As the editor of FT Alphaville and author of Trillions, financial journalist Robin Wigglesworth chronicles how index funds grew from an academic joke into the dominant force in global markets. His work focuses on the mechanics of market plumbing and the uncomfortable reality that simple rules usually beat professional stock-pickers.

Part 1: The Core Logic of Indexing

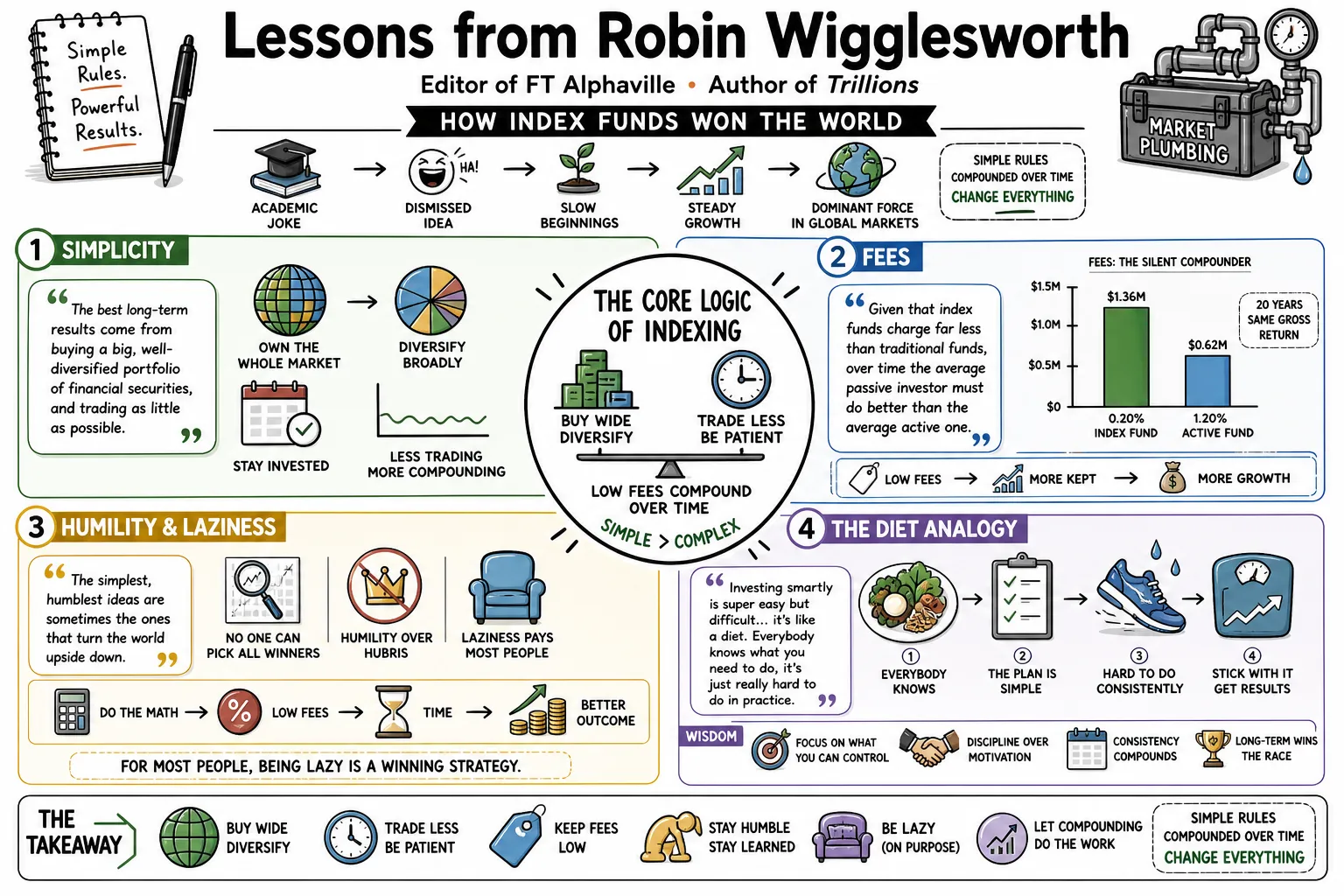

- On Simplicity: "The best long-term results come from buying a big, well-diversified portfolio of financial securities, and trading as little as possible." — Source: [Goodreads]

- On Fees: "Given that index funds charge far less than traditional funds, over time the average passive investor must do better than the average active one." — Source: [Goodreads]

