Lessons from Prem Watsa

Prem Watsa founded Fairfax Financial in 1985 to explicitly replicate the Berkshire Hathaway model, using property and casualty insurance float to fund long-term investments. While often called the "Canadian Warren Buffett," Watsa distinguishes himself through strict downside protection and a habit of making massive contrarian bets when markets panic. These notes outline his mechanics for generating float, surviving financial cycles, and allocating capital across a decentralized business.

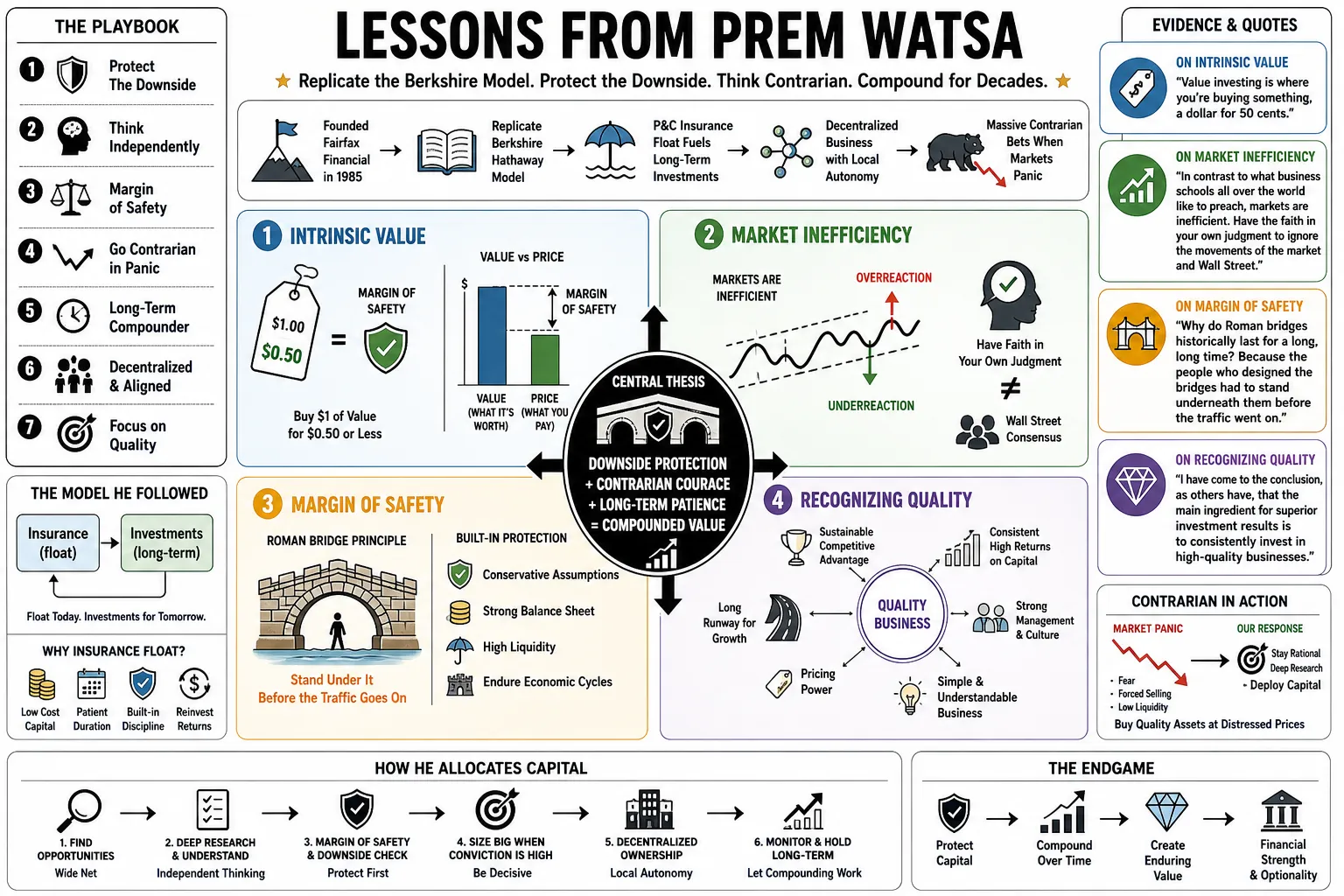

Part 1: Value Investing and Margin of Safety

- On Intrinsic Value: "Value investing is where you're buying something, a dollar for 50 cents." — Source: Amazon AWS Transcript

