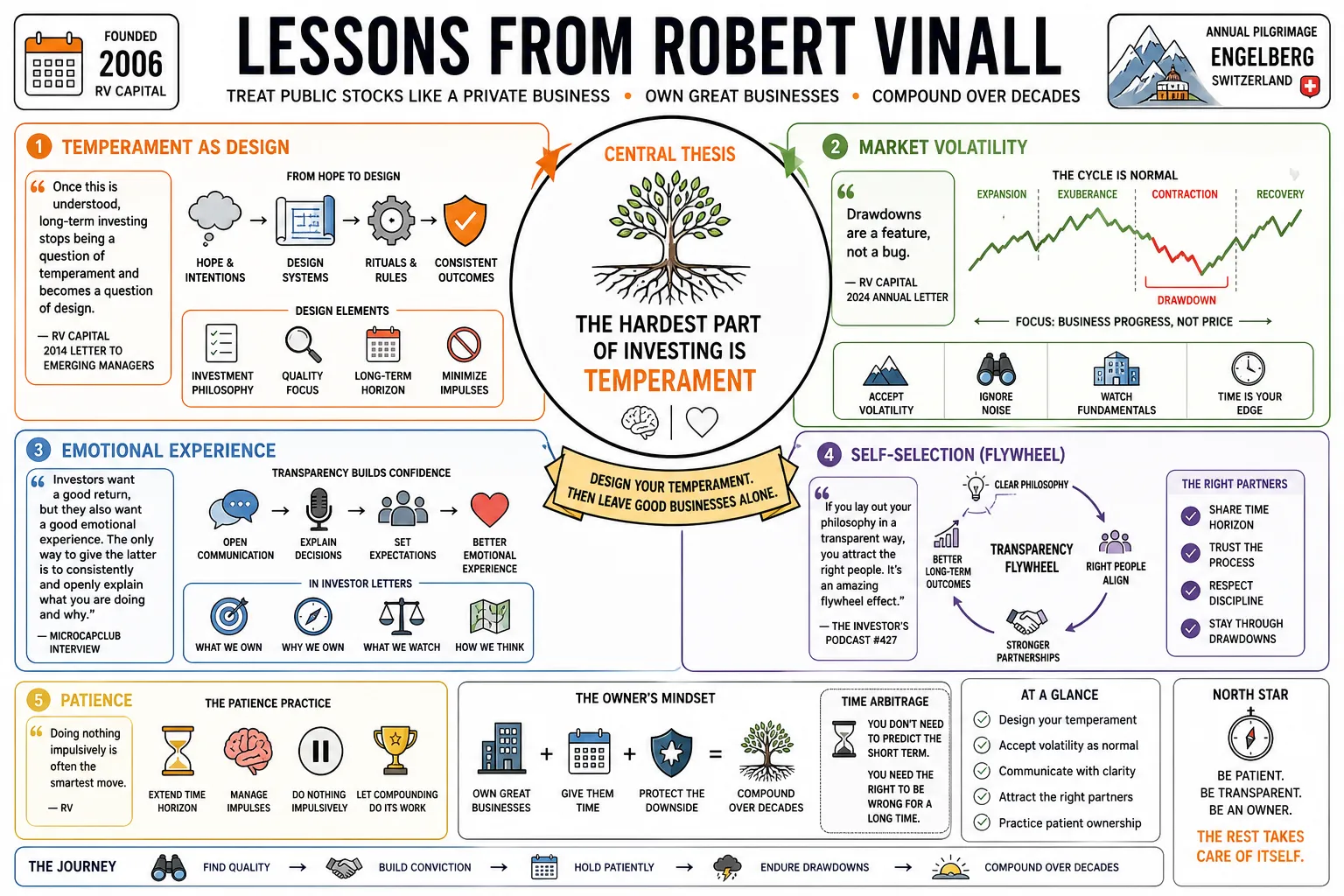

Lessons from Robert Vinall

Robert Vinall launched RV Capital in 2006 to treat public stocks with the same multi-decade patience as a private business owner. Between his transparent investor letters and his annual pilgrimage to Engelberg, Switzerland, he has shown that the hardest part of investing isn't the math, but the temperament required to leave a good company alone.

