive, high-conviction bets on the energy and metals markets. He targets structural supply imbalances to find asymmetric returns, navigating extreme volatility to position for the messy global shift toward decarbonization.

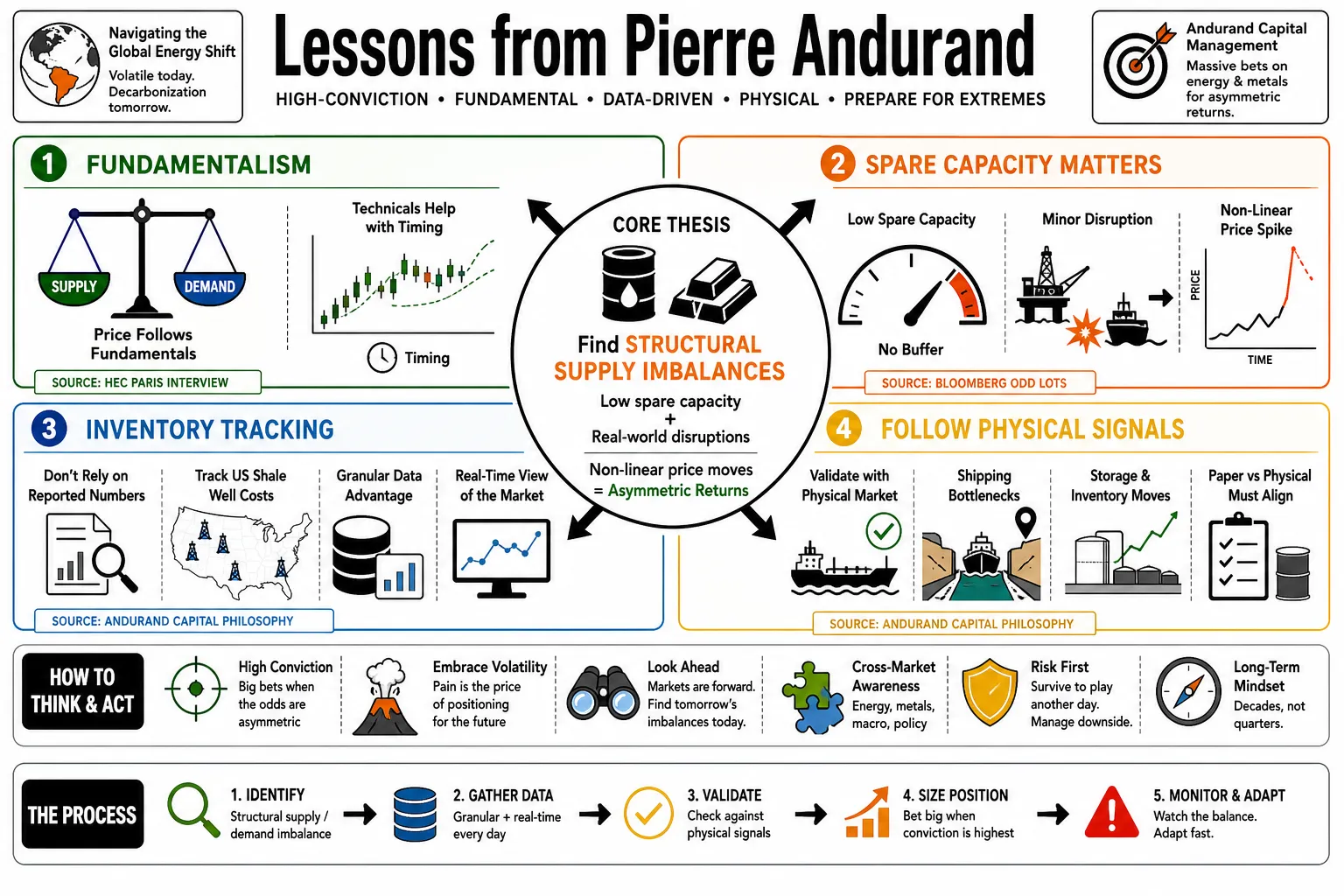

Part 1: Oil Market Mechanics and Supply Dynamics

- On Fundamentalism: "I am a fundamentalist. While technicals can assist with timing, it is the underlying balance of supply and demand that ultimately dictates the price of any commodity." — Source: HEC Paris Interview

- On Spare Capacity: "The oil market is extremely vulnerable when spare capacity is low. If you don't have a buffer, any minor disruption can lead to a non-linear price spike that the market cannot easily absorb." — Source: Bloomberg Odd Lots

- On Inventory Tracking: "Successful trading requires granular data. We don't just look at reported numbers; we track individual well costs in the US shale patch and monitor physical shipping bottlenecks in real-time." — Source: Andurand Capital Philosophy