- On Humility in Investing: "The simplest, humblest ideas are sometimes the ones that turn the world upside down." — Source: [Robin Wigglesworth]

- On Being Lazy: For most people, it generally pays to be lazy and choose a cheap passive fund, as the math of compounding low fees is nearly impossible for active management to beat over the long run. — Source: [YouTube]

- On The Diet Analogy: "Investing smartly is super easy but difficult... it’s like a diet. Everybody knows what you need to do, it’s just really hard to do in practice." — Source: [The Bull Podcast]

- On Managing Expectations: "People don’t pull money out of a fund when it does what it says on the tin. If the market drops 20%, the index fund is down 20%—it’s just done its job." — Source: [The Bull Podcast]

- On Emotional Resilience: We are equipped to deal with bad news when we’ve been warned about it beforehand, which is why an index tracking its benchmark downward rarely triggers mass panic among its investors. — Source: [The Bull Podcast]

- On The North Dakota Hero: "My investing hero is this one dude who manages a North Dakota pension plan. His main job is whenever somebody from Wall Street calls him up and pitches him something, he listens politely, says 'no thank you,' and hangs up." — Source: [The Bull Podcast]

- On The Profound Shift: "You may not think that the era of the index fund matters to you, but it does in countless ways that we are only starting to fathom." — Source: [MoneyWeek]

- On Reshaping Capitalism: The index fund is one of the most profound forces to rip through the finance industry in history and it could ultimately help reshape capitalism itself. — Source: [MoneyWeek]

Part 2: The End of Active Management in Drag

- On Closet Indexers: "A lot of, frankly, active funds were just passive funds in drag." — Source: [MoneyWeek]

- On The Squeeze: "Mediocre fund managers are simply being gradually squeezed out of the industry." — Source: [Goodreads]

- On Wall Street Fees: "When trillions of dollars are managed by Wall Streeters charging high fees, it will usually be the managers who reap outsized profits, not the clients." — Source: [SoBrief]

- On The Poker Analogy: Although financial markets are wildly dynamic, poker provides a compelling metaphor for why markets appear to be becoming harder to beat even as the tide of passive investing continues to rise. — Source: [Goodreads]

- On The Past: "The old days of 'have a hunch, buy a bunch, go to lunch' are long gone." — Source: [Goodreads]

- On Value Creation: If trillions of dollars are managed by high-fee Wall Street managers, the system fundamentally enriches the managers rather than generating excess returns for their clients. — Source: [SoBrief]

- On The Survival of the Fittest: Passive investing has driven out mediocre active managers by making it painfully obvious who is actually delivering alpha and who is just hugging a benchmark. — Source: [YouTube]

- On Garbage Products: The financial industry frequently markets complex, expensive, or subpar strategies under the guise of passive or rules-based investing just to justify fees. — Source: [ETF Stream]

- On Sticking It to the Industry: "It takes a lot of guts and stubbornness and bloody-mindedness to essentially stick two fingers up against your own industry and say all the stuff you’re doing is useless." — Source: [Afford Anything]

- On Overpaying: In the history of active management, investors have consistently paid hedge fund fees for index-fund performance, a model that the passive revolution is systematically dismantling. — Source: [MoneyWeek]

Part 3: The Big Three and Concentrated Power

- On Unprecedented Scale: "Over the past decade, about 80 cents of every dollar that has gone into the US investment industry has ended up at Vanguard, State Street, and BlackRock." — Source: [Goodreads]

- On Voting Control: "At some point, they will control the majority of the votes of every major company in the US and globally. This will be one of the defining battlegrounds for index funds and ETFs in the coming decade." — Source: [Goodreads]

- On Index Providers: "The rise of passive investing has given significant power to index providers. These companies determine which securities are included in their benchmarks, influencing the flow of trillions of dollars." — Source: [SoBrief]

- On The Big Two: "We focus a lot on the 'Big Three'—BlackRock, State Street, and Vanguard. In reality, it’s just a 'Big Two' because BlackRock and Vanguard are so much bigger than State Street and growing quicker." — Source: [MoneyWeek]

- On The BlackRock-Barclays Deal: "It is certainly by far the most successful deal in the history of investment management and arguably the most successful M&A deal in the history of business because it has transformed BlackRock." — Source: [Goodreads]

- On Larry Fink's Strategy: Fink has his detractors, but he is arguably the most strategically brilliant person in investment management due to his ability to spot trends and jump on them faster than peers. — Source: [Goodreads]

