Lessons from Steve Mitzenmacher

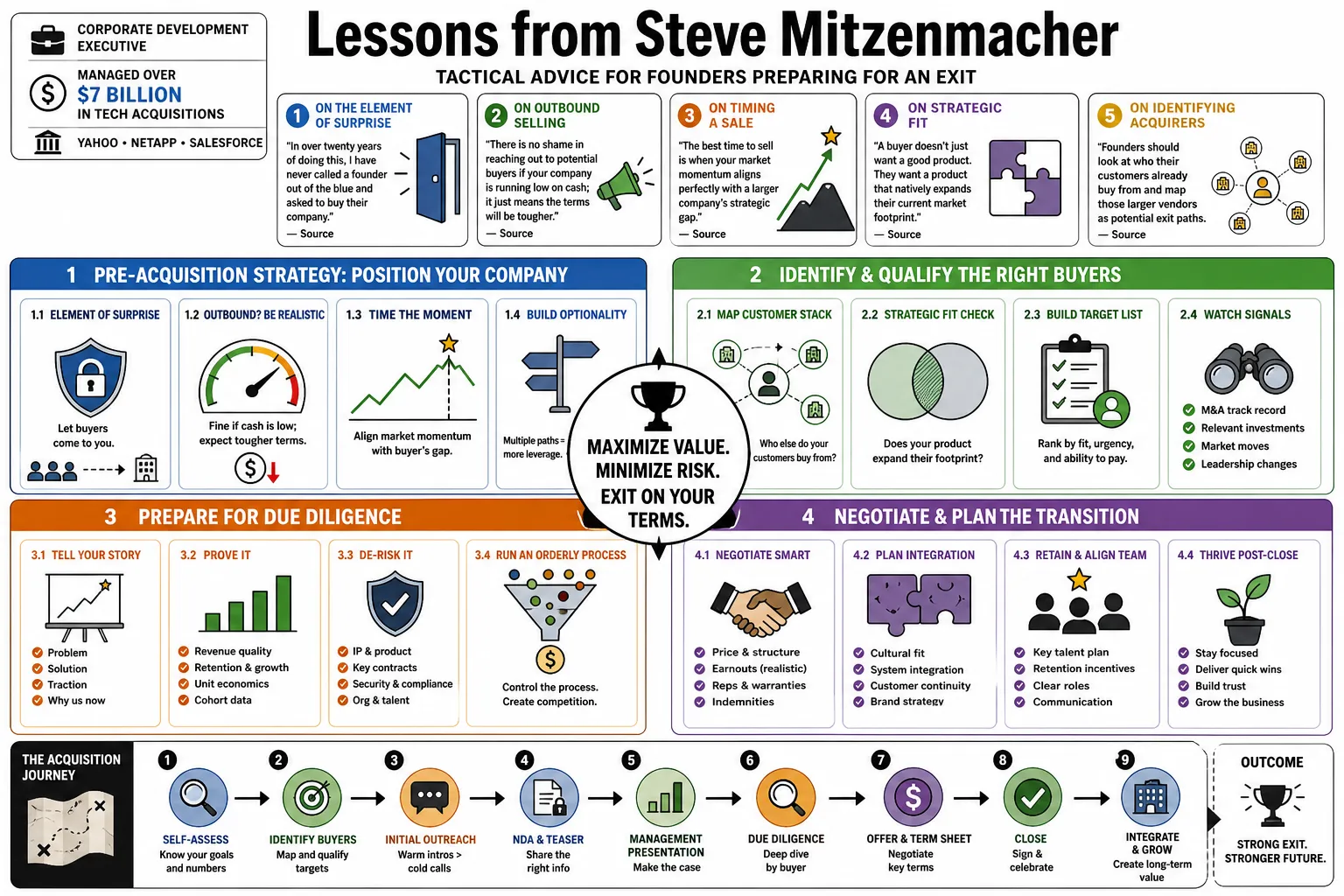

Steve Mitzenmacher is a corporate development executive who has managed over $7 billion in technology acquisitions for Yahoo, NetApp, and Salesforce. This profile outlines his tactical advice for founders preparing for an exit, detailing the actual mechanics of evaluating buyers, managing due diligence, and surviving the transition from startup to corporate subsidiary.