- On Physical Signals: "Always validate your paper trades with physical market signals. If the futures are rallying but the physical premiums are falling, the rally is likely driven by sentiment rather than reality." — Source: The Hedge Fund Journal

- On Backwardation: "Extreme backwardation is a clear sign of a physical shortage. It tells you that the market is desperate for barrels today and is willing to pay a massive premium over future delivery." — Source: Bloomberg TV

- On US Shale Resilience: "One of the greatest mistakes in recent years was underestimating the efficiency of US shale producers. They can now grow production at much lower prices than the market previously thought possible." — Source: Financial Times

- On OPEC+ Strategy: "OPEC+ acts as a micromanager of the global oil market. They aim to floor prices, but their ability to do so depends entirely on their willingness to sacrifice market share." — Source: Reuters

- On "Shadow" Supply: "Geopolitical assumptions are dangerous. We learned that the lack of sanction enforcement on certain nations can lead to a surge in 'shadow' supply that offsets official production cuts." — Source: Hedgeweek

- On Refining Bottlenecks: "It’s not just about the crude; it’s about the products. A shortage of refining capacity can lead to a disconnect where gasoline and diesel prices skyrocket even if crude prices remain stable." — Source: Bloomberg Odd Lots

Part 2: The Energy Transition and "Green Metals"

- On Copper as the New Oil: "Copper is now a more compelling structural trade than oil. While oil demand will eventually peak, the energy transition and AI data centers are creating a 'jaws opening' between supply and demand for copper." — Source: Bloomberg News

- On Electrification Demand: "The amount of copper needed for the global electric grid is staggering. We are moving from a market of 500,000 tons of growth per year to 1 million tons, with no new mining supply to match it." — Source: Top Traders Unplugged

- On Copper Price Targets: "Copper could reach $15,000 per ton in the short term and potentially $40,000 per ton within five years. The price must rise high enough to force a demand response or justify massive new investment." — Source: The Hedge Fund Journal

- On Mining Lead Times: "You cannot just turn on a copper mine. It takes 10 to 15 years from discovery to production. This creates a multi-year structural deficit that is almost impossible to bridge quickly." — Source: Bloomberg Odd Lots

- On Lithium Oversupply: "I am bullish on lithium long-term, but bearish in the short-term through 2027. Temporary oversupply means the price needs to stay depressed until the next wave of EV demand catches up." — Source: Andurand Capital Investor Letter

- On Nickel and Aluminum: "Industrial metals like nickel and aluminum are the backbone of the energy transition. They will be the primary beneficiaries as the world shifts away from fossil fuel infrastructure." — Source: Forbes

- On Decarbonization Costs: "Decarbonizing the global economy will be incredibly expensive and commodity-intensive. Investors who ignore the materials required for this transition are missing the largest macro story of the decade." — Source: HEC Paris

- On the Substitution Effect: "People assume high prices will lead to substitution, but in many green technologies, there is no viable substitute for copper’s conductivity or nickel’s energy density." — Source: Bloomberg TV

- On Portfolio Rotation: "Oil does not always have to be the larger risk in the portfolio. There are periods where the risk-reward for 'green metals' is significantly more attractive than for hydrocarbons." — Source: The Hedge Fund Journal

- On the End of the Internal Combustion Engine: "The transition to EVs is not a trend; it is a structural shift. Once the cost of ownership for an EV drops below a certain point, the demand for oil in passenger transport will collapse." — Source: Reuters

Part 3: Trading Strategy and Asymmetric Returns

- On Asymmetric Upside: "My core philosophy is seeking trades where I can risk 1 to make 10, 20, or even 40. I am not interested in 'picking up pennies' with limited upside." — Source: HEC Paris Interview

- On Buying Volatility: "I prefer buying options over selling them. This strategy limits my downside to the premium paid while giving me uncapped exposure to a major market move." — Source: Top Traders Unplugged

- On Convexity: "Look for convex payoffs. You want to be positioned so that if you are right about a fundamental shift, the value of your position increases exponentially rather than linearly." — Source: Andurand Capital

- On High Conviction: "When you have a strong fundamental view supported by data, you must have the courage to take a large position. Diversification is often just a hedge against lack of knowledge." — Source: Financial Times

- On Market Timing: "The 'why' matters for the trade, but the 'when' matters for the profit. Even a perfect fundamental view can lose money if you are too early and the market moves against you first." — Source: Bloomberg Odd Lots

- On Respecting Price Action: "Even when my models say the price should be higher, I remain respectful of the market. If a trade pulls back 30% for no obvious reason, I will often cut it to protect capital." — Source: eFinancialCareers

- On the Dangers of Selling Options: "Selling options is a 'rent-collecting' strategy that eventually ends in catastrophe. You are effectively betting that the world will stay stable, which is a poor bet in commodities." — Source: HEC Paris