- On Inevitable Consolidation: "The scale nature of the index industry means the big will naturally get bigger and barring any unforeseen regulatory intervention, BlackRock and Vanguard are going to become even more titanic than they are today." — Source: [Goodreads]

- On Corporate Governance: The rise of passive ownership raises deep questions about corporate governance, particularly whether index fund giants are engaged enough to prevent corporate slough. — Source: [YouTube]

- On Systemic Risk: The concentration of ownership among just a few colossal asset managers creates potential negative externalities that the market has not yet fully priced in or regulated against. — Source: [YouTube]

Part 4: The Vanguard Renegades

- On Unsung Heroes: While Jack Bogle is the most famous figure of the passive revolution, the intellectual heavy lifting was actually done by a broader group of renegades, including John Mac McQuown. — Source: [YouTube]

- On Initial Ridicule: Early index funds faced intense industry skepticism, perfectly captured by a 1977 Institutional Investor article that claimed indexing was an idea whose time would soon pass. — Source: [Medium]

- On The Bogle Boys: Bogle mentored a cohort of young assistants, known as the Bogle Boys, who carried his vision forward and ultimately helped construct a multi-trillion dollar passive investing empire. — Source: [FT]

- On Winning The War: "The index fund revolution had finally been won… a boon to mankind." — Source: [Medium]

- On Consumer Friendliness: Vanguard today operates as perhaps the most consumer-friendly financial institution in the world, saving retail investors billions of dollars in fees thanks to Bogle's moral commitments. — Source: [FT]

- On Bogle's Legacy: Warren Buffett correctly observed that if a statue is ever erected to honor the person who did the most for American investors, Jack Bogle is the undeniable choice. — Source: [Wikipedia]

- On Bogle's Warnings: Later in life, Jack Bogle himself warned about the very monster he created, stating he did not believe the resulting concentration of corporate voting power would serve the national interest. — Source: [Wikipedia]

- On Academic Roots: The disruption of the financial industry did not begin on Wall Street, but rather in the academic research of the 1960s and 70s by figures like Eugene Fama and Burton Malkiel. — Source: [YouTube]

- On Renegade Innovation: The invention of the index fund required a specific type of Wall Street renegade—individuals willing to embrace academic theory over the macho culture of active stock picking. — Source: [Medium]

Part 5: Inelastic Markets and Efficiency

- On The Paradox of Efficiency: "Someone has to make markets efficient, and somehow they have to be compensated for the work involved." — Source: [Goodreads]

- On Disbelieving Efficiency: "I don’t think markets are efficient. I think there are active managers that can and do over time beat the markets... but I do think it’s a lot harder than most people realize." — Source: [Top Traders Unplugged]

- On Inelastic Markets: As passive flows dominate the market, stock prices become more sensitive to inflows and outflows, creating structural upward trends that active managers struggle to correct. — Source: [YouTube]

- On The Self-Referential Market: "Rather than looking at the real economy and seeking to understand its future development, passive allocation self-referentially looks to the financial economy to inform its asset allocation choices." — Source: [Goodreads]

- On Blind Allocation: "As more and more investable money is managed without regard to research, evaluation, corporate governance, quality of management and an actual assessment of long-term prospects... what does that trend mean for capitalism?" — Source: [Goodreads]

- On Systemic Blind Spots: When capital is allocated strictly by market capitalization rather than fundamental research, the market loses the critical pricing signals that traditionally direct money to the most innovative companies. — Source: [Goodreads]

- On Unified Trades: Global stock markets increasingly move as one trade, driven heavily by index flows and mega-cap concentration in a few technological leaders. — Source: [Traders Union]

- On Breaking Things: "If 2021 was the year of 'peak stupid' in markets, is 2022 the year when everything breaks?" — Source: [Man Group]

- On The Necessity of Active Management: Even the biggest proponents of indexing must acknowledge that passive investing relies entirely on the remaining active managers to set prices; without them, the index has no brain. — Source: [Goodreads]

Part 6: Financial History as Soap Opera

- On Market Drama: "The history of financial markets has more wild plot twists, temper tantrums and triumphant comebacks than a daytime soap opera." — Source: [Financial Times]

- On The Illusion of Money: "Money’s basically just a confidence game then. It’s literally just a printed IOU on a piece of paper... that everybody hopes they won’t actually have to cash in." — Source: [Financial Times]

- On Human Folly: "Stupidity... is not something that is a resource that we run out of in humankind." — Source: [Man Group]

- On The 60/40 Obituary: "The death of the 60/40 fund—that obituary has been written a million times. I’ve probably written a hundred of them myself." — Source: [The Bull Podcast]