Part 1: The Pre-Acquisition Strategy

- On the element of surprise: "In over twenty years of doing this, I have never called a founder out of the blue and asked to buy their company." — Source: [SaaStr]

- On outbound selling: "There is no shame in reaching out to potential buyers if your company is running low on cash; it just means the terms will be tougher." — Source: [SaaStr]

- On timing a sale: "The best time to sell is when your market momentum aligns perfectly with a larger company's strategic gap." — Source: [Solganick]

- On strategic fit: "A buyer doesn't just want a good product. They want a product that natively expands their current market footprint." — Source: [Zumaya Advisors]

- On identifying acquirers: "Founders should look at who their customers already buy from and map those larger vendors as potential exit paths." — Source: [SaaStr]

- On standalone viability: "You must run the business as if it will never be acquired. Buyers smell desperation and price it accordingly." — Source: [Solganick]

- On market signaling: "Publicly partnering with a corporate development team's competitors is a quick way to get them to finally return your emails." — Source: [Zumaya Advisors]

- On product overlap: "If your core feature is on an acquirer's immediate roadmap, you are in a race to sell before they build it themselves." — Source: [SaaStr]

- On early engagement: "Introduce yourself to corporate development teams a year before you actually need to raise money or sell." — Source: [Zumaya Advisors]

- On realistic outcomes: "Not every exit will be a billion-dollar transaction. Most successful M&A deals are tactical acquisitions under fifty million dollars." — Source: [Solganick]

Part 2: Building Relationships with Acquirers

- On the first meeting: "Your first conversation with a buyer should never be a pitch to sell the company. It should be a discussion about the industry." — Source: [SaaStr]

- On consistent updates: "Send corporate development leaders brief, quarterly updates on your traction. They track execution over time, not just in one meeting." — Source: [Zumaya Advisors]

- On corporate development roles: "Our job is to monitor the ecosystem constantly so that when the CEO wants to make a move, we already know exactly who to call." — Source: [SaaStr]

- On internal champions: "You need a product manager or business unit leader inside the acquiring company who is willing to fight for the deal." — Source: [Solganick]

- On authentic connections: "Skip the heavy sales pitch. Buyers appreciate intellectual honesty about where your product struggles just as much as your growth metrics." — Source: [Zumaya Advisors]

- On backchanneling: "We will always talk to our mutual customers to see if your product is actually sticky, long before we tell you we are interested." — Source: [SaaStr]

- On maintaining contact: "If a large company passes on acquiring you once, keep the relationship open. Leadership changes and strategic priorities shift." — Source: [Zumaya Advisors]

- On partnership as a stepping stone: "A successful technical integration or go-to-market partnership is the most reliable audition for an eventual acquisition." — Source: [Solganick]

- On rejecting an offer: "If you turn down a solid acquisition offer, there is less than a ten percent chance that specific company will ever come back to the table." — Source: [SaaStr]

Part 3: The Harsh Realities of Being Acquired

- On the emotional toll: "Getting acquired is an overly complex and frequently painful process that will test every member of your executive team." — Source: [SaaStr]

- On losing control: "The moment the deal closes, founders have to accept that they are no longer the ultimate decision-makers." — Source: [Zumaya Advisors]

- On process fatigue: "M&A is designed to be exhausting. The buyer has teams of people dedicated to this; the startup founder is usually trying to run the business at the same time." — Source: [SaaStr]

- On deal certainty: "Nothing is final until the wire hits the bank. Deals fall apart at the very last minute for reasons completely outside a founder's control." — Source: [Solganick]