Part 1: Psychology & Temperament

- On Temperament as Design: "Once this is understood, long-term investing stops being a question of temperament and becomes a question of design." — Source: RV Capital 2014 Letter to Emerging Managers

- On Market Volatility: "Drawdowns are a feature, not a bug." — Source: RV Capital 2024 Annual Letter

- On Emotional Experience: "Investors want a good return, but they also want a good emotional experience. The only way to give the latter is to consistently and openly explain what you are doing and why." — Source: MicroCapClub Interview

- On Self-Selection: "If you lay out your philosophy in a transparent way, you attract the right people. It's an amazing flywheel effect." — Source: The Investor's Podcast #427

- On Patience: "Doing nothing impulsively is often the smartest move." — Source: RV Capital 2018 Annual Letter

- On Conviction: "Sometimes you can win just because you believe in something and don’t give up." — Source: RV Capital 2021 Annual Letter on Carvana

- On the News Cycle: "The news is, by definition, always new. The risk in focusing excessively on what is new is missing gradual changes that are permanent." — Source: Hedge Fund Alpha Interview

- On Emotional Intelligence: "Culture provides a kind of operating manual for employees of what they should do when it’s not clear what they should do." — Source: Good Investing Interview

- On Trust: "The hardest part isn't finding the right investments, it's finding the right investors." — Source: RV Capital 2022 Half-Year Letter

- On Skin in the Game: "It's fairly obvious and intuitive that you want to avoid mistakes and get better when it's your own money." — Source: Art of Value Podcast

Part 2: Business Quality & The Widening Moat

- On Moat Trajectory: "Yes, moat width is important, but it is not the most important thing. A business is always evolving, and investors should focus on whether the moat is widening or not." — Source: RV Capital Presentation at the University of Zurich

- On the Rowing Analogy: "If one rower is miles behind the other but going fractionally faster, in a long period of time, he's going to catch up. I look for the widening moat." — Source: Stock Unlock Interview

- On Execution: "Execution is absolutely important to maintain and expand the moat. In fact, moats often come about because of great execution rather than an inherent advantage." — Source: RV Capital 2014 Letter

- On Complacency: "In a dynamic, rapidly changing economy, having a wide moat can sometimes be a disadvantage because it breeds complacency." — Source: ValueSider Analysis

- On Quality Metrics: "To check if a moat is widening, you can look at quantitative metrics like ROIC, but also qualitative elements like innovation and customer experience." — Source: RV Capital 2023 Presentation

- On Feedback Loops: "Competitive advantage increases over time as a rule when there are positive feedback loops." — Source: RV Capital 2011 Annual Letter

- On Shared Value: "I look for companies where the customer gets a better deal as the company gets larger." — Source: RV Capital 2020 Annual Letter

- On Amazon's Moat: "Take Amazon: its success isn't only due to its huge scale, but due to the relentless attention to execution—innovating with faster delivery times." — Source: Business Owner Fund TGV Letters

- On Intangible Assets: "The best moats are often cultural and intangible rather than just scale or patents." — Source: RV Capital 2024 Presentation in London

- On Business Durability: "The first question I ask is: Will the company be around and flourishing in 10 or 20 years?" — Source: Investing City Podcast #56

Part 3: Management & Culture

- On Management's Role: "Management is not secondary to the presence of a moat... it can have a positive or negative impact on a company's moat." — Source: RV Capital 2014 Letter

- On the Founder's Mentality: "Culture ultimately comes from the values and the personality of the founder." — Source: Good Investing Podcast

- On Life's Work: "I always look to invest in a manager who has made the company his or her life’s work." — Source: RV Capital 2012 Annual Letter

- On Love for Business: "Love is not a word that you often find being used in financial circles, but that's actually what you're really looking for in a manager." — Source: MicroCapClub 2014 Interview

- On CEO Likability: "One of the most important qualities of a CEO is they have to be likable. If you’re charging out of the trenches, people have to like you to follow you." — Source: RV Capital 2021 Annual Gathering Video