- On Market Inefficiency: "In contrast to what business schools all over the world like to preach, markets are inefficient. Have the faith in your own judgment to ignore the movements of the market and Wall Street." — Source: Motley Fool

- On Margin of Safety: "Why do Roman bridges historically last for a long, long time? Because the people who designed the bridges had to stand underneath them before the traffic went on." — Source: Motley Fool

- On Recognizing Quality: "I have come to the conclusion, as others have, that in general you find better investments in businesses with good economics, secular tailwinds, and sustainable competitive advantages than you do in trying to get one last puff out of proverbial cigar butts." — Source: Economic Times

- On The Graham Influence: "The first big lesson from Graham was that reason and rationality were a great winning combination... it really just tipped the odds in my favor." — Source: Graham and Doddsville

- On Speculation: "An investment operation is one which, upon thorough analysis, promises safety of principal and an adequate return. Operations not meeting these requirements are speculative." — Source: Traders Union

- On True Independence: "Don't ever think that the market knows more than you do about the underlying business. That's the biggest mistake you can make." — Source: Quotes Wise

- On Pricing Power: "High-quality, Buffett-favoured value stocks, which have competitive advantages and can pass on cost increases to customers, are likely to do well." — Source: Scribd Transcript

- On Profit Uncertainty: "To be clear, we expect to make significant profits from our common stock positions – but we don't know when!" — Source: Fairfax 2023 Shareholder Letter

- On Doing the Work: "You have to do your own homework. Have the faith in your own judgment to ignore the movements of the market." — Source: Motley Fool

Part 2: Macroeconomics and Risk Management

- On Preparation: "Predicting rain doesn't count, but building an ark does." — Source: Motley Fool

- On Market Euphoria: "A bubble is inflated by nothing firmer than expectations. The moment people cease to believe that house prices will rise forever... the market will crash." — Source: GuruFocus

- On Deflationary Environments: "If the 2008–2009 recession was like any other recession that the U.S. has experienced in the past 50 years, we would not be hedging today." — Source: GuruFocus

- On Derivatives Volatility: "The credit default swaps are extremely volatile... their ultimate value will therefore only be known upon their disposition." — Source: GuruFocus

- On Admitting Mistakes: "Shorting is dangerous, very short term in nature and anathema to long term value investing. Your Chairman continues to learn – slowly!" — Source: Hedge Fund Alpha

- On Big Tech Valuations: For the largest technology companies to maintain their historical growth rates, they would have to add the equivalent of a new Fortune 500 company annually, a pace that is mathematically unsustainable. — Source: YouTube Interview

- On Defensive Positioning: "Buy defensive assets and cash-flowing businesses when everyone else is chasing growth." — Source: YouTube Interview

- On Rising Interest Rates: "Higher interest rates are boosting Fairfax... the volatility from bond gains or losses going forward will be cushioned by the discounting of our insurance liabilities." — Source: Fairfax Shareholder Letters

- On Inflation vs Growth: "Inflation and higher interest rates are small factors compared to the economic growth taking place." — Source: Economic Times

Part 3: Insurance, Float and Capital Allocation

- On the Concept of Float: "The big strength we have in insurance is the float that it generates." — Source: Fairfax Shareholder Letters

- On the Advantage of Float: "Insurance float was a form of low-cost, long-term capital, superior to loans or equity funding." — Source: Newsgram

- On the Goal of Underwriting: "Our long-term aim is actually no-cost float." — Source: YouTube Interview