- On employee anxiety: "The period between a leaked acquisition rumor and the actual close is the most dangerous time for employee retention." — Source: [Zumaya Advisors]

- On shifting priorities: "A larger company will often kill your favorite feature because it competes with their legacy cash cow." — Source: [SaaStr]

- On integration realities: "You might think you are joining to change how the big company operates, but mostly, they will absorb you into how they operate." — Source: [Solganick]

- On founders' timelines: "Most founders are required to stay for two to three years post-acquisition, and many find that tenure deeply frustrating." — Source: [Zumaya Advisors]

- On cultural clashes: "Startups move fast because they have to. Big companies move slow because they are protecting an existing revenue base." — Source: [SaaStr]

- On resource allocation: "Post-close, you will suddenly find yourself fighting for engineering resources with internal teams you didn't even know existed." — Source: [Solganick]

Part 4: Managing Due Diligence

- On basic hygiene: "Keep your cap table, employment agreements, and customer contracts organized from day one. Sloppy records destroy deal momentum." — Source: [SaaStr]

- On the data room: "A well-structured data room dramatically reduces friction and shows the acquirer that your management team is mature." — Source: [Solganick]

- On technical debt: "Engineering diligence will always uncover the shortcuts you took to get to market. Be upfront about them before the audit begins." — Source: [Zumaya Advisors]

- On customer concentration: "If a massive percentage of your revenue comes from two clients, buyers will view that as a severe vulnerability during diligence." — Source: [SaaStr]

- On legal surprises: "Pending litigation or poorly documented intellectual property assignments are the quickest ways to kill a term sheet." — Source: [Solganick]

- On open source software: "Acquirers are terrified of open source compliance issues. A messy codebase can easily derail an acquisition." — Source: [Zumaya Advisors]

- On managing the narrative: "Never let the buyer's diligence team find a problem you haven't already disclosed and contextualized." — Source: [SaaStr]

- On diligence fatigue: "Answering hundreds of highly specific questions from corporate lawyers is grueling, but it is the only way to get the deal done." — Source: [Solganick]

- On financial modeling: "Your historical financials must tie perfectly to your SaaS metrics. Any discrepancy there signals incompetence." — Source: [Zumaya Advisors]

Part 5: Negotiation and Valuation

- On price anchors: "The first number thrown out sets the gravity for the rest of the negotiation. Understand your market worth before that happens." — Source: [SaaStr]

- On deal structure: "A high top-line valuation means nothing if the earn-outs are impossible to hit and the escrow holdbacks are massive." — Source: [Solganick]

- On leverage: "The only real leverage a founder has in an M&A negotiation is a credible alternative, whether that is another buyer or a fresh round of funding." — Source: [Zumaya Advisors]

- On the cost of time: "Time is the enemy of all deals. Prolonged negotiations increase the risk of macroeconomic shifts or internal buyer changes killing the transaction." — Source: [SaaStr]

- On negotiating with BigCo: "You are negotiating against people who buy companies for a living. Hire experienced advisors to level the playing field." — Source: [Solganick]

- On non-competes: "Founders should expect rigorous non-compete clauses. The buyer is paying to ensure you don't immediately build a competitor." — Source: [Zumaya Advisors]

- On walking away: "You must be genuinely willing to walk away from the table, and the buyer has to believe you will actually do it." — Source: [SaaStr]

- On retention pools: "Carve out a specific financial pool to retain your key engineers. Without them, the buyer loses the value of the acquisition." — Source: [Solganick]

- On board alignment: "Before entering deep negotiations, ensure your investors are completely aligned on the minimum acceptable price." — Source: [Zumaya Advisors]

Part 6: Navigating the LOI and Deal Mechanics

- On the letter of intent: "The LOI is just a roadmap. The actual binding agreements will contain pages of aggressive protective provisions for the buyer." — Source: [SaaStr]

- On exclusivity: "Signing an exclusivity agreement heavily shifts power to the buyer. You can no longer use other offers to drive the price up." — Source: [Solganick]