- On Setting the Example: "Does the management set the right example in terms of frugality, work ethic, and ethics?" — Source: RV Capital 2009 Annual Letter

- On Promoters: "I avoid managers who spend more time marketing the stock than running the business." — Source: RV Capital 2014 Letter to Emerging Managers

- On Mosaic Theory in Culture: "When you are trying to assess a culture, talk to people who have left on good terms... What you are doing is building a mosaic." — Source: The Art of Value Interview

- On Rationality: "I look for an engaged and rational owner. Rationality is rarer than brilliance." — Source: RV Capital 2016 Annual Letter

- On Capital Allocation: "Management’s primary job is to protect and grow the earning power of the business over very long periods of time." — Source: RV Capital 2013 Annual Letter

Part 4: Valuation & Capital Allocation

- On the Cheapskate Trap: "One of my big mistakes is passing on a number of great businesses because they looked optically overpriced." — Source: Mohnish Pabrai's 'Chai with Pabrai'

- On Optical vs. Real Expense: "In the end, it turned out they were not overpriced, but when you looked at them, they looked expensive." — Source: RV Capital 2014 Letter

- On Growth Math: "If I assume a business grows by 25%, all things being equal, that stock will be worth another 25% because its earnings power went up." — Source: RV Capital 2022 Half-Year Letter

- On Paying Up: "Buying great businesses at 80 times earnings typically is not going to be a great way to get rich." — Source: The Investor's Podcast Episode #427

- On Five-Year DCFs: "I chose a five-year DCF on Wix because there was no need to go any further in the future to justify the price I paid." — Source: RV Capital 2022 Annual Gathering Transcript

- On Capital-Light Compounders: "Wix is about as good a company as you can imagine... it is capital-light and operates with negative working capital." — Source: RV Capital 2024 Annual Letter

- On Reinvestment Runway: "The truly great investments are in companies that can grow by reinvesting their cash flow as Wix is doing." — Source: RV Capital 2022 Annual Letter

- On Dividend Skepticism: "I prefer companies that have the opportunity to reinvest their earnings at high rates rather than paying them out as dividends." — Source: RV Capital 2010 Annual Letter

- On Cash Buffers: "I avoid debt and seek to avoid it at the companies I invest in. Leverage is the enemy of patience." — Source: RV Capital 2022 Half-Year Letter

Part 5: Portfolio Strategy & Concentration

- On Munger's Diversification: "Charlie Munger explained that one needs a mere two stocks to have proper diversification. Two stocks." — Source: RV Capital Blog Post - Dinner with Charlie

- On Concentration: "The 'Business Owner' fund typically holds around 10 to 12 investments. We want our best ideas to move the needle." — Source: RV Capital 2024 Presentation

- On the 'Big Five': "We group our portfolio into our highest-conviction holdings where the business model is largely proven." — Source: RV Capital 2021 Annual Letter

- On Holding Periods: "I think in terms of decades, not years. My goal is for our turnover to be as close to zero as possible." — Source: RV Capital 2013 Annual Letter

- On Selling Framework: "I only sell if the fundamental hypothesis changes or if there is a massive deterioration in management quality." — Source: RV Capital 2025 Annual Letter Draft/Summary

- On Selling Too Early: "The most difficult thing is that you buy an incredible business, you sell it, and it keeps going. I'm hoping to get better at avoiding that." — Source: Chai with Pabrai Interview

- On Counter-Cyclical Positions: "Credit Acceptance has made the greatest strides when other lenders are forced to scale back." — Source: RV Capital 2022 Annual Letter

- On Financial Infrastructure: "I view companies like Interactive Brokers as technology platforms disguised as brokerages." — Source: RV Capital 2024 Annual Letter

- On Cash Levels: "I rarely hold significant cash. I believe the best use of capital is to be fully invested in our best ideas." — Source: RV Capital 2015 Annual Letter

Part 6: Learning & Mistakes

- On Mistakes of Omission: "The greatest cost to an investor isn't a stock that goes to zero, but the great business you failed to buy." — Source: RV Capital 2014 Annual Letter