- On Structural Deficits: "Markets are slow to price in structural changes. Most participants are focused on the next month, which allows those with a 5-year view to find significant mispricings." — Source: The Hedge Fund Journal

- On Liquidity Calibration: "Calibrate your position size based on market liquidity. A high-conviction bet in a thin market like cocoa requires much smaller relative sizing than a bet in Brent crude." — Source: Bloomberg Odd Lots

- On Absolute Returns: "Our goal is not to beat a benchmark; it is to generate absolute returns in all environments. This requires the flexibility to be long, short, or out of the market entirely." — Source: Andurand Capital

Part 4: Risk Management and Market Psychology

- On Survival: "The first rule of trading is to live to fight another day. No matter how sure you are of a trade, you must never size it so large that a 50% move against you wipes you out." — Source: eFinancialCareers

- On Cutting Losses: "Discipline in cutting losses is the only way to survive the overconfidence that follows a winning streak. You must be able to admit you were wrong before the market forces you to." — Source: Forbes

- On Taking Breaks: "If the fund hits a specific drawdown trigger—say 15%—I take a two-week break from trading. This ensures my next decisions are data-driven rather than an emotional attempt to 'win it back'." — Source: Andurand Capital Investor Letter

- On the Risk Ladder: "We use a 'risk ladder' where exposure is automatically reduced at tiered drawdown levels. This prevents a bad trade from turning into a fund-ending event." — Source: The Hedge Fund Journal

- On Managing Ego: "Your ego is your greatest enemy in trading. You must be willing to be wrong in public and pivot your strategy immediately when the facts change." — Source: Hedgeweek

- On Optimism: "To be a successful risk-taker, you must have an optimistic outlook. You need the confidence to believe that you can navigate the uncertainty and come out ahead." — Source: HEC Paris Interview

- On Post-Success Slumps: "The most dangerous time for a trader is immediately after a major success. Success breeds sloppiness, and sloppiness leads to catastrophic risk management." — Source: eFinancialCareers

- On Emotional Detachment: "Market movements are not personal. To survive decades in this business, you must detach your self-worth from your P&L." — Source: Top Traders Unplugged

- On Liquidity Traps: "The market often becomes 'broken' due to a lack of liquidity. In these moments, prices can move $10 on no news, and your priority must shift from profit to preservation." — Source: Bloomberg News

- On High Conviction Drawdowns: "High conviction is a double-edged sword. It leads to triple-digit gains, but it also means you will face extreme drawdowns that require iron nerves to navigate." — Source: Financial Times

Part 5: Geopolitics and Global Energy Security

- On Supply Shocks: "Non-linear price spikes are almost always triggered by geopolitical supply shocks. When inventories are already low, the market has no way to cushion the blow." — Source: Bloomberg TV

- On Russia and Europe: "Europe’s survival during the gas crisis showed that markets are more resilient than predicted. Demand destruction and fuel switching can happen quickly when prices are high enough." — Source: Bloomberg Odd Lots

- On Sanction Enforcement: "Sanctions are only as effective as their enforcement. If the US allows 'shadow' exports to increase to keep prices low domestically, the impact of the sanctions is neutralized." — Source: Hedgeweek

- On the Middle East Risk Premium: "The market often discounts geopolitical risk until there is actual physical evidence of barrels leaving the system. Betting on 'fear' alone is no longer a reliable strategy." — Source: Reuters

- On China’s Demand Catalyst: "China’s reopening remains the single largest wild card for global energy demand. Even a modest recovery can add millions of barrels per day back into a tight market." — Source: Bloomberg Odd Lots

- On Energy Independence: "The transition to renewables is a matter of national security, not just climate. Moving to a copper-based economy reduces reliance on volatile oil-producing regions." — Source: HEC Paris

- On Israeli Strikes on Iran: "A major strike on Iranian oil infrastructure would be a 'regime change' event for oil prices. The market is often complacent about this tail risk." — Source: Bloomberg News

- On the Role of Speculators: "Speculators provide the liquidity that allows producers to hedge. Without us, price discovery would be even more chaotic and energy security would suffer." — Source: Bloomberg Odd Lots

- On Strategic Petroleum Reserves: "Using the SPR for price management rather than emergency supply is a dangerous game. It leaves the world vulnerable to a real disruption later on." — Source: Financial Times

Part 6: Carbon Markets and Climate Change Economics

- On Punitive Carbon Pricing: "The price to put carbon in the atmosphere should be really punitive. It must be high enough to force industrial change rather than just being a cost of doing business." — Source: Forbes

- On Carbon as an Asset Class: "Carbon credits (EUAs) are a structural long. As regulations tighten, the supply of allowances will decrease, forcing prices higher over the next decade." — Source: Andurand Capital research