- On The Bond Market: Bonds are the invisible architecture of the modern world, now bigger than the stock market and rivaling even the global banking system in influence. — Source: [Robin Wigglesworth]

- On Repeating Cycles: Financial history reveals that investors consistently forget the lessons of past panics, assuming the current technological or structural paradigm has eliminated downside risk. — Source: [Financial Times]

- On Trust: At its core, the entire architecture of global finance relies not on hard assets, but on a shared, fragile hallucination of trust between counterparties. — Source: [Financial Times]

- On Narrative Economics: Markets are ultimately driven less by spreadsheets and more by the compelling narratives that investors choose to believe about the future. — Source: [Financial Times]

- On Humility vs. Hubris: The history of Wall Street is essentially a cycle of profound hubris inevitably followed by a devastating, humbling crash. — Source: [Financial Times]

Part 7: The Joy of Financial Journalism

- On Career Choices: When asked why he never left journalism to become a high-paid hedge fund manager, he replied simply that journalism is just too damn fun. — Source: [My Worst Investment Ever]

- On Being a Permanent Student: "What I love about journalism is that you’re almost paid to be a student—a permanent student. I get to learn new things from smart people all day long." — Source: [Top Traders Unplugged]

- On The Alphaville Mission: The goal of FT Alphaville is to dig deeply into anything deeply nerdy or plain delightful that reporters spot in markets, business, or the global economy. — Source: [My Worst Investment Ever]

- On Avoiding Celeb Finance: "Financial journalism can sometimes be at its worst a little bit of celebrity journalism... but for people in finance." — Source: [Top Traders Unplugged]

- On Covering the Boring: "The reason why I started covering [index funds] so much at the FT is because I felt it was under-covered in comparison to some of the more titanic hedge fund managers." — Source: [My Worst Investment Ever]

- On Sniffing Out Nonsense: A core function of financial journalism is to cut through the heavily marketed jargon of the asset management industry and expose when a complex product is just a basic idea packaged with high fees. — Source: [ETF Stream]

- On Independent Thinking: True financial journalism requires the willingness to stand outside the consensus of the City or Wall Street and point out when a widely accepted practice makes no mathematical sense. — Source: [Top Traders Unplugged]

- On Following the Plumbing: Often, the most important stories in finance are not found in the flashy stock picks, but in the mundane plumbing of the financial system, like benchmark construction and custodial banks. — Source: [My Worst Investment Ever]

- On Simplifying the Complex: The ultimate test of a financial writer is the ability to take the deeply esoteric mechanics of modern markets and translate them into a narrative that reveals their societal impact. — Source: [Robin Wigglesworth]

Part 8: Quants and the Barbell Future

- On Rules-Based Investing: "The reason I think quantitative investing is going to take over the world is that I think we're all moving towards rules-based investing." — Source: [Top Traders Unplugged]

- On The Ultimate Quant: At its core, an index fund is not a passive vehicle at all; rather, it is just a really simple, highly transparent quant fund. — Source: [Top Traders Unplugged]

- On Algorithmic Speed: "Algorithms can read thousands of quarterly financial reports in the time it takes a human to switch on their computer." — Source: [Goodreads]

- On The Barbell Future: The asset management industry is polarizing into a barbell shape: one side dominated by dirt-cheap, plain-vanilla passive funds, and the other by highly specialized, expensive active strategies. — Source: [YouTube]

- On Genuine Alpha: While genuine alpha can still be found in specialized areas like private equity or distressed debt, finding it requires skill that is exceedingly rare and almost impossible to identify in advance. — Source: [YouTube]

- On Shrinking the Middle: The traditional middle of the market—mutual funds charging one percent to lightly actively manage a portfolio of large-cap stocks—is facing functional extinction. — Source: [YouTube]

- On Technological Disruption: The transition from human stock-pickers to systematic, algorithmic trading represents an irreversible shift in the bedrock of how capital is allocated globally. — Source: [Goodreads]

- On Unforeseen Consequences: The total automation of capital allocation may ultimately create new, highly correlated systemic risks that neither humans nor algorithms have historical data to predict. — Source: [Goodreads]

- On The End of the Hunch: The era of the star manager relying on intuition and gut feeling has been permanently replaced by data science, factor analysis, and systematic rebalancing. — Source: [Goodreads]

- On Letting Winners Ride: Ultimately, regardless of whether a portfolio is managed by a human or a machine, the fundamental law of compounding remains that you cannot outsmart the markets, and you must always let your winners ride. — Source: [QuoteFancy]