- On the Failing of Value Investing: "The greatest failing of value investing lies in the stocks it persuades you NOT to buy!" — Source: RV Capital 2014 Annual Letter

- On Admitting Debt Mistakes: "I underestimated the financial leverage at Carvana. I hate debt and seek to avoid it." — Source: RV Capital 2022 Annual Letter

- On Iterative Learning: "The way I learn to invest is by looking at past investments and figuring out why they did well or less well." — Source: Good Investing Podcast Interview

- On Thinking for Yourself: "The best students are those who can't help thinking for themselves and aren't waiting to be told what to do." — Source: RV Capital 2014 Letter to Emerging Managers

- On Circle of Competence: "I am permanently trying to expand the edges of my circle of competence to encompass new companies and countries." — Source: RV Capital 2017 Annual Letter

- On Transparency as a Tool: "Being open about my mistakes helps me process them and ensures I don't repeat them." — Source: MicroCapClub 2014 Interview

- On Early Lessons: "In my early years, I was too focused on cheapness and not enough on quality. That was a painful but necessary evolution." — Source: RV Capital 2010 Annual Letter

- On the Value of Experience: "Every time you make an investment, you're learning something from it. That flows into future decisions." — Source: Investing City Podcast #56

Part 7: The Investment Process & Practice

- On the 'Business Owner' Mantra: "Invest like an owner in businesses run by an engaged owner with the capital of investors who think like owners." — Source: RV Capital Website Homepage

- On Engelberg: "The annual gathering in Engelberg is about building a community of like-minded partners, not just reporting numbers." — Source: RV Capital 2023 Half-Year Letter

- On the Submarine Rule: "Nobody wants an asshole in a submarine. In a small community, trust and character are everything." — Source: RV Capital 2021 Annual Gathering Commentary

- On Postcards: "Writing postcards from my discovery trips helps me share the visceral reality of businesses on the ground." — Source: RV Capital Postcard Series

- On China: "One should not let news noise distract from the rapid innovation and quality of Chinese owner-managed companies." — Source: RV Capital 2021 China Discovery Trip Postcard

- On Discovery Trips: "A discovery trip is not about finding a stock to buy tomorrow, but about expanding one's worldview." — Source: RV Capital 2023 Kenya Postcard

- On Guidance Skepticism: "I'm personally not a fan of guidance. If it was up to me, I would advise all my companies not to provide it." — Source: RV Capital 2022 Annual Gathering Q&A

- On Deep Research: "I spend most of my time reading annual reports and transcripts. There are no shortcuts to understanding a business." — Source: RV Capital 2011 Annual Letter

- On CEO Communications: "I look for annual letters that are candid and written for owners, not for analysts." — Source: RV Capital 2012 Annual Letter

Part 8: Advice for Emerging Managers & Investors

- On Fund Structure: "Get the structure of your business right on Day 1. On Day 2 it’s too late." — Source: RV Capital 2014 Letter to Emerging Managers

- On Marketing: "Don’t waste time marketing. Focus on generating a great track record, and the right people will find you." — Source: RV Capital 2022 Half-Year Letter

- On Fund Moats: "Analyze your own fund like you would a business you invest in. You want to create a moat around your own decision-making." — Source: MicroCapClub 2014 Interview

- On Operational Costs: "Keep costs ultra-low. It’s hard to be patient when you have an enormous amount of fixed costs." — Source: RV Capital 2014 Letter to Emerging Managers

- On Investor Alignment: "Seek great partners who provide encouragement and challenge you, rather than just capital." — Source: RV Capital 2014 Letter

- On Excellence: "True differentiation is rarely a function of well-roundedness; it is typically a function of lopsidedness." — Source: RV Capital 2022 Half-Year Letter

- On QUIRKY Funds: "Amazing results come from aiming high, ignoring conventional wisdom, and being content being quirky." — Source: EmergingManagers.org Interview

- On Proving the Process: "I advise young investors to prove their process with their own capital first before asking others for theirs." — Source: Economic Times Interview

- On the Long Game: "The ultimate goal is for the fund to outlive its founder. That requires building systems and culture from the start." — Source: RV Capital 2024 Presentation