- On Decentralized Operations: "Our success throughout our history... has come under a decentralized structure with outstanding management executing a disciplined approach to underwriting." — Source: Fairfax Shareholder Letters

- On Management Retention: "If you trust people they stick around... our presidents and senior execs average close to 20 years with the company. That’s a massive advantage." — Source: YouTube Interview

- On Quiet Execution: "We put our heads down and worked hard and have gotten results. Once in a while we will talk if we have anything to say." — Source: Motley Fool

- On The Holding Company Model: Fairfax operates as a pure holding company where insurance subsidiaries manage their own daily underwriting, leaving the central team completely focused on capital allocation. — Source: Substack

- On Emerging Insurance Markets: "In India only 5% of homeowners have insurance, so there's a huge runway." — Source: Stockchase

- On Consistency: "Over these past 13 years we have written close to $200 billion of gross premium and produced cumulative underwriting profits... with reserve redundancies each and every year." — Source: GuruFocus

Part 4: Business Principles and The Golden Rule

- On The Golden Rule: "Treat people the way you want to be treated. That is the golden rule underlining Fairfax's path to success." — Source: CCMM

- On Doing the Right Thing: "Integrity is doing the right thing even when it is painful." — Source: UWO

- On Taking Advantage: "It is never a good idea to take advantage of someone who has their back pushed against a wall... Never compromise your integrity." — Source: CCMM

- On Assessing Leadership: "We focus on the leader of the target organization because... the leader sets the culture of the organization." — Source: UWO

- On Evaluating Acquisitions: "We look for good businesses, with good, ethical and honest leadership... leadership that does not want to sell and retire, but wants to build." — Source: Hedge Fund Alpha

- On Building Trust: "Our reputation for a decentralized management-friendly approach enables us to attract partners that are like-minded who share our long-term approach to value creation." — Source: Fairfax India

- On Corporate Egos: "One must be very fearful of individuals with large egos who demonstrate arrogance in the workplace." — Source: CCMM

- On Teamwork: "Anything in the world is possible if you don't pay attention to who gets the credit at the end of the day." — Source: Invest Wizardry

- On Giving Back: "You must do well to do good." — Source: Fairfax Shareholder Letters

- On Retaining Founders: "We will acquire companies with good management already in place." — Source: Scribd

Part 5: Patience and Long-Term Compounding

- On "Hold Forever": Fairfax's core operating assumption when acquiring a business is that they will hold it forever, providing a permanent home for founders. — Source: Economic Times

- On Volatile Returns: "Our earnings are lumpy. We have never had guidance in 23 years because we have ups and downs and take the long-term view." — Source: Motley Fool

- On Quarterly Thinking: "All business affairs must be thought out on a long-term basis and rash decisions must be avoided at all costs. Fairfax does not forecast on the short term." — Source: Fairfax Shareholder Letters

- On Building for Generations: "We're stewards, not owners in the sense that... we want to build this company for the next hundred years." — Source: YouTube Interview

- On Avoiding the Quick Exit: The corporate name "Fairfax" stands for "Fair, Friendly Acquisitions," serving as a public declaration that they are not a traditional private equity firm seeking a fast exit. — Source: CCMM

- On Enduring the Noise: "The long history of the stock market shows that value investing pays off. You have to be patient." — Source: Amazon AWS Transcript

- On Shareholder Alignment: "Since its inception, Fairfax has been focused on the long-term view rather than short-term earnings to the benefit of all shareholders." — Source: Economic Times

- On Avoiding Unnecessary Sales: "There is no offer that is too good to refuse. Shareholders know that the company can't be sold and employees know they can build long-term and stable careers." — Source: CCMM

- On Geographic Commitment: "My focus is on putting everything back into India. We've got $7 billion in India and we expect to have another $7 billion over time." — Source: India Times

Part 6: Contrarianism and Market Psychology

- On The Courage to Zig: Value investing relies entirely on courage; you must have the stomach to heavily commit capital when the rest of the market is running the other way. — Source: Substack

- On Market Exuberance: "When the music stops, it stops very quickly." — Source: Motley Fool