- On Policy-Driven Scarcity: "Unlike oil, where supply is geological, carbon allowance supply is political. This makes it a unique asset class that is less correlated with traditional macro factors." — Source: The Hedge Fund Journal

- On Climate Change vs. COVID: "For COVID, there is a vaccine. For climate change, it gets worse every year, and then you get stuck. There is no quick fix once the tipping points are reached." — Source: Forbes

- On Green Inflation: "The transition to a green economy is inflationary by nature. We are replacing cheap, established energy systems with expensive new ones that require massive amounts of raw materials." — Source: HEC Paris Interview

- On Stranded Assets: "Investors must be wary of 'stranded assets' in the oil sector. Any project with a 20-year payback period is at extreme risk as demand peaks and declines." — Source: Reuters

- On the Cost of Polluting: "If it’s cheap to pollute, no one will innovate. High carbon prices are the most effective tool we have to drive technological breakthroughs." — Source: Bloomberg TV

- On Methane Leakage: "Methane is the 'low hanging fruit' of climate action. Tracking and stopping methane leaks in oil infrastructure is the fastest way to reduce the sector’s footprint." — Source: Andurand Capital

- On the Responsibility of Traders: "Commodity traders have a front-row seat to the energy transition. We have a responsibility to direct capital toward the materials that will enable a low-carbon future." — Source: HEC Paris

Part 7: Lessons from Volatility and Drawdowns

- On the "Long and Wrong" Trade: "Admitting I was 'long and wrong' in 2023 was essential. You cannot trade effectively if you are more committed to your ego than to the reality of the price action." — Source: Hedgeweek

- On Negative Oil Prices: "Predicting negative oil prices in 2020 was a lesson in physical constraints. When storage is full, the price of an asset is not zero; it is whatever it costs to make it go away." — Source: Bloomberg Odd Lots

- On High Conviction Perils: "The same high conviction that delivered 154% in 2020 led to a 55% loss in 2023. You must accept that outsized returns come with the price of outsized volatility." — Source: Financial Times

- On Underestimating Shale: "In 2023, I underestimated how much oil US producers could bring to market despite low rig counts. Efficiency gains are harder to model than rig counts." — Source: Bloomberg News

- On Market Noise: "The daily news cycle is mostly noise. To find real edge, you must step back and think about where the market will be in 3 to 5 years." — Source: eFinancialCareers

- On the "Broken" Market Lesson: "Liquidity is the oxygen of the market. When it dries up, fundamental analysis becomes a secondary factor to the technicals of margin calls and forced selling." — Source: Bloomberg Odd Lots

- On Adapting to Change: "I started as an oil trader, but in 2024 I made more money in cocoa and copper. A trader must be a generalist who follows the structural stories, not just a single asset." — Source: Bloomberg News

- On Positioning vs. Fundamentals: "Even with perfect fundamentals, you can lose money if everyone is already positioned for the same outcome. Always check the 'crowdedness' of a trade." — Source: Top Traders Unplugged

- On Managing Investors: "Transparent communication during drawdowns is vital. Investors in high-conviction funds must understand that volatility is the feature, not the bug." — Source: Andurand Capital Investor Relations

Part 8: Soft Commodities and the Future of Energy

- On the Cocoa Deficit: "The surge in cocoa prices was a classic structural story. Years of underinvestment and climate-related crop failures created a deficit that could only be balanced by record prices." — Source: Bloomberg Odd Lots

- On Climate Impacts on Agriculture: "Climate change is making agriculture as volatile as energy. We are seeing more 'biblical' crop failures that disrupt global supply chains." — Source: HEC Paris

- On Nominal vs. Real Prices: "Never say a price is 'too high' just because it is an all-time high in nominal terms. You must ask what price is needed to destroy demand." — Source: Bloomberg Odd Lots

- On Peak Oil Demand (2027-2030): "Oil demand will likely peak before 2030. We are already seeing the plateau in many regions as electrification accelerates." — Source: Reuters

- On the AI Energy Surge: "AI data centers are the newest driver of commodity demand. The amount of electricity—and therefore copper and gas—needed to power these centers is being underestimated." — Source: Bloomberg News

- On the Underinvestment Supercycle: "We are in a commodities supercycle driven by a decade of underinvestment in 'old economy' assets like mines and refineries." — Source: The Hedge Fund Journal

- On the Future of Hedge Funds: "The future belongs to discretionary managers who can synthesize massive amounts of data with human judgment. Algorithms struggle with the non-linear shifts in geopolitical risk." — Source: eFinancialCareers

- On Global Connectivity: "Commodities are the ultimate global asset class. A drought in West Africa or a strike in an Australian mine has immediate consequences for an investor in London." — Source: HEC Paris Interview

- On Constant Learning: "The day you think you have mastered the market is the day you begin to lose. Every cycle teaches you something new about human behavior and physical constraints." — Source: Top Traders Unplugged