- On working capital: "The working capital adjustment is often where buyers quietly claw back money right before the close. Pay close attention to the formula." — Source: [Zumaya Advisors]

- On reps and warranties: "Founders often underestimate how much personal liability they might retain through the representations and warranties in the purchase agreement." — Source: [SaaStr]

- On closing conditions: "Minimize the number of closing conditions in the definitive agreement. Every condition is a potential exit hatch for a nervous buyer." — Source: [Solganick]

- On communication blackouts: "During the LOI phase, strict confidentiality is mandatory. A leaked deal can cause the acquirer to walk away immediately." — Source: [Zumaya Advisors]

- On legal counsel: "Never use your general startup lawyer for an M&A transaction. You need a specialist who understands standard market terms." — Source: [SaaStr]

- On the escrow account: "Expect ten to twenty percent of the purchase price to be locked in escrow for a year to cover any undisclosed liabilities." — Source: [Solganick]

- On closing night: "The actual closing is usually just a stressful series of wire transfers and signature pages, not a celebration." — Source: [Zumaya Advisors]

- On managing the transition: "Even after the ink dries, you have to immediately shift into leading your team through the shock of the announcement." — Source: [SaaStr]

Part 7: Post-Acquisition Integration

- On the first hundred days: "The success or failure of an acquisition is almost always determined by how well the teams integrate in the first hundred days." — Source: [Solganick]

- On keeping promises: "If the buyer promised your team autonomy, hold their feet to the fire early on, or you will quickly become just another department." — Source: [Zumaya Advisors]

- On migrating systems: "Integrating IT, HR, and finance systems is the most boring but necessary part of making the combined company function." — Source: [SaaStr]

- On brand equity: "A smart acquirer knows when to keep the acquired brand alive and when to fold it quietly into their main product suite." — Source: [Solganick]

- On sales enablement: "If you don't teach the massive parent sales team how to actually sell your product, the acquisition will fail to generate revenue." — Source: [Zumaya Advisors]

- On culture shock: "Your team is used to Slack and fast decisions; the new company operates on scheduled meetings and committee approvals." — Source: [SaaStr]

- On protecting top talent: "Large organizations will try to reassign your best engineers. You have to aggressively block those transfers to maintain momentum." — Source: [Solganick]

- On measuring success: "Post-close success is rarely about the tech. It is about whether the acquired product successfully cross-sells into the existing customer base." — Source: [Zumaya Advisors]

- On founder integration: "Founders who try to act like rogue mavericks inside a Fortune 500 company rarely last their full earn-out period." — Source: [SaaStr]

Part 8: The Role of Corporate Development

- On the mandate: "Corporate development exists to buy time. We acquire companies because it is faster than building the capability from scratch." — Source: [Solganick]

- On internal politics: "Half of my job as an acquirer is convincing our internal engineering leaders that they should not just build it themselves." — Source: [SaaStr]

- On tracking targets: "We maintain spreadsheets of hundreds of companies, tracking their funding rounds and executive changes for years before making a move." — Source: [Zumaya Advisors]

- On walking away: "A good corporate development executive knows how to kill a bad deal even after months of work have gone into it." — Source: [Solganick]

- On valuation discipline: "We will pay a premium for a perfect strategic fit, but we will not overpay just to win a bidding war." — Source: [SaaStr]

- On post-mortem reviews: "The best M&A teams rigorously review their past acquisitions to understand why certain deals failed to hit their targets." — Source: [Zumaya Advisors]

- On competitive defensive buys: "Sometimes an acquisition is purely defensive—buying a company just to make sure a primary competitor doesn't get them." — Source: [Solganick]

- On market mapping: "You have to deeply understand the entire vendor landscape before you can confidently recommend buying a specific player within it." — Source: [Zumaya Advisors]

- On the long game: "Corporate development is a relationship business. How you treat founders during a failed negotiation dictates your reputation in the market." — Source: [SaaStr]