- On Reversions to the Mean: "Trees don't grow to the sky, and markets don't fall to the floor." — Source: Motley Fool

- On Following the Crowd: "Buy when you hear the sound of cannons. Sell when you hear the sound of trumpets." — Source: Quotes Wise

- On Systemic Disconnects: "There continues to be a big disconnect between the financial markets and the underlying economic fundamentals." — Source: Hedge Fund Alpha

- On Pessimism: Investors routinely fail to recognize that the safest entry point for any asset is the precise moment when public sentiment is at absolute maximum pessimism. — Source: Hedge Fund Alpha

- On Independent Conviction: "The best opportunities are often found where others aren't looking." — Source: Policy Magazine

- On Ignoring the Media: Once a thesis is built entirely on underlying fundamentals, checking the daily financial news is an active detriment to executing the trade. — Source: Motley Fool

- On Economic Disasters: "Ben Graham made the point that only 1 in 100 of the investors who were invested in the stock market in 1925 survived the crash of 1929–1932." — Source: Traders Union

Part 7: Books, Mentors and Influences

- On "Security Analysis": Watsa considers Graham and Dodd's text the primary manual of value investing, specifically citing it as his introduction to the concept of margin of safety. — Source: Value Investing Education

- On Modern Valuation: Watsa refers to George Athanassakos's book, Value Investing: From Theory to Practice, as an essential modern update to Graham's original texts. — Source: UWO

- On "There's Always Something to Do": Watsa wrote the foreword for this biography of Peter Cundill, repeatedly praising Cundill's unyielding discipline in hunting deep value assets. — Source: Talkative Man

- On Qualitative Assessment: Philip Fisher's Common Stocks and Uncommon Profits heavily influenced Watsa's framework for evaluating management competence instead of just balance sheets. — Source: Talkative Man

- On "The Great Depression: A Diary": Watsa recommended Benjamin Roth's book to his shareholders to demonstrate the psychological toll of a deflationary environment. — Source: Value Investing Education

- On John Templeton: "I met with him, beginning in 1978, every year... Like him, I take the long-term view, buy the best and short the worst." — Source: Hedge Fund Alpha

- On The Right Mindset: "What the mind can conceive and believe, it can achieve." — Source: Policy Magazine

- On His First Boss: Watsa credits his former superior at Confederation Life, John Watson, for handing him a copy of Security Analysis and fundamentally altering his career trajectory in 1974. — Source: Graham and Doddsville

- On Intellectual Homage: Watsa named his son Ben in honor of Benjamin Graham, marking the profound personal impact the author had on his worldview. — Source: Outlook India

Part 8: Life Lessons, Failure and Resilience

- On Family First: "Life is sometimes difficult and family must always come first. This is a non-negotiable point." — Source: CCMM

- On Work and Faith: "Work as hard as you can, as though everything depends on you. Pray as hard as you can, as though everything depends on God." — Source: The Canadian Encyclopedia

- On Learning from Failure: "It is all right to fail but we should learn from our mistakes." — Source: CCMM

- On Keeping Perspective: Watsa uses the biblical warning, "What profiteth a man if he gains the whole world, but loses his soul?" to remind his executives that wealth without ethics is meaningless. — Source: Geny Money

- On Immigrant Hustle: "As long as you are willing to work hard and do something about which you are passionate, then there is unlimited opportunity." — Source: Economic Times

- On Fun at Work: "We believe in having fun – at work!" — Source: Invest Wizardry

- On India's Future: "We think India will be the single best place to put money in the future." — Source: Swarajya Mag

- On Economic Freedom: "What we never had in India was economic freedom. But now with the startup nation, that's flying. It doesn't make a difference what your background is." — Source: Economic Times

- On Real Wealth: True success is modeled on figures like John Templeton, who accumulated massive wealth but chose to live frugally while executing large-scale philanthropy. — Source: Policy Magazine

- On Enduring Value: The ultimate purpose of a corporation is not to generate fast trading gains, but to create real value for society and build an institution that outlives its founder. — Source